BitMart VIP Insights | May Crypto Market Review and Hotspot Analysis

- Core Viewpoint: In May 2025, the macro environment of "high inflation + hawkish bias" intensified, leading to a "surge followed by a pullback" trend in the crypto market. Key hotspots centered around the regulatory compliance push driven by the CLARITY Act and the upgrade of on-chain financial infrastructure powered by Uniswap V4. Institutional capital clearly concentrated on BTC, while ETH and SOL faced relative downward pressure.

- Key Elements:

- Macro Pressure Dominates Market Sentiment: The US April CPI rose to 3.8% year-over-year. FOMC minutes revealed internal分歧 at its highest level since 1992, pushing expectations for a rate cut this year to nearly zero, leading to increased volatility in risk assets.

- Crypto Market Cap Rose Then Fell: The total market capitalization rose to a monthly high of $2.821 trillion at the beginning of the month, but quickly declined due to hawkish signals, ending the month at $2.657 trillion, essentially erasing all gains for the month.

- Performance Divergence Among Core Assets: BTC pulled back after breaking $80,000 but still exhibited "resilience" characteristic of institutional holdings; ETH fell about 11% month-over-month, impacted by declining institutional preference; SOL underperformed BTC, hampered by slow recovery in ecosystem liquidity.

- Regulatory Legislation Reached a Milestone: The CLARITY Act passed the Senate Banking Committee by a vote of 15-9, establishing a dual-track classification standard for digital assets as commodities/securities, seen as a significant turning point in the US crypto regulatory framework.

- On-Chain Financial Infrastructure Upgrade: The Uniswap V4 Hook ecosystem exploded, pushing DeFi into the era of "programmable liquidity"; Hyperliquid reached an all-time high driven by ETF and derivatives expansion, focusing on high-growth on-chain financial platforms.

