A Comprehensive Overview of the On-Chain Options Track: From Opyn to Rysk, Who Has Overcome DeFi's Toughest Challenge?

- Core Thesis: After numerous failures, on-chain options are experiencing a renaissance driven by improved infrastructure, growing institutional demand, and user education by prediction markets. The ecosystem is currently rebuilding with a 30-day notional trading volume of $1.44 billion, but has moved away from early attempts to simply replicate traditional markets towards more professional and segmented architectures.

- Key Takeaways:

- In 2024, global options contract volume was over 4 times that of futures. The U.S. daily average options premium traded value reached $36 billion, and the single-day notional value peak for 0DTE options surpassed $1 trillion.

- Early protocols like Opyn, Hegic, and Ribbon, among 11 others, failed due to thin liquidity, poor capital efficiency, and suboptimal user experience. Weak market maker participation was a primary bottleneck.

- The rebuilding of the current on-chain options ecosystem is jointly driven by Rollups reducing gas fees, CLOB and RFQ replacing the AMM model, simplified products, and user education from prediction markets.

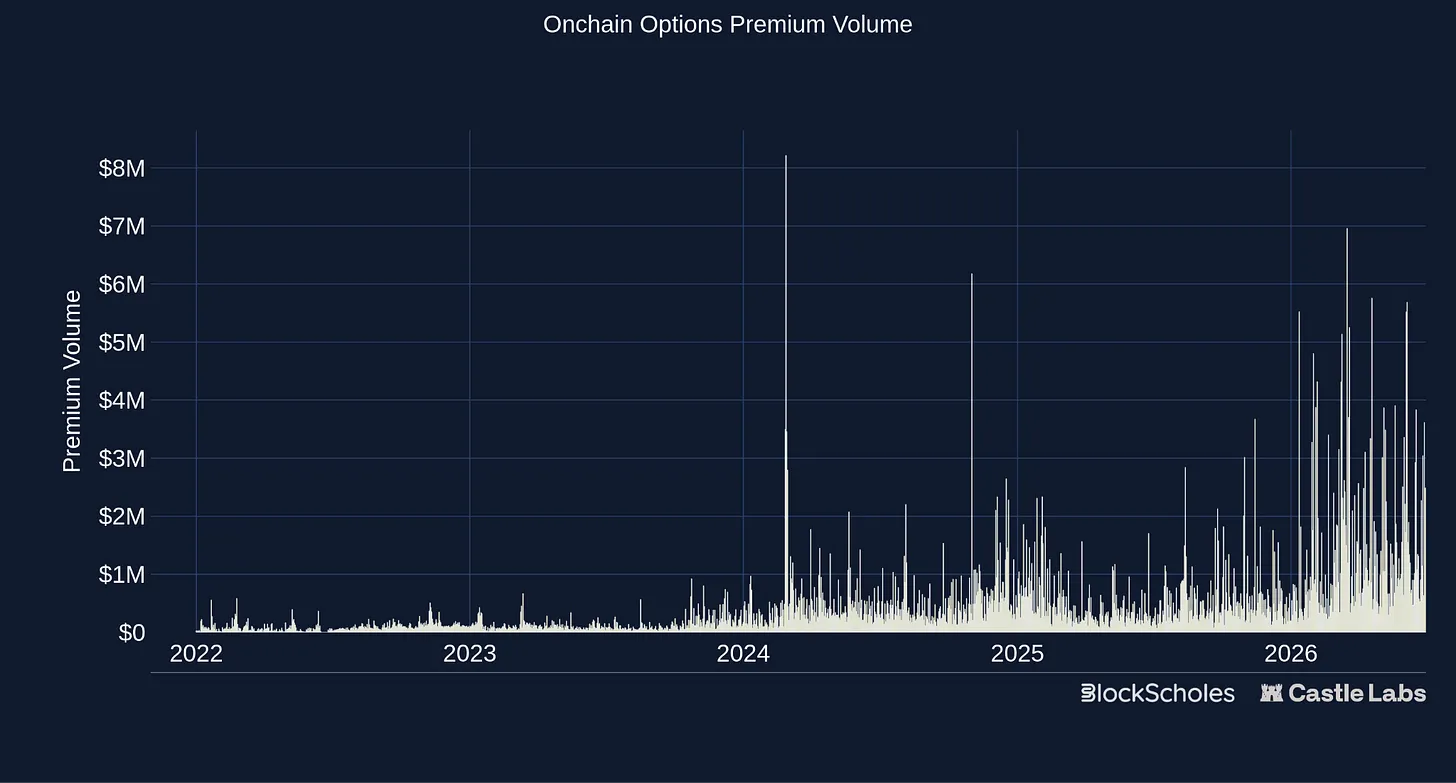

- On-chain options have a 30-day notional trading volume of approximately $1.44 billion, with premium trading volume hitting an all-time high. Most activity is concentrated in a few protocols like Derive, Rysk, and Aevo.

