年化超13%、Apyxは「ビットコインのキラーアプリケーション」をオンチェーンに移行中

- 核心見解:Strategyが発行するビットコインクレジット商品STRCを基盤に、新プロジェクトApyxはオンチェーン金融アーキテクチャを通じてSTRCの高利回りをDeFiに取り込み、利回り11%超、安定性とコンポーザビリティを兼ね備えた利付きステーブルコインapxUSD/apyUSDを構築。現在、最も急成長しているステーブルコインプロトコルの一つとなっている。

- 重要要素:

- STRCはStrategyが発行する優先株式で、利回りはビットコインの長期的な上昇期待に基づき12.3%超、発行規模は既に104億ドルを突破。

- Apyxはデュアルトークンモデルを導入:apxUSD(1ドルにペッグ、取引用)とapyUSD(利回りを生む媒体、現在のAPY約11%)。中核的な利回りはSTRCの配当に由来。

- ApyxはMorpho、Curve、Pendleなどの主要プロトコルと統合し、利回りの分割と組み合わせにより、ユーザーはレバレッジやイールドファーミングなどの複雑な操作を実行可能にし、資金効率を向上。

- ApyxのポイントプログラムはSeason 1(終了済み、トークン5%を割り当て)とSeason 2(10月11日まで継続、トークン6%を割り当て)に分かれ、TGEおよびエアドロップは10月13日に予定されており、ユーザーは明確な見通しを持てる。

- 競合のSaturnと比較して、ApyxはTVL規模(50億ドルに到達)、利回り(約2%高い)、利回り停止リスクの不在、そして明確なTGE日程において優位性を持つ。

- リスクは、原資産の信用リスク(Strategyおよびビットコイン市場への依存)とDeFi複合リスク(スマートコントラクトの脆弱性、流動性危機など)に存在する。

Original | Odaily Planet Daily (@OdailyChina)

Author | Liao Liao

The cryptocurrency market, especially the DeFi sector, is constantly seeking underlying assets that offer stability, high liquidity, and high yields. As yields on traditional Real World Assets (RWA), such as US Treasuries, have stabilized, the DeFi market's thirst for high-yield yield-bearing assets has sparked a new paradigm shift. Against this backdrop, stablecoin projects based on STRC are rising at a remarkable pace.

Stablecoins, the cornerstone of the crypto world, have evolved from fiat-collateralized types (like USDT, USDC), to over-collateralized crypto assets (like USDS), to algorithmic stablecoins (like the collapsed UST), and more recently, basis-trading stablecoins (like USDe).

However, **the current market pain point is that stablecoin yields below 10%, or even 5%, can no longer meet the risk premium demands of on-chain capital, while excessively high algorithmic yields often come with systemic risks like 'death spirals.'**

STRC-driven stablecoin projects have emerged at the right time to fill this gap. **Judging by TVL growth rate, on-chain capital flows, and community discussion热度, building stablecoins based on STRC has become one of the most closely watched niche sectors in the current DeFi market.**

Especially with the support of yield protocols like Pendle and Morpho, these products have evolved beyond simple 'stablecoins' into a new asset form that combines stability, yield potential, and financial composability.

What is STRC?

