Understand the "Agentic Economy" Thesis from Circle's Founder — How the Next Decade's Economic Landscape Will Be Reshaped

- Core Thesis: In his paper "The Agentic Economy," Circle CEO Jeremy Allaire argues that AI agents and blockchain onchain economies are not parallel trends but two sides of the same coin forming the future economy. AI drives the cost of thinking and working toward zero, while blockchain drives transaction costs toward zero. Their convergence will reshape corporate structures, monetary systems, and ownership distribution.

- Key Elements:

- Corporate Deconstruction: AI agents break down internal work within companies into outsourcable skills, weakening the traditional logic of internalizing work and making the "company of one" a reality.

- Onchain Trust: The agentic economy requires an identity and accountability layer, where public blockchains are tied to real-world identity verification to ensure every autonomously acting agent has a traceable, responsible entity behind it.

- Monetary Foundation: Agents can only operate on currency that is fully backed, has final settlement, and runs on open networks (e.g., stablecoins). This enables high-frequency, micro-transactions at machine speed, avoiding the risks of traditional banking systems.

- New Credit Models: Onchain data can generate a "data flywheel," reducing underwriting costs and enabling working capital loans for AI agents. The risk of such loans is far lower than human credit due to the predictability of tasks.

- Inherent Globalism: This economic system is built on software, replacing nation-bound currency, contracts, and labor. Borderless globalization becomes the default norm, while national regulation needs to shift toward managing accountable entities.

- Value Flow: As agents purchase "outcomes" rather than "access rights," software pricing shifts from subscriptions to pay-per-unit-of-work. Value flows from the AI model layer to the agent layer that owns customers and context.

- Key Risk: The concentration of ownership is the core challenge. The share of labor income may decline, but if ownership is broadly distributed, automation can achieve shared abundance; otherwise, it will exacerbate inequality. Expanding ownership requires onchain mechanism design.

Original text from Circle Founder Jeremy Allaire

Translation|Odaily (Qin Xiaofeng) (@QinXiaofeng 888 )

Editor's Note: On July 13, Circle Founder Jeremy Allaire published a research paper titled "The Agentic Economy," exploring the convergence of AI Agents with the future economic system. Allaire stated that as AI Agents begin to undertake enterprise work and value flows natively through open, programmable networks, the Agentic Economy and the Onchain Economy will ultimately become two sides of the same economic system.

"This paper is the culmination of decades of my work building internet infrastructure and crystallizes a question I've focused on from the start: Can open software and open networks not only transform how we share information but also reshape our social, political, and economic landscape? Many of the ideas in this paper stem from two convictions I held when founding Circle. First, money can flow through open protocols just as information flows on the open internet. Second, a blockchain is a network computer: a foundational platform where autonomous software and machines can store value, exchange value, and directly coordinate economic activity without human intervention," Allaire explained his motivation for the research.

He added that these initial concepts matured over time, culminating in a deeper understanding of how finance and economic systems integrate with software and the internet. This integration, combined with the emergence of truly powerful artificial intelligence and agent systems, allowed the theory to expand: it describes not just a new form of money or a new network, but a fundamentally new mode of economic operation and its implications for humanity, labor, capital, ownership, and a new social contract. This is precisely what this treatise aims to explore.

The original paper is 89 pages long. Those interested can download the full text here: https://agenticeconomytreatise.com/treatise/index.html; Odaily has compiled a summary of thekey points. Enjoy~

——————————————

01 The Convergence and Deconstruction of the Firm

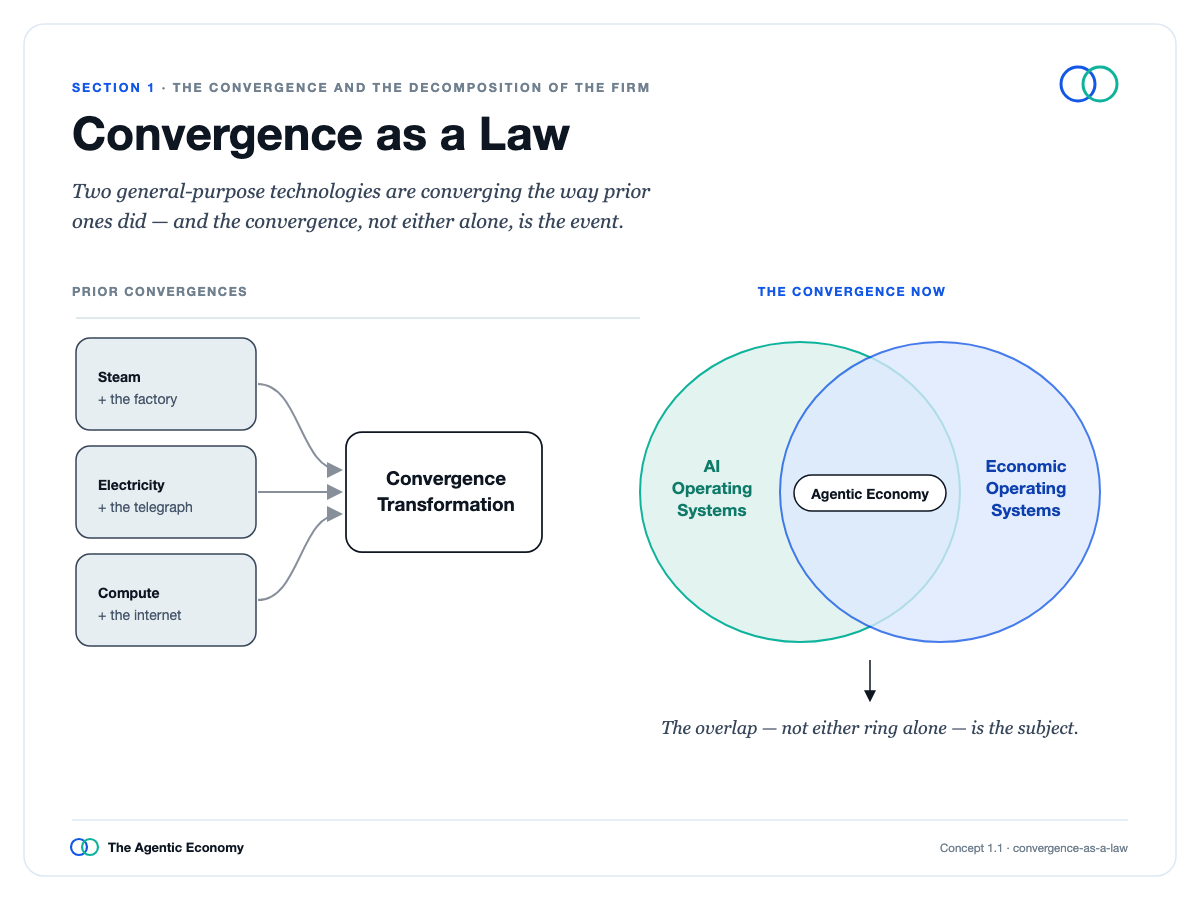

Every major shift in the internet era follows the same path: it doesn't originate from a single invention, but from several technologies maturing independently and suddenly converging. The web, mobile, cloud, and social media were all such convergences, repeating the same underlying pattern.