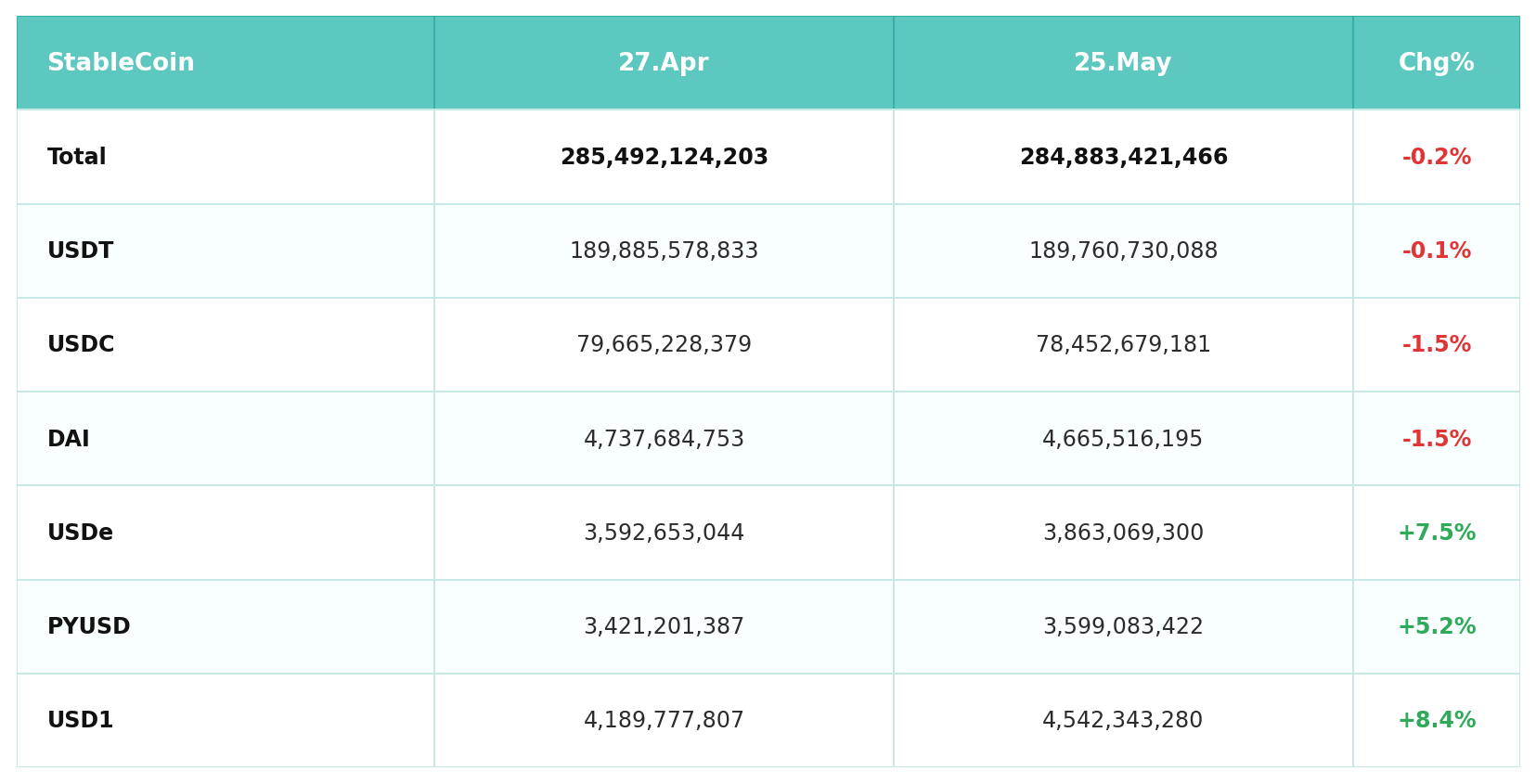

- Capital Structure Shift and Rise of New Stablecoins: The total stablecoin market size remained largely flat, but USDT and USDC experienced slight contractions. Meanwhile, emerging compliant stablecoins like USD1 and USDe grew against the trend, reflecting a capital shift towards yield-bearing and compliant types.

TL,DR

- The overall macro environment in the US in May presented a pattern of "high inflation + hawkish expectations." Fed meeting minutes revealed significantly intensified internal policy分歧, and market expectations for a rate cut this year rapidly cooled. Meanwhile, the April CPI rose to 3.8% year-over-year, further strengthening market pricing for higher rates for longer. Concurrently, US stocks maintained strength driven by AI capital expenditure expansion and better-than-expected tech earnings, but experienced a phase correction at the end of the month due to inflation and hawkish signals, leading to distinctly increased volatility in risk assets.

- The crypto market in May showed a "surge and retreat" trend. Early in the month, trading volume and total market cap strengthened alongside回暖 risk appetite and a BTC rally. However, impacted by hawkish Fed signals in mid-to-late May, the market exhibited clear divergences between price and volume, with signs of capital withdrawal. Total market cap briefly rose to a monthly high before rapidly declining. It stabilized slightly at the end of the month, but most of the gains were given back, indicating that macro pressures still dominate market sentiment. Among newly listed projects, GENIUS and BILL represented two major narratives favored by current capital: on-chain trading infrastructure and AI identity verification, reflecting the ongoing preference for projects with strong narratives in AI, compliance, and infrastructure.

- ETF flows in May presented a pattern where "BTC was relatively resilient, while ETH faced sustained pressure." Although BTC ETFs saw net outflows in some phases, their cumulative capital scale remained at historical highs, indicating that institutions' long-term allocation logic has not fundamentally changed. In contrast, ETH ETFs experienced more pronounced capital outflows and liquidity pressure, reflecting that current institutional risk appetite remains clearly tilted towards BTC. The total stablecoin market cap remained largely stable, with USDT and USDC contracting slightly, while emerging stablecoins like USD1, USDe, and PYUSD grew against the trend, signaling a capital shift from traditional trading stablecoins towards yield-bearing and compliant stablecoins.

- BTC overall showed a "rally followed by correction" in May. It briefly breached the $80,000 mark and set a new phase high, but subsequently fell back due to higher-than-expected inflation, hawkish Fed rhetoric, and ETF outflows, cooling market sentiment significantly. In contrast, ETH and SOL underperformed BTC. ETH faced headwinds from declining institutional capital preference, while SOL was affected by a slow recovery of ecosystem liquidity, indicating that current market capital remains concentrated in core assets like BTC.

- The core hotspots in the crypto market in May centered on two main themes: "regulatory compliance" and "on-chain financial infrastructure upgrades." The advancement of the CLARITY Act is seen as a crucial turning point for the US crypto regulatory framework, while the SEC's proposed "innovation exemption" for tokenized stocks further strengthens the long-term narrative for RWA and on-chain securities markets. Concurrently, Hyperliquid hit an all-time high driven by ETFs and the expansion of on-chain derivatives, reflecting that market capital is refocusing on high-growth on-chain financial platforms. In DeFi, the explosion of the Uniswap V4 Hook ecosystem propelled "programmable liquidity" as a new narrative.