- Derive (formerly Lyra), which transformed into a CLOB platform, accounts for 79.2% of on-chain options notional value, serving professional traders through order books and incentive programs.

- Rysk focuses on covered calls and cash-secured puts, positioning options as yield-generating products. Its monthly notional trading volume grew from $50 million in January to $182 million in May.

- On-chain exotic options, such as perpetual options, AMM-native options, and short-term "touch" options, expand convexity exposure and ultra-short-term trading scenarios that traditional options cannot cover.

Original Author: Castle Labs

Original Compilation: TechFlow

Introduction: Options have become the dominant force in derivatives across global exchanges, with contract volume in 2024 being 4 times that of futures. The average daily premium trading volume for options in the US reached $360 billion. However, on-chain options were once one of the most brutal failures in the crypto world, with 11 protocols including Opyn, Hegic, and Ribbon falling one after another. Now, with improved infrastructure, growing institutional demand, and prediction markets educating users, on-chain options are finally being rebuilt from the ruins, with a 30-day notional trading volume of $1.44 billion. This ecological panorama explains why this time might be different.

Options in Financial Markets

Most people don't realize that they've actually been trading options their entire lives.

If you've bought insurance, you paid a premium for a conditional payout in the future. This is a put option because you are protecting yourself against a decline in the value of the underlying asset. If you've taken out a mortgage, you hold the right to refinance early. This is a call option because you have the exclusive right (but not the obligation) to "redeem" or cancel your current debt contract.

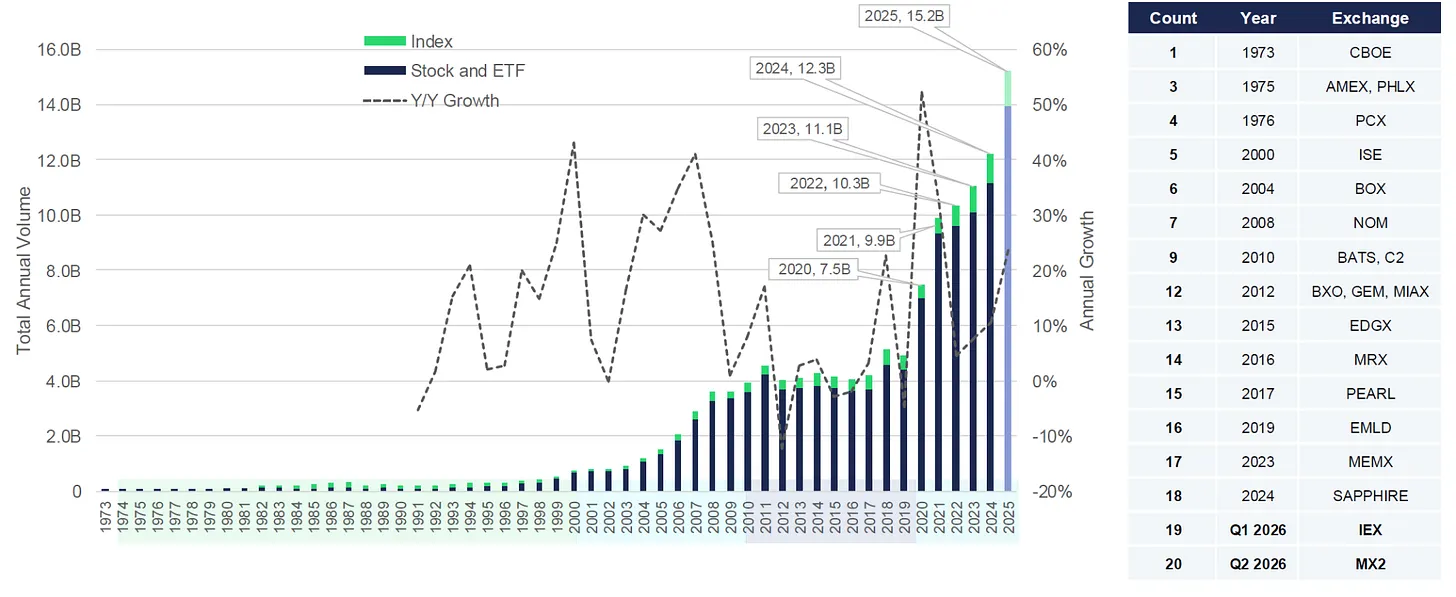

Options now far exceed futures in global exchange derivatives trading volume. In 2024, options contract volume was more than 4 times that of futures. In 2025, US listed options set a record for the sixth consecutive year, trading approximately 15.2 billion contracts, equivalent to about $36 billion in premium trading daily.