Law of Convergence

When capabilities converge, the cost of what was once expensive approaches zero. Once costs hit zero, the scale of that activity explodes. This happened with the web for information, mobile and social for communication, and the cloud for software.

Now, two new systems are converging, applying the same force to the two areas the internet has never fully digitized: intelligence itself and the economy itself. The first is the intelligence system, composed of AI models and the agents built upon them, driving the cost of thinking and working toward zero. The second is the economic system, composed of blockchains, where money, contracts, and coordination run as software, driving transaction costs toward zero. They empower each other, and the central thesis of this entire treatise is: These are not two parallel trends, but two sides of the same economy.

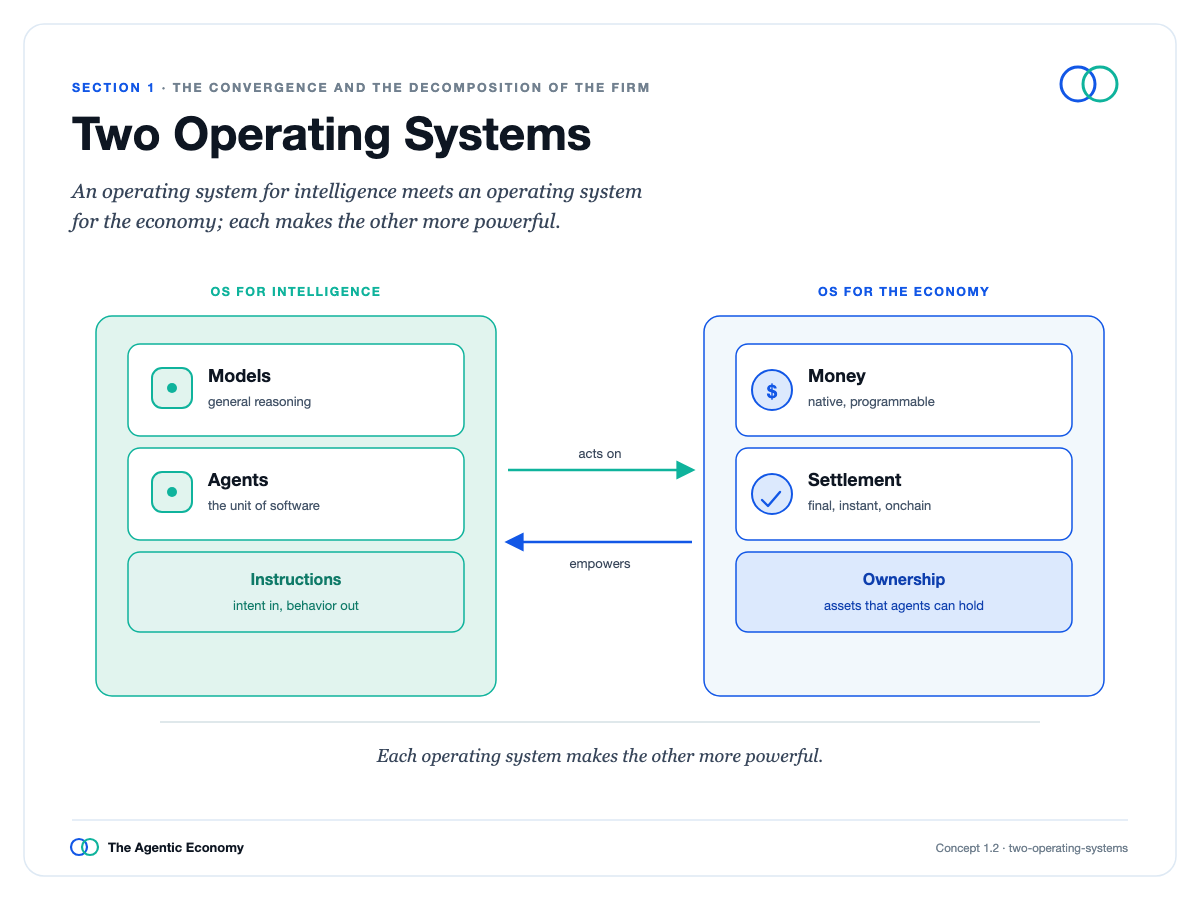

Two Operating Systems

The intelligence system is most critical because it changes the very nature of software.

You no longer program; you give instructions in natural language, and it reasons out the answer rather than following fixed steps. The basic unit is the Agent: a reasoning process to which you delegate a task. This transforms software from a program that machines execute verbatim into work you can entrust to a thinking machine. It also allows the core tasks of a firm to be decomposed and restructured into skills that agents can perform.

