Securitize Drops 40% in First Week of Trading, Tokenization Industry Faces Patent War

- Core Thesis: The roughly 40% plunge in Securitize's stock price post-SPAC listing reflects the inherent valuation re-pricing risk of the SPAC mechanism and the cloud of patent litigation, rather than a fundamental collapse of the tokenization industry. The patent lawsuit initiated by tZERO could mark the beginning of an industry-wide patent war.

- Key Elements:

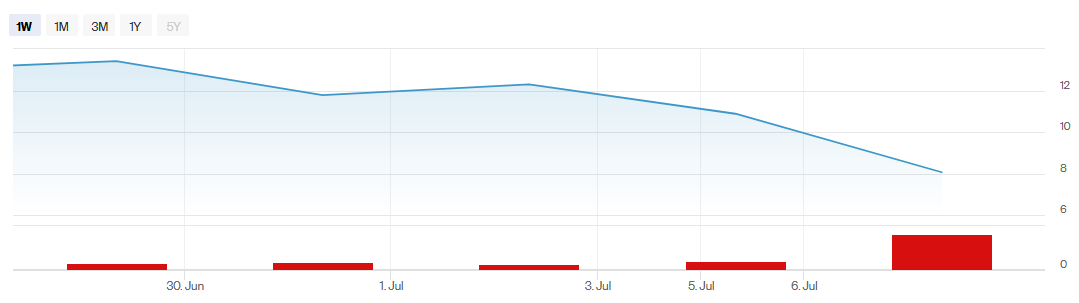

- After its SPAC listing, Securitize's stock price fell approximately 40% from its high within a week, trading at $8.06. The decline is primarily attributed to shifts in SPAC investor composition rather than a deterioration in the company's fundamentals.

- Similar crypto companies that went public via SPACs (Twenty One Capital, ProCap Financial) experienced analogous crashes, with declines exceeding 80% and 76% from their respective highs, highlighting a systematic flaw in the pricing mechanism.

- tZERO accuses Securitize of infringing on two core patents (rules for security token smart contracts and an integrated crypto platform), demanding a halt to commercialization and seeking damages. Securitize has filed a declaratory judgment action for non-infringement.

- tZERO holds 105 patents covering core aspects of tokenization infrastructure, has identified at least six other potential infringement targets, and plans to send further notices.

- The industry's RWA market size has expanded from approximately $22 billion at the beginning of the year to over $33 billion, pushing the conflict between patent barriers and commercialization into a substantive phase.

Original Author: Sanqing, Foresight News

On July 2, Securitize (NYSE: SECZ) officially debuted on the New York Stock Exchange through a SPAC merger with Cantor Equity Partners II. Its stock price initially rose on the first trading day, leading the market to view it as a milestone event signifying the tokenization industry gaining recognition from traditional capital markets. However, just a few trading sessions later, the script took a sharp turn. As of the close on July 7, SECZ was trading at $8.06, plummeting 25.92% in a single day, hitting an intraday low of $8.00, and retreating approximately 40% from its highs in the first week of listing.

Source: NYSE

This is a company selected by BlackRock's tokenized money market fund, BUIDL, to serve as its transfer agent. It is a leading platform in the tokenization space recognized by capital markets, with a pre-merger valuation of $1.25 billion. The stark contrast of its post-listing decline has led many investors to scrutinize the gap between the "tokenization narrative" and "secondary market realities."

SPAC Mechanism Exposes Problems Before Fundamentals

Over the past few years, almost all crypto-related companies that went public via SPAC have experienced similar valuation repricing during the redemption period.

Twenty-One Capital (XXI), also orchestrated by Cantor Fitzgerald affiliates, fell approximately 25% on its first day of trading on the NYSE on December 9, 2025, following its SPAC merger, closing at $11.42. It subsequently trended lower, with its stock price dropping below $6 at one point, down over 80% from its peak of $49. Similarly, ProCap Financial (BRR), a bitcoin treasury company that completed its merger around the same time, listed at $10 per share but now trades near $2.4, representing a decline of roughly 76%.

Many market observers attribute this sharp decline to the SPAC structure itself, rather than a deterioration in the company's fundamentals.

According to CoinDesk, Arca's Jeff Dorman publicly stated that the volatility is more attributable to the SPAC mechanism than to fundamental deterioration. Post-SPAC listing, the investor base undergoes a complete shift, transitioning from SPAC subscribers who originally favored fixed-income-like returns to stock holders focused on long-term fundamentals. This redemption process itself inherently creates significant volatility.

Market confidence in the "tokenization" narrative itself has not collapsed; rather, it is confidence in the SPAC pricing mechanism that has been shaken. Despite the share price decline, on its first day of listing, Securitize tokenized $295 million worth of its own stock and deployed it on Solana and Avalanche.

Securitize's decline also occurred against a backdrop of overall pressure on U.S. crypto-related stocks. As of early July, Coinbase and Circle's stock prices have fallen approximately 63% and 74%, respectively, from their all-time highs set in July 2025. Over the same period, the S&P 500 index only retreated about 2% from its June peak. When an entire sector's stocks are more volatile than the underlying assets, a newly listed tokenization platform can hardly remain immune.