For Zero Days to Expiration (0DTE) options, the peak daily notional value for just the SPX exceeded $1 trillion, with an average of 2.3 million contracts per day, accounting for 59% of the product's total trading volume in 2025. 0DTE options expire on the trading day; they are used to chase huge, quick returns from intraday stock volatility but also carry the risk of losing 100% of the investment quickly.

In 2024, the National Stock Exchange of India (NSE) accounted for approximately 84% of global stock options contracts; but in terms of value, the total premium paid by US options buyers was still about 4 times that of India. This suggests that Indian retail investors are trading a vast number of tiny contracts, while US participants trade fewer contracts, but of larger size and higher price.

The appeal of options is also entering crypto products, although currently mainly from institutions.

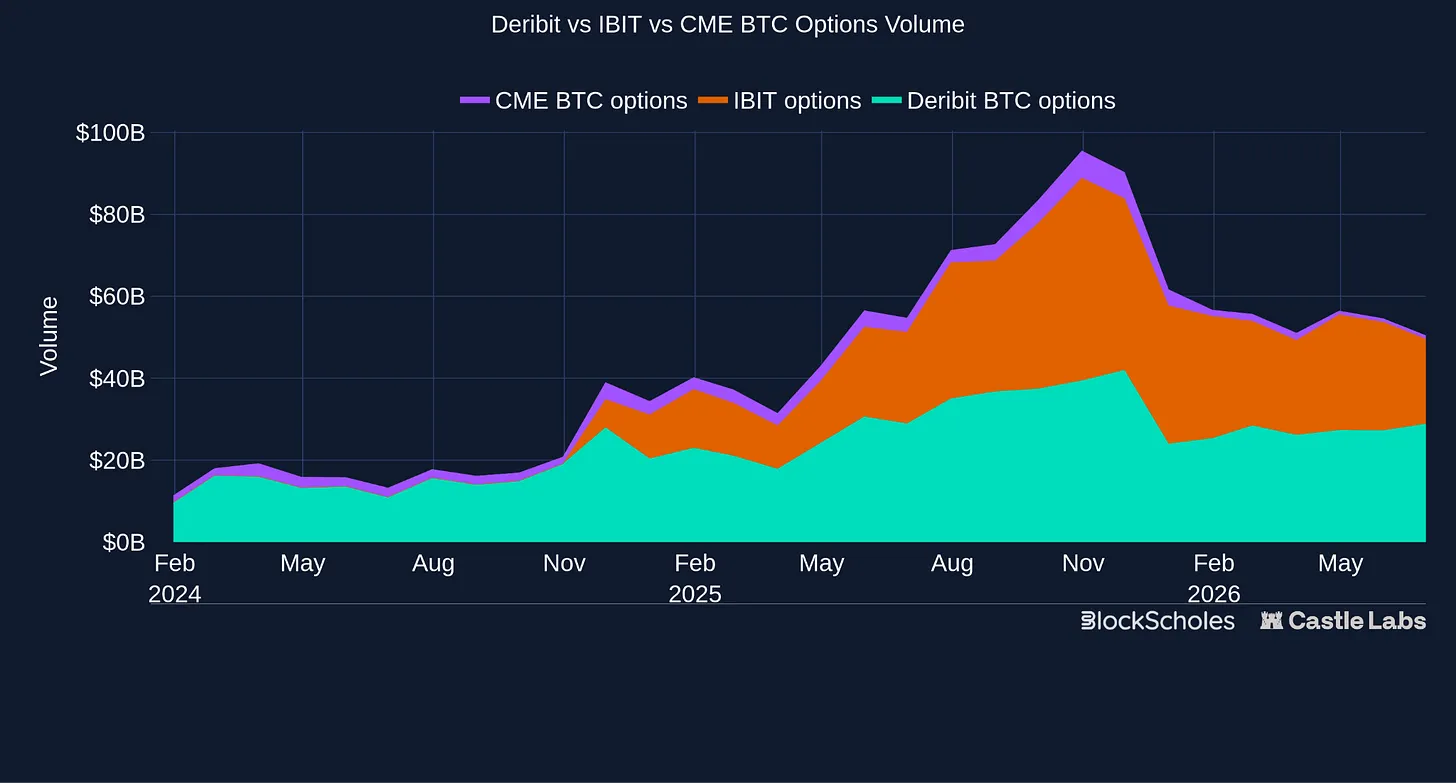

CME, the largest regulated derivatives exchange in the US, now offers 24/7 crypto options. This is an unprecedented shift for a traditional exchange aiming to retain its user base, acknowledging the appeal of the 24/7 crypto market. Furthermore, in April, the open interest for BlackRock's IBIT options surpassed BTC on Deribit, rising from $26.9 billion to $27.6 billion, even though Deribit launched over a decade ago.

Options are extremely versatile tools that can be used in a wide range of applications:

Hedging: Using options as an insurance policy for price exposure (buying puts to lock in a hard floor against downside losses, or buying calls to avoid missing a sudden rally).

