Trading volume exceeds Pumpfun, is the AgentFi dark horse Bankr undervalued?

- Core Thesis: Bankr is not a simple token launchpad but an "Agent Runtime" integrating a complete DeFi tech stack, AI agent execution environment, and multi-chain support. Its significant divergence between trading volume and market cap indicates the market is notably underestimating its underlying product and genuine user activity.

- Key Points:

- Severe Inversion of Volume and Market Cap: Bankr's single-day Launchpad trading volume ($74 million) surpasses the total volume of all Pumpfun tokens ($44 million), making it 1.67 times larger. However, Bankr's FDV ($52 million) is merely 1/32nd of Pumpfun's ($1.75 billion).

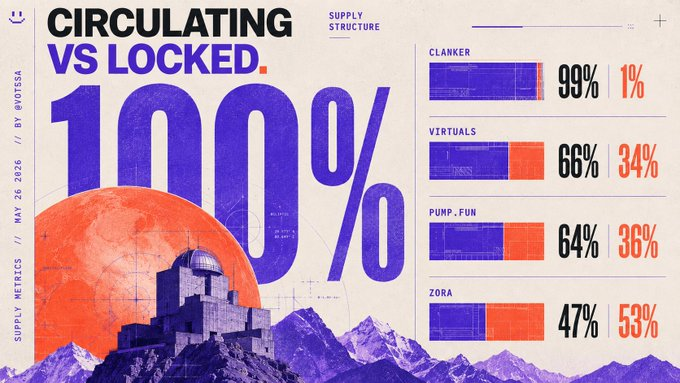

- Zero Funding and Fully Circulating Supply: Bankr was fairly launched in December 2024 with no pre-sale, no VC investment, and 100% of its supply fully circulating from day one. This starkly contrasts with Pumpfun, which raised $1 billion and faces significant unlocks in 6 weeks.

- Fee Treasury Strategy and Cyclical Buy Pressure: Instead of selling the native tokens it earns, Bankr holds them to build a treasury. Its Club subscription service creates cyclical buy pressure through automatic $BNKR purchases (already buying 1.13% of the total supply), which is not captured in traditional valuation models.

- Underperformance Compared to Peers: Despite a high FDV, Virtuals faces declining fees and no holder revenue; Zora's trading volume is 1/580th of Bankr's, yet has a similar market cap with VCs facing a 91% unrealized loss; Clanker saw quarterly revenue plummet 95% after fee restructuring.

- Future-Oriented Expansion Plans: Bankr's core functionality has already been extended to BNB Chain as infrastructure. Its strategy is to first cultivate the Agent ecosystem, and only launch token minting features after validating demand – an approach opposite to models offering direct airdrops.

Original Author: @votesa

Original Translation: AididiaoJP, Foresight News

On May 27, the trading volume of tokens launched on the Bankr platform reached $74 million, while Pumpfun's token trading volume was $44 million. Bankr's FDV is $52 million, compared to Pumpfun's FDV of $1.75 billion.

Despite a 32x difference in market cap, the tokens launched on Bankr generate 67% more trading volume.

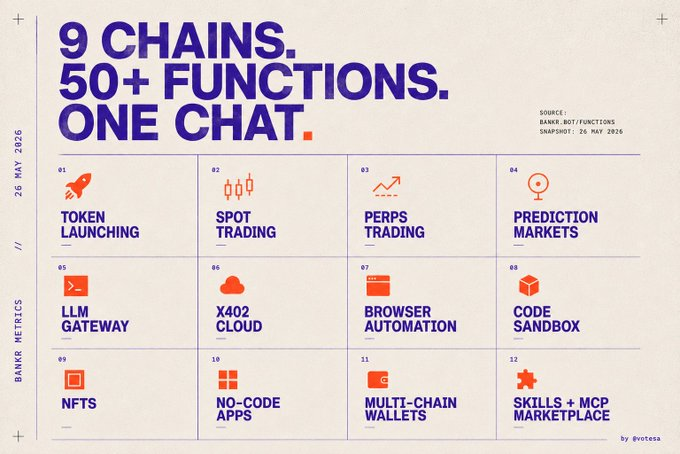

What Exactly is Bankr?

Most people stop at "a Launchpad on Base," which is a trap.