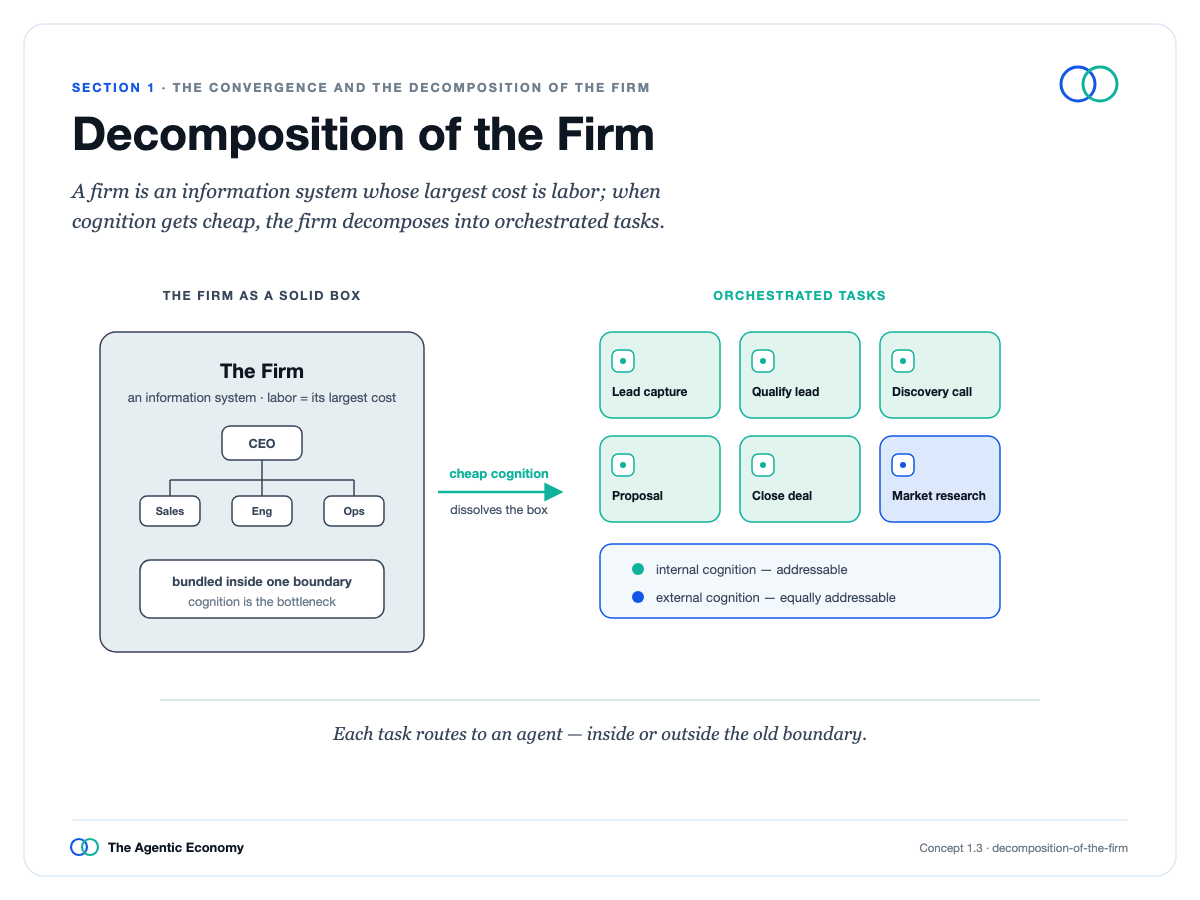

Beneath the brand and the building, a company is essentially organized thinking: product, marketing, sales, finance, legal, plus the external firms it hires. These are almost entirely human labor, which is the largest cost in the economy – precisely what cheap, powerful intelligence targets.

Decomposition of the Firm

It also upends the traditional explanation for why firms exist. Firms grow large because coordinating work externally is expensive, so they internalize it. When any non-physical work can be done by an agent you find, hire, and pay instantly, this logic weakens. A single person can accomplish what once required an entire department.

This arrives first in software and other information-intensive work, and slowest in the physical realm, awaiting breakthroughs in robotics. This is not simply about headcount reduction: one person paired with a powerful agent becomes extraordinarily productive, while judgment, relationships, and ultimate responsibility remain human. This leaves a tension to be explored further, resolved later in the treatise through ownership: even as the share of the economy paid to human labor declines, individual capability can be amplified.

Click to read Section 1: https://agenticeconomytreatise.com/treatise/section-1.html

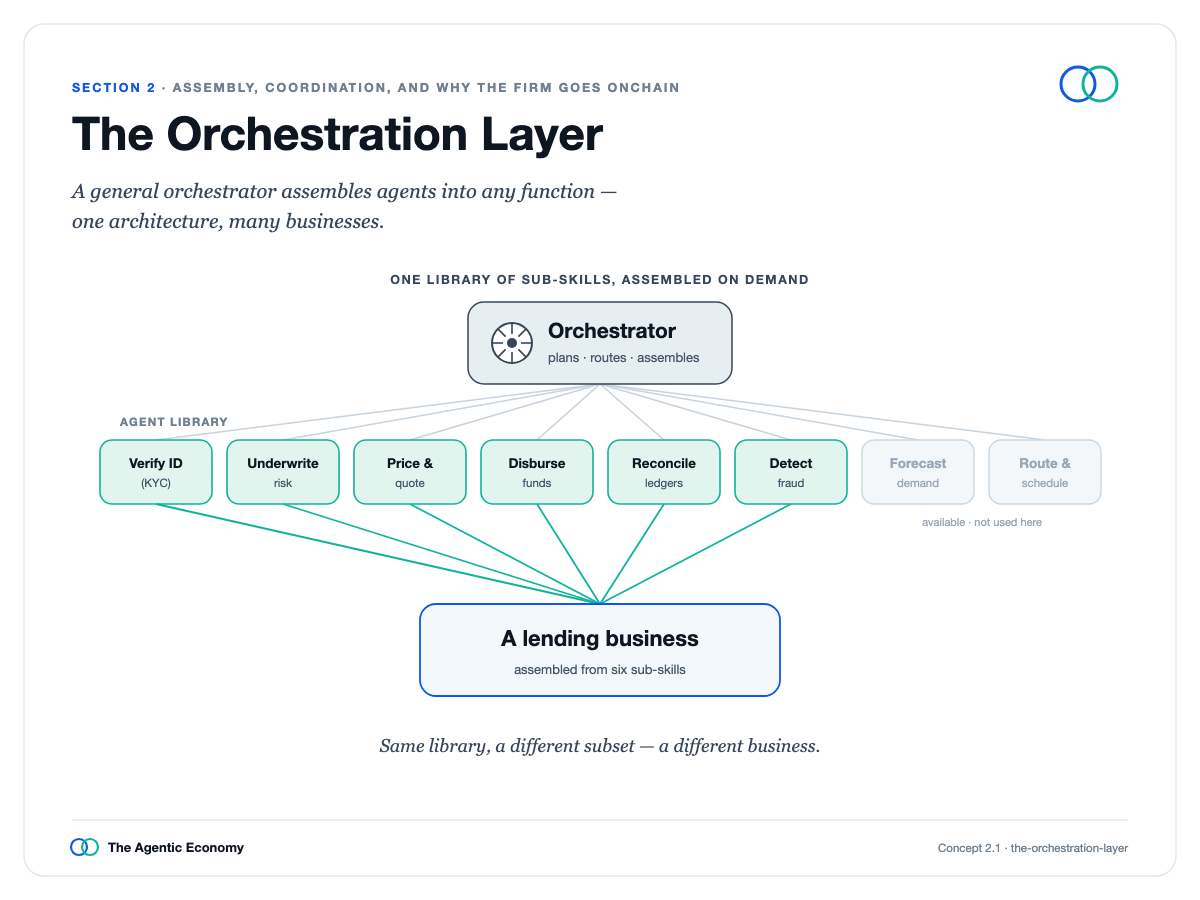

02 Assembly, Coordination, and Why Firms Go Onchain

Once a firm is decomposed into skills, the real question isn't which can be automated, but how these pieces are reassembled.

The answer is the orchestration layer: a general manager agent receives an objective, breaks it into tasks, assigns them to specialized agents, and stitches the results back together, with supporting software passing context and memory between steps. The same mechanism applies to any function, so marketing, finance, sales, and product are essentially the same machine applied to different work.

Humans don't disappear. Some remain in the loop, performing or verifying work needing human judgment. Others rise above the loop, setting goals, defining standards, monitoring quality, and deciding when the machine should stop and ask for guidance. The shift from performing work to supervising work is the true form of human oversight, and the tools for this are arriving.