Income Generation: Selling options to earn a steady stream of cash premiums from the market. This is useful for non-directional users who can generate passive yield on existing assets (covered calls), or get paid in advance while waiting to buy at a lower price (cash-secured puts).

Speculation: Expressing a view on price or volatility without directly purchasing the asset, regarding direction, timing, or specific price movements (achievable through a range of option strategies).

Customized Strategies: Combining multiple options into structured products, often used by banks and asset managers to create yield products or downside protection notes.

Early On-Chain Attempts

Given their prominent role in traditional markets, options were considered a natural product-market fit for the volatile on-chain crypto market. It turned out to be one of its most repeated failures.

This was by no means due to a lack of experimentation, as evidenced by the products launched in previous cycles:

Opyn tokenized vanilla options on Ethereum in 2019, but was hampered by thin liquidity, high collateral requirements, and high fees on the mainnet.

Hegic experimented with a peer-to-pool model in 2020, simplifying the buyer experience, but the pooled LPs bore risks that were difficult to hedge.

Ribbon, Friktion, and Dopex launched vaults in 2021, creating simple deposit-and-earn structured products for users seeking yield without managing positions. However, volatility was sold into thin, cyclical demand, compressing yields until premiums could no longer exceed risk.

Lyra, Premia, Pods, and Siren experimented with options AMMs, attempting to provide continuous liquidity across strike prices and expiries. They struggled with pricing and hedging, as LPs inherited complex volatility and inventory risks while organic flow remained thin.

In 2022, Opyn launched Squeeth, a perpetual contract tracking squared ETH exposure, allowing users to gain convexity without managing periodic options. Launched with high fees on Ethereum, the product was difficult to explain and expensive to hold when funding rates were high.

The industry was repeatedly hindered, primarily by structural constraints. Weak market maker participation led to thin two-way liquidity on trading venues and pushed difficult-to-hedge risks onto passive LPs. Capital inefficiency accompanied unreliable volatility surfaces, while user experience fell into a no-man's land: too complex for retail, but lacking the professional architecture institutions required.

New Infrastructure and Improvements

Conditions have been steadily improving since these early attempts:

Rollups and Ethereum scaling have reduced gas fees, making complex on-chain operations cost-effective while improving execution and settlement.

CLOBs and RFQs are beginning to replace AMM models, creating a more natural environment for professional traders and market makers to quote specific strike prices and expiries, update prices in real-time, and control risk more efficiently.

Simplified products target narrower audiences, as venues focus on launching specific products for specific users.

Prediction markets make option-like payoffs accessible to mainstream retail through binary outcomes, normalizing conditional payoff trading.

Institutional demand for crypto options has been steadily growing, mainly via Deribit, and more recently through IBIT and CME.

On-chain conditions have also improved. More robust options markets are beginning to form, with a 30-day notional volume of approximately $1.44 billion, and premium trading volume hitting all-time highs this year.

The resulting landscape looks vastly different from the first DeFi options cycle. Protocols are no longer simply trying to be an on-chain Deribit. The ecosystem involves many participants, ranging from institutional trading venues and ETF wrappers to on-chain vanilla options, new exotic options, and binary options operating through prediction markets.

In the following sections, we will delve into the current options landscape, focusing on what is happening on-chain.

