A 10,000-Word Deep Dive into On-Chain Treasuries: Among Eight Major Tracks, Who Is Rising and Who Is Declining?

- Core Thesis: The article provides a quantitative analysis of the blockchain "treasury" landscape, breaking it down into eight categories. It points out that overall TVL has dropped approximately 50% from its peak, but RWA treasuries have bucked the trend with a 37.8% increase. The author emphasizes the need to examine the structural shift in treasuries from the perspectives of modular lending, risk curation, and asset types.

- Key Elements:

- Treasuries are defined as tools for users to access active yield-generating strategies, excluding pure off-chain asset wrappers such as BlackRock's BUIDL.

- Categories like lending, liquid staking, and restaking have been hit the hardest, while RWA treasuries, having no crypto asset exposure, have shown uncorrelated growth.

- The curator model, driven by platforms like Morpho, is modularizing lending treasuries, with its TVL on Ethereum and Base exceeding $7.5 billion.

- Risk-curated treasuries are growing rapidly, with a TVL of approximately $6.5 billion, but 75% is concentrated among the top three curators: Sentora, Steakhouse, and Gauntlet.

- RWA treasuries have a five-year compound annual growth rate (CAGR) of 231.3%. Platforms like Maple Finance benefit from product composability, but leveraged revolving loans face risks of liquidation and redemption delays.

- Perpetual contract LP treasuries, such as Jupiter Perps, have seen TVL decline due to market volatility. Hyperliquid HLP once suffered significant losses after traders manipulated positions.

- Option treasuries are attempting a revival through RFQ systems and optimized designs (e.g., Derive V2), but the overall category remains subdued compared to its peak.

Original Author: Castle Labs

Original Translation: Jiahuan, ChainCatcher

This article is excerpted from our research on "Treasurification".

Vault Taxonomy

This section of the report provides a quantitative analysis of the vault landscape to offer a comprehensive picture of the sector and its evolution. We analyze the ecosystem by category, tracking TVL shifts across different vaults and curators.

We break down curator concentration and provide an outlook on major capital flows, contextualizing the structural shifts that will define vaults this year.

Vaults should not be viewed as a single, monolithic market but should be assessed by their distinct implementation methods, each with different parameters, risk vectors, and stress test responses. Aggregated data only provides a partial picture, urgently requiring a more granular analytical perspective.

Before starting the analysis, it is important to define the term "vault" as the foundation of our methodology.

Our definition is based on the deployment path. A vault is categorized as a "tool for users to actively seek yield-generating strategies". Any asset that is purely a wrapper for off-chain instruments is excluded from our analysis.

Maple's syrupUSDC meets the vault criteria: users deposit stablecoins into the protocol, which lends them to institutional borrowers, accumulating APY through the yield generated by the credit activities of the issued token.

Lido stETH is a vault: users deposit ETH, the protocol earns staking rewards, which are distributed via a rebasing token. Centrifuge JAAA is a vault: users gain exposure to AAA-rated CLO yields through a tokenized wrapper that generates returns from its credit positions.

BlackRock's BUIDL is not a vault under this definition: it is a direct token issuance representing a 1:1 claim on an off-chain US Treasury fund.

Applying this perspective, we have defined eight structural categories: Lending Vaults, Liquid Staking, Restaking, Risk-Curated Vaults, Vault Infrastructure Providers & Yield Optimizers, RWA Credit Vaults, Perpetual LP Vaults, Options Vaults.

For the purpose of this analysis, we treat Risk-Curated Vaults as a separate category to better understand their dynamics and growth.

Before diving into each category, let's first examine the overall performance of vaults.