Bankr is closer to an Agent Runtime, encompassing a complete DeFi tech stack:

- Token launches via Doppler

- Spot trading on Uniswap and Aerodrome

- Limit orders, stop-loss, DCA, TWAP

- Leveraged forex and commodities via Avantis

- Hyperliquid perpetuals and spot

- Polymarket positions

- NFTs (buy, sell, mint)

- LLM gateway supporting 30+ models

- x402 cloud for paid API endpoints

- Browser automation with storage credentials

- Code sandbox

- No-code app marketplace

- Skills + MCP directory

All of this operates across 9 chains, with gas sponsored by the protocol on 5 of them.

And it's all integrated with X, Telegram, Farcaster, Discord, XMTP, Web terminal, CLI, and REST API.

The Launchpad is just one feature within this stack, yet this single Launchpad's 24-hour trading volume already surpasses the total volume of all tokens ever launched on Pumpfun.

The Data Speaks

December 3, 2024: BANKR was fairly launched on Farcaster—no pre-sale, no fundraise. The Agent deployed the token directly onto the social platform. Anyone could buy, and the team had to buy alongside everyone else.

18 months later:

- Launchpad cumulative trading volume: $4.35 billion

- Lifetime fees: $26 million (57% to creators, 36.1% to protocol, the rest to ecosystem + launchers)

- Wallets holding BNKR: 187,092

- Zero VC

- 100% of supply fully circulating since day one

Top deployments by total volume:

- MOLT: $283 million

- DRB: $260 million

- CLAWD: $154 million

- KellyClaude, FELIX, etc., each exceeding $40 million+

These are the kind of ranking projects any Base Launchpad would aspire to have.

On the subscription side: Bankr Club generated $404,500 in lifetime revenue from 12,422 recurring transactions, at $20 per month or $198 per year, paid by converting USDC to $BNKR. This is a continuous source of buying pressure that no one factors into their P/F models.

Comparison with Other Projects

Four projects in the same conceptual赛道, one of which raised no funds yet sees daily trading volume increasing, and its market cap is at the bottom of the range.

Pumpfun

Market cap is 11x smaller, FDV is 32x smaller, yet the tokens it launches generate 67% more daily trading volume.

Pumpfun's annualized fees are indeed substantial, that's true. It also raised $1 billion at a $4 billion FDMC, currently down 56% from the public round entry price, and just burned 36% of its circulating supply on April 29.

Burn mitigates supply pressure but simultaneously eliminated the buyback policy—the proportion of revenue used for buybacks dropped from 100% to 50%, effectively halving the engine.

Moreover, on July 12, 2026 (just six weeks away), 82.5 billion tokens (8.25% of the maximum supply) will unlock all at once from the team + investor cliff. The team receives 50 billion, investors receive 32.5 billion, after which it converts to monthly linear vesting until 2029.

@virtuals_io

FDV is 13x smaller, circulating market cap is 9x smaller.

- Virtuals fee revenue: $66.7 million

- Bankr fee revenue: $26 million

- Cumulative fee gap is 2.5x, yet the FDV gap is 13x.

Furthermore, Virtuals' fee rate is on a downward trend: 30-day fees are only $1.19 million, with even worse performance on shorter timeframes.

Holder revenue on DefiLlama: $0. Although the documentation mentions a buyback-and-burn mechanism, there is no standardized on-chain attribution showing it actually happening. The premium is purely based on narrative, not cash flow.

@zora

The daily trading volume of all tokens launched on Zora is only $127,000, compared to Bankr's $73.98 million—a 580x difference, yet their market caps are roughly similar.

Zora raised $60 million in 2022 from Haun Ventures at a $600 million valuation. Series A investors are currently down 91% on paper, and the market cap is now below the amount raised.

@clanker

On February 10, 2026, Bankr migrated from Clanker to Doppler, and Clanker was excluded from the fee stream. What happened in the following quarter:

- Q1 2026 Revenue: $27.58 million

- Q2 Partial: $1.49 million

Revenue plummeted by 95%, perfectly correlating with the fee redirection.

- Bankr Market Cap: $55 million

- Clanker Market Cap: $21 million

After building its own stack, Bankr's market cap is now 2.6 times that of Clanker.

This is the difference between "building a feature" and "building an infrastructure."

Who Are You Trading Against?

