Monera Digital|Crypto Market May Report: Four Major Reasons Behind the Accelerated Market Decline

- Core Insight: In May, Bitcoin's market experienced two handovers of pricing power — first suppressed by macro factors, then driven down by internal capital outflows. By the end of the month, the macro environment improved, but the crypto market refused to rally, indicating that internal deleveraging had become the core drag, pushing the market into an accelerated phase of the deep bear.

- Key Elements:

- Macro & Geopolitics: The rebound in US inflation and personnel changes at the Federal Reserve shifted market pricing toward "forced rate hikes," pushing the 30-year US Treasury yield to 5.19%. By month-end, after geopolitical tensions eased, Bitcoin's correlation with the Nasdaq turned deeply negative — stocks rose while crypto fell alone.

- Capital Outflows: Bitcoin spot ETFs recorded a net outflow of $2.425 billion for the month, the third-largest monthly outflow in history. The Coinbase premium index turned entirely negative, indicating systematic deleveraging of crypto assets by US institutions.

- On-Chain Capitulation: Short-term holder MVRV fell below the 1.0 breakeven line, entering loss territory. The NUPL indicator dropped from the "euphoria" zone to the edge of "hope-fear," confirming capitulatory selling.

- Derivatives Risk: Open interest unexpectedly rose to over $64 billion, while longs saw $307 million in liquidations by month-end (vs. only $90 million for shorts), completing a deleveraging cycle.

- Key Defense Breached: Bitcoin's price broke through the $75,000-$76,000 cost basis of corporate treasuries. Gamma squeeze by market makers was triggered, leading to cascading sell-offs.

- Cyclical Value Zone: The 200-week moving average percentile dropped to 10.2%, placing it in historical bottom-value territory. However, history shows that from the percentile bottom to price reversal typically takes 3–6 months.

Core Takeaways

May was a month of two transfers of pricing power. First, the risk-free rate wrested pricing power away from crypto narratives, fully exposing Bitcoin's high-beta nature. Then, as both interest rates and geopolitical tensions eased towards the end of the month, internal capital outflows and holder capitulation took over price control.

On the price front, BTC briefly surged to the $82,850 area at the start of May, before succumbing to pressure and declining steadily. It closed the month at $73,674, forming a unidirectional downward trend. The most noteworthy period was the final week – the external environment had turned substantially accommodative, but the crypto market refused to rally. This is a textbook case of "failed liquidity transmission" and a quintessential example of the brutality of a deep bear market.

The internal deterioration across three fronts simultaneously was the true root cause of May's decline:

· First, dual hemorrhaging of new capital. BTC spot ETFs saw net outflows of $2.425 billion for the full month, the third-largest monthly outflow since the inception of BTC ETFs (trailing only February 2025's $3.555 billion and November 2025's $3.481 billion). Simultaneously, stablecoin supply contracted.

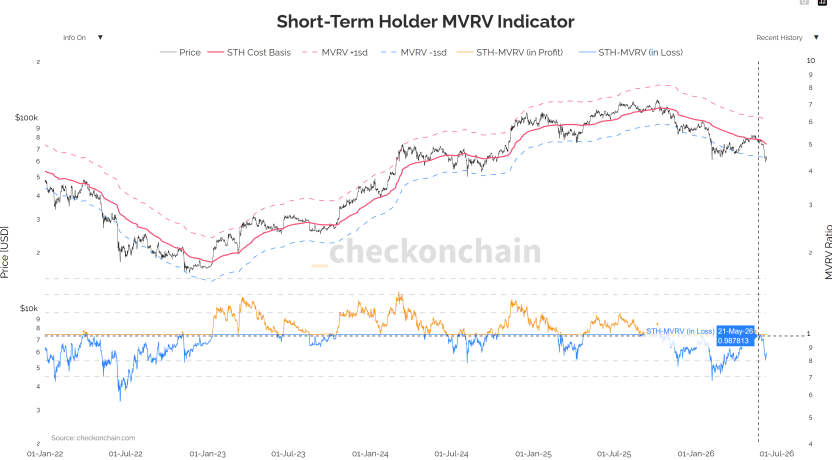

· Second, holder capitulation and forced selling. The short-term holder MVRV ratio fell below the 1.0 breakeven line into loss territory, exhibiting a textbook on-chain capitulation pattern.

· Third, derivatives longs adding leverage against the trend. Open interest counter-trend increased to over $64 billion, with funding rates turning positive. This culminated in a brutal deleveraging event with $307 million in long liquidations (vs. only $90 million in shorts).

May marks the "launch" of a new independent downtrend following the end of a rebound consolidation, representing an "accelerated phase" of cyclical deep bear market cleansing. When it stops no longer depends on the macro environment, but on whether external capital can stop the bleeding and whether the pace of long-term holder distribution can slow down.