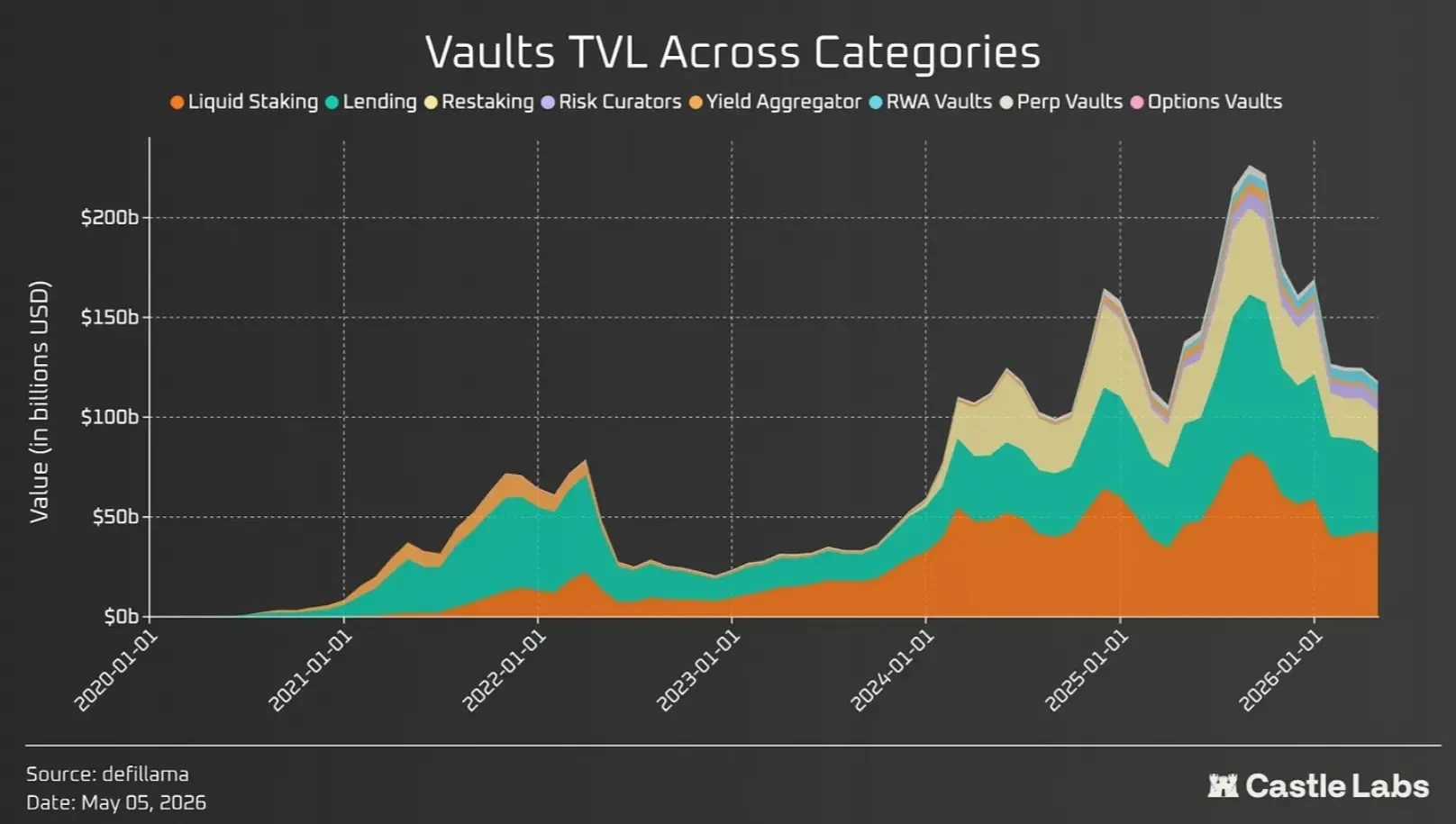

Current State of the Vault Ecosystem

The net TVL for all defined vault categories totals $120.4 billion, a decline of approximately 50% from its peak of around $241 billion in October of last year. The downward trend post-October peak was driven by the "October Liquidation Event," which triggered cascading liquidations across DeFi.

Due to overlaps, vault TVL figures are higher than the current DeFi TVL (~$86 billion). For example, liquid staking protocols like @LidoFinance issue stETH, a rebasing asset representing staked ETH yield, which is used as collateral in lending protocols like @Aave and @Morpho.

If we move to a category-level analysis, the overall picture changes drastically. Recent events have led to TVL outflows and prompted a broader reality check on security and risk management across the industry (hopefully steering towards a security-first approach).

Categories like Lending, Liquid Staking, and Restaking were hit the hardest due to their significant exposure to on-chain assets that drive the on-chain economy; meanwhile, RWA vaults, with no crypto asset exposure, continue to show uncorrelated growth.

Categories like Options Vaults peaked in April 2022 and have struggled since. Risk-curator-led vaults suffered hits comparable to other major categories due to the "October Liquidation Event." Their TVL peaked around late October and subsequently declined following the Stream Finance collapse.