Orchestration Layer

When a company defines a task clearly enough to operate it internally, it is also clear enough to be hired externally. Thus, an open agent market emerges almost as a byproduct.

This market could go two ways. It might evolve into a few large platforms selling agents like utilities, or, more likely and interestingly, into a genuine labor market of specialized agents, because deep expertise still holds value. Enduring firms will be those agents that specialize deeply in one domain.

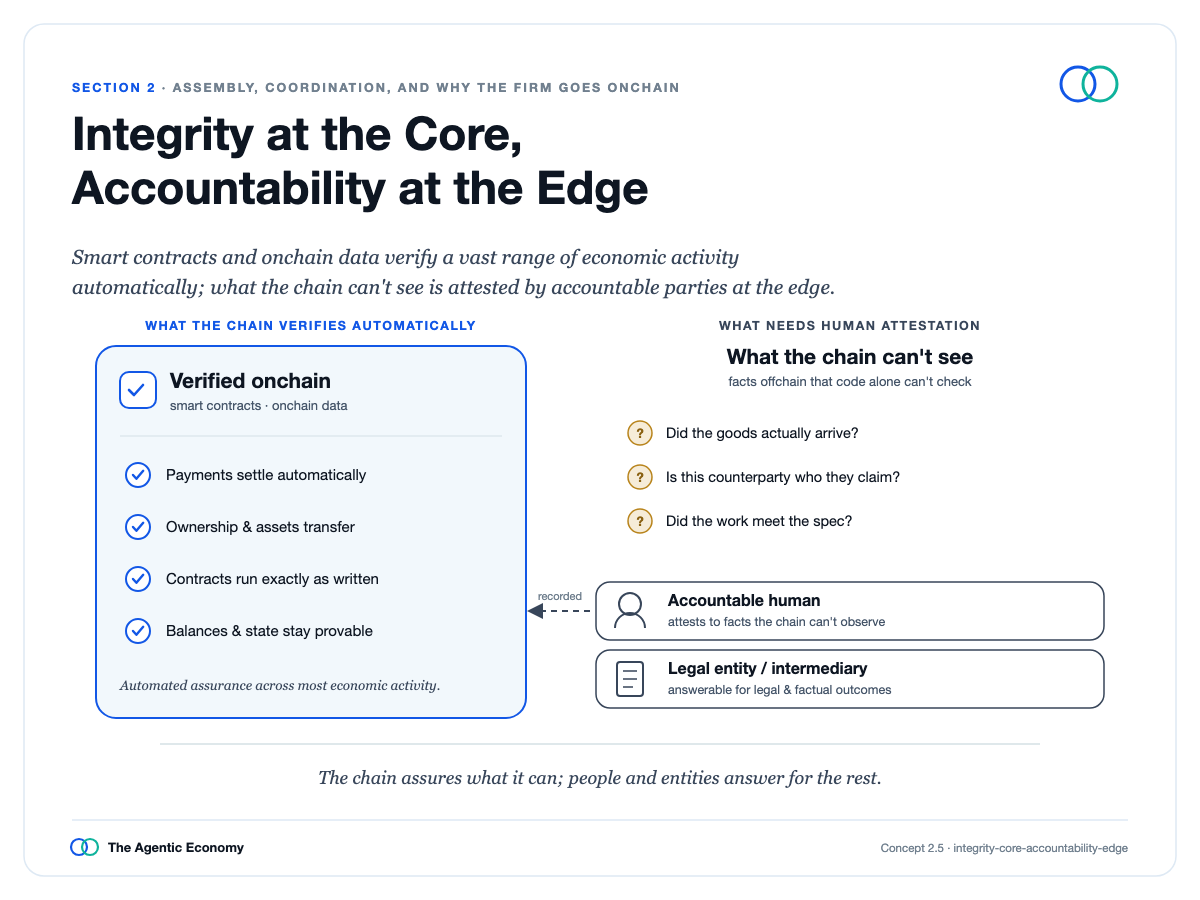

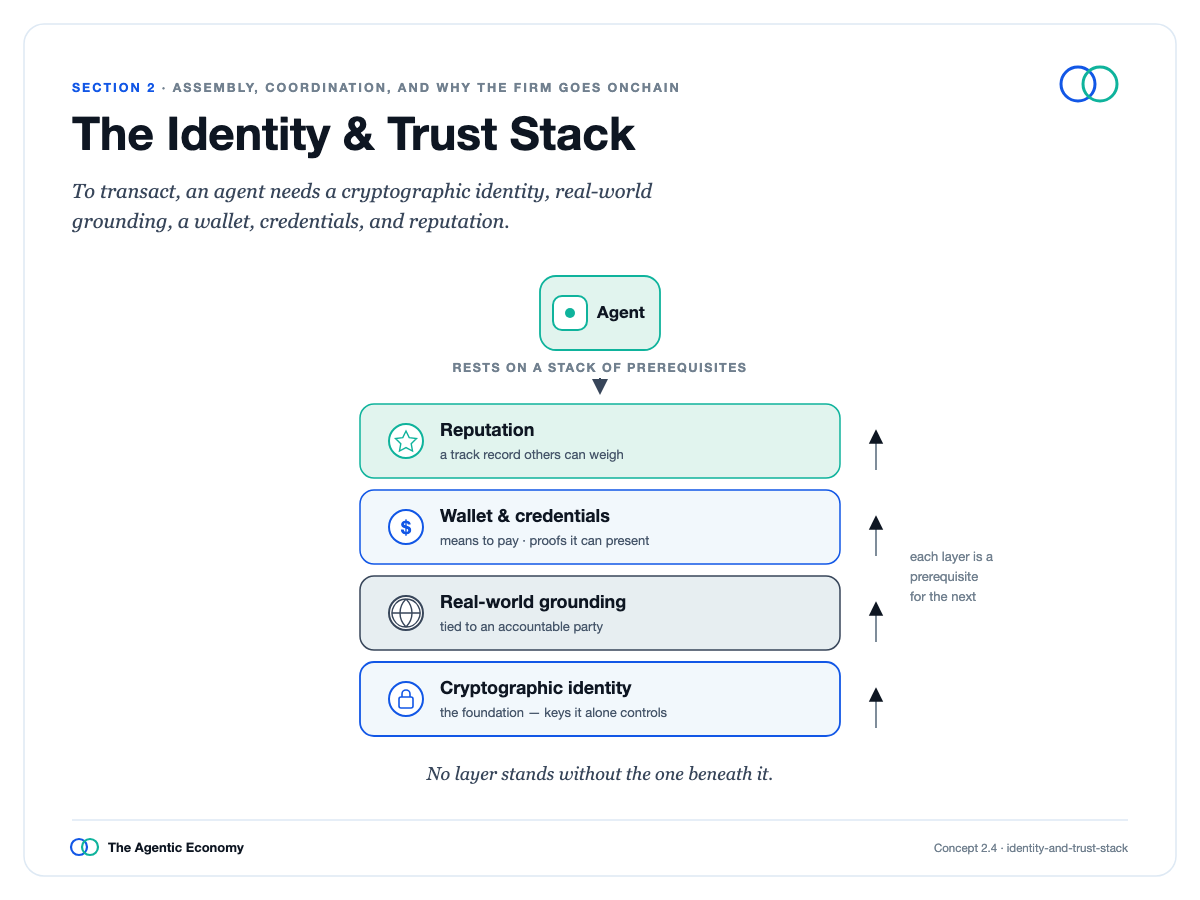

But hiring software assembled anywhere in the world requires you to trust it, and this is the problem that pushes everything onchain.