- In June, the market will closely watch the first FOMC meeting chaired by Warsh and the latest dot plot. The Fed's stance on inflation and the interest rate path will directly impact Treasury yields, BTC trends, and overall risk appetite. On the regulatory front, the CLARITY Act enters the full Senate voting stage. If it proceeds smoothly, it will further define the digital asset regulatory framework, accelerating institutional capital inflow, ETF adoption, and the development of compliant stablecoins. Meanwhile, Hong Kong's stablecoin HKDAP has completed testing on the Ethereum mainnet and is planned for formal issuance at the end of Q2, suggesting that the competition for compliant stablecoins in Asia, along with on-chain payments and RWA ecosystem development, may heat up further in June.

1. Macro Perspective

Policy Direction

In May, the Federal Reserve's policy framework underwent its most significant leadership transition in the current cycle. The minutes of the Fed's April 28-29 FOMC meeting (the last chaired by Powell), released on May 20, revealed that internal policy分歧 reached the highest level since 1992. Of the four dissenting votes, Governor Stephen Milan favored a 25bps rate cut, while Presidents Hammack, Kashkari, and Logan opposed retaining dovish language in the statement, effectively calling for a stronger stance. The minutes also showed that a majority of officials clearly stated that if inflation persists above the 2% target, rate hikes would become an "appropriate option." Market pricing subsequently adjusted significantly, with expectations for a rate cut this year nearly evaporating and the implied probability of a rate hike between end-2026 and early 2027 rising notably.

On the personnel front, the Senate confirmed Kevin Warsh as the 16th Chair of the Federal Reserve on May 13 by a vote of 54 to 45, the narrowest margin in modern history, largely along party lines with only Democratic Senator Fetterman of Pennsylvania crossing the aisle to support. Powell's term officially ended on May 15. Warsh's first FOMC meeting as Chair is scheduled for June 16-17, where a new dot plot and Summary of Economic Projections will be released. The market will scrutinize his every word with maximum sensitivity.

US Stock Market Trends

The US stock market largely continued its strength in May. The S&P 500 recorded positive returns for eight consecutive weeks, the longest winning streak since December 2023. The Nasdaq rose in seven out of eight weeks. The Dow Jones Industrial Average closed near 50,580 on May 22, hitting a phase high during the month. The primary driver was a better-than-expected Q1 earnings season, with major tech companies generally reporting strong profits and AI capital expenditure expansion boosting sentiment. Phased progress in US-Iran ceasefire negotiations also provided external support for risk assets. In late May, the April CPI jumping to 3.8% and the hawkish signals from the meeting minutes triggered a brief pullback, but overall US stock resilience remained robust.

Inflation Data

The US Bureau of Labor Statistics released the April CPI on May 12: CPI grew 3.8% year-over-year, the highest since May 2023, with a month-over-month increase of +0.6% (down from +0.9% in March but still significantly above expectations). Core CPI (excluding food and energy) was +2.8% year-over-year and +0.4% month-over-month, both above forecasts. By component, energy prices rose another 3.8% month-over-month in April, continuing the pass-through from the March oil price shock. The shelter index increased +0.6% month-over-month, remaining stubbornly high. Food prices rose +0.5% month-over-month, with food at home up +0.7%. Overall, the higher-than-expected inflation dashed market hopes for a natural decline in inflation after the energy shock subsided. The 2.8% year-over-year core reading makes it difficult for the Fed to resume a dovish stance anytime soon.

Employment Data

The US Department of Labor released the April nonfarm payrolls report on May 8: Nonfarm payrolls increased by 115,000, slowing significantly from the revised 185,000 in March, but still above the average market expectation previously lifted by rebound sentiment from the ceasefire. The unemployment rate held steady at 4.3%, while the labor force participation rate ticked up slightly. Average hourly earnings rose 3.6% year-over-year and +0.2% month-over-month to $37.41, suggesting wage inflation pressure is manageable. Job gains were primarily in healthcare (+37,000), transportation and warehousing (+30,000), and retail trade (+22,000). Federal government employment continued to decline, while the information and manufacturing sectors saw slight decreases. Overall, the April employment data shows a "moderate slowdown" rather than a rapid deterioration. In the context of persistently high inflation, this neither triggers a rate cut for the Fed nor provides an urgent reason for a rate hike, further narrowing the policy window.