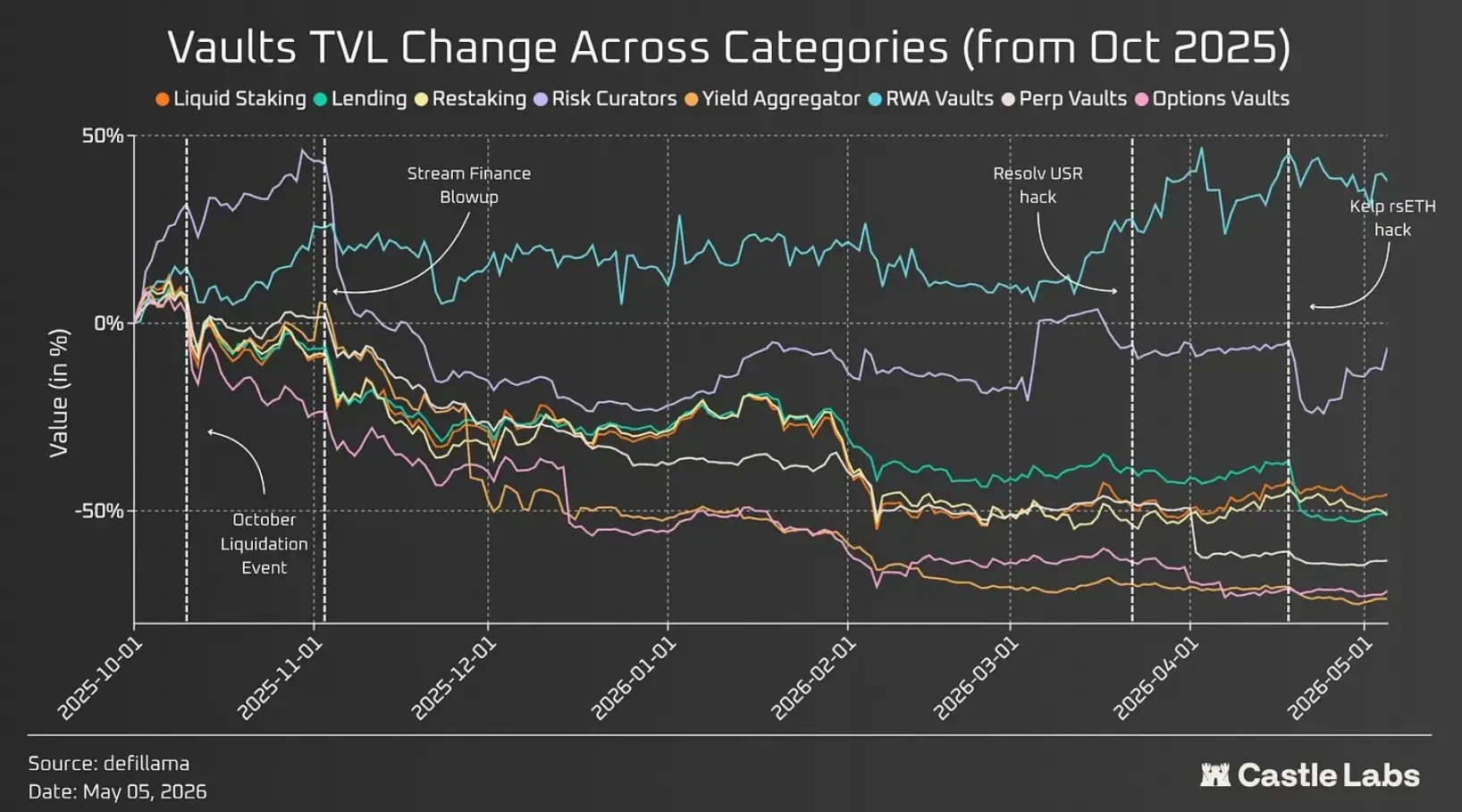

The three incidents between October 2025 and May 2026 (Stream Finance, Resolv, and Kelp hacks) provided a good stress test window, as these crashes/exploits had cascading effects across DeFi.

In the chart below, we highlight the TVL history of these categories during this specific period. As mentioned, most underperformed, with only RWA vaults growing by 37.8% over the same period, while other categories experienced significant pullbacks.

Next, we continue to analyze the growth of each vault category, focusing on recent trends and shifts.