1. Macro & Geopolitics: Two Transfers of Pricing Power, Transmission Broken in Final Week

Phase One: Inflation Rebounds Again, Easing Expectations Dashed

The April CPI released on May 12th was the first inflection point of the month. While seemingly moderate on the surface, the structure was deteriorating – core services inflation (supercore) accelerated for the third consecutive month. This is the most sticky dimension, directly linked to employment and wages. The following day, April PPI surged to 6.0%, hitting its highest level since late 2022. Meanwhile, China's PPI turned positive for the first time in 41 months, ending the tailwind of "Chinese goods deflation" that had suppressed global inflation for two years.

The market's focal point for debate underwent a paradigm shift: from "when will rates be cut?" to "how much will rates be raised?". It's important to clarify a time dimension – a rate hike at the next meeting is almost off the table (CME shows over 99.4% probability of no change in June). However, the tail risk for the policy path has been significantly upgraded. The market no longer believes in automatic rate cuts and is instead pricing in the possibility of "forced hikes." This shift alone is sufficient to systematically raise the discount rate for all high-beta assets.

Phase Two: Fed Personnel Earthquake, Reaction Function Becomes Unstable

On May 15th, reformist Kevin Warsh officially took the helm at the Federal Reserve, pushing for a "de-transparency" agenda including abolishing the dot plot and cancelling press conferences. On the same day, the outgoing chairman broke with 75 years of Fed tradition, announcing they would remain as a governor until 2028 to provide internal checks and balances. This represents the deepest internal power split at the Fed since 1951. The market implication lies not in the policy disagreement itself, but in the significantly reduced predictability of the Fed's reaction function. The bond market responded directly: the 30-year Treasury yield surged to 5.19%, a level not seen since the eve of the subprime mortgage crisis, and the Dollar Index hit a six-week high. For assets valued by discounted cash flow, this was a direct and insurmountable blow.

Phase Three: Geopolitical Ice Breaks, But Transmission Chain Fractures

Geopolitics was the core disruptor for oil prices, and consequently the inflation path, in May. The month played out in four acts: "Détente – Setback – Escalation – Breakthrough." Early-month conciliatory statements sent WTI crude down over 7% in a single day, and BTC breached $80,000 for the first time. Mid-month, US-Iran negotiations stalled. Late month saw frequent conflict escalation, with Brent crude hovering around $107–111. The narrative reversed at month-end. On May 28th, the US and Iran reached a 60-day truce memorandum, including "unrestricted passage" through the Strait of Hormuz and Iran clearing naval mines. The geopolitical risk premium was largely digested, and WTI settled at $88.53.

Entering the final week, the negative feedback loop of "geopolitical tension → high oil prices → sticky inflation → rate hike expectations → stronger USD and yields → risk asset pressure" was abruptly interrupted. The 10-year Treasury yield fell ~11 basis points for the week to 4.45%, the Dollar Index dropped to 98.91. The S&P 500 gained 1.43% for the week, the Nasdaq rose 2.39% to record closing highs, and the Nikkei surged over 1,200 points in a single day. Under normal circumstances, this combination of "lower rates, lower oil, lower dollar, higher equities" should have provided significant support for crypto, but the market refused to rally. This is a clear warning sign of crypto's deteriorating fundamentals.

A complete reset of correlations reinforces this point. Mid-month, Asia-Pacific risk aversion (Korea's KOSPI triggered a circuit breaker with a 5% single-day drop) briefly pushed the correlation between BTC and the Nasdaq higher. However, moving into late May, the 30-day rolling correlation coefficient between BTC and the Nasdaq fell significantly and turned deeply negative, hitting a one-year low. The same macro tailwinds were allocated to completely different destinies: stocks rallied together, while crypto fell alone – empirical evidence of this deep negative correlation.

This decoupling has a dual meaning. In the short term, it is objective confirmation that "internal cleansing is dominant" – crypto no longer moves in sync with macro risk appetite but is instead driven by its own capital flows and positioning structure. In the medium term, it suggests that even if US stocks continue to hit new highs, the pull effect on crypto will be extremely limited. Additionally, one must maintain medium-term vigilance: Goldman Sachs warns that global visible crude oil inventories only cover 73 days of demand. Geopolitical détente does not mean oil prices have peaked. The specter of inflation remains, and its impact on risk assets is uncertain.

2. Capital Flows: Monthly ETF Reversal, Coinbase Premium Deteriorates

This is the most directionally significant part of the month, and the most direct evidence of "internal hemorrhaging."