Patent Lawsuit Opens a Fissure in the Industry

On June 15, tokenization infrastructure company tZERO sent a "cease and desist and reservation of rights" letter to Securitize, alleging that its two core products, DS Protocol and Vault Registrar, infringe on patents held by tZERO, specifically U.S. Patent No. 11,216,802 (covering self-executing security token smart contract rules) and No. 11,394,560 (covering a cryptographic integration platform).

tZERO demanded that Securitize cease the commercialization of the related products by June 18, or else it would seek injunctive relief and monetary damages.

Securitize took the initiative, filing a "Declaratory Judgment of Non-Infringement" lawsuit (Case No. 1:26-cv-00722, Securitize, Inc. v. tZERO Group, Inc. et al.) in the U.S. District Court for the District of Delaware on June 22. It seeks a court declaration that its products do not infringe on tZERO's patents, characterizing the opponent's allegations as "baseless," "lacking substance," and "contrary to the spirit of fair competition in the industry."

The case is currently in its early stages, assigned to Judge Gregory B. Williams, with no substantive answers, counterclaims, motions to dismiss, or news of a settlement yet filed. This means multiple outcomes remain possible, including out-of-court settlement, partial dismissal, or even tZERO withdrawing its claims.

The significance of this lawsuit extends far beyond a typical commercial dispute.

Nor is tZERO's patent assertion a spur-of-the-moment decision. The company, founded in 2014 and originating from Overstock.com's (a veteran U.S. online retailer whose founder, Patrick Byrne, is an early blockchain evangelist) vision for a security token trading platform, launched a strategic review of its intellectual property portfolio after completing a management change at the end of 2025.

According to tZERO's June 15 announcement on the progress of its intellectual property portfolio enforcement, it holds 105 patents spanning 23 patent families. Its business scope covers core aspects of tokenization infrastructure, including compliant security token systems, crypto asset integration, and KYC verification processes.

More critically, tZERO has explicitly stated that its patent review has identified "at least six" other market participants with potential infringement, covering areas such as compliant RWA platforms, institutional infrastructure, prime brokers, and decentralized exchanges. It plans to send infringement warning letters to more companies after completing its analysis.

As of July 8, the case remains in its early stages, with neither party having submitted substantive answers, counterclaims, or settlement documents.

However, the patent pressure on Securitize extends beyond just tZERO. During the same period, Liquid Rarity Exchange has also filed a separate lawsuit against Securitize concerning two other patents, seeking damages and injunctive relief.

In other words, Securitize might be the first, but not the only one. According to data from rwa.xyz, the RWA market size has accelerated from approximately $22 billion at the beginning of the year to over $33 billion, with the industry moving from "proof-of-concept" to "actual deployment" stage.

This is the context in which tZERO has chosen to turn its long-dormant patent portfolio into a commercial bargaining chip. As patent barriers in the tokenization industry begin to be actively asserted, almost any platform claiming "core technology" could be drawn into similar disputes. This warrants more long-term attention than a single stock price pullback.

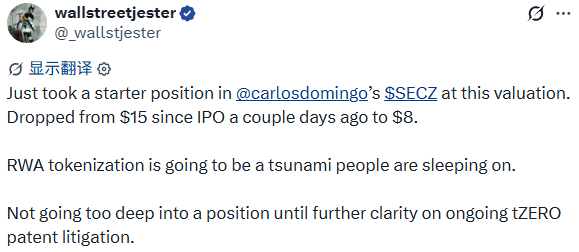

As X user wallstreetjester noted, despite "just building a position" in SECZ, they explicitly stated they "will not add significantly until there is clearer progress on the litigation." This reflects the genuine sentiment of some potential buyers.

Primary Markets Trust Endorsements; Secondary Markets Trust Liquidity

Securitize's shareholder lineup is undeniably prestigious. BlackRock's BUIDL fund chose it as its transfer agent. The PIPE financing round also attracted institutional investors like Borderless Capital and Hanwha Investment. The SPAC transaction itself was initiated by Cantor Fitzgerald affiliates.

This narrative of "joint endorsement by traditional financial institutions" was highly persuasive during the primary market fundraising stage and was a critical support for Securitize's pre-merger valuation of $1.25 billion.

But the secondary market doesn't buy endorsements; it buys liquidity. The market still believes in the "tokenization" story; what has truly cooled is the short-term pricing of Securitize's specific stock.

BlackRock's name can make primary market investors willing to pay for a valuation story, but it cannot make secondary market investors willing to hold shares while a patent dispute is unresolved and SPAC redemption pressure persists. Trust is a static brand asset; liquidity is a dynamic outcome of gaming. This crash perfectly demonstrates that there is no necessary conversion relationship between the two.

Securitize's stock price will eventually stabilize or rebound once the transition of its investor base is complete – this is an almost inevitable stage of growing pains for SPAC-listed companies. However, the patent war initiated by tZERO merits caution from all participants in the tokenization industry.

With tZERO holding 105 patents and targeting at least six potential infringers, this suggests that the next phase of competition in the tokenization industry may no longer be simply about securing compliance licenses, building institutional relationships, or boasting trading volumes.

For platforms still telling valuation stories based on "being the first to implement a certain technical solution," a cease-and-desist letter could bring that story to an abrupt halt at any time.

This downturn for Securitize has erased short-term valuation. But the lawsuit filed by tZERO may have unveiled a patent war that the entire tokenization industry is not yet ready to face.