Lending Vaults

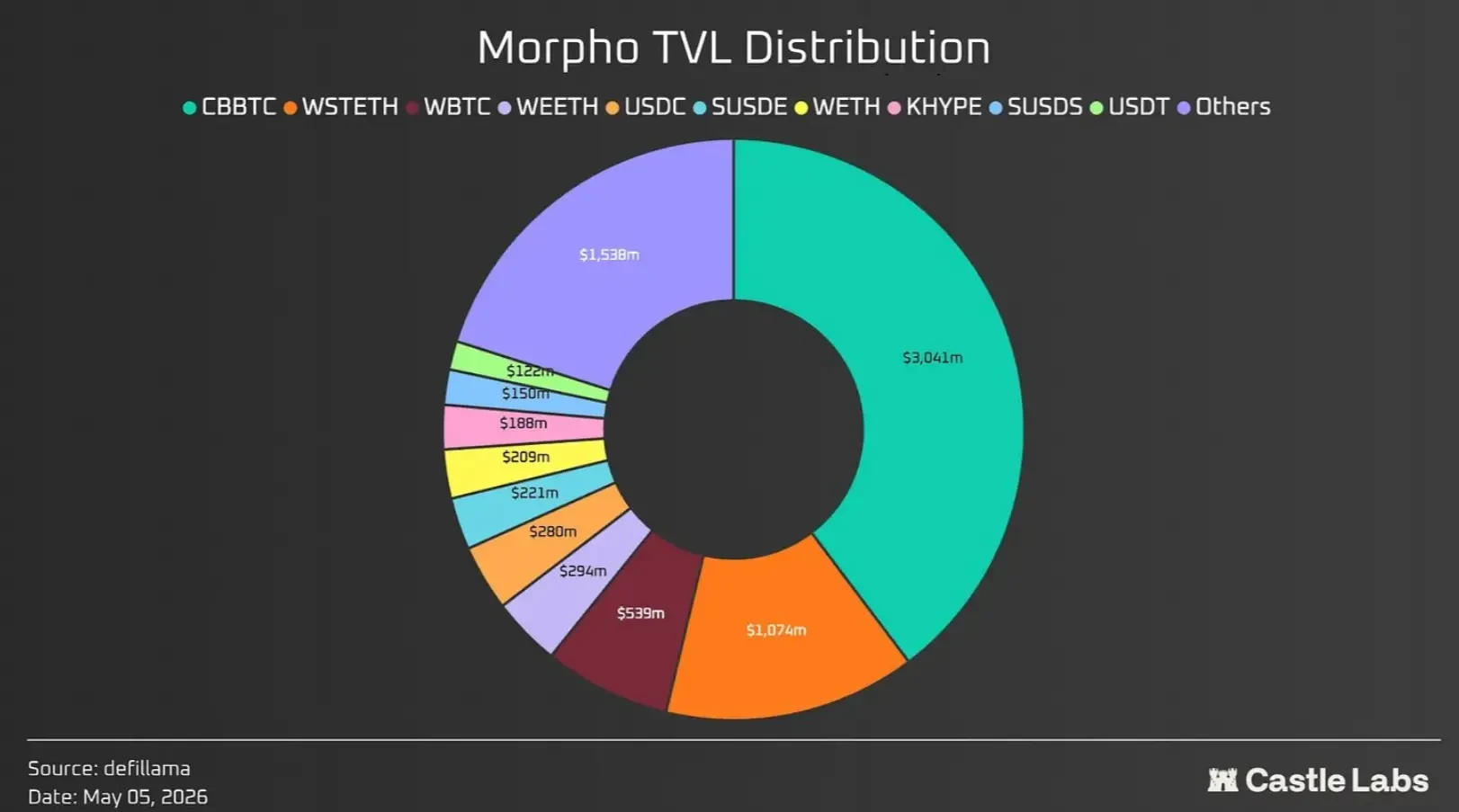

Lending is the largest vault category, comprising the vast majority of DeFi TVL. Last year marked a broad shift towards curated vaults, driven by products like Morpho that helped expand this trend.

On Morpho, curators can create their own vaults that can have exposure to multiple markets and earn yield for depositors. These vaults can ultimately be curated by any provider, including traditional financial institutions.

Morpho's recent Vaults V2 upgrade provides curators with more features, including the ability to embed approved adapters to source yield from multiple origins, granular risk controls (e.g., setting absolute or relative caps on vault exposure), built-in KYC controls, and other functionalities.

In the same context, Aave also launched its V4 version, introducing an architecture of Spokes and a unified liquidity hub. Spokes offer enhanced functionality through custom risk parameters, isolated collateral types, and per-market oracle configuration.

It differs from Morpho's curator-led model in that Aave's governance still needs to review and approve these Spoke implementations, whereas Morpho is permissionless. This marks Aave's transition from monolithic lending to modular lending.

The curator model has enabled Morpho to accumulate over $7.5 billion in TVL on Ethereum mainnet and Base. Base has been a massive contributor to Morpho's growth, rising from $604 million to over $2.8 billion.

This demonstrates the power of distribution partnerships Morpho has pursued, such as the collaboration with Coinbase: currently, approximately 40% of TVL in USD terms is cbBTC, while it has helped facilitate over $1 billion in loans for Coinbase users.

In response to the curator model finding product-market fit (PMF) among institutional investors, Aave is competing in the institutional赛道 via Horizon, which has accumulated over $350 million in TVL since its launch.

Furthermore, in recent months, Aave has undergone many changes, including service providers like BGD and ACI leaving Aave Labs, and the announcement and approval of the "Aave will Win" framework, allocating 100% of revenue from Aave's products to token holders.

None of these events had much direct impact on Aave users. The only impact was on the price performance of the Aave token, but the recent KelpDAO attack changed the situation: Aave lost over $12 billion in TVL, bringing it closer in TVL terms to its competitor Morpho.

The ratio of Aave TVL to Morpho TVL previously ranged between 5x and 6x, but has now dropped below 2x due to that event.

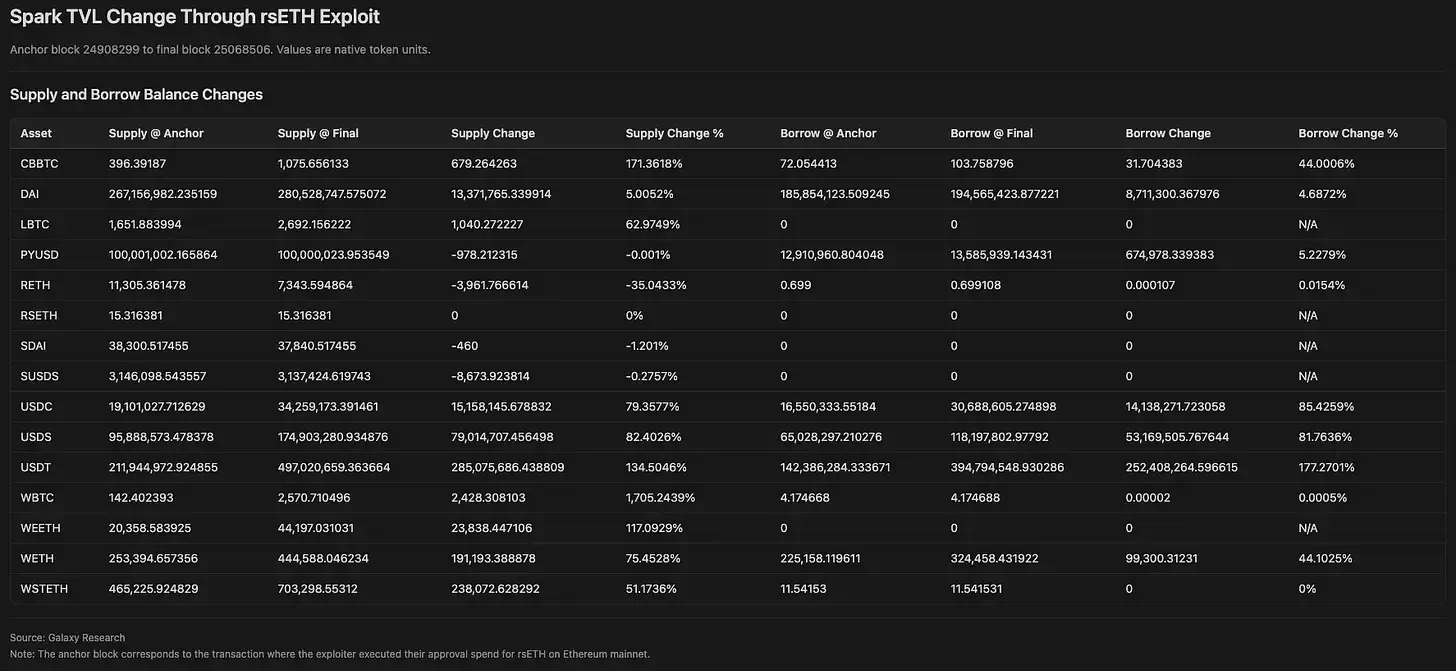

@sparkdotfi, part of the Sky ecosystem, is also one of the lending protocols that benefited most from capital inflows after the rsETH hack.

