Tonight, Powell's "Last FOMC": Likely to Hold Steady, but with a More Hawkish Tone

- Core View: The Fed's April FOMC meeting is expected to keep the benchmark interest rate unchanged, with market focus on the hawkish signals from Powell's final chair meeting and whether the committee will formally imply that "rate cuts are essentially off the table," shifting the policy path risk to a two-way direction.

- Key Elements:

- Rate Decision No Surprise: Market consensus is to hold rates in the 3.5%-3.75% range, with only Governor Miran potentially casting the sole vote for a 25-basis-point cut.

- Inflation and Employment Data: The Iran war and energy shocks are pushing up oil prices, with the expected timeline for cooling inflation delayed by another year. March employment data showed resilience, reducing the urgency for rate cuts.

- Dovish Stance Tightening: Previously dovish officials like Waller and Daly are now emphasizing inflation risks. Daly's baseline scenario has shifted to rates staying flat for the entire year, and Miran has also scaled back rate cut expectations.

- Statement Wording Key: Changing "additional adjustments" to "any adjustments" would mean the preset path for rate cuts disappears, shifting focus to two-way risks. However, a majority of voting members favor maintaining current guidance.

- Hawkish Lean in Powell's Press Conference: He is expected to reiterate inaction and that inflation is the policy priority. If he emphasizes that the war has a greater impact on inflation, it will be seen as a very hawkish signal.

- Powell's Final Act: His term ends on May 15th, with successor Kevin Warsh's nomination path clear. This meeting sets the tone for the transition of the policy starting point.

Original author: Zhao Ying

Original source: Wallstreetcn

The outcome of the Fed's April FOMC meeting is virtually a foregone conclusion — interest rates will remain unchanged. However, the true focus of this meeting lies in the signals that Powell's final policy session as Chair will send, and whether the Committee will formally convey to the market a hawkish stance that "rate cuts are essentially off the table."

The Federal Reserve will announce its interest rate decision at 2:00 AM Beijing time on April 30th. The benchmark rate is expected to remain unchanged in the 3.5% to 3.75% range. Market consensus is highly aligned, anticipating only a single dissenting vote from Governor Miran in favor of a 25-basis-point cut.

The latest changes stem from the inflation front. The conflict in Iran and energy shocks continue to disrupt the outlook. Gasoline prices remain above $4, and traffic through the Strait of Hormuz remains severely hampered. Meanwhile, recent employment data has shown resilience, reducing the urgency for dovish members to push for immediate support of the labor market.

Fed officials generally expect the decline in inflation to be delayed by a full year again. Market expectations for rate cuts have narrowed significantly. Deutsche Bank has retracted its previous forecast for a September rate cut, adjusting its baseline scenario to the Fed "holding steady indefinitely" near the neutral rate.

The core contention of this meeting centers on the wording of the statement and the risk characterization in the press conference. The addition or removal of a single word in the forward guidance could send vastly different policy signals to the market. Furthermore, with the DOJ concluding its investigation into Powell, Kevin Warsh's path to Fed Chair nomination is largely cleared, adding historical significance to this meeting.

Holding Steady is Consensus, Debate Shifts to 'Next Steps'

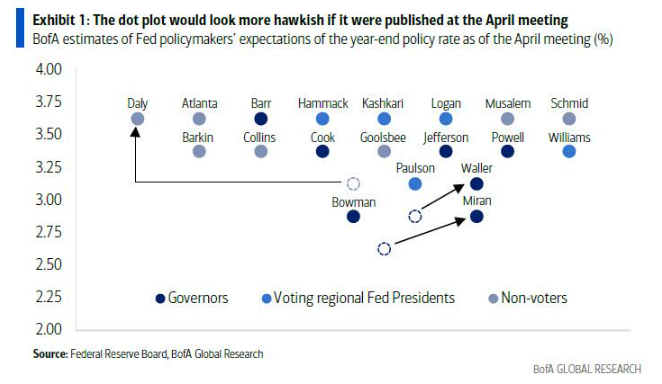

This FOMC meeting has no dot plot, and the interest rate decision itself is hardly a surprise. The focus is on whether the Fed is still willing to retain the policy hint that "the next move is more likely to be a cut," or if it will begin to acknowledge that risks have become two-sided.

According to Bank of America, the current inflation outlook remains as unclear as it was during the March meeting. Although stock market trading seems to assume the Iran conflict is over, energy and shipping disruptions persist, and there is still high uncertainty regarding the passthrough of the conflict to core inflation.

The employment side has not provided sufficient reason for the Fed to urgently pivot dovish. March data on nonfarm payrolls, ADP employment, and initial jobless claims all indicate resilience in the labor market, even showing some signs of improvement. This makes it harder for members who previously advocated for rate cuts to continue emphasizing "downside risks to employment" as their primary policy justification.

Even Doves Are Tightening, Urgency for Cuts Declines

Heading into this meeting, the most notable change within the Fed was the increasingly hawkish tone adopted by previously dovish-leaning members.

In his speech last week, Waller not only emphasized the upside inflation risk from the Iran war but also mentioned labor supply shocks. He argued that the economy might "require little or no net new job creation" to keep the unemployment rate stable. BofA believes Waller may still desire a rate cut this year, but potentially smaller and later than previously anticipated.

Daly went a step further. She stated that if policy remains unchanged throughout the year, it would provide good restraint on inflation without restricting or damaging the labor market. She also suggested that the Iran war's impact on inflation might be greater than its impact on growth. Daly's current baseline scenario has shifted to a flat rate path for the entire year.

