Avenir Group Bets on WasabiCard: Why Are Stablecoin Payments Getting Hotter as U-Cards Fade?

- Core Insight: Competition in stablecoin payments is pivoting from consumer-facing U-card products to B2B backend infrastructure. Capital is betting on service providers like WasabiCard that offer card issuance, APIs, clearing & settlement, and compliance capabilities. Their growth can compound through enterprise client expansion, potentially reshaping the industry landscape.

- Key Elements:

- WasabiCard has completed a nearly $10 million Pre-A funding round, with investors including the Li Lin family office, Avenir Group. Cumulatively, it has raised nearly $10 million, focusing on global card issuance resources and compliance system building.

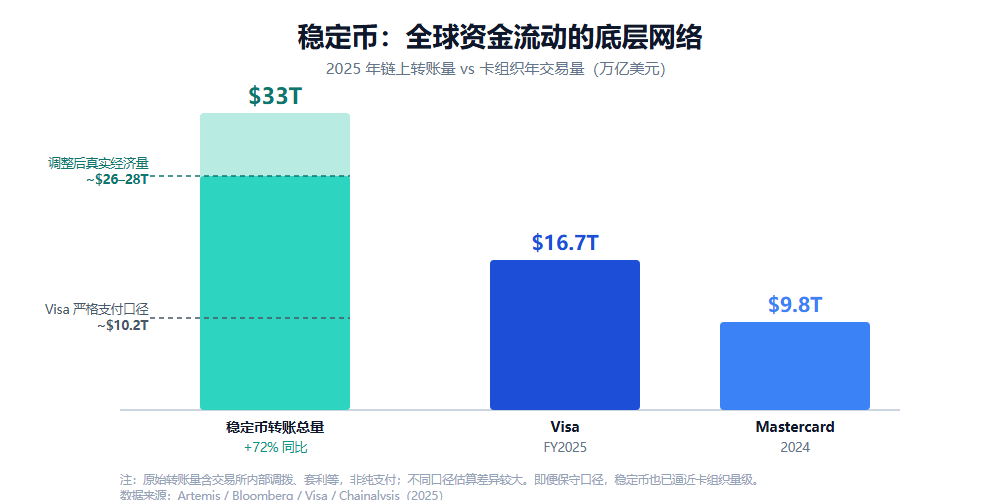

- According to a Fireblocks report, nearly 90% of institutions have engaged with stablecoin payments, with 49% using them for payment scenarios. Global stablecoin on-chain transfer volume reached $33 trillion, an increase of 72% year-over-year, surpassing the combined total of Visa and Mastercard.

- The C-end U-card model (e.g., RedotPay: 6 million users, $10 billion annual transaction volume) relies on external card issuance and compliance partnerships, making it difficult to sustain long-term; B-end infrastructure (e.g., BVNK: $30 billion annual processing volume) was acquired by Mastercard for $1.8 billion, demonstrating a higher moat.

- WasabiCard has served over 500 enterprise clients, issued more than 500,000 cards, and surpassed $1 billion in transaction volume. It supports multi-chain access and positions itself as a "white-label" global card issuance and payment API infrastructure, leading in B-end payout (41% most valued) and compliance (34%) capabilities.

- Traditional payment giants are accelerating their moves: Stripe acquired Bridge for $1.1 billion, Mastercard plans to acquire BVNK for $1.8 billion, and Visa intends to expand stablecoin-linked cards to over 100 countries. This underscores that infrastructure is the key strategic position.

Li Lin is placing another bet.

On June 3, 2026, WasabiCard, a global stablecoin payment infrastructure platform, completed its Pre-A round of financing. Combined with earlier rounds, total funding has now approached nearly $10 million. Investors include Vernal Capital, Avenir Group, Vision Plus Capital, and 01VC — among which Avenir Group is Li Lin's family office.

Interestingly, almost simultaneously, another piece of news was circulating within communities: Fiat24 suspended new account applications in mainland China. Meanwhile, several crypto card services familiar to Chinese users, such as SafePal and Bitget Wallet, have partnerships reliant on Fiat24's card issuance capabilities.

On one hand, capital is betting on an "invisible" payment infrastructure company; on the other, an underlying service provider's policy adjustments directly affect certain front-end card products. Viewed together at this point in time, it provides a fresh perspective for re-examining the stablecoin payment track.