The Crypto Options Ecosystem

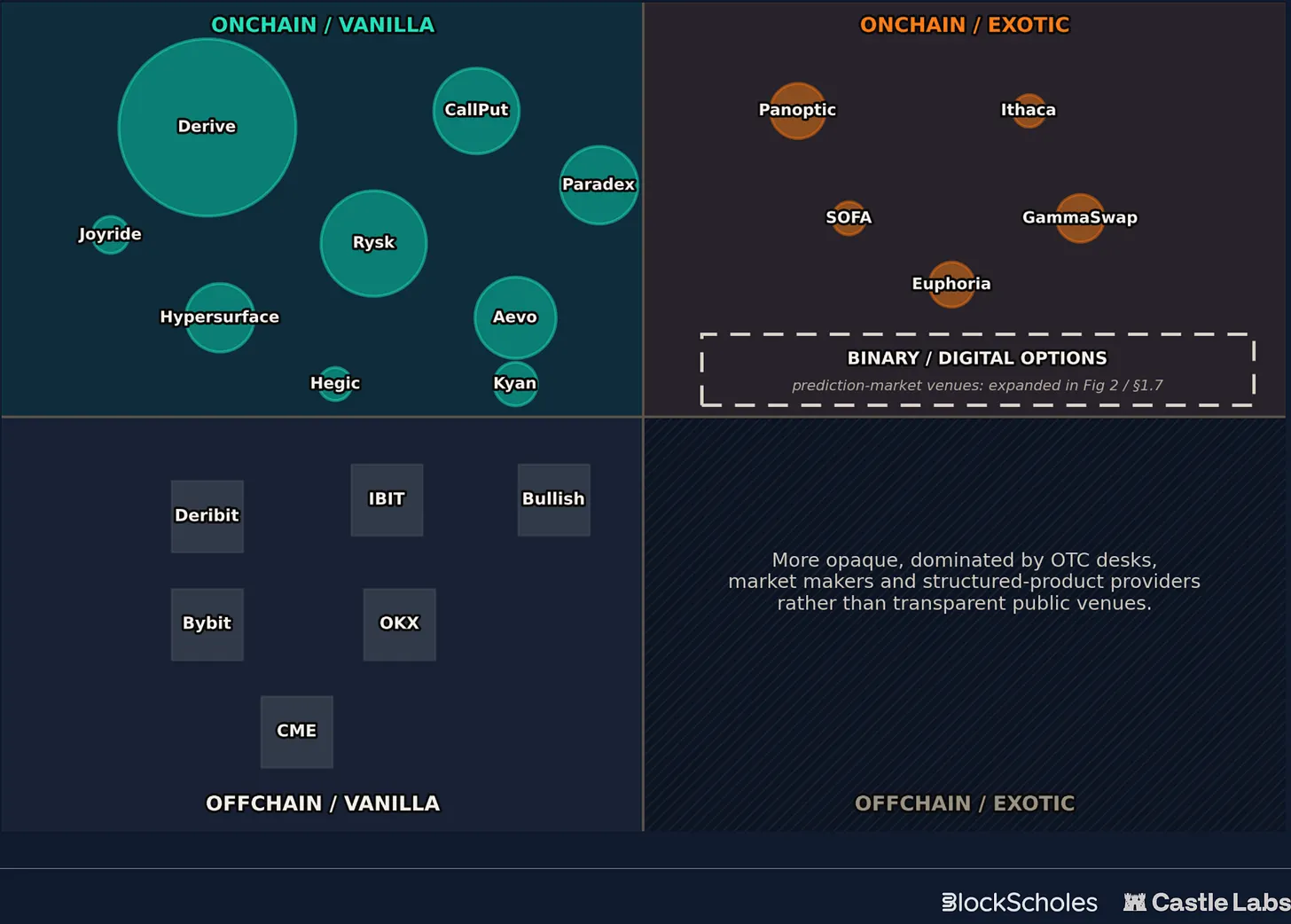

The crypto options landscape is a set of adjacent markets with different settlement and payoff types. The map below divides the ecosystem along these two dimensions:

Settlement: On-chain vs. Off-chain

Payoff: Vanilla vs. Exotic

Off-chain vanilla options remain the clear leader, driven by Deribit, IBIT, CME, and CEXs like Binance and OKX. On-chain vanilla trading venues are beginning to rebuild liquidity around CLOBs, RFQs, and more streamlined, user-centric products, while settling trades on-chain.

More experimental products reside within on-chain exotic options, using options or option-like payoffs as building blocks rather than simple listed calls, puts, and spreads. Examples include:

Perpetual Options: Replacing fixed expirations with a streaming premium mechanism. This allows traders to hold volatility positions indefinitely, without the friction and gas costs of manually rolling contracts.

AMM-Native Options: Creating option-like exposure from AMM liquidity positions rather than listed calls and puts. This enables advanced yield farmers to hedge Impermanent Loss and allows long-tail asset speculators to buy calls and puts on newer, unlisted tokens.

Short-Term Touch Options: Providing instant, fixed payouts at the exact moment an asset hits or breaks a specific price target. This structure is heavily used by retail day traders, scalpers, and event-driven news traders chasing quick feedback loops during short bursts of extreme intraday momentum.

The fourth quadrant—off-chain exotic options—is more opaque, dominated by OTC desks, market makers, and structured product providers rather than transparent public trading venues.

This report focuses on the on-chain side of the map, covering vanilla options venues and exotic option primitives, before turning to binary option-like markets, most commonly expressed as prediction markets.

On-Chain Vanilla Options Trading Venues

Recent progress in on-chain plain vanilla options is evident, not by changing the payoff itself, but by refining the surrounding infrastructure, product design, and user experience. These platforms are generally moving from passive LP pools to CLOBs and RFQs, making room for portfolio margining and yield-bearing collateral, while launching more targeted yield products that simplify outcomes for users.

This section will introduce several of the most prominent platforms currently.