The solution is identity layering. The base layer is a public blockchain verifiable by anyone. On top sits real-world identity verification, the same verification banks already operate at scale, along with the agent's own wallets and credentials, and reputation that accumulates over time but is bound to a verified real-world creator. Together, these form a chain of accountability: Every action by an agent is traceable back to the real person or company responsible for it.

Integrity by Design, Accountability Throughout

A single company's private database cannot achieve this because trust locked inside one operator doesn't transfer. Identity rooted in a public chain and real-world verification can. Therefore, autonomy here is not anonymity. Behind an agent acting autonomously, there is always a person responsible.

Chain of Accountability

Click to read Section 2: https://agenticeconomytreatise.com/treatise/section-2.html

03 The Monetary Base: Speed, Safety, and Finality

Agents need money they can hold and transfer, operating at machine speed, for both huge and micro amounts, without needing to pause at every payment to verify the money itself is sound. The last point is key, pointing to a classic answer: Fully backed money, with final settlement, operating on an open network.

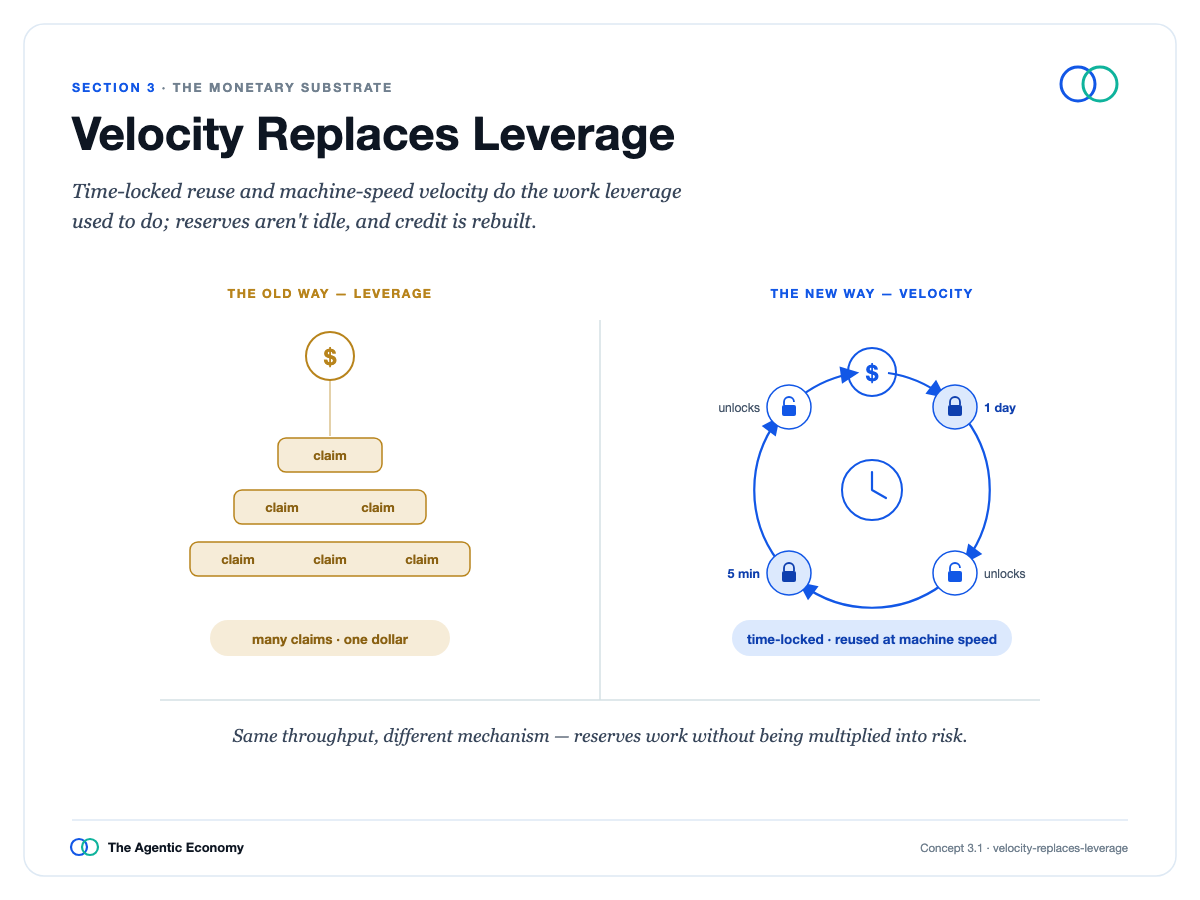

Speed Replaces Leverage

Start with speed, because it will reorganize everything else.

When transferring money costs nearly zero, settlement is instantaneous, and money can be controlled by software, the same dollar can be reused many times in a short period. Any amount is available the moment it arrives, and micropayments between agents finally become feasible. This is precisely the pattern information and software already follow on the internet, now extended to money.

Every part of the answer has its reason for existing.

A natural objection is that banks create speed by repeatedly lending out the same deposit. Would full backing kill credit? No. When money circulates fast enough, a dollar can be locked for seconds then lent out. Speed takes over the role leverage once played. Credit is rebuilt on top of the base, not abolished.

Why the Base Money Takes No Risk

Why insist the base money has no risk? Because speed makes risky money dangerous in proportion to how fast it circulates. A bank run that once took weeks can now happen in minutes. An agent settling instantly cannot stop to judge whether each dollar is sound.

Fully backed money is the only money that is worth exactly one dollar for everyone, everywhere, without relying on national safety nets that can't cover a global system. Settlement must be equally certain: Not probabilistic finality after some time, but final in one second. Settlement means settlement.