Even Miran, considered the most dovish member of the FOMC, indicated a preference for three rate cuts this year instead of four, citing the worsening inflation mix since the start of the year. BofA suggests that if the April meeting had a dot plot, some members' 2026 rate expectations would already be higher, and the risk of more "dots" shifting higher continues to increase by June.

Statement Wording: One Word Difference, Starkly Different Signals

The biggest potential change in this FOMC statement is whether the Fed will hint that the risks to the policy path have become "two-sided."

The current statement's phrasing regarding "additional adjustments" carries a dovish presupposition that the next move is a cut. Changing it to "any adjustments" or simply removing "additional" would imply the next policy move's direction is no longer predetermined, formally opening the policy path to two-sided risks. The March meeting minutes showed that the number of members supporting the adoption of two-sided risk language increased from "several" in January to "some," and the wording became firmer.

Bank of America sees this as a close call, but believes a majority of members still prefer to keep the current forward guidance language unchanged. Deutsche Bank leans towards substantial guidance adjustments being postponed until June, when the Committee will have more clarity on the Middle East situation, labor market stability, and inflation transmission channels, though the risk is clearly tilted towards the hawkish side.

Additionally, one adjustment is expected in the statement. Given the downward revision to Q4 GDP and weak consumer spending in January and February, the Fed might downgrade its description of economic activity from "solid" to "moderate." However, BofA notes that this adjustment itself has a dovish tinge, somewhat contradicting the Committee's current overall intent to project a hawkish signal to the market.

Press Conference: Powell's Hawkish Stance a Near Certainty

If this indeed is Powell's final press conference as Chair, he will most likely maintain a moderately hawkish stance.

According to BofA, Powell's core message will likely be that the Fed is firmly holding steady, and current policy is well-positioned to address risks to its dual mandate. With high uncertainty persisting, the Fed sees no reason to push back against market pricing for a flat rate path.

The most sensitive question in the press conference will be the threshold for rate hikes. If Powell reiterates that rate hikes are not the base case for a majority of the Committee, the market might interpret it as a dovish signal. Conversely, if he emphasizes the importance of completing the inflation-fighting mission or notes that inflation has been above target for years, it would be seen as hawkish.

Notably, "inflation" was mentioned 67 times at the March press conference, while "labor market / employment / unemployment" was mentioned only 40 times, clearly making inflation the heaviest weight on the policy scale. He is not expected to provide a quantitative threshold for rate hikes.

Regarding the Iran war, Powell is expected to acknowledge both upside risks to inflation and downside risks to growth and the labor market. But the market will focus on which way he leans. If his comments align with Daly's view that the war's impact is greater on inflation than growth, the market is likely to interpret it as very hawkish.

Focus: Are Rate Cuts Scuttled, or Merely Delayed?

Nick Timiraos, often called the "Fed's new mouthpiece," wrote before the meeting that the April session marks a pivotal point for a deeper policy debate: how much longer can the Fed maintain the stance that the "next move is more likely to be a cut rather than a hike"?

Timiraos noted that two years ago, Powell downplayed stagflation concerns, saying he saw "neither stag nor flation." But now, the energy shock from the war combined with inflation still above the 2% target makes the historical mirror of 1970s stagflation feel less distant.

He emphasized that the Fed is observing how the U.S. economy digests its fourth supply shock in five years, including the pandemic restart, the Russia-Ukraine conflict, tariff turmoil, and the Iran war. Each shock viewed in isolation could be dismissed as a transient event requiring no policy response, but their cumulative effect makes inflation expectation management more challenging.

Timiraos believes the statement itself could be as important as the rate decision. If the Fed modifies the formal statement language to imply that rate cuts are essentially off the table, the market impact could be as significant as an actual policy action.

Final Dance and Position Handover

This meeting commands extra attention because it might be the last FOMC under Powell's chairmanship.

Powell's term as Fed Chair ends on May 15th. He has previously pledged to serve as "temporary Chair" until his successor is confirmed. With the DOJ ending its investigation into matters related to Powell, Kevin Warsh's path to Senate confirmation appears clearer.

UBS expects Kevin Warsh could be sworn in before the June 16-17 FOMC meeting. If this timeline materializes, the April meeting will be the final policy communication window of the Powell era, and the market will be more attentive to whether he leaves his successor with a policy starting point of "no cuts for longer."

Market Reaction: Tail Risks Beneath a Non-Event Surface

Views from Goldman Sachs' trading desk suggest the market broadly views this FOMC as a low-volatility event, but directional sensitivities exist across different assets.

On rates, Goldman analyst Brian Bingham expects no significant hawkish shift in inflation wording in the statement, with Powell reiterating a wait-and-see approach. However, with only about 5 basis points of movement priced in through December, the threshold for further substantial selling and pricing in actual rate hike probabilities is high. Deviations from the baseline scenario are more likely to point towards higher rates, fewer cuts, and a flatter curve.

On FX, Goldman trader Carlie Ladda believes a slightly hawkish Fed could trigger some dollar buying, but it is unlikely to form a sustained trend. The market remains more focused on the Iran situation, corporate earnings, and month-end factors. The desk leans towards selling dollars on any bounce.

On equities, Goldman's Vickie Chang notes that the main risk from the FOMC for the stock market is if Powell becomes more cautious, emphasizing inflation risks from commodity price shocks, potentially dampening risk appetite. Risk assets have largely priced out the conflict's impact, and downside tail risks may be underestimated.