Political Factors

The US-Iran ceasefire was the core geopolitical variable throughout May. Following the initial truce on April 8, a new two-week temporary ceasefire agreement was reached between the US and Iran through Pakistani mediation in early May. The US also advanced "Operation Freedom" to secure commercial shipping in the Strait of Hormuz. Brent crude oil fell sharply from its peak to around $94.80/barrel, and WTI dropped to near $95.75. However, the fragility of the ceasefire was prominent, as Iran's Supreme National Security Council continued to reject the full reopening of the strait, and oil prices subsequently rebounded to around $108 for Brent. The phased détente in the ceasefire provided breathing room for global risk assets and was a key macro catalyst for BTC's breakout above $80,000.

On the crypto regulatory legislative front, the full text of the "Clarity in Digital Assets Market Act" (CLARITY Act) was published by the Senate Banking Committee on May 11. It passed the committee markup on May 14 by a vote of 15 to 9, advancing to the full Senate for consideration. This is a substantive step forward following the committee's markup in late April. Polymarket's probability of it passing within the year subsequently rose to over 85%.

Outlook for Next Month

Looking ahead to June, Warsh's first FOMC meeting (June 16-17) is the most critical macro event. The updated interest rate dot plot will be released simultaneously, and the market will be highly sensitive to his weighting of inflation versus employment. If the April inflation readings of 3.8% headline and 2.8% core persist, Warsh will face significant pressure. If he adopts a notably hawkish tone, Bitcoin's ability to hold above $75,000 will be tested. The May CPI data, released on June 10, will be the final key inflation input before the dot plot. On the legislative front, the outcome of the full Senate vote on the CLARITY Act will be the most important regulatory signal of this cycle.