The chart below shows the TVL changes for the protocol:

Most notably, Bitcoin supply nearly tripled, stablecoin borrows increased by 78% to $752 million with utilization remaining manageable, and WETH borrows increased by 44.1% to 325,000 WETH.

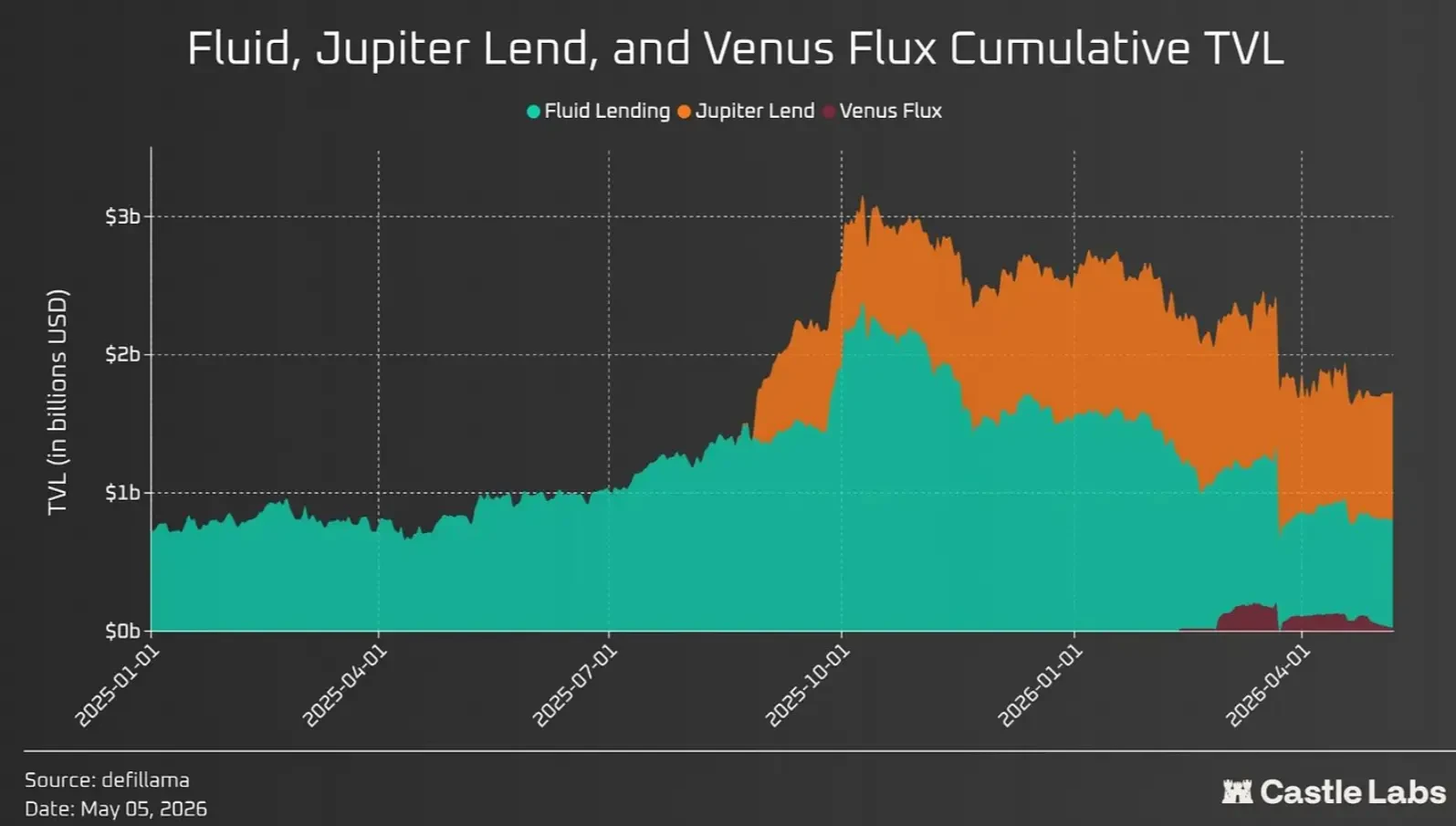

@0xfluid's unified liquidity layer also introduces a different approach to liquidity design, where lending, borrowing, and DEX share the same pool of funds. User collateral acts as LPs in the Fluid DEX, earning trading fees, while borrowed funds are deployed as smart debt into DEX pools, earning fees to offset borrowing interest costs.

Another interesting move by Fluid is its partnership with protocols like @JupiterExchange and @VenusProtocol, through which white-label products like JupLend (Solana) and Venus Flux (BSC) were launched, with TVLs currently reaching $926 million and $21 million respectively.