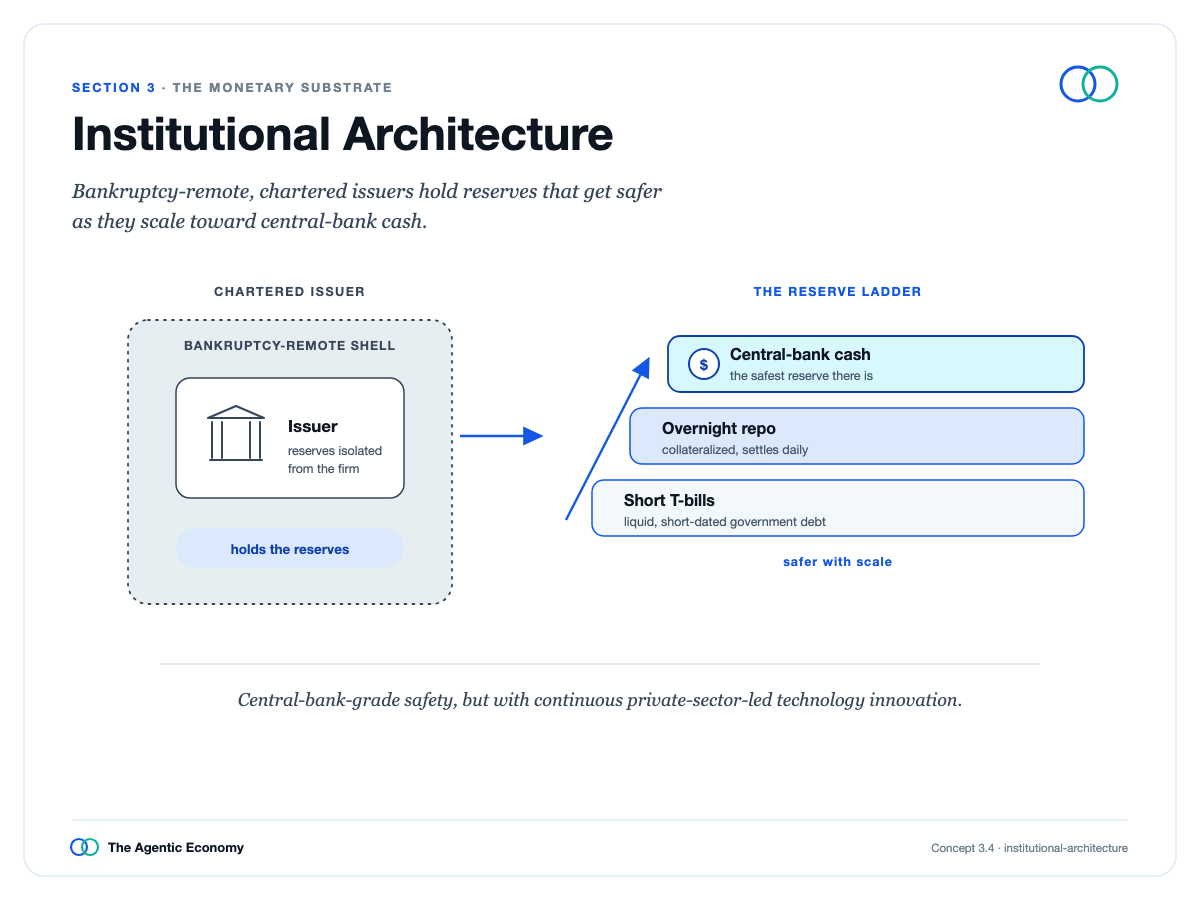

Institutional Architecture

Refunds and fraud protection still exist, but as optional layers built on top – escrow, refund pools, insurance – not embedded in the money itself. These safety nets don't activate automatically; they depend on real institutions being built: large issuers that are regulated, bankruptcy-remote, and backed by increasingly safe reserves.

One line must be clear: Holding the money yields nothing. Reserve yield goes to the issuer and flows into the ecosystem. When you seek yield, you are no longer holding money; you are lending it and taking risk. Confusing the two collapses the entire safety argument.

Click to read Section 3: https://agenticeconomytreatise.com/treatise/section-3.html

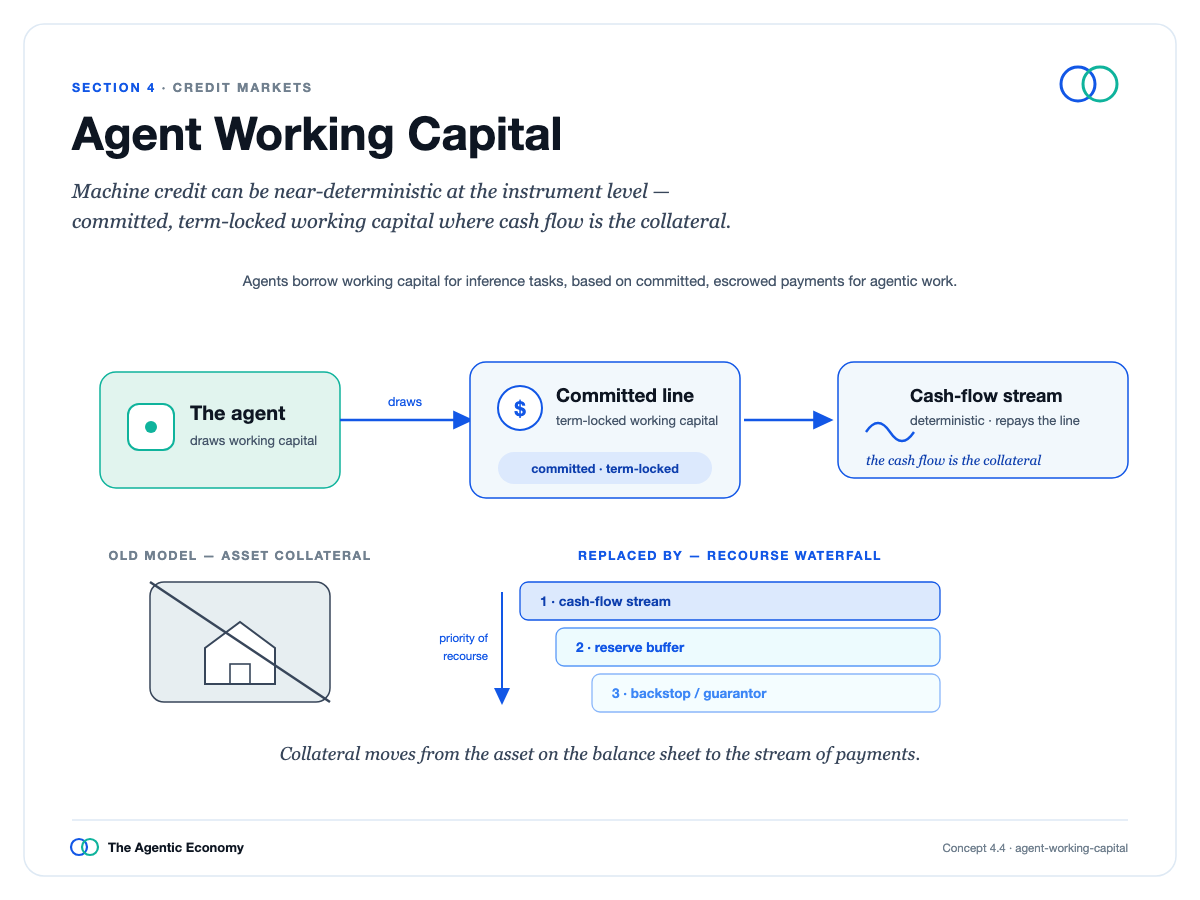

04 Credit Markets: Machine Underwriting, Agent Working Capital, and Prudential Guardrails

When the base money is fully backed, credit doesn't disappear; it moves to the other side of that line and returns stronger, reaching more people, priced more accurately, and failing more visibly than the system it replaces.