2. Crypto Market Overview

Token Data Analysis

Trading Volume & Daily Growth Rate

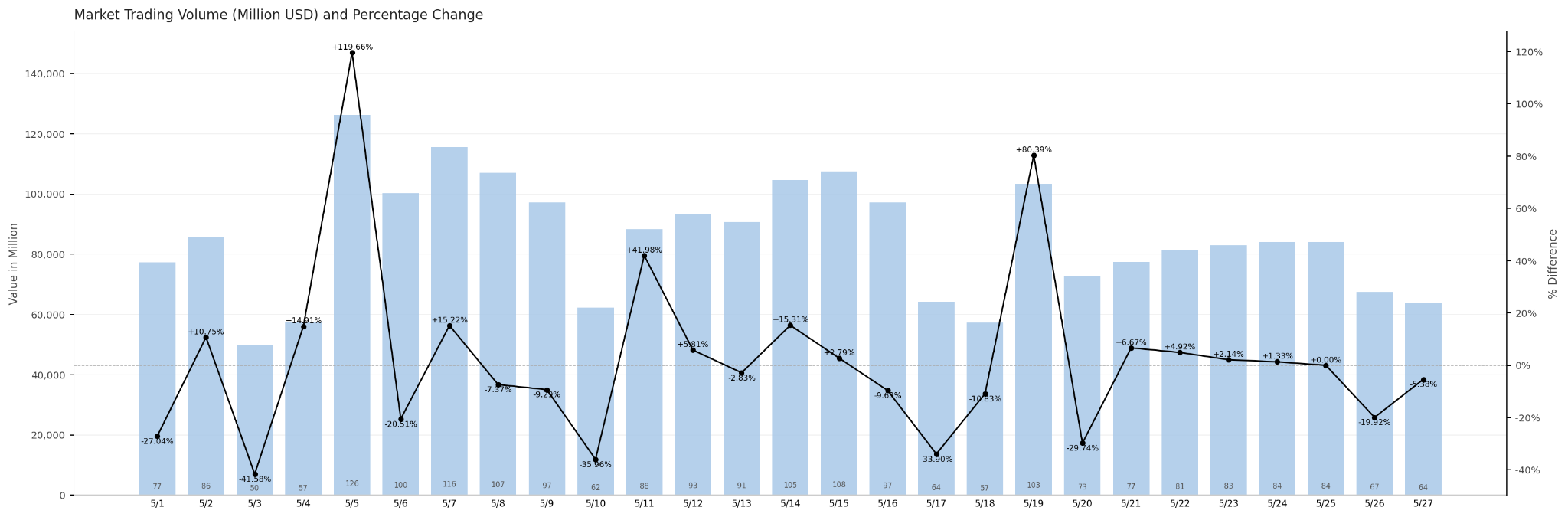

Market trading volume remained active overall in May, but structurally showed a clear "price-volume divergence" signal. Volume concentrated in two phases during the month. The first phase was from May 5 to 7, with daily turnover reaching $126.2 billion, $100.3 billion, and $115.6 billion, the highest levels of the month. Market capitalization rose concurrently, a classic feature of a volume-driven, trending upward movement. The second phase occurred around May 14-15 and May 19, when volume surged back to the hundred-billion level, but market capitalization declined simultaneously. This divergence suggesting rising prices on increasing volume indicates dominant short-side forces and concentrated selling pressure. At the end of the month (May 26-27), volume shrank to $67.4 billion and $63.7 billion, the lowest range of the month, indicating conservative short-term sentiment and increased participant观望 willingness. Overall, the volume structure in May reveals a complete sentiment evolution chain: from "chasing rallies" to "cutting losses and fleeing" to "lurking in观望."

Total Market Cap & Daily Change

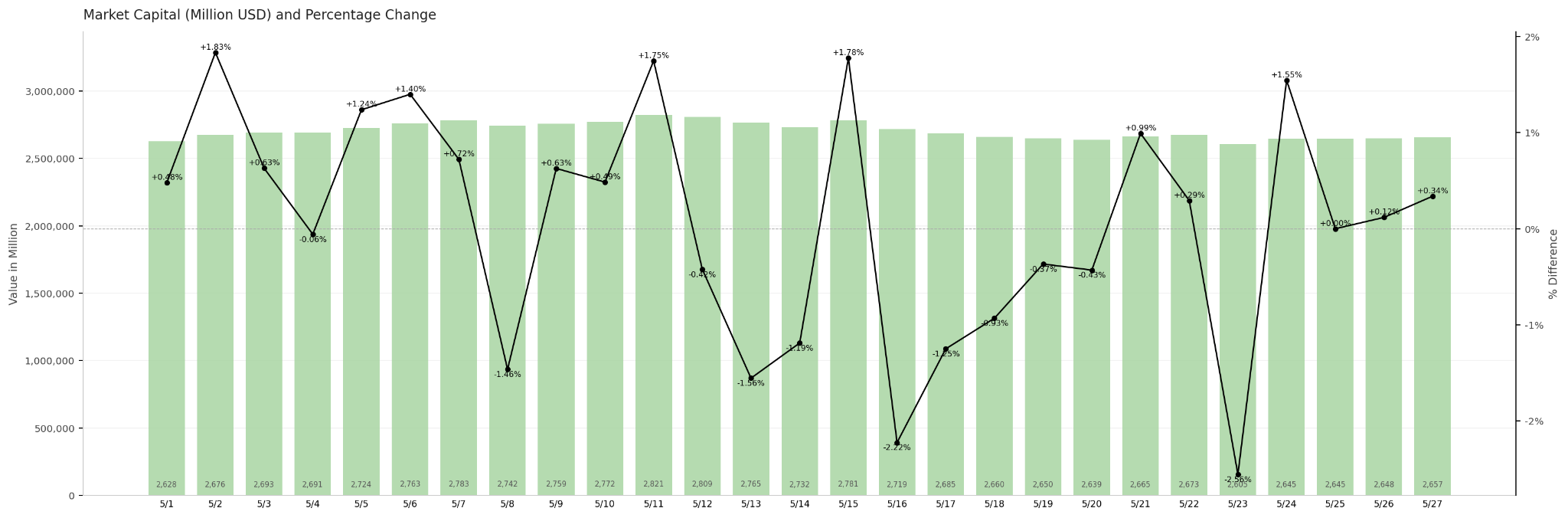

The total cryptocurrency market cap showed a "rise first, then fall, stabilizing at month-end" trend in May. Starting from the late-April base of $2.615 trillion, market cap climbed steadily as risk appetite improved and BTC broke through $80,000, reaching a monthly high of $2.821 trillion on May 11, up 7.8% from the start of the month. However, the uptrend was short-lived. The hawkish signals from the May 20 FOMC meeting minutes caused a sharp reversal in sentiment. Market cap rapidly declined from its peak, hitting a monthly low of $2.605 trillion on May 23, a drop of about 7.7% from the peak. It rebounded slightly to $2.657 trillion by month-end, roughly flat (+1.6%) compared to the end of April, with almost all monthly gains erased. Overall, the "surge and retreat" pattern of the total market cap in May clearly maps the suppressing effect of macro disturbances on crypto market sentiment – short-term catalyst-driven rallies struggle against systemic risk aversion.