This stems from Fluid's broader positioning to collaborate with key players across chains and capture more market share, with these partners sharing fees with Fluid.

Worth mentioning are @kamino vaults, the primary lending stack on Solana with over $1.6 billion in TVL. The protocol has seen significant growth through its K-Lend model (the Solana equivalent of Morpho). This allows Kamino to partner with established curators like Gauntlet and target institutional integration.

The largest vault on the platform is currently @SentoraHQ PYUSD with over $219 million in TVL, while the second largest is RockawayX's RWA USDC vault at just $33 million, indicating significant room for growth for Kamino and Solana as a whole.

Liquid Staking & Restaking

Liquid staking and restaking account for a large share of vault TVL, at $42.4 billion and $20.6 billion respectively.

The main players in liquid staking are Lido ($21.8B), Binance Staked ETH ($8.9B), @Rocket_Pool ($1.2B), and @Coinbase cbETH ($320M).

Over time, Lido has maintained its dominance, with its issued asset stETH being highly composable across DeFi. However, Lido's dominance also signifies concentration risk. They have expanded their product line by introducing the Earn product, which acts as an aggregation layer, depositing user funds across DeFi to earn yield. However, this product was impacted after the recent Kelp DAO hack due to its exposure to $rsETH.

Binance Staked ETH, leveraging Binance's user base, has grown 121.8% since last year.

Growth has been slow for other protocols and the category overall, coming at the expense of staking yield dilution, with current staking yields around 2.5%.

On the other hand, restaking and liquid restaking grew as a category to enhance yields earned from liquid staking.

The hack of @KelpDAO, a liquid restaking protocol, and the broader DeFi cascade highlighted the composability risks associated with these assets being accepted as collateral throughout DeFi, which in this event acted more as a bug than a feature.

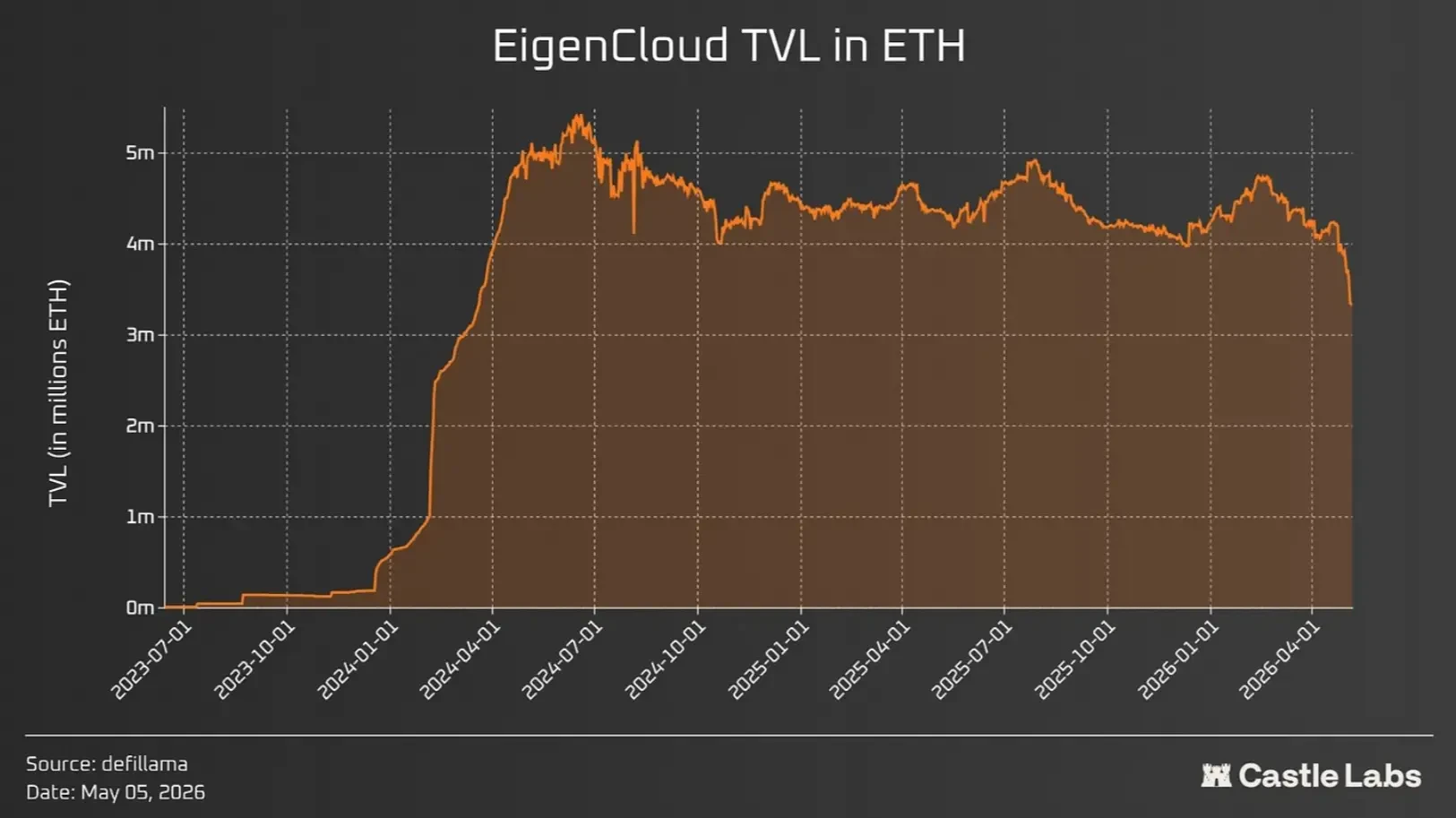

Key players in restaking and liquid restaking are @EigenCloud ($7.8B), @ether_fi ($5.7B), Kelp DAO ($1.6B), and Renzo ($167M).