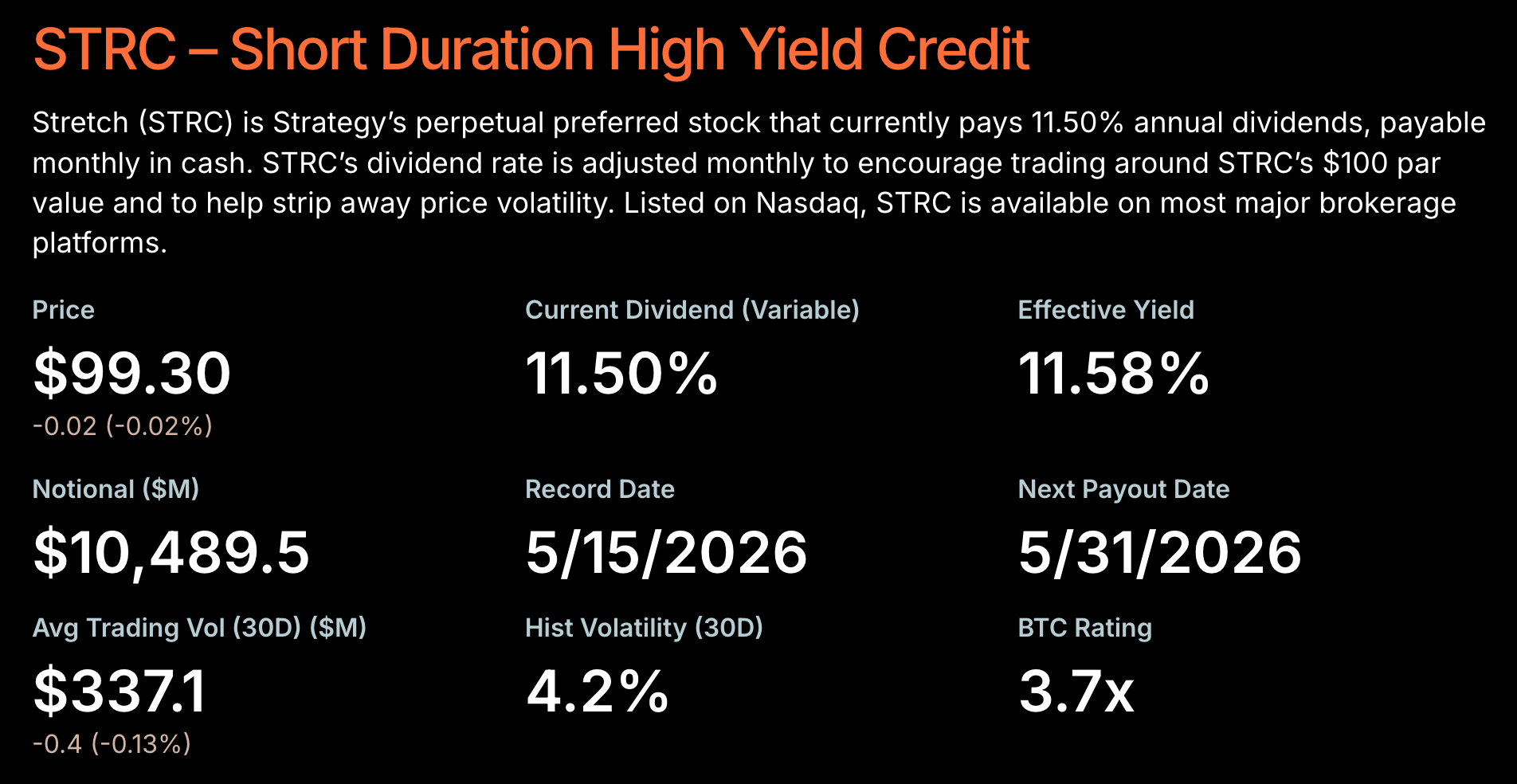

**STRC refers to a 'Bitcoin credit instrument' launched by Strategy, a Bitcoin treasury company.**

Odaily note: For a detailed analysis of STRC, refer to: A Comprehensive Guide to STRC: Strategy's New Magic Trick for Raising Funds and Buying Bitcoin.

Simply put, Strategy raises funds from the market by issuing STRC and uses the proceeds to continuously purchase Bitcoin. STRC holders, in turn, receive a floating interest yield of over 12.3%, paid monthly. Unlike traditional bonds, STRC is preferred stock, not debt, and therefore has no fixed maturity date. At the same time, its dividend rights are superior to common stock (MSTR), giving it a strong 'fixed-income-like' attribute.

**What makes STRC unique is that it effectively converts the long-term appreciation expectation of Bitcoin into a 'Digital Credit' product acceptable to traditional capital markets.**

To keep STRC stable around its $100 face value, Strategy dynamically adjusts its dividend rate – when STRC falls below face value, it increases the yield to attract capital; when STRC rises above face value, it suppresses the premium through additional issuance.

Since Strategy launched STRC, the market response has been quite positive, thanks to its relatively stable 'peg' performance (several temporary deviations have been successfully corrected) and relatively attractive yields.

**As of writing, the total issuance of STRC has exceeded $10.4 billion, accounting for over 60% of the total global preferred stock issuance in 2026.**

Earlier this month, **Strategy founder Michael Saylor stated in an interview with David Lin that digital credit products like STRC are Bitcoin's 'killer app'** (refer to: Interview with Michael Saylor: I said I would sell Bitcoin, but never as a net seller).

However, traditional STRC shares typically circulate among Wall Street hedge funds, regulated institutions, and high-net-worth accredited investors. Due to barriers such as access, compliance, and capital channels, on-chain DeFi users find it difficult to directly access this high-yield product that is sweeping traditional financial markets.