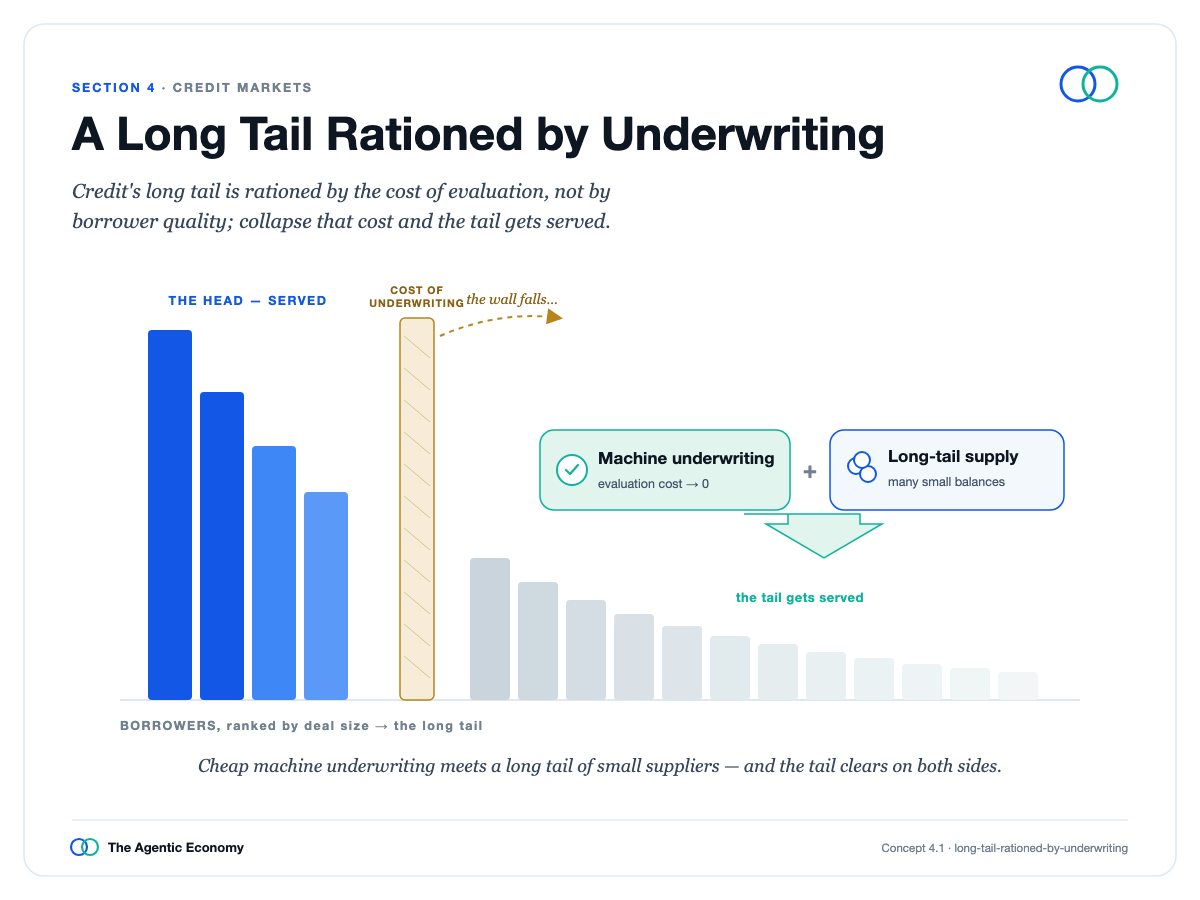

Long Tail Under Constrained Underwriting

The key is redefining the problem. Massive numbers of borrowers – small merchants, gig workers, households, and now agents – are underserved not because they are risky, but because the cost of vetting each small loan exceeds the loan's value. Credit rationing depends on underwriting cost, not borrower quality. Lower underwriting cost, and you serve a vast population of creditworthy borrowers previously overlooked.