Behind this perspective lies a rapidly expanding real demand.

1. The Ebb of U Cards: What's Receding Isn't Demand, but the Model

According to Fireblocks' "State of Stablecoins 2025" report, 49% of surveyed institutions already use stablecoins for payments, with another 41% in the testing or planning phase. This means nearly 90% of institutions are engaging with stablecoin payments in some form.

Demand is rising, but the means of meeting that demand are changing.

As is well known, over the past few years, the most discussed form of stablecoin payment in the Chinese market has been the "U Card": users deposit stablecoins like USDT or USDC into a card product for online subscriptions, consumption, or offline payments. This concept is also the easiest for users to understand and adopt.

But the U Card is merely the visible front end.

Behind a single card lies a complex web of card issuing licenses, card network partnerships, KYC/AML systems, risk control frameworks, stablecoin-to-fiat conversion, clearing and settlement networks, merchant channels, and cross-border payment capabilities. What users typically remember are consumer-facing brands like RedotPay, KAST, or Crypto.com, while institutions like WasabiCard remain relatively unknown.

In fact, thanks to infrastructure companies like WasabiCard, issuing a single "card" today is no longer a difficult task.

Projects can outsource every step — stablecoin acceptance, credit allocation, card issuance, spending channels — to third-party service providers, simply branding and launching the front end themselves. This, in a sense, is a key reason for the rapid proliferation of U Card products in recent years.

So, Fiat24 tightening account openings is just a trigger.

The real issue is that the consumer-facing U Cards, which spread rapidly over the past few years, are essentially a "light front-end, heavy external dependence" model. The hardest parts were outsourced, leaving the brand, customer acquisition, and the user interface behind. While this solved the "how to spend U," it did not solve the "how to sustainably, stably, and compliantly run this business long-term" problem.

Over the past year, the contraction or even withdrawal of several front-end card products has repeatedly demonstrated that a front-end experience alone cannot sustain a payment business capable of weathering market cycles.

This point is crucial.

U Card products can be copied, subsidies can be matched, and users can quickly migrate based on fees, risk controls, and usability. What is truly difficult to replicate are the back-end capabilities:

- The ability to maintain stable card issuing and acquiring partnerships across multiple markets;

- The capacity to handle identity verification and anti-money laundering requirements across different jurisdictions;

- The capability to maintain consistency in fund and information flows across stablecoin top-ups, fiat conversion, card spending, and merchant settlement;

- The ability to develop a mature risk control system for handling anomalous transactions, high-risk addresses, chargebacks, refunds, freezes, and compliance reviews;

This is the logical starting point for Avenir Group and other institutions betting on WasabiCard — what these institutions are eyeing might not be another crypto card product, but a stablecoin payment business transitioning from "cards" to "infrastructure."

2. Why Avenir Group is Betting on WasabiCard

In recent years, the crypto market has not lacked grand narratives.

From DeFi, NFTs, and GameFi to public chains, L2s, Restaking, and AI + Crypto, industry cycles are often driven by asset prices, token expectations, and liquidity expansion. However, payments have always been a different kind of business. It's less glamorous and rarely creates extreme valuation imagination in a short time, yet it is closer to real-world transaction needs.

Because whenever a transaction occurs, every specific step — payment, currency exchange, card issuing, settlement, acquiring, and cross-border transfer — presents an opportunity to generate revenue.

The scale of this business is already impossible to ignore. Artemis data shows that global stablecoin on-chain transfer volume reached $33 trillion in 2025, a 72% year-over-year increase, surpassing the combined total of Visa and Mastercard. Even excluding non-payment uses like internal exchange transfers and arbitrage, its real economic scale now approaches that of traditional card networks.

Whether these fund flows ultimately correspond to trading, allocation, or settlement, it means stablecoins have become a crucial underlying network for global capital movement. But precisely because of this, for an on-chain USDT/USDC transfer to truly become a usable payment for businesses, a receivable salary for employees, an acceptable settlement for merchants, or a spendable card balance for users, a complete suite of off-chain financial infrastructure is required.

This is precisely the opportunity for companies like WasabiCard.

They handle the "dirty and hard work": interfacing with card networks and issuing resources, building enterprise APIs, managing fund settlement, overseeing risk control and compliance, and enabling corporate clients to embed stablecoin payment capabilities into their own business processes. These tasks don't attract market attention as quickly as launching a token, but once the capability is proven, it often creates greater reusability.