This is precisely where Apyx, the subject of this article, comes into play.

**Apyx's mission is to act as a bridge between Wall Street's digital credit instruments and on-chain DeFi legos. By employing an innovative on-chain financial architecture, it brings the excess yield opportunities of STRC on-chain, constructing a next-generation yield-bearing stablecoin that combines high liquidity, composability, and higher returns.**

Deconstructing Apyx: Potentially the Highest-Yielding Stablecoin on the Market

Unlike many stablecoin projects that rely on airdrop narratives and lack genuine income sources, Apyx's core competitiveness lies not just in its 'higher APY', but in its simultaneous possession of traditional financial capital capabilities and the composability of on-chain protocols.

Background-wise, the core supporter behind Apyx is the US-listed treasury company DeFi Development Corp. This company not only participated in Apyx's incubation and strategic investment but also provides a key bridge connecting traditional capital markets with the on-chain world.

In terms of product design, Apyx employs a dual-token model: apxUSD + apyUSD.

Among them, apxUSD is closer to a traditional stablecoin, pegged to $1, primarily serving as a medium of exchange and providing on-chain liquidity. apxUSD does not automatically accrue yield; it acts more like a highly liquid 'base dollar asset' suitable for trading, payments, lending, and other scenarios.

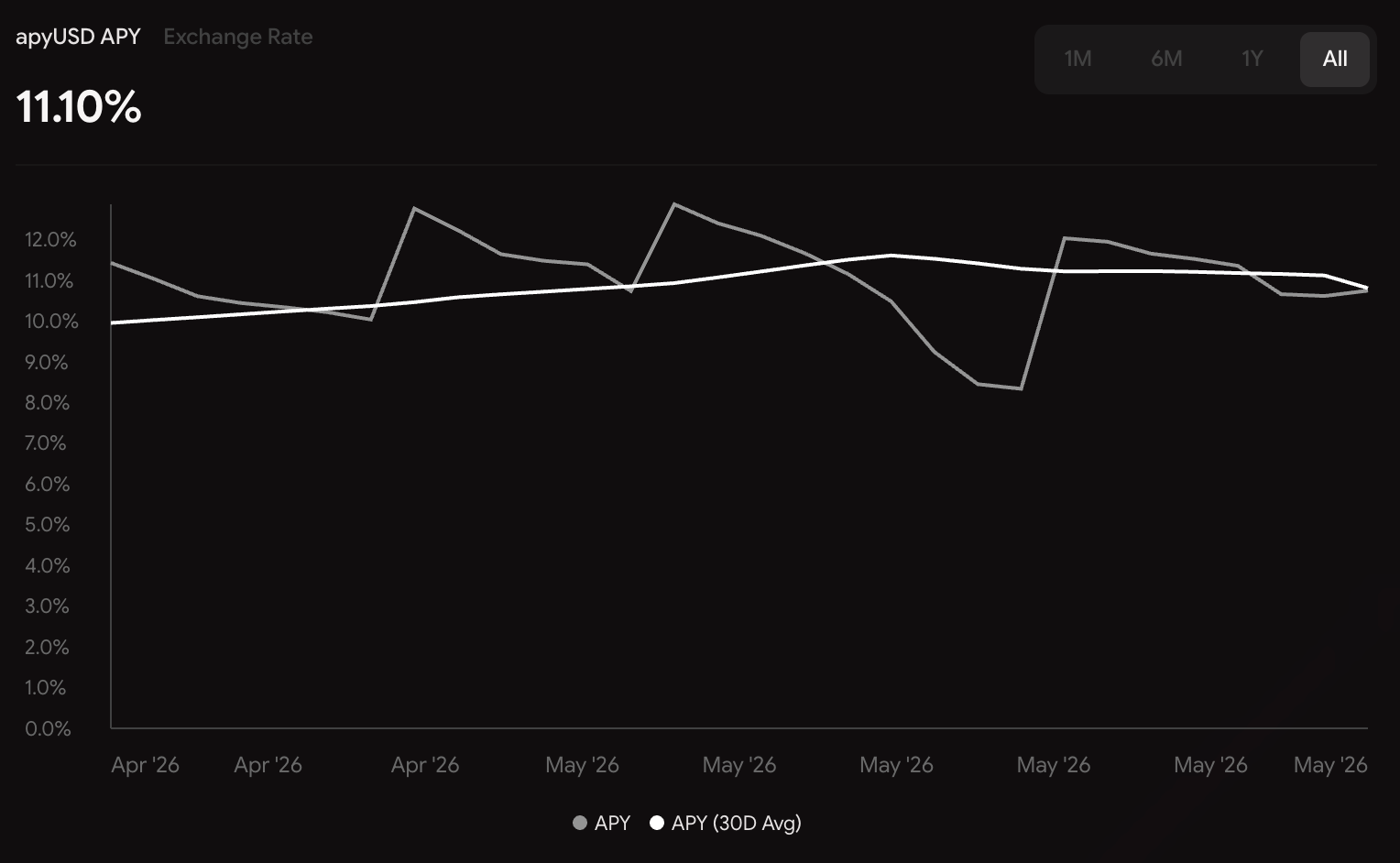

The core value of Apyx is truly embodied in apyUSD. Users can lock apxUSD to obtain apyUSD (with a 20-day unlock period). apyUSD is similar to Lido's wstETH, its price increases continuously as the underlying yield accumulates. In other words, apyUSD itself is the vehicle for yield.

Currently, **apyUSD's real-time annualized yield is approximately 11%, with an expected annualized yield exceeding 13%.** In the context of continuously declining yields for dollar stablecoins, a stablecoin asset with a genuine yield source and double-digit returns naturally becomes exceptionally attractive.

Furthermore, it's important to emphasize that **unlike many stablecoin projects that rely on token subsidies for short-term high yields, Apyx's core yield comes from STRC dividends, making its yield source more stable and sustainable.**

Defillama data shows that since its launch at the end of February this year, **the issuance scale of apxUSD has rapidly reached 502 million in less than three months, making it the 21st largest stablecoin protocol by issuance in the DeFi world.**

Of course, yield alone is not enough to sustain a stablecoin ecosystem. What truly determines a protocol's ceiling is the composability and liquidity efficiency of its assets. On this point, Apyx has clearly done extensive work – **Apyx is already deeply integrated with major protocols like Morpho, Curve, and Pendle.**