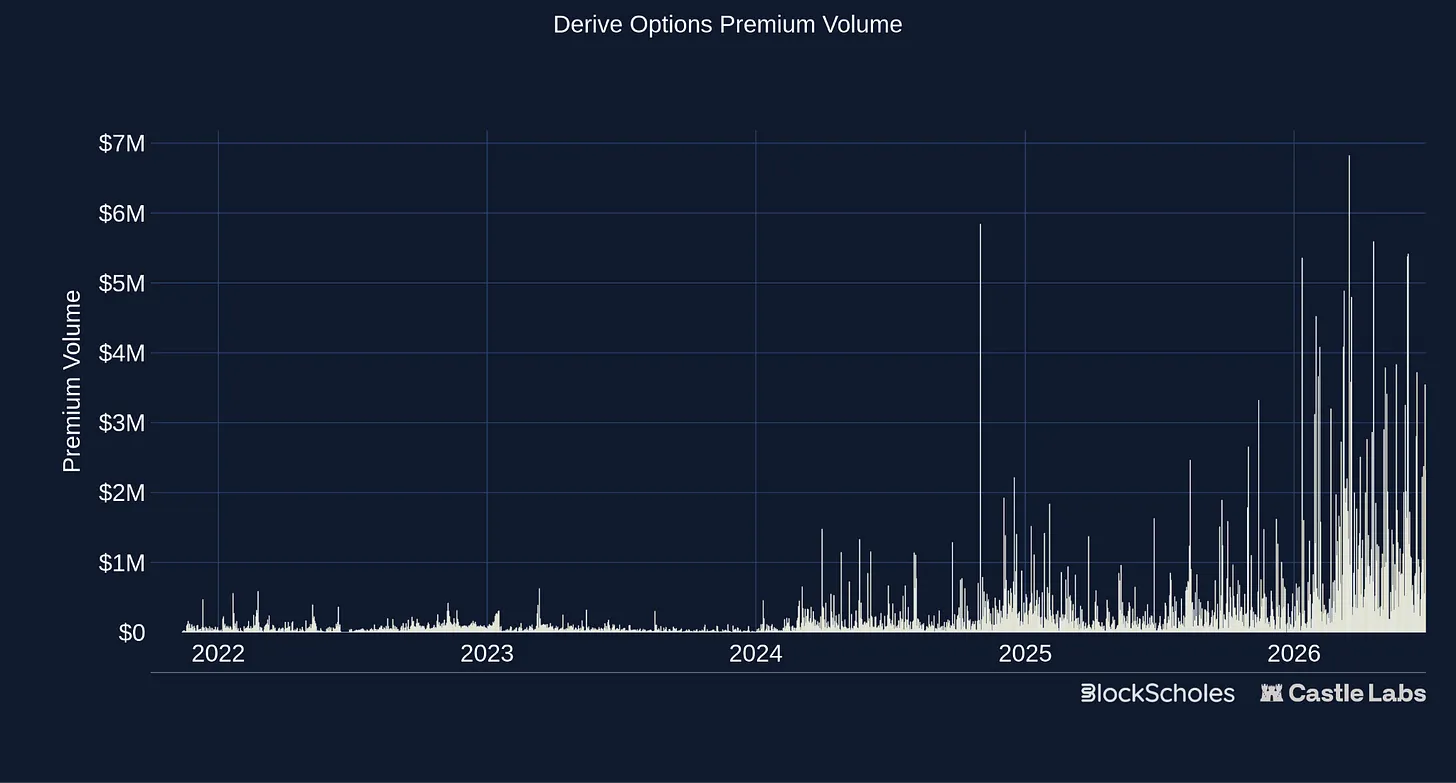

Derive

Derive is a prime example of this architectural shift. It evolved from Lyra, an options AMM, into the CLOB-based platform we see today. Now operating on its own OP Stack L2, Derive offers cross-margined options and contracts through a professional order book interface. Derive does not attempt to hide the complexity of options from users, thus targeting professional traders, market makers, institutions, and other sophisticated volatility traders. It looks much like a traditional options exchange, offering a range of assets, strike prices, and expirations that can be combined to create customized payoff structures.

Using an off-chain matching engine for instant execution, paired with on-chain L2 settlement, allows institutional allocators to trade at the speed of centralized exchanges like Deribit while maintaining non-custodial ownership of their assets. Derive also offers a range of vault products. Unlike previous attempts, these leverage the underlying exchange to execute predetermined options strategies, aiming to earn yield for depositors.

Derive currently accounts for the majority of on-chain options activity, with a 30-day notional value of $1.142 billion and premium of $44.3 million, representing 79.2% and 87.2% of the category, respectively. It should be noted that Derive uses market maker incentives, OP incentives, DRV rewards, and rebate programs to support liquidity.

Despite the incentives for liquidity and participation, Derive still demonstrates the industry's evolution over the years. Mature options exchanges now run on high-performance appchains, accessible to both institutions and market makers.