Because from a business model perspective, B2B infrastructure and consumer-facing card products are fundamentally different businesses.

Consumer card products require continuous customer acquisition, ongoing subsidies, persistent user education, and must navigate users constantly comparing fees, usability, and brand trust. In contrast, once B2B payment infrastructure is integrated by exchanges/wallets, payment companies, or overseas enterprises, it benefits from the growing transaction volumes of its clients. The former is trapped in a cycle of customer acquisition, while the latter more readily forms compound growth.

More importantly, once a project integrates a particular payment API into its business, the switching costs become high. The partnership is more likely to deepen around transaction volume, settlement amounts, and business scale. This is the beauty of underlying infrastructure: it doesn't need to outrun everyone itself; as long as any of its clients succeed or scale up, it can share in the growth dividends.

Breaking this down explains why capital is increasingly focused on the infrastructure layer:

- Payments are one of the easiest scenarios for stablecoins to generate real cash flow. Compared to Web3 narratives still reliant on token cycles and liquidity speculation, it's closer to genuine transaction demand. It's a business model driven less by market sentiment and more by transaction volume and network scale.

- Service providers like WasabiCard already have operational and compliance foundations, having accumulated reusable capabilities in B2B client relationships and highly compliant systems. For investors, "already integrated" is far more valuable than "planning to be integrated."

- Capital isn't buying a point product, but a scalable infrastructure. Its growth can be "piggybacked" on the growth of its clients, rather than requiring new customer acquisition for every single transaction.

For an investment institution, the ceiling of a point U Card product depends on how many end-users it can acquire and their active spending frequency. However, the potential of a stablecoin payment infrastructure depends on how many enterprise clients it can serve, how many payment scenarios it covers, and whether it can become the common capability layer behind numerous front-end products.

From this perspective, Avenir Group's investment in WasabiCard is less about providing some form of "authoritative endorsement" and more akin to a seasoned crypto player making a directional bet on stablecoin payment infrastructure.

Where this bet points might be more significant than the funding itself.

3. Comparing Not Scale, but Position: Where Does the B2B Moat Lie?

Of course, this doesn't mean the infrastructure model is inherently easier to succeed with. In stablecoin payments, consumer cards and B2B infrastructure are two different tracks. Directly comparing absolute scale is meaningless; the key is to look at positioning.

Consider the benchmark on the consumer track, RedotPay. It currently boasts over 6 million users, covers more than 100 countries, has an annual transaction volume of approximately $10 billion, and annual revenue exceeding $150 million. In 2025, it raised a cumulative $194 million, reaching a valuation of over $1 billion.

It's arguably the ceiling for what U Cards can achieve — but it's telling that even this champion relied on licensed entities like Reap for card BINs, Fireblocks and Sumsub for compliance, and Circle's network for cross-border payouts.

In other words, even the leading card stands atop a layer of underlying infrastructure.

Now look at the "graduate" on the B2B track, BVNK. Processing over $30 billion in annual payment volume, covering 130+ countries, and holding licenses including MiCA, it was ultimately acquired by Mastercard for up to $1.8 billion, marking the largest stablecoin infrastructure acquisition to date.

It offers an alternative endpoint for this track: not chasing end-users, but building deep underlying capabilities, continuously refining compliance, and eventually being integrated by a giant into a global network.

WasabiCard stands on this same track. As of this funding round, it has officially disclosed serving over 500 enterprise clients globally, issuing more than 500,000 cards, processing over $1 billion in transaction volume, and completing integration with multiple chains including Avalanche, Arbitrum, and BNB Chain. It recently joined Circle's partner program.

It consolidates card issuing, API, settlement, and payment capabilities into a single interface, focusing on a localization strategy by partnering with banks in major global markets. Its positioning is that of an infrastructure company capable of "one-click" exporting global white-label card issuing, API, clearing, settlement, and payment capabilities. This localization strategy allows WasabiCard to leverage local banking capabilities in various regions to compliantly issue cards to local users; simultaneously, its enterprise clients need only integrate its API once to achieve global card issuance.

Critically, based on public information, WasabiCard's focus is not solely on issuing cards to consumers, but on continuously expanding global card issuing resources, enterprise payment APIs, global fund distribution (payout), multi-chain asset access, and compliance system development. This means it provides not a single payment product, but a set of underlying payment capabilities that different platforms and business scenarios can invoke.