Trending Tokens in May

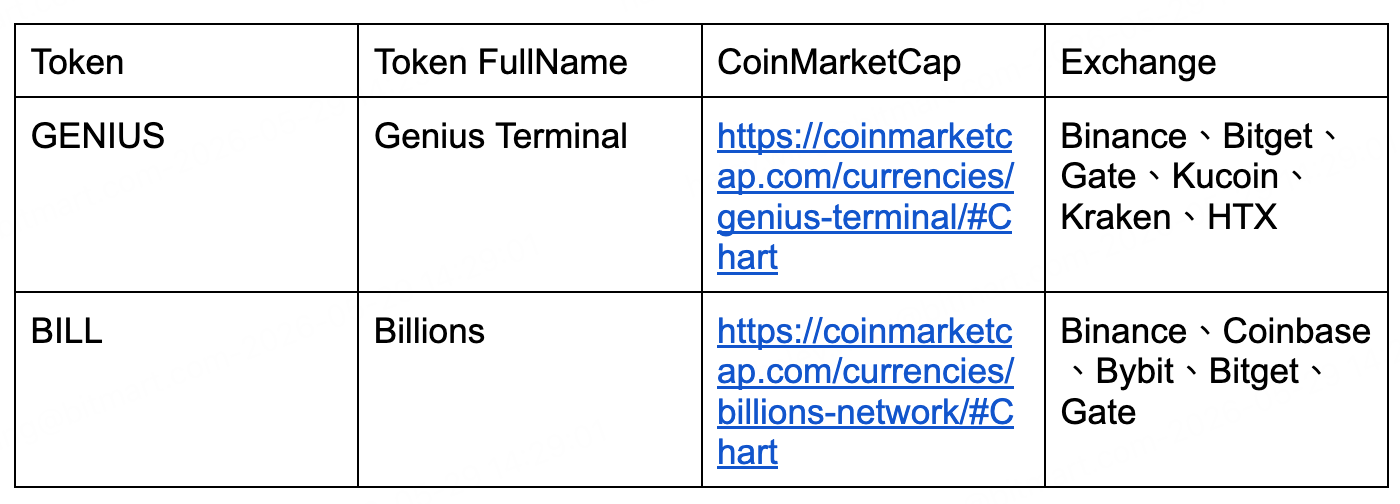

Among tokens newly listed in May, GENIUS and BILL represent the two main narratives currently favored by capital: on-chain trading infrastructure and AI identity verification. GENIUS, incubated by YZi Labs, is positioned as an integrated on-chain trading operating system. In its first week on Binance, its trading volume exceeded $2 billion. BILL, leveraging a ZK-proof-driven decentralized human identity protocol, backed by Coinbase Ventures and Polychain, surged over 10x from its TGE price. The common characteristics are strong backer endorsements, simultaneous listings on major exchanges, and clear product narratives, confirming that projects resonating with macro themes like AI and compliant infrastructure still command a significant liquidity premium in the current market environment.

Among tokens newly listed in May, GENIUS and BILL represent the two main narratives currently favored by capital: on-chain trading infrastructure and AI identity verification. GENIUS, incubated by YZi Labs, is positioned as an integrated on-chain trading operating system. In its first week on Binance, its trading volume exceeded $2 billion. BILL, leveraging a ZK-proof-driven decentralized human identity protocol, backed by Coinbase Ventures and Polychain, surged over 10x from its TGE price. The common characteristics are strong backer endorsements, simultaneous listings on major exchanges, and clear product narratives, confirming that projects resonating with macro themes like AI and compliant infrastructure still command a significant liquidity premium in the current market environment.