Restaking products like EigenCloud and EtherFi have expanded over time to encompass more services.

EigenCloud's 2025 rebranding helped position itself as the AWS of crypto, driving the development of verifiable computation.

EigenDA, Eigen's data availability layer, is used by multiple L2s, including @megaeth, @Mantle_Official, and @Celo. Data posted on EigenDA has exceeded 1.8 TB and generated approximately $90,000 in total fees.

EigenCloud's TVL in ETH terms had been flat for a long time but recently declined after the Kelp hack, as users tend to withdraw funds during uncertain periods.

Similarly, EtherFi has expanded into a neobank with thousands of active card users, who have cumulatively spent approximately $440 million through its products.

Additionally, they have a Liquid product (remember EtherFi originally launched as a liquid staking protocol) that supports multiple strategies to boost yields across DeFi. One of its top ETH yield vaults has a TVL of $177.5 million.

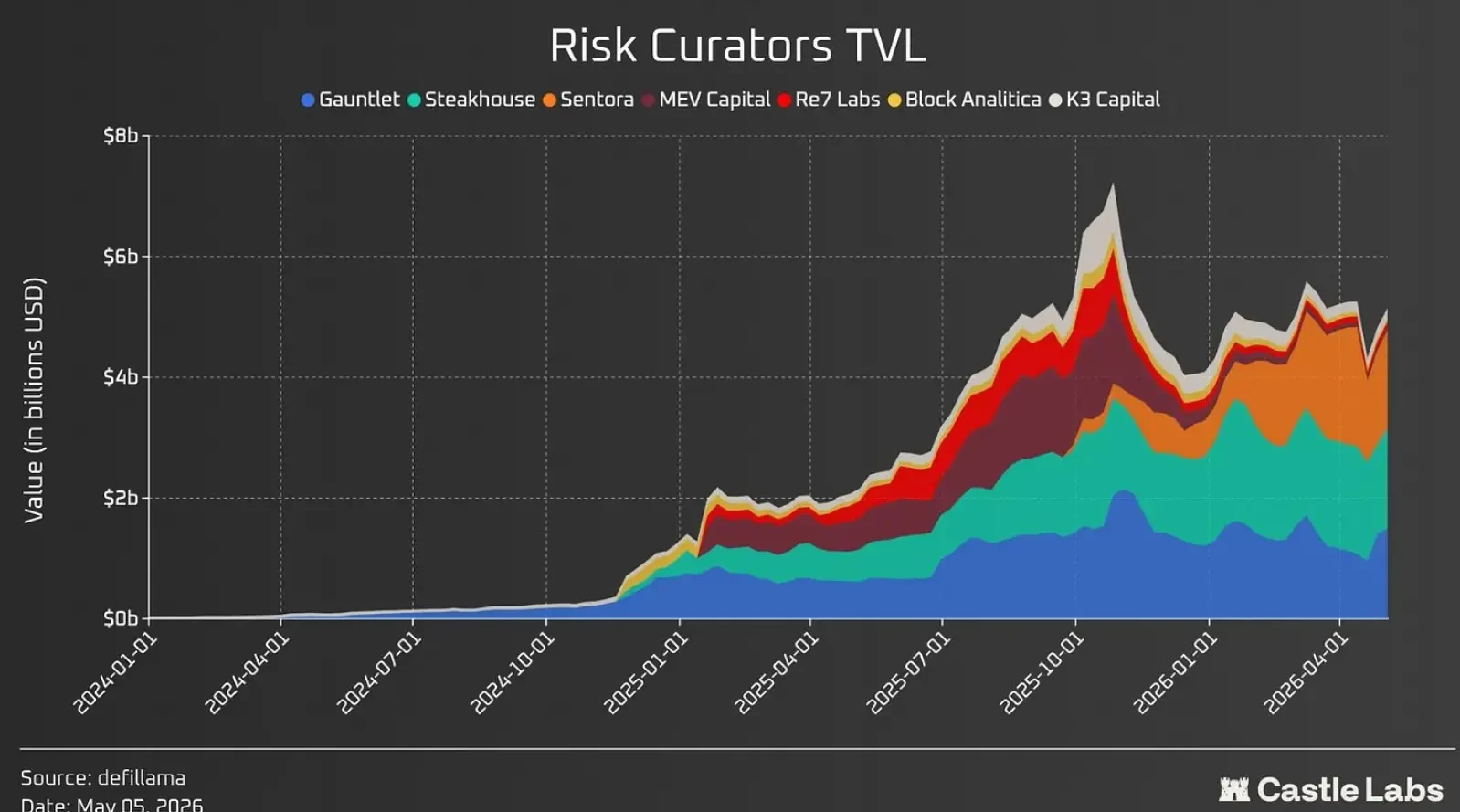

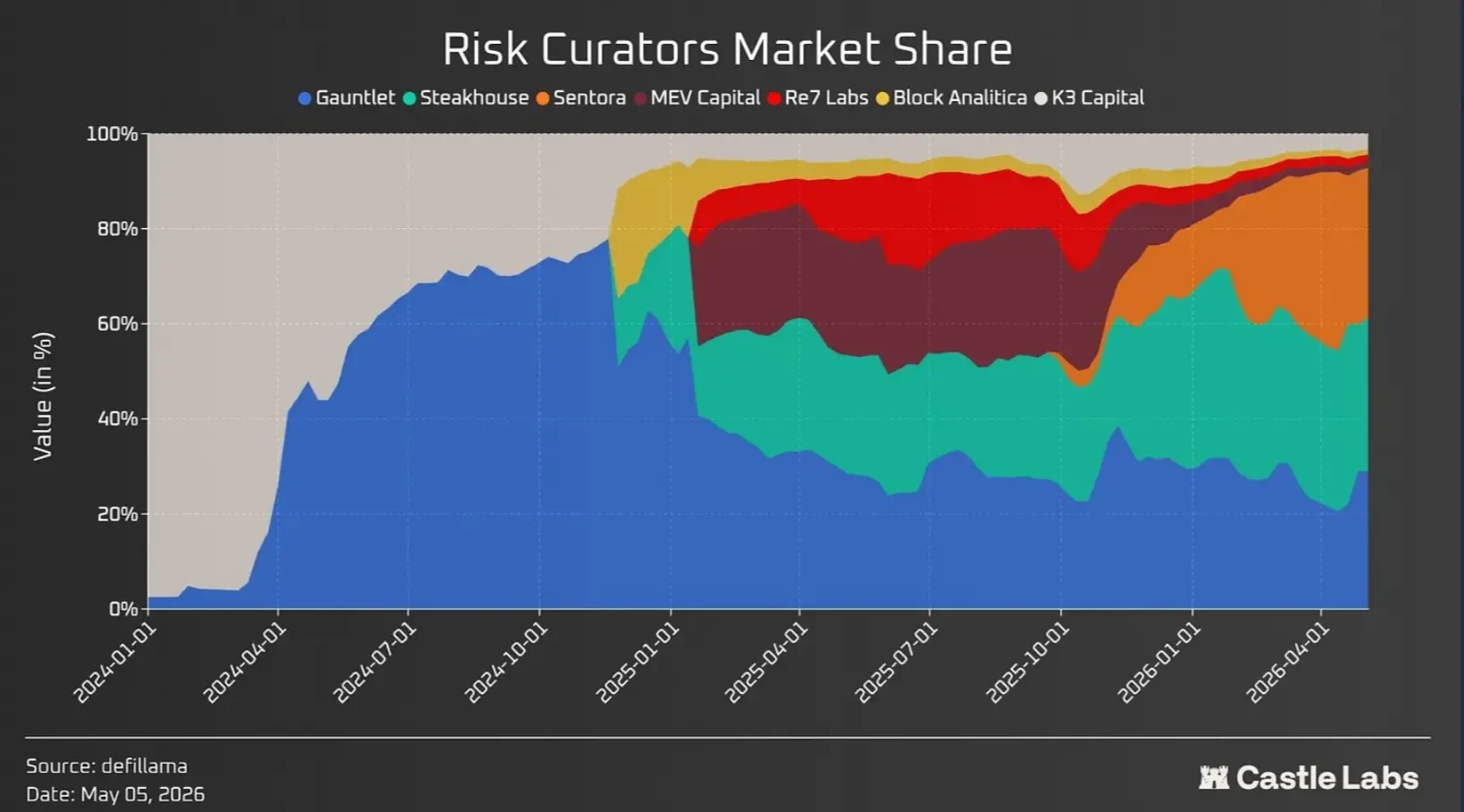

Risk-Curated Vaults

Risk-curated vaults are among the fastest-growing categories, reflecting the shift from monolithic to modular lending. The curated vaults they offer on platforms like Morpho earn them performance and management fees, akin to how traditional finance funds operate, deploying user capital across various strategies to generate returns.

The current TVL for this category is approximately $6.5 billion, with 75% held by three curators: Sentora ($1.85B), @SteakhouseFi ($1.63B), and @gauntlet_xyz ($1.5B), indicating less competition in this category.

These risk curators charge lower fees than traditional finance hedge funds and venture funds, which typically charge management fees (~1-2% of total AUM) and performance fees (~10-20% of interest earned). For example, Steakhouse Financial, the largest curator by revenue, generates $3 million in annualized revenue on $2.13 billion AUM (an annualized fee rate of ~0.14% of total AUM).

These curators typically charge only performance fees, and in some cases management fees, but these are currently much lower. This results from a competitive landscape where curators vie to offer the lowest fees to attract the most TVL.

But even so, risk curator concentration is in the hands of the top three providers dominating, which is better than liquid staking, where Lido is far ahead.

Furthermore, what does this concentration mean? The Steakhouse team comments: "Concentration may follow the power law found in traditional asset management analogs (e.g., ETFs), where the majority of AUM clusters around leading managers. This is not necessarily a bad thing, but a reflection of scale and trust compounding around top managers who compete on performance, product range, and fee loads. The beauty of DeFi is that the arena is open. Anyone can come in and compete. We expect top-tier concentration to persist, alongside healthy competition at the edges and room for specialization."

Concentration dynamics recently shifted after the Stream Finance incident. Before that, MEV Capital and Re7 also had