BitMart Contract Review: Main Trading Pairs' Liquidity Ranks Among Industry Leaders

- Core Viewpoint: In March 2026, amidst Bitcoin's range-bound market conditions, BitMart altered the structure of its contract market by listing a large number of new contract tokens and significantly enhancing the liquidity depth of major trading pairs, attracting more high-frequency trading.

- Key Factors:

- The market was predominantly range-bound, leading traders to rely more on short-term operations and leveraged contracts, which increased the overall market turnover rate.

- BitMart listed 62 new contract tokens that month, covering multiple popular sectors. This shifted the trading structure from "single concentration" to "multi-point distribution," expanding the scope for short-term strategies and accelerating capital turnover.

- For BTC and ETH perpetual contracts, BitMart's core liquidity metrics—such as order book depth, slippage control, and trade execution stability—outperformed most leading platforms, reducing trading costs.

- The improvement in liquidity and matching efficiency allowed large orders to be executed continuously without significantly impacting market prices, enhancing the platform's capacity to handle large-scale trades.

- The platform's future development depends on the sustained increase in liquidity for mainstream trading pairs and the stability of system execution efficiency, which directly impacts user experience and capital retention.

Market data shows that in March 2026, the Bitcoin price repeatedly touched key levels before pulling back, lacking a sustained unidirectional trend. Prices fluctuated frequently within short cycles, with the market dominated by range-bound consolidation.

Under this market structure, trading behavior exhibited periodic changes. The profit potential for some traders' holding strategies narrowed, leading to a greater reliance on short-term operations. Capital holding periods shortened, entry and exit frequency increased, and the overall market turnover rate rose.

In contrast, spot trading struggled to generate continuous profits in a ranging market, while contract trading, supporting two-way positions, allowed repeated participation during both upward and downward moves. Simultaneously, leverage mechanisms amplified capital efficiency, making contracts the primary tool for high-frequency trading.

Changes in trading behavior also drove increased activity in the contract market. Competition among platforms focused on liquidity, depth, and order execution speed.

62 New Contracts Launched, Asset Supply Continues to Expand

In March, BitMart launched 62 contract trading pairs, significantly increasing the number of available trading instruments. Public data shows the new assets covered multiple popular sectors, including high-volatility and high-attention projects.

With more trading instruments available, capital is no longer concentrated in a few major cryptocurrencies but is dispersed across more assets. The trading structure shifted from "single concentration" to "multi-point distribution." This change brings two direct results:

First, trading frequency increases. More instruments provide more trading opportunities, expanding the scope for short-term strategies.

Second, capital turnover accelerates. Users switching between different assets enhances overall trading activity.

After the increase in trading pairs, the platform's order flow became more stable. Trading behaviors across different cryptocurrencies formed a dispersed structure, reducing the impact of volatility in a single asset on the overall market.

The expansion of trading pairs not only increased quantity but also changed trading patterns. The focus shifted from primarily relying on major assets like BTC and ETH to simultaneous activity in both major and long-tail assets. This structure boosted the platform's overall trading volume and order density.