3. On-Chain Data Analysis

Analysis of BTC and ETH ETF Inflows and Outflows

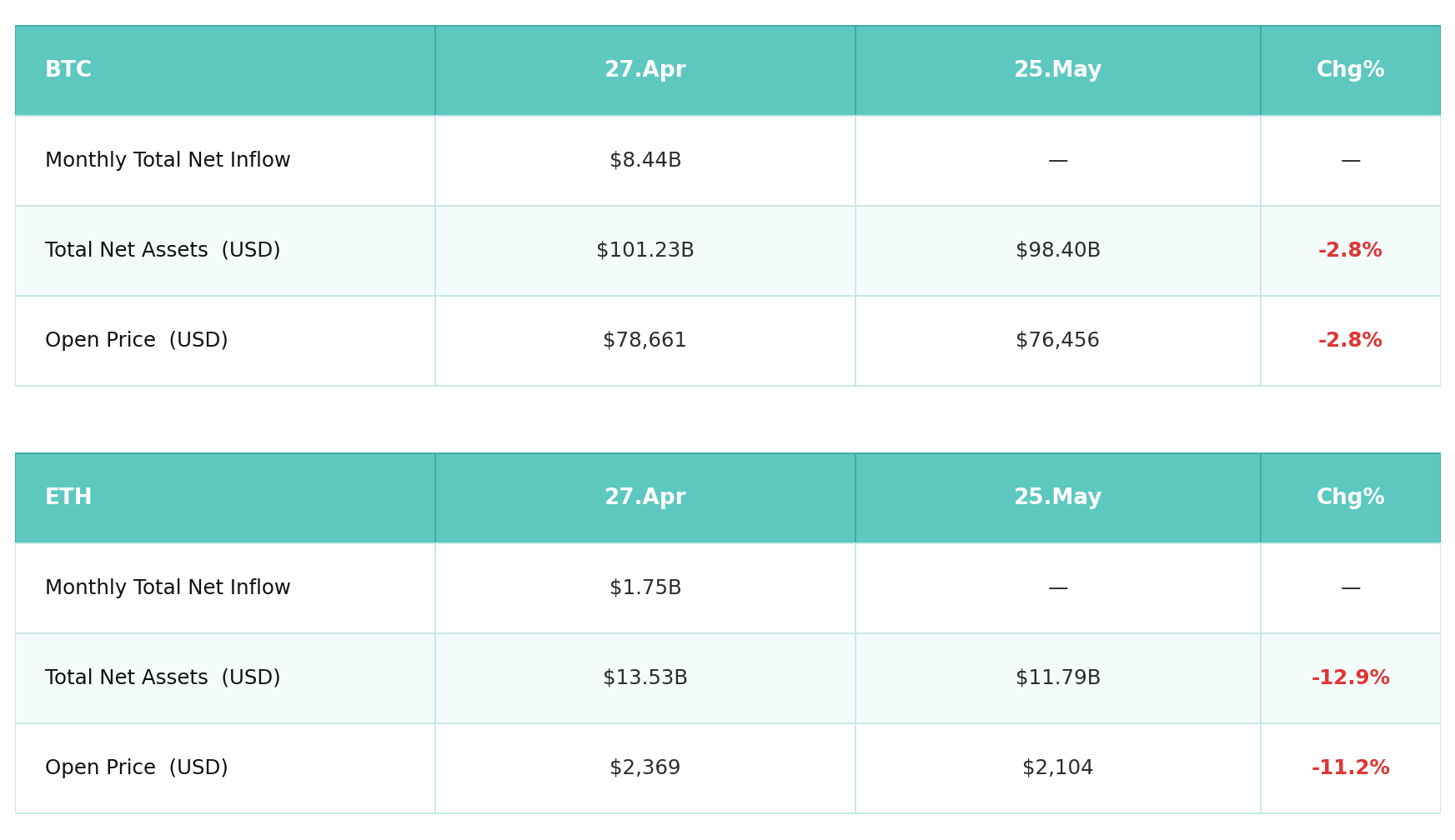

Bitcoin spot ETFs faced overall pressure in May. Net asset value fell from $101.23 billion at the end of April to $98.40 billion (-2.8%), roughly in line with the BTC price decline, indicating relatively stable holdings. The asset shrinkage was mainly price-driven rather than due to large-scale redemptions. As of May 26, BTC ETFs saw a single-day net outflow of $334 million, but cumulative net inflows accumulated to a historic high of $56.75 billion, indicating that the long-term institutional allocation logic remains intact. ETH ETFs faced more pronounced pressure: net asset value fell from $13.53 billion to $11.79 billion (-12.9%). The ETH price dropped 11.2% during the month, and combined with marginal net capital outflows, both factors dragged on performance. On May 26, ETH ETFs saw a single-day net outflow of $35.04 million, with daily turnover of only $614 million, significantly lagging BTC ($4.4 billion), indicating that institutional willingness to allocate to ETH remains notably weaker than to BTC. Overall, the May ETF data presents a pattern of "BTC resilience vs. ETH pressure," consistent with the phased contraction in risk appetite. However, the large cumulative position base also suggests that institutional capital has not entered a systemic withdrawal mode.