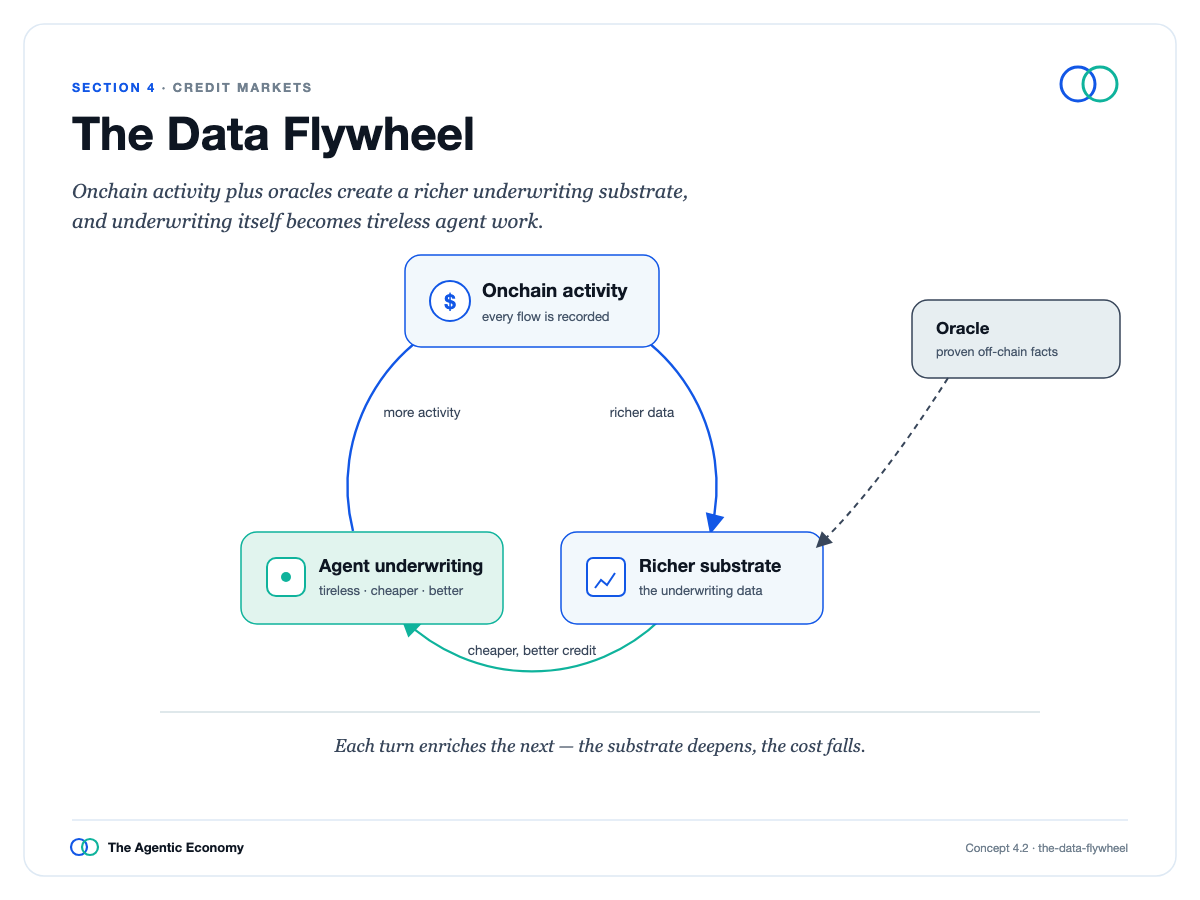

Data Flywheel

Driving the cost down is a data flywheel: Onchain activity is structured, verifiable, and real-time, enabling far superior risk models compared to fragmented historical records. Better data leads to better loans, which attracts more activity and more data.

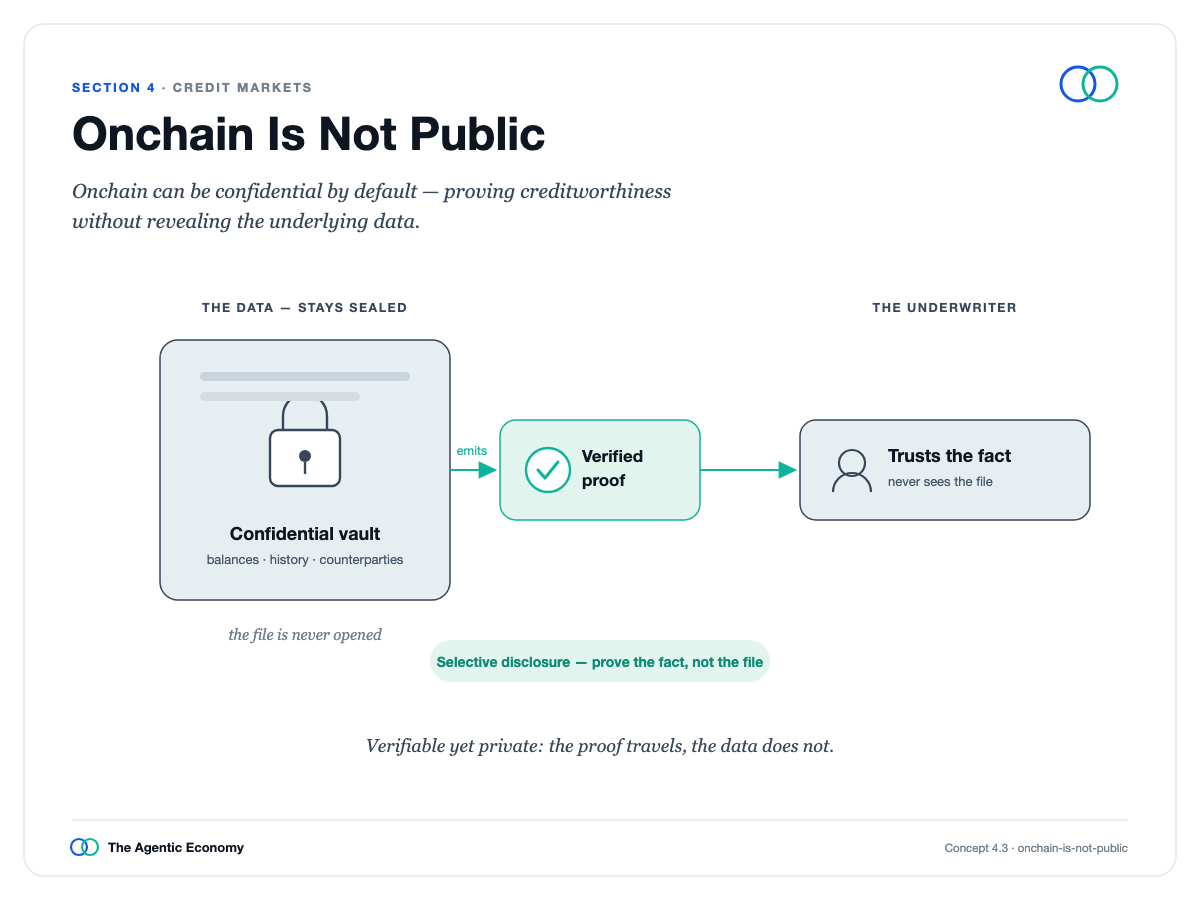

People naturally worry this puts everyone's finances on a public ledger. The answer is simple: Onchain does not mean public. New privacy technologies allow people to prove what a lender needs to know – their creditworthiness or loan balance – without revealing details.

Onchain is Not Public

The core is a genuinely new type of loan: Working capital for agents. It is unusually predictable because it removes the biggest variable in human lending – whether the borrower intends to repay – reducing risk to a short-cycle, limited-scope question about a specific job.

Agent Working Capital

Imagine an agent borrowing four dollars' worth of compute to complete a ten-dollar job it's already been hired for. The lender isn't guessing character; it's merely pricing the probability the job gets accepted. Collateral is inverted: instead of slowly seizing unrelated assets through courts, the loan is secured first by payment for the job itself, claimed automatically, and backed by the agent's posted bond, its reputation, and ultimately the real person behind it.

The result is credit that is cheaper, more accessible, yet safer – which seems impossible until you realize the gains come from better information, not more leverage.

The honesty this claim requires is that predictability decays over time: tasks completed in seconds are nearly mechanical, while month-long financing reverts to ordinary risk.

Thus, machine credit doesn't replace human credit; it becomes a new low-risk benchmark against which human lending is priced.

And it's all under watch: risk manifests as it accumulates, automatic brakes make rushing into the same pattern or provider progressively more expensive, and insurance is priced on actual conditions, not outdated averages.

Click to read Section 4: https://agenticeconomytreatise.com/treatise/section-4.html

05 Natively Global

The architecture has exactly three layers.

The bottom layer is money: a stablecoin serving as unit of account and final settlement. The middle layer is the economic operating system: coordination, contracts, and value exchange run as programmable smart contracts with finality. The top layer is agent execution: where actual work gets done, powered by AI and the cloud.

The crucial thing about these three is where they live. Each is software. Each runs on the internet. Each also replaces something once tied to a nation-state: software money replaces national banking systems stitched together