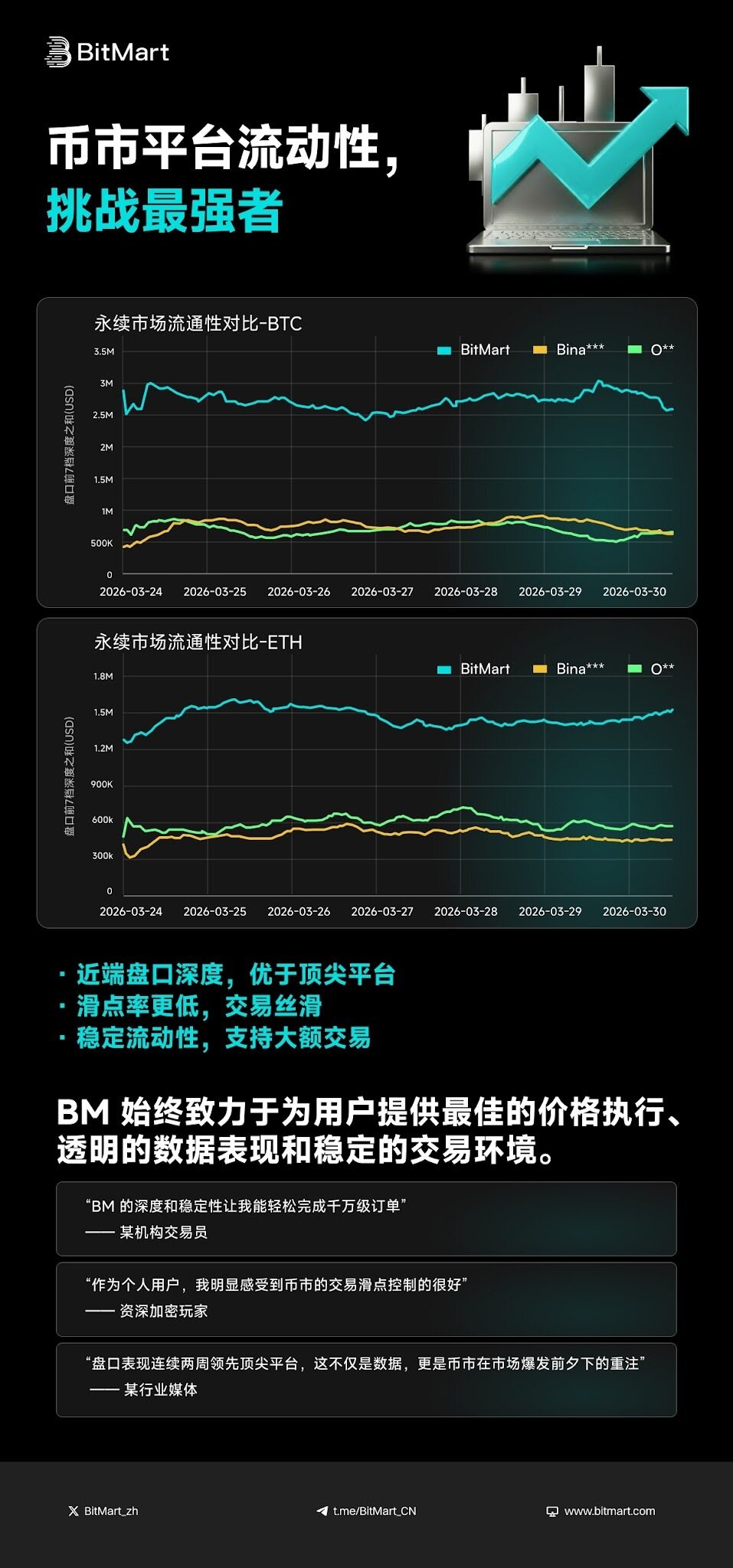

Liquidity and Depth Performance: BTC, ETH Major Contracts Outperform Most Leading Platforms

March data shows that in the perpetual contract market, BitMart's liquidity performance for major trading pairs like BTC and ETH ranks at the forefront of the industry, surpassing some leading trading platforms.

In terms of order book depth, BitMart consistently maintained a high level of order size at key price ranges. The total depth of the top 7 levels for BTC perpetual contracts remained stable at a high level, far exceeding that of benchmark platforms during the period from March 24th to 30th. This means the market can absorb larger trading volumes within the same price range.

A similar trend was evident in ETH perpetual contracts. The distribution of orders on the book became more uniform, and the density of buy and sell orders increased, causing prices to change continuously rather than in jumps during fluctuations.

Improved depth directly impacts slippage performance. For orders of the same size, BitMart's execution price deviates less, effectively controlling the market price impact of large orders. For medium-to-high frequency traders and large capital users, this difference directly translates to lower trading costs.

From an execution results perspective, the combined effect of liquidity and matching efficiency allows orders to be filled closer to the expected price. During periods of rapid market volatility, orders can still be matched within the target range, reducing price deviation caused by insufficient liquidity.

Stable order book depth brings another result: large trades can be executed continuously. In a high-liquidity environment, multiple orders can be filled in batches without significantly altering the market price. This characteristic enables the platform to handle larger-scale trading.

Current data indicates that for major perpetual contracts like BTC and ETH, BitMart has surpassed most leading industry platforms in three core metrics: order book depth, slippage control, and trade execution stability, reaching even higher levels during certain periods.

In March, by increasing the number of trading instruments and enhancing the depth of major trading pairs, BitMart altered the trading structure of the contract market. Trading shifted from concentration to dispersion, and order execution moved from amplified volatility towards stability.

Subsequent changes will depend on two factors: whether liquidity for major trading pairs continues to increase, and whether system execution efficiency remains stable. These two metrics determine the trading experience and whether capital will stay on the platform.