Analysis of Stablecoin Inflows and Outflows

The overall stablecoin market size was largely flat in May. Total circulation contracted slightly from $285.49 billion on April 27 to $284.88 billion on May 25 (-0.2%), showing no systemic capital exodus from the market. Structural divergence is more noteworthy: the two major stablecoins, USDT (-0.1%) and USDC (-1.5%), saw modest shrinkage, possibly related to some institutions reducing on-chain exposure amidst rising macro uncertainty (Moody's downgrade of US sovereign rating, hawkish FOMC stance). In contrast, emerging stablecoins expanded against the trend: USD1 grew 8.4%, USDe grew 7.5%, and PYUSD grew 5.2% during the month. The rapid scaling of USD1 is particularly notable, highly resonating with improved regulatory expectations driven by the CLARITY Act legislative progress. Overall, the stabilization of total stablecoin supply means market "dry powder" is ample, while the structural shift towards new players reflects capital making early moves to position in the compliant regulatory track.

4. Analysis of Major Currency Prices

Bitcoin (BTC) Price Analysis

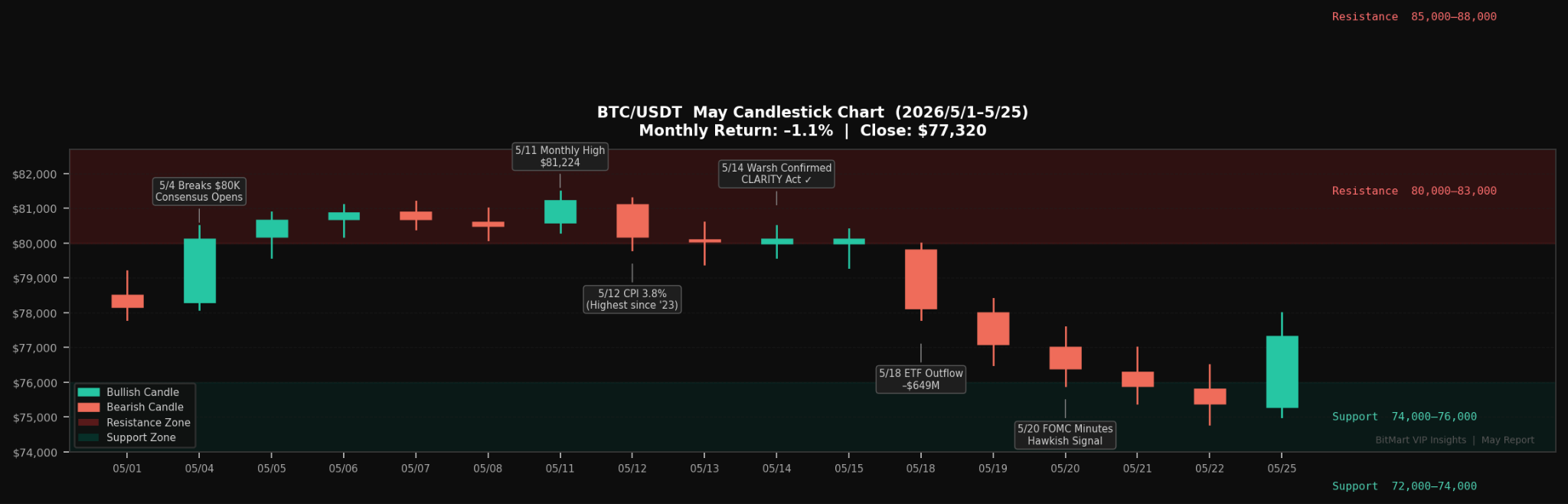

In May, Bitcoin completed its most anticipated technical breakout of the year so far, followed by a notable correction. The monthly trend exhibited a three-phase structure: "volume-driven breakout – institutional profit-taking – ETF capital withdrawal."

BTC started from around $78,661 at the end of April, closing at $78,178 on May 1. Benefiting from the geopolitical ceasefire, the tug-of-war intensified around the $80,000 level. On May 4, BTC closed above $80,000 for the first time since January 2026, triggering about $300 million in short liquidations and creating a brief mechanical upward acceleration. BTC hit a monthly high of $81,224 on May 11. Subsequently, following the release of the April CPI data on May 12 (3.8% YoY, well above expectations) and the FOMC meeting minutes on May 20 revealing a hawkish lean among most officials towards rate hikes, market sentiment cooled rapidly. Starting May 18, US spot BTC