On Morpho, users can use apyUSD as collateral to borrow other assets, enabling operations that 'earn yield while releasing liquidity'. More aggressive players can even engage in loop strategies to amplify their yield exposure. Curve handles the liquidity issue. By creating trading pools with major stablecoins like USDC and USDT, Apyx ensures low slippage even during large swaps, which is crucial for a stablecoin system.

As for Pendle, it is perhaps the most explosive component of the Apyx ecosystem. Because Pendle can split yield-bearing assets into PT (Principal Token) and YT (Yield Token), apyUSD is no longer just an asset for 'holding and collecting yield'. It evolves into a tradeable, leveragable, and speculative yield product. Conservative users can lock in fixed returns via PT, while more aggressive users can amplify their bets on future yields by purchasing YT.

Precisely because of this high composability, Apyx's ecosystem expansion speed is significantly faster than many traditional stablecoin protocols.

**In a sense, Apyx is not just 'issuing a high-yield stablecoin'; it is attempting to establish a set of on-chain credit markets centered around STRC.**

Points Program and Strategies

In today's DeFi market, 'points' are no longer just simple user incentive tools but more like a way to pre-price future token rights. Especially as the market enters a new phase of liquidity competition, **a project's ability to continuously attract capital often depends on two things: whether the yield is high enough and whether the token expectations are clear enough.**

Apyx's ability to rapidly accumulate significant TVL in a short time is largely related to its current points system. According to the official plan, Apyx's points program follows a phased approach:

- Season 1 ended on May 22, 2026. The team has confirmed allocating 5% of the total token supply to early participants in this phase.

- Immediately after Season 1, Season 2 was launched and will run until October 11, continuing to release an additional 6% in token incentives.

- After Season 2 ends, Apyx will conduct its TGE and airdrop on October 13.

This rhythm is quite clever. On one hand, the end dates of each Season naturally create 'sprint windows', encouraging capital inflows before the deadline. On the other hand, the seamless transition to Season 2 avoids the common 'TVL crash after Season 1' problem seen in many projects. Most importantly, **Apyx has confirmed a specific TGE and airdrop date, giving users a much clearer interaction expectation.**

For the market, this means Apyx’s airdrop expectation is not a short-term event but more like a months-long liquidity war. From a user's perspective, the key question is 'how to earn points more efficiently'.