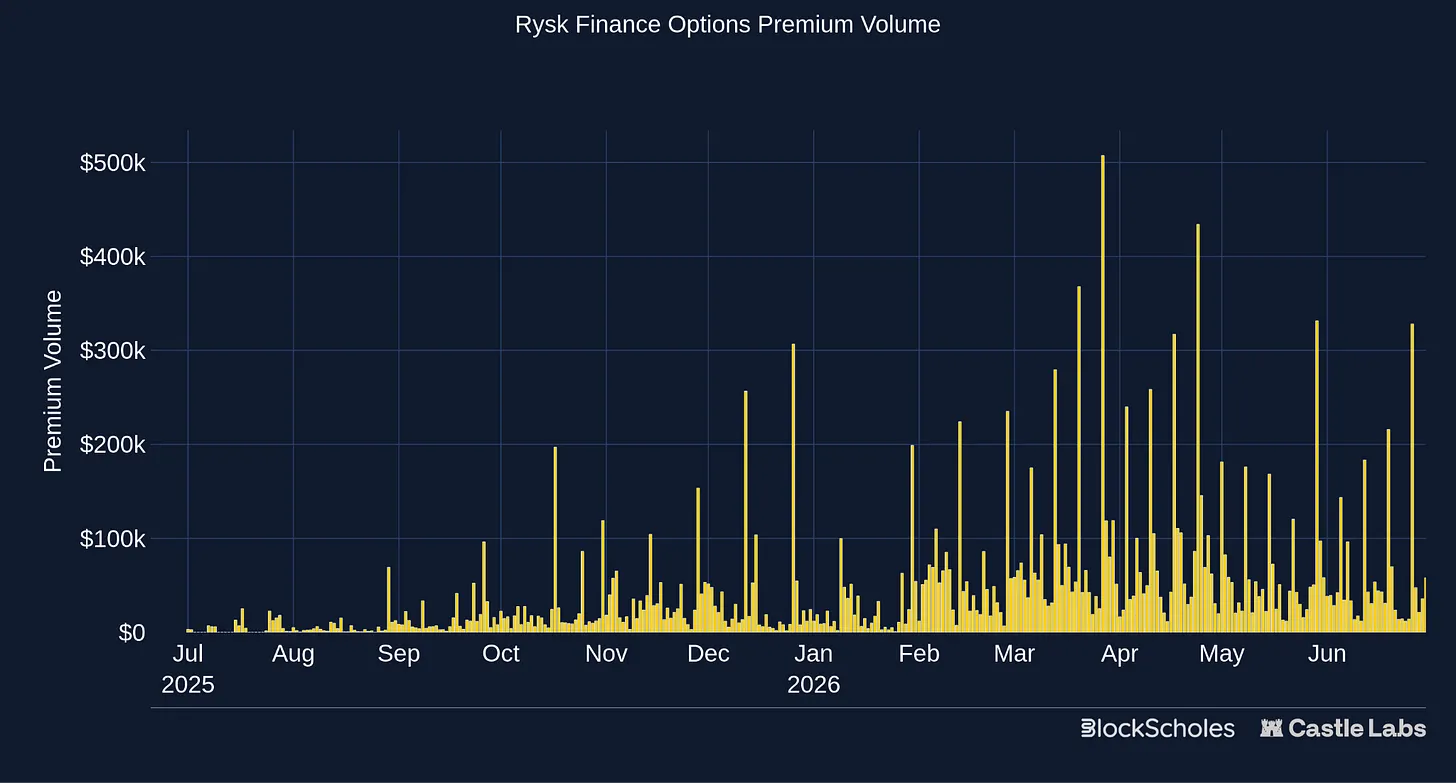

Rysk

Rysk takes a completely different approach from Derive. It is built around covered calls and cash-secured puts, using options as a prepaid yield product while keeping strike prices and expirations optional, differing from past options vaults. It routes user demand through an RFQ system where market makers quote on specific requests, buying option flow and managing their own risk elsewhere. Rysk focuses on simplifying the complexity of options products through robust asset selection, clearly defined outcomes, and a seamless user experience, making it attractive to both retail and institutional investors.

For the user, the product is simple. Earn yield on your assets while agreeing on a price level at which you are willing to sell or buy. This is reflected in its broad base of actual users. They all want to earn yield, but in different ways and with different strategies. Treasuries, DAOs, and funds are long-term holders who already have a view on at which price they'd be willing to buy or sell assets. Even if they don't want to, they can still earn yield at further-out strikes. Institutional users, like Hyperion, a Nasdaq-listed HYPE treasury company, run curated vault strategies on Rysk’s infrastructure. Its mandate is to accumulate HYPE, making the cash-secured put strategy a natural choice, earning yield while placing orders at lower price levels.

Rysk generated $136.3 million in notional value and $1.94 million in premium over the past 30 days, representing 9.5% of the category's notional value. Rysk's monthly notional volume grew from $50 million in January to $182 million in May, also staying above $175 million in March and April.

