Five and a Half Months into the Bear Market: A Crypto Market Health Check

- Core View: The report posits that the current crypto market is in the mid-stage of a bear market, a critical period for in-depth analysis and identifying future trends. The market structure is undergoing profound changes, with value shifting towards the application layer, as DEXs and specific applications capture market share.

- Key Elements:

- The total crypto market cap has fallen 45% from its peak. If historical patterns hold, it could drop another 30% from the peak to $1.67 trillion. Stablecoin supply, after hitting a local high in March, has stagnated for 5 months, suggesting a potential entry into a fiat redemption phase.

- The share of DEX spot trading volume has significantly increased from around 5% in 2022 to 25% of CEX volume, indicating active "crypto-native" users, with Uniswap, Meteora, and Pancakeswap being the main players.

- Perpetual contract daily volume is 4 times that of spot, highlighting its appeal to retail traders. The DEX share of perpetual volume has risen from 4% at the start of the year to 9.3%, with Hyperliquid dominating this segment.

- Revenue generated by DeFi protocols has surpassed that of Layer 1 blockchains, yet their total market cap share is only 2%, far below L1's 80%, indicating a significant divergence between market valuation and revenue-generating capacity.

- New trading tokens (e.g., memecoins) and trading applications (e.g., Axiom, Pump Fun) demonstrated strong product-market fit in the last cycle. Although current revenues have fallen sharply from their peaks, the related business models and user demand are expected to persist.

- The report predicts that in the next expansion cycle, the regulatory environment may benefit offshore "yield-bearing stablecoins" like Ethena's USDe. The winners in the stablecoin competition will depend on their ability to build "sticky services" (e.g., payments, banking) around the stablecoin.

Source: The DeFi Report

Compiled and Organized by: BitpushNews

We are now 5.5 months into the latest "crypto winter."

The tide has gone out. Animal spirits have dissipated. The tourists have all left.

Rightfully so, it's time to roll up our sleeves and get to work. Because bear markets are when the wheat is separated from the chaff.

This is the time for clear judgment and conviction building.

In this report, we will dive deep into a set of data charts to assess the health of the crypto ecosystem and the trends we believe are shaping the next expansion.

Let's begin.

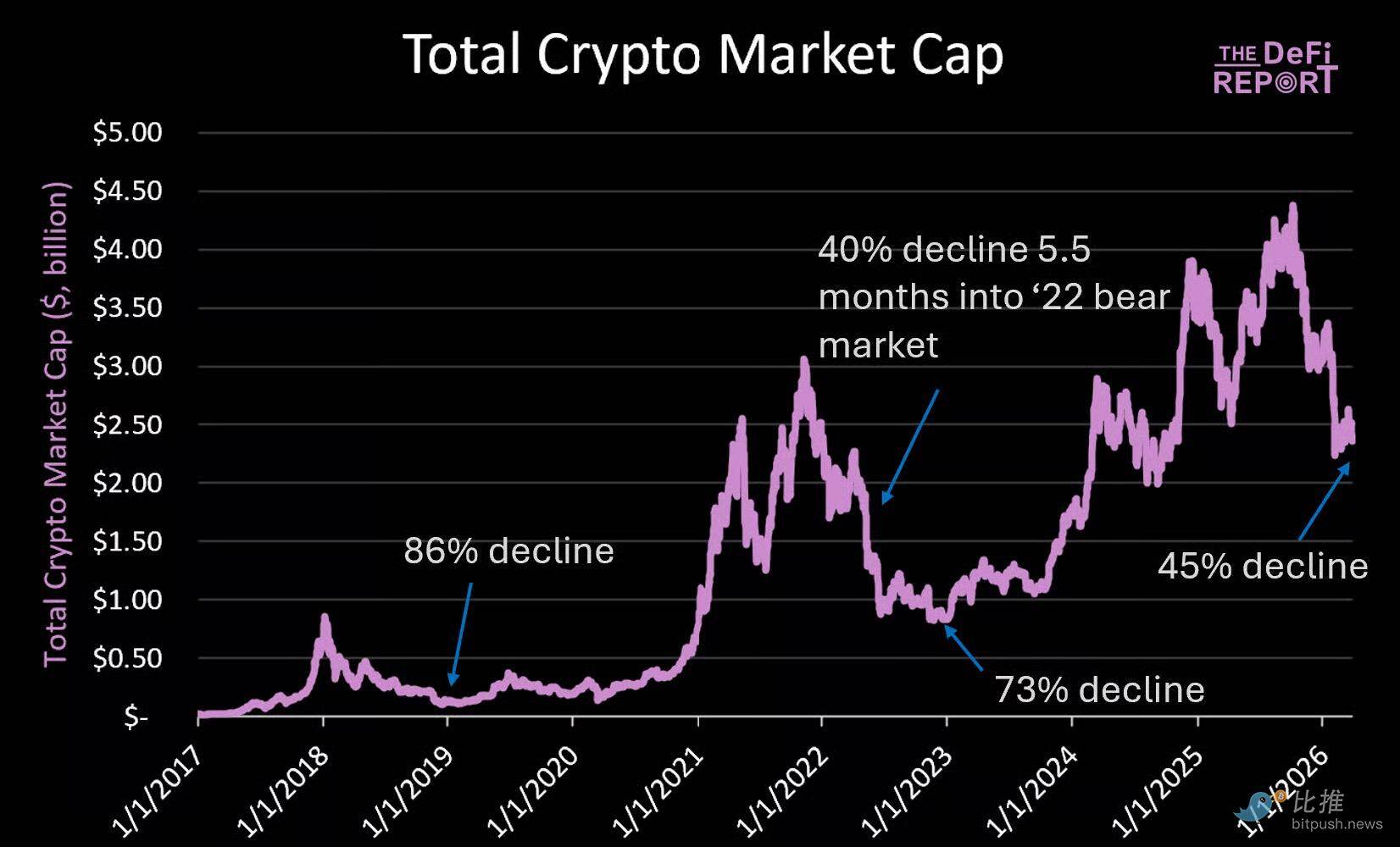

Total Cryptocurrency Market Cap

Current breakdown by major categories:

- BTC: 57%

- L1s: 25%

- Stablecoins: 14%

- DeFi: 2%

- Other: 2%

Note: Both the Stablecoin and DeFi categories generate more revenue than L1s—highlighting the persistent monetary premium L1s still receive from market participants.

As shown above, the total crypto market cap is currently $2.4 trillion—down 45% from its peak ($4.4 trillion), roughly in line with where we were 5.5 months into the last bear market, which was down 40%.

Key Takeaways

- If the total market cap decline matches the relative peak-to-trough decline of '22 vs. '18, we could see a 62% drop from the peak to $1.67 trillion (a further 30% decline from current levels).

- In the '22 bear market, the decline accelerated 5 months after stablecoin supply peaked and began to fall. We are at a similar stage in the cycle today, as stablecoin supply hit a local high on March 16, right around 5 months into the bear market. More on stablecoins later.

- Finally, BTC dominance typically declines during bear markets (it was 38% at the '22 bottom). It is currently 57%. We expect a more moderate decline during this bear market.

Why?

This cycle has fewer novel and exciting use cases, as VCs have clearly realized blockchains are best suited for finance and payments. This reduces the amount of capital that could flow to non-BTC crypto assets.

For this reason, BTC dominance was 60% when the market peaked in October. At the '21 market top, BTC's market share was only 43%.