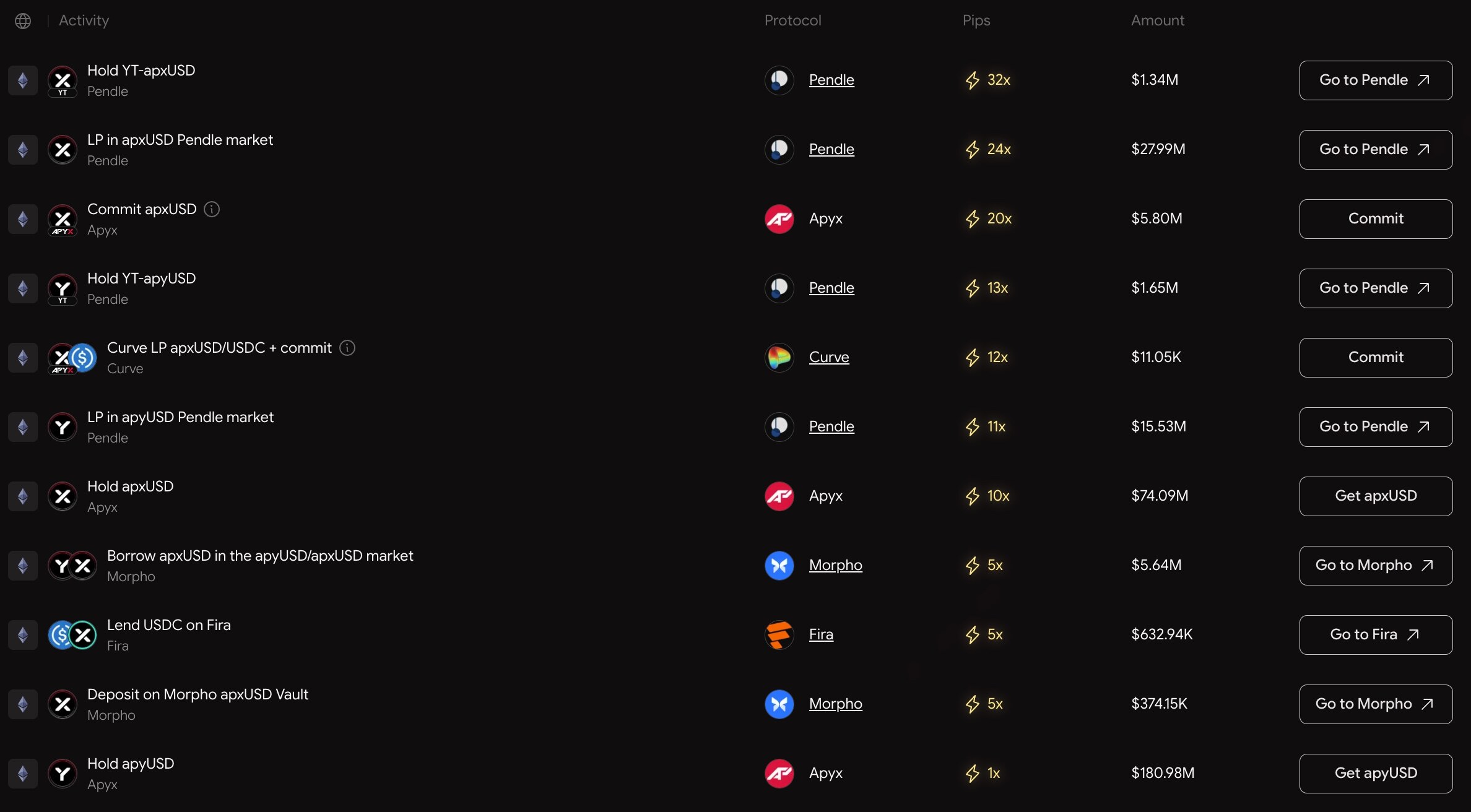

Apyx provides the point-earning efficiency for different operations on its website. **Simply put, it can be divided into 'basic mode' and 'advanced mode'.**

'Basic mode' involves simply holding apxUSD (10x points) or apyUSD (1x points). 'Advanced mode' means flexibly using the integrated protocols mentioned above, such as borrowing/lending apxUSD on Morpho (5x points) or providing LP for apxUSD on Curve (12x points). The most efficient strategy inevitably involves Pendle, where directly holding apxUSD's YT earns 32x points, and providing LP for apxUSD on Pendle gives a 24x point multiplier.