This is the part most reports skip.

When you buy, who else is at the table?

- Bankr: Zero fundraise, 100% circulating supply since December 2024, zero upcoming unlocks. No one holds cheap tokens waiting to provide exit liquidity.

- Pumpfun: Raised $1 billion at a $4 billion FDMC, 82.5 billion tokens unlock in six weeks (50 billion team, 32.5 billion investors), followed by monthly linear vesting until 2029. They are already -56% from the public round entry price, with strong motivation.

- Zora: Raised $60 million at a $600 million valuation, 53% of supply still locked. Series A is currently -91%. Upon vesting, they need to exit in the -50% to -90% range just to break even. Any spot buyer is providing them with exit liquidity.

- Virtuals: 34% still locked, standard AI Agent era cliff+vesting structure, same dynamic.

Everyone in this comparison has sold part of their cap table to funds that are either underwater now or waiting to unlock.

Bankr holders face none of these on the other side.

And then there's the hidden value that no one is pricing.

Hidden Value No One Prices: The Fee Wallet Treasury

Bankr does not sell the tokens it receives as fees.

The FairVC Dune dashboard policy is clear: all token fees are held.

The fee wallet's current value is approximately $1.31 million, spanning over 50+ holdings.

Top holdings include:

- Aeon: $235,000

- NOOK: $114,000

- Surplus: $104,000

- MiroShark: $75,000

- cyb3rwr3n: $58,000

Plus 47+ smaller positions, along with protocol fee WETH and USDC.

The numbers fluctuate with the price of launched tokens, but the key is the policy.

Other Launchpads dump the native tokens they earn; Bankr chooses to hold.

This means there is one less seller on the order book for every token launched on Bankr.

Club Subscription Buying Pressure

Each $20 subscription converts USDC to $BNKR via DEX buy. With 12,422 transactions, 1.13% of the total supply has been bought.

Recurring monthly, hardcoded into the product. No one factors this into their P/F models.

Doppler's Institutional Endorsement (Indirect)

Bankr currently uses Doppler as its active launch backend. Doppler raised $9 million in Q2 2025 from Pantera, Variant, Figment, and Coinbase Ventures. Bankr inherits the institutional signal of the Doppler stack with zero dilution—others have already paid for the rails.

Bankr Fund

They are starting to put the treasury to work. Bankr just announced a fund to directly invest in projects within its own ecosystem.

A Launchpad that earns native tokens on every launch, holds them, and is now recycling capital back into the Agent ecosystem that feeds it.

Compare this to @virtuals_io (zero return to holders) or @zora (the only liquid money is the Series A trying to exit at -91%).

Bankr is the only one in this group that simultaneously has:

- An organically growing treasury every day

- A clear plan to reinvest the treasury into the ecosystem that sustains it

Next Moves

Bankr is expanding to BNB Chain.

On May 21, 2026, @BNBCHAIN launched the Agent Survival Pack—a 6-partner program aimed at enabling AI Agents to pay their own operational costs on-chain. Bankr is the first designated partner.

This is Bankr methodically opening a new market. The inference rail is already live. The team has publicly stated that once suitable creators are ready on BNB Chain, the next step is token launches.

The strategy is patient and correct: serve the Agents first, and only launch the Launchpad once demand is proven.

This is the complete opposite of how almost every other Launchpad approaches multi-chain expansion—they throw the Launchpad into an empty ecosystem and wonder why no one shows up.

Trading Thesis

If the category "multi-chain Agent Runtime + Full DeFi Stack" exists, Bankr is the only candidate on Base with all the following attributes:

- Real activity, not narrative

- A self-sustaining treasury

- A cyclical buying pressure mechanism

- An active investment fund

- Zero upcoming unlocks

Other contenders:

- Virtuals: Excessive narrative premium (9x market cap gap, fees declining)

- Pumpfun: Excessive VC fundraise premium ($1 billion sunk, cliff in six weeks)

- Zora: Excessive VC fundraise premium, Series A -91%

- Clanker: Revenue cliff-diving (Q1 to Q2 -95%)

The market has not yet priced this category.

Once it does, the revaluation will come from Bankr's own capital base, not from funds waiting to dump.

Once you understand how this founder operates, the data above no longer looks like luck, but rather the compounded output of one of the most undervalued creators on Base.