科技IPO大潮前夜,Polymarket联手纳斯达克抢「估值裁定权」

- 核心观点:Polymarket 通过与纳斯达克旗下 NPM 合作,利用其独家私募估值数据推出 pre-IPO 公司市值预测合约,旨在抢占高增长私募市场的估值定价权,并逆转被竞争对手 Kalshi 反超的市场颓势。

- 关键要素:

- 合作背景:SpaceX、OpenAI 等 pre-IPO 公司估值超万亿,但普通投资者因门槛高、信息不透明而难以参与,预测市场被视为理想的切入点。

- 合作内容:Polymarket 与 Nasdaq Private Market (NPM) 独家合作,上线 SpaceX、OpenAI 等公司市值的预测合约,NPM 提供结算数据。

- 竞争劣势:过去八个月,Polymarket 在月交易量(4月102亿美元 vs Kalshi 148亿)、活跃用户数及估值上均被 Kalshi 反超,且美国本土份额仅约11%。

- 数据价值:合作的关键在于 NPM 首次对其私募估值数据向预测市场开放,这些数据源自其处理的近800亿美元员工股交易。

- 双向共赢:NPM 为 Polymarket 提供结算数据,而 Polymarket 的实时合约价格曲线将作为“机构信号”提供给 NPM 客户,实现数据双向流动。

- 数据变现战略:此举是 Polymarket 继向 ICE、道琼斯出售数据之后的又一数据变现举措,旨在抢夺私募市场估值的裁定权。

In this wave of tech IPO frenzy, everyone wants to "get on board," including Polymarket.

With at most 23 days until SpaceX lists on Nasdaq, this IPO is poised to shatter every record in the history of public offerings.

OpenAI was valued at $500 billion in its last funding round, Anthropic is reportedly worth $400 billion, and SpaceX stands at $1.75 trillion. Globally, there are 1,600 unicorn companies with a combined valuation of $5 trillion. Historically, returns in this space have only been accessible to institutions and accredited investors. Buying shares directly in these companies requires a six-figure minimum, a one-year lock-up period, accredited investor status, and a network of connections — something the average person simply cannot access.

Moreover, private companies have no obligation to disclose their valuations. Funding round valuations are lagging indicators, secondary market quotes are fragmented, and the actual transaction prices of employee shares are highly sensitive internal information. This, precisely, is the perfect entry point for prediction markets.