Competitive Landscape and Apyx's Advantages

As a nascent sector still in its very early stages, the STRC-driven stablecoin market currently doesn't have many truly core players. **In terms of capital scale, market attention, and ecosystem expansion speed, only two projects have really formed influence: Apyx and Saturn.** In a sense, this 'digital credit stablecoin' sector is gradually showing a dual-leader competitive landscape.

Although Saturn launched earlier, Apyx has already overtaken it in terms of data. Overall, Apyx's competitive advantages are evident in the following dimensions.

**Firstly, absolute TVL scale and underlying asset holdings advantage.** Apyx has set a clear strategic goal in its project positioning – to become the world's largest institutional holder of STRC. As of the end of April, its holdings reached $125 million (Saturn had only $50 million). Once Apyx achieves its strategic goal, it could monopolize the on-chain yield distribution rights based on Strategy's digital credit at the source. Furthermore, for stablecoins, Apyx's TVL scale advantage means deeper trading pools, lower slippage for large swaps, and more robust liquidity efficiency, safely accommodating large capital inflows and outflows.

**Secondly, higher yields with no risk of yield suspension.** For the target customer base of Apyx and Saturn, the core demand is continuous and predictable yield. Compared to Saturn's sUSDat, Apyx's apyUSD static holding yield consistently maintains an annualized advantage of around 2%. Moreover, crucially, sUSDat's design is deeply tied to the exchange rate of STRC. When STRC falls below the 'Watermark' due to ex-dividend or other reasons, yield accrual for YT-sUSDat completely pauses. Apyx does not have this problem at all.

**Thirdly, a clearer TGE expectation and no VC sell pressure.** Users in the crypto industry most dislike 'indefinite point PUA'. Compared to Saturn, Apyx has clearly disclosed its TGE date and the timing and token allocation for each Season's points activities, making users psychologically more likely to stay engaged. Additionally, Apyx's development did not involve VC funding, only a minimal amount of early investment, partly from the founding contributors themselves. This means no private round institutions can dump on retail investors before the token generation event, making the token rewards corresponding to the points more ideal.

Potential Risks and Outlook

**It must be clearly emphasized that Apyx's high yield does not mean 'risk-free'.** Essentially, Apyx is still a yield product built upon Bitcoin's credit structure, not a traditional risk-free dollar asset. Therefore, before discussing its growth potential, the risk sources behind it must be acknowledged.

**First, the credit risk of the underlying asset itself.** STRC's core logic is built on Strategy and its Bitcoin balance sheet. In other words, the market accepts STRC's yield essentially because it believes Strategy can continuously use its Bitcoin assets to maintain its credit structure and successfully complete financing, expand its balance sheet, and make interest payments.

Should extreme volatility occur in the Bitcoin market, such as a sharp crash in a short period, or a significant decline in market risk appetite for Strategy's leverage model, STRC's market pricing, liquidity, and yield structure could all be affected. While this 'systemic risk' doesn't mean the protocol will immediately collapse, it does mean Apyx's yield source is tied to the Bitcoin cycle to a certain extent.

**Second, typical DeFi composability risks.** Because Apyx is deeply integrated with protocols like Morpho, Curve, and Pendle, its ecosystem is built upon highly complex on-chain composability. The advantage of this structure is greatly enhanced capital efficiency; the cost, however, is that the system's risks become more coupled.

For example, if an underlying protocol suffers a smart contract vulnerability, liquidity crisis, or abnormal liquidation mechanism, the risk could propagate through the LP, collateral, and yield-splitting structures to the entire ecosystem. Especially as loop strategies and high-leverage plays become more common, market volatility can be further amplified.

Therefore, **Apyx is best understood as a 'medium-to-high risk, high yield' on-chain credit asset, not a replacement for traditional over-collateralized stablecoins. But it is precisely this risk stratification that gives Apyx its unique appeal in the current market environment.**

The stablecoin market today faces an increasingly obvious problem: yields are rapidly homogenizing. As US Treasury yields decline and traditional arbitrage opportunities narrow, the real yields most stablecoin protocols can offer are becoming increasingly limited. **The market needs new yield sources, and users are willing to bear a certain level of risk for higher returns.**

Over the past few years, from LSD and Restaking to Pendle's yield trading, the entire DeFi market has been validating the same point: **Users have never been averse to risk; what they truly reject is assets with an unfavorable risk-reward ratio.** The emergence of STRC just provides the market with a new 'risk vs. reward' option.

In the past few months, the continuous growth in TVL for Apyx and the entire STRC sector demonstrates that the market is voting for this narrative with real capital.