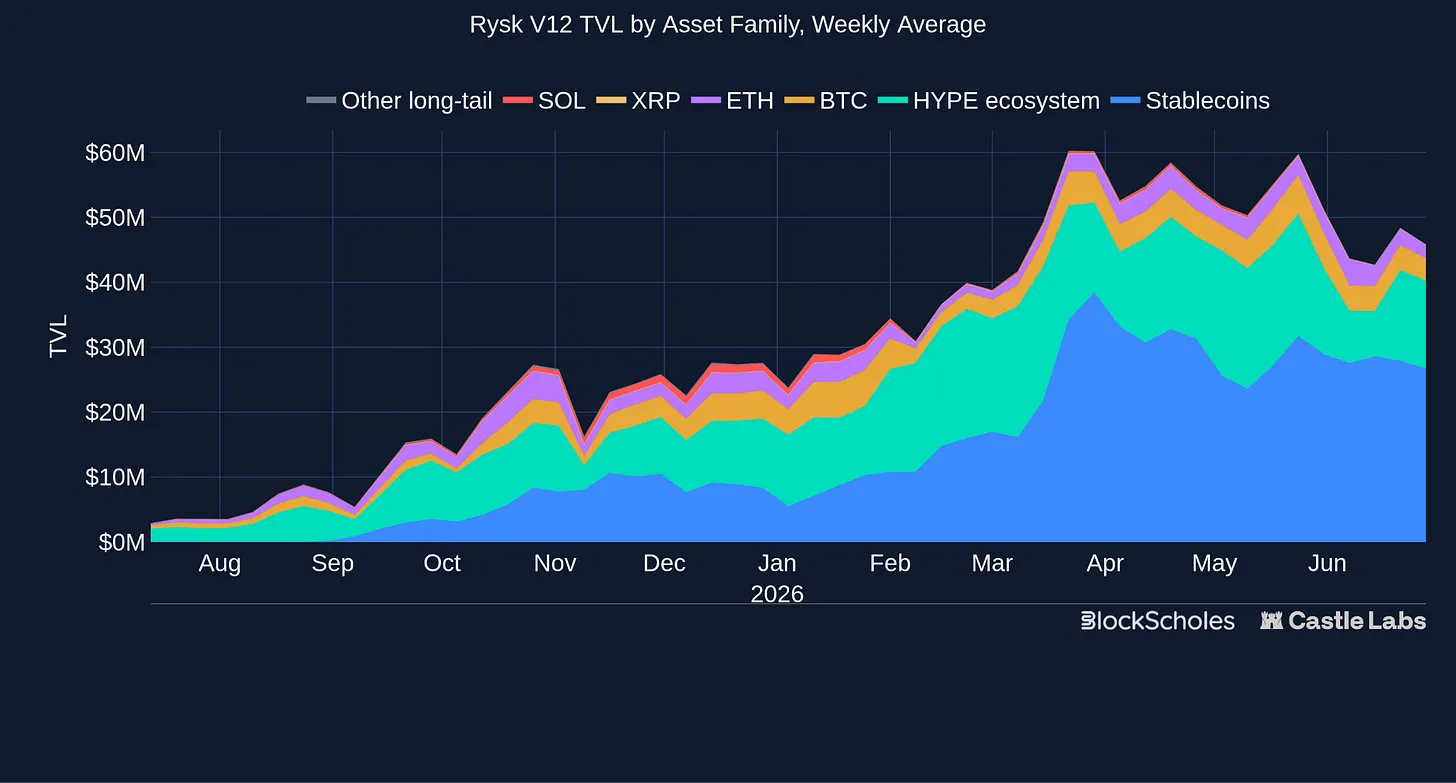

Unlike Derive, TVL is more relevant for Rysk because the product is based on collateralized options selling strategies. To receive premiums, you need to deposit all collateral, whereas in Derive, users can buy cheap options with low premiums to chase large gains.

Rysk has found a different product-market fit in the options space, repositioning options from a trading tool to a yield product based on selling volatility. As yields compress across the industry, this has become highly competitive relative to lending, staking, and basis products, as evidenced by its strong sustained growth since launch.

Aevo

Like Derive, Aevo evolved from an early options product into an order book exchange. It evolved from Ribbon Finance, one of the first major DeFi Options Vault (DOV) products, before pivoting to a broader derivatives platform. Today, Aevo offers options alongside contracts, pre-launch markets, OTC, and automated strategies on a custom L2, utilizing off-chain order matching and on-chain settlement. Orders are matched in microseconds via an off-chain central limit order book (CLOB) to replicate the CEX user experience, while user funds remain securely locked in on-chain smart contracts hosted on a custom OP Stack Ethereum L2 rollup.

Launched in 2023, Aevo saw its most active options period during 2024. Since then, reported TVL and visible options activity have declined from earlier highs, although options premium trading volume has recently started to pick up again.

Aevo's main unique selling point is