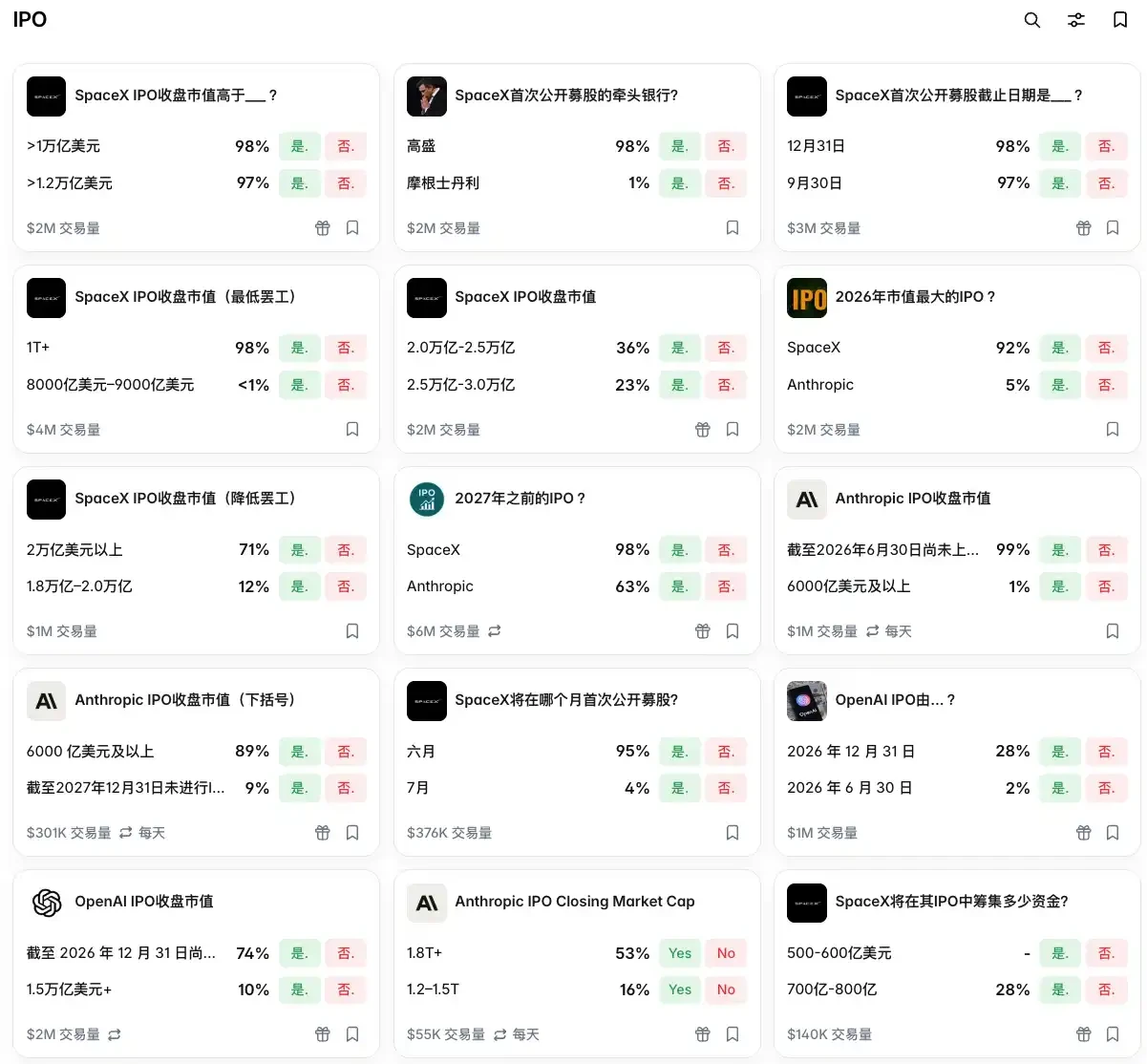

On May 19, Polymarket, seizing the moment, launched exclusive partnerships with Nasdaq, introducing a suite of prediction contracts focused on the valuations of pre-IPO companies. Users can bet on whether OpenAI's valuation will break $1 trillion by year-end, whether Anthropic will hit $1.1 trillion by December 31, and whether SpaceX can reach $1.5 trillion before June 30. Nasdaq, serving as the data source, will be responsible for the final settlement of these contracts.

Polymarket previously had a market for OpenAI's first-day closing market cap, with Bloomberg reporting that it accumulated $1.6 million in trading volume since last September. Existing IPO contracts on Kalshi are even more numerous: the probability of Cerebras Systems going public before 2027 is priced at 95%, Kraken at 83%, Databricks at 70%, and Discord at 70%. Contracts for OpenAI and Anthropic also exist.

Both competitor platforms are taking the pre-IPO wave very seriously.

Polymarket's Comeback

Over the past eight months, Polymarket has been overtaken by Kalshi in nearly every visible metric.

In April, Kalshi's monthly trading volume was $14.8 billion, up 13% month-over-month. Polymarket's combined global and US app volume was $10.2 billion, down 8.9% month-over-month. Active traders dropped from 733,000 in March to 643,000 in April, a decline of 12%. In terms of valuation, Kalshi's latest round was at $22 billion, while Polymarket is reportedly in talks at $15 billion.

In an April report, Bank of America noted that in the US domestic prediction market, Kalshi captures approximately 89% of the share.

Kalshi's path in recent years has been smoother than Polymarket's. In 2020, the CFTC granted it a Designated Contract Market license — the first and only one in the US specifically for event contract platforms. This means Kalshi can handle US dollars, issue 1099 tax forms, integrate with Robinhood's SDK, and have its probability data cited by CNN and CNBC. In February, Kalshi was selected by TIME for the TIME100 Most Influential Companies list, and its app store ranking once approached ChatGPT's.

In contrast, Polymarket withdrew from the US market in 2022 after being fined $1.4 million by the CFTC. It was only in July 2025 that the CFTC and the Department of Justice concluded a new investigation into it, allowing it to acquire a compliant trading license through the acquisition of QCEX.

However, Polymarket's partnership with Nasdaq this time is likely a signal of its counterattack.

Polymarket's partner is specifically Nasdaq Private Market (hereinafter referred to as NPM), a company incubated by Nasdaq that specializes in serving private companies. Its main business focuses on two things:

First, organizing secondary market liquidity programs for employee shares. Employees of companies like OpenAI, SpaceX, and Anthropic hold large amounts of stock options or restricted stock. Since the companies aren't public, they can't sell on the open market. NPM helps these companies organize tender offers, allowing employees to sell their shares to approved external investors. NPM itself has disclosed handling nearly $80 billion in such transactions, covering over 1,000 company-led liquidity programs and serving more than 200,000 employee shareholders.

Second, building a valuation database for private companies. NPM sees daily transaction prices for employee shares of OpenAI, Anthropic, and SpaceX on the secondary market. This data was previously sold only to institutional clients at a hefty annual fee.

A key step in this partnership is NPM's agreement to make this valuation data available to Polymarket for the first time.

Rodolfo Sanchez, Vice President of Data at NPM, made a crucial statement in the press release: "The data flows in both directions." NPM provides data to Polymarket for contract settlement, and in return, Polymarket's contract price curves become an "institutional signal" for NPM's clients. When institutional clients buy NPM data, they also get a probability curve dynamically priced by hundreds of thousands of retail traders.

Selling Data, Grabbing Settlement Power, Capturing Retail Traders

This is not the first time Polymarket has sold its own data.

In October 2025, ICE announced an investment of up to $2 billion at an $8 billion pre-money valuation. The focus of this deal wasn't the valuation but the terms. ICE secured the exclusive global distribution rights for Polymarket's data. The sales channels of the NYSE's parent company began selling Polymarket's probability data to global institutional clients.

In January 2026, an exclusive partnership with Dow Jones was announced. Polymarket's prediction data was integrated into the Wall Street Journal, Barron's, MarketWatch, and Investor's Business Daily. The News Corp-owned financial media conglomerate started embedding Polymarket's probability signals as a standard module, akin to the Dow Jones Index or VIX, into its pages.

In February 2026, ICE officially launched the Polymarket Signals and Sentiment product. Real-time quotes from thousands of contracts on Polymarket were organized into a structured data stream and distributed to institutional clients via the ICE Consolidated Feed, running on the same pipeline as NYSE stock data, bond prices, and corporate announcements. In the Q1 earnings call, ICE President Ben Jackson listed this product alongside Reddit and Dow Jones, calling them the three pillars of ICE's alternative data services.

And this latest partnership is about seizing the settlement power for this year's hottest market: private company valuations.

We suspect Kalshi won't stay idle. Its next move will likely involve negotiating a partnership with another private market data provider to replicate this structure. However, mainstream private data providers like Forge and PitchBook are smaller in scale than NPM and cover fewer companies. Since NPM is now exclusively tied to Polymarket, Kalshi's entry into this arena will come at a higher cost.