So, where exactly does the moat for this capability lie?

The Fireblocks report provides a clue: when banks and payment institutions select stablecoin infrastructure vendors, 41% value "fast and reliable payout" the most, and 34% value compliance. In short, payout and compliance are the two most critical factors for enterprise selection, precisely what issuing a single card cannot replace.

For a representative B2B player like WasabiCard, this means proving not just that it can issue cards, but that it can become the stablecoin payment operating system behind different enterprise clients, serving broader internet companies and cross-border business scenarios.

4. PayFi: The Moment When "Infrastructure" Gets Noticed Again?

If the most exciting part of stablecoin payments in recent years was U Cards, then the next phase worth watching might be PayFi infrastructure.

For a long time, PayFi was easily simplified to "card issuing" or "cashback," making it seem more like a consumer product track than a financial infrastructure one.

But over the past two years, this has been changing significantly.

Financial infrastructure related to stablecoin issuance, payment, and settlement has become one of the few asset classes in the crypto industry capable of consistently generating cash flow. Consequently, the PayFi track has attracted nearly all types of players, from crypto-native projects and traditional payment giants to stablecoin issuers, exchanges, and dedicated stablecoin public chains, all vying for position in their own ways.

Most telling are the sequential moves by traditional payment giants:

- In October 2024, Stripe acquired the stablecoin infrastructure company Bridge for approximately $1.1 billion, then one of the largest acquisitions in the crypto space;

- A year and a half later, in March 2026, Mastercard announced its intention to acquire stablecoin infrastructure provider BVNK for up to $1.8 billion, paying about $700 million more than Stripe and setting a new record;

- Around the same time, Visa expanded its partnership with Bridge (now part of Stripe), planning to extend stablecoin-linked cards from 18 countries to over 100;

- Earlier, PayPal had already launched its own stablecoin, PYUSD;

Plotting these actions from payment giants, card networks, and major fintech companies on a single map reveals not just an isolated bet on crypto payments by one company, but a preemptive positioning by the entire payment industry around the stablecoin on-ramp.

Because the impact of stablecoins extends beyond payment experience; it challenges deeper profit and power structures within the traditional financial system — directly relating to who will control accounts, cross-border channels, and even clearing and settlement in the new era. From this perspective, giants proactively connecting to on-chain accounts, stablecoin assets, and merchant receiving terminals is less an embrace of innovation and more a fear of being bypassed and left behind in the next restructuring of payment clearing.

However, as giants start competing for the infrastructure layer themselves, the window for independent infrastructure players becomes particularly clear: either become an irreplaceable link within the giant's network, or grow into that network yourself. After all, regulation and licenses, KYC/AML, card network partnerships, and localized compliance are precisely the parts that consumer-facing U Card products, built on traffic and subsidies, find hardest to sustain long-term.

This explains why companies like WasabiCard intend to use this round of funding primarily for building global compliance systems, expanding multi-banking network connections, and upgrading core clearing and settlement systems. These directions aren't glamorous, but they are the essential underlying capabilities stablecoin payments must build up when transitioning from a user product to financial infrastructure.

Looking further ahead, PayFi's potential could extend to AI Agent payments. If AI Agents truly begin executing automated transactions on behalf of users in the future, payment infrastructure cannot be designed solely around "humans." Machines will also need callable accounts, verifiable authorizations, controllable spending limits, auditable transaction records, and the ability to execute small, high-frequency payments automatically within compliance boundaries.

This will make the endgame for stablecoin payment infrastructure more complex. Of course, this is still a more long-term vision.

But it at least demonstrates that the value boundary of stablecoin payments is far greater than a single U Card.

Final Thoughts

Encrypted payment cards are certainly a good business.

They connect stablecoins with real-world spending, giving users the first tangible feeling that "U can be spent." This is precisely why U Cards rapidly broke through in the Chinese market, becoming the most easily understandable entry point for PayFi.

But the biggest dividends may not lie with the cards themselves.

In the past, the market more easily remembered a card, an app, a cashback campaign, or a low-fee gateway. However, as stablecoins enter larger-scale real-world business scenarios, the decisive factor for the industry's long-term structure might be deeper underlying capabilities.

Players like WasabiCard, operating relatively behind the scenes, might not have been the most