Monthly ETF Flows: A Complete Reversal from Net Inflows in April to Massive Net Outflows in May

Let's start with BTC spot ETFs. April recorded net inflows of $1.966 billion, pushing cumulative net inflows to an all-time high of $58.088 billion, with total net assets breaking $100 billion for the first time, reaching $100.532 billion. Entering May, the flow direction completely reversed – a massive net outflow of $2.425 billion for the full month, the third largest monthly outflow since the product's inception, trailing only February 2025 (-$3.555 billion) and November 2025 (-$3.481 billion). Cumulative net inflows fell back to $55.663 billion, and total net assets shrank to $94.169 billion, evaporating over $6.4 billion in a single month.

The key is that this was an escalating trend within the month, not a one-time shock: cumulative net outflows were already around $1.417 billion by mid-May, expanding further to the full-month outflow of $2.425 billion by month-end. Capital didn't stabilize; instead, it accelerated its flight towards the end of the month.

ETH spot ETFs confirm the same pattern: April still saw net inflows of $356 million with total net assets of $13.253 billion; May turned into net outflows of $541 million, also ranking as the third-largest monthly outflow historically (trailing only November 2025's $1.424 billion and December's $617 million). Cumulative net inflows fell back to $11.37 billion, and total net assets shrank to $11.266 billion. Both BTC and ETH saw net inflows in April and massive net outflows in May, each recording their respective third-largest monthly outflows – this represents a systematic de-allocation by institutions from the entire crypto asset class.

The conclusion is clear: The "ETF marginal buyer" narrative, which had driven the entire uptrend since the halving, has effectively exited the stage in May. The most important channel for new capital went from being a "capital engine" in April to a "sucking pump" in May.

Coinbase Premium: Shifted from Mostly Positive Premium in April to Severely Negative Premium in May

The Coinbase Premium Index is the most direct window to gauge spot buying and selling pressure from US-based institutions. In April, the index still showed mostly positive premium (green), meaning US institutions were net buyers on most trading days, forming the spot-side foundation for April's rebound. Entering May, the index turned almost entirely negative (red) and to a severe degree – as the chart shows, the negative premium zone expanded continuously, with depth nearing the extreme area of -0.22%. This is one of the most persistent and deepest negative premium zones of the past year.

The inflection point where the premium turned from positive to negative aligns perfectly with the reversal rhythm of monthly ETF net outflows, confirming each other. The core driver behind this is an asset reallocation dominated by relative yields – as US Treasury attractiveness rose, US institutions "voted with their feet," swapping BTC positions for Treasury positions. Interestingly, late in the month, even after Treasury yields fell and the arbitrage incentive weakened significantly, the negative premium did not recover, holding steady instead. This suggests that institutional exit has transcended simple "yield comparison" and includes a layer of confirmation regarding expectations for a downward crypto cycle.

Divergence Between Futures and Spot

Concurrent with the ETF slowdown, CME open interest counter-trend grew to over $64 billion. The market shifted from being "spot absorption-driven" to "futures positioning-driven." The so-called "resilience above 80K" was not real incremental capital, but an extension of leveraged positions. The eventual cleansing came in the form of a brutal stampede with $307 million in long liquidations in a single week versus only $90 million in shorts.

3. On-Chain: Comprehensive Breach of Cost Basis Matrix, Capitulation Signal Confirmed

On-chain data portrays the "internal cleansing" even more vividly.

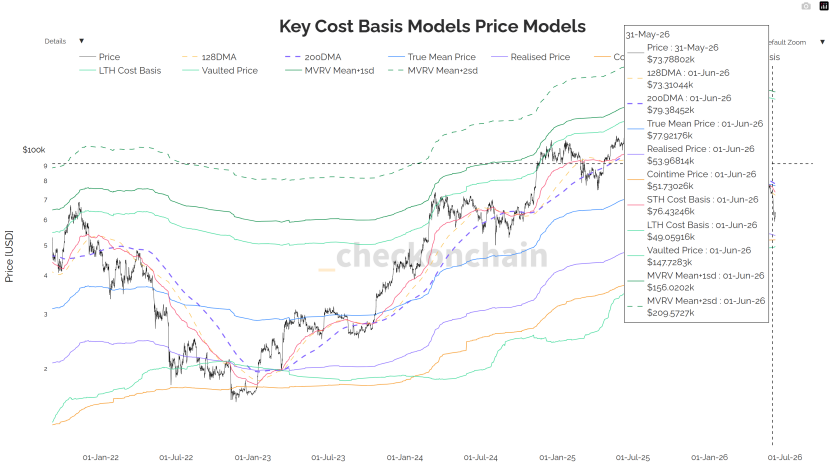

1. Realized Market Mean and 200-Day Moving Average: From Never Holding to Confirmed Loss

According to the Key Cost Basis Models chart, the Realized Market Mean and 200-day MA together form a bull-bear boundary zone repeatedly validated over the past three cycles. In May, this zone was located in the $77K–$79K range. The early-month rebound briefly reclaimed it but failed to hold. A break below on May 18th meant essentially losing the boundary. By month-end, price was trading below this boundary zone, finding factual support at lower moving average areas. This key threshold has turned from support below to a "resistance ceiling" above, meaning all short-term holders are deeply underwater.

2. Realized Profit/Loss Ratio: Falling Instead of Rising

A 30-day MA of this indicator greater than 1 indicates profit-taking dominance. It was at a low of 0.4 in February 2026 and rose to 1.8 by mid-May. However, confirming a switch to a bull market would require it to hold above 2.0. The reality by month-end: it never even touched 2.0, instead falling back to 1.56. Every rally encountered selling pressure from early buyers trying to break even, making each rebound short-lived.

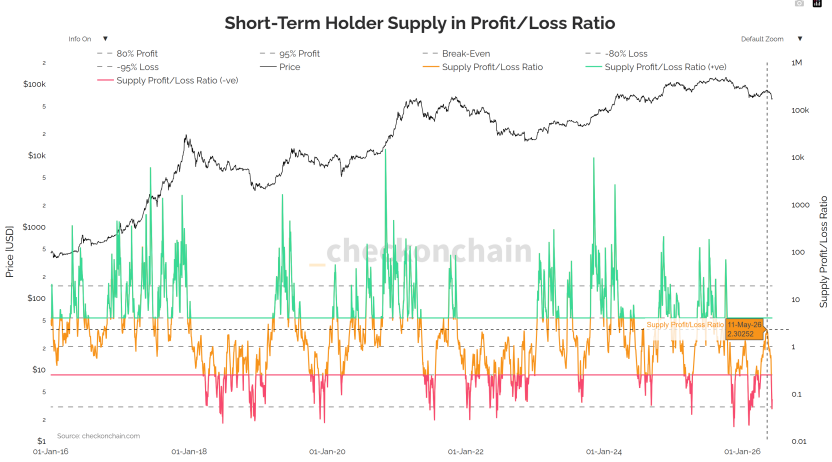

3. MVRV and NUPL: Capitulation Signal Confirmed

The STH-MVRV indicator chart clearly shows the ratio has crossed below the 1.0 breakeven line into loss territory – this is an objective measure of overall short-term holder loss and one of the most recognizable capitulation signals in past deep corrections. The NUPL indicator confirms the deteriorating sentiment. As seen on the chart, NUPL has significantly retreated from the "Optimism – Belief" zone (blue-green) seen earlier this year to the edge of the "Hope – Fear" zone (orange), approaching the critical transition zone seen before the bottom of the 2022 bear market. This is an objective measure of sustained compression in market unrealized profits and a structural decline in risk appetite.

4. Derivatives & Corporate Treasury: Leverage Cleansing and the 75K Psychological Line

1. Market Maker Gamma and Expiry Day Effects

Price stability in early May came from market maker long gamma positioning. BTC was pinned in a narrow $80K range, not due to true supply-demand balance, but a mechanical "price stabilizer" created by market makers holding significant long gamma – selling on rallies, buying on dips, actively compressing volatility. This is why, despite hot CPI and geopolitical tension, BTC's actual volatility actually declined (30D RV fell to 27%).

The consecutive roll-off of two major expiry dates directly changed the market structure. The May 15th monthly expiry saw over $40 billion in notional principal liquidated for IBIT alone. After this massive position rolled off, the market makers' stabilizing capacity waned, and BTC broke below $77.5K on May 18th. The second, more critical monthly expiry on May 29th saw approximately $75 billion in concentrated liquidation across the market. Before the expiry, the spot price had already breached the $75K max pain point and the zone of highest short gamma, causing passive short hedging flows that further heightened late-month selling pressure.

2. The 75K Trap Has Been Triggered

The largest cluster of short gamma was locked in the $75K–$76K range (over $8 billion in negative gamma). Once price fell into this zone, market maker hedging reversed into pro-cyclical selling, creating a downward gamma squeeze. The month-end reality is that this trap was triggered, coinciding with the breaking of the psychological cost basis floor for corporate BTC treasuries. The triple-layer resonance defense line has only one remaining layer – the deeper, cycle-level accumulation cost basis.

3. Skew Defensive Intent Continues to Rise

1M Skew expanded from +2.7% at the start of the month to +6.2% on the day of the breakdown, while 6M Skew remained elevated at +10%. Institutions are not just hedging short-term events; they are building structural downside protection for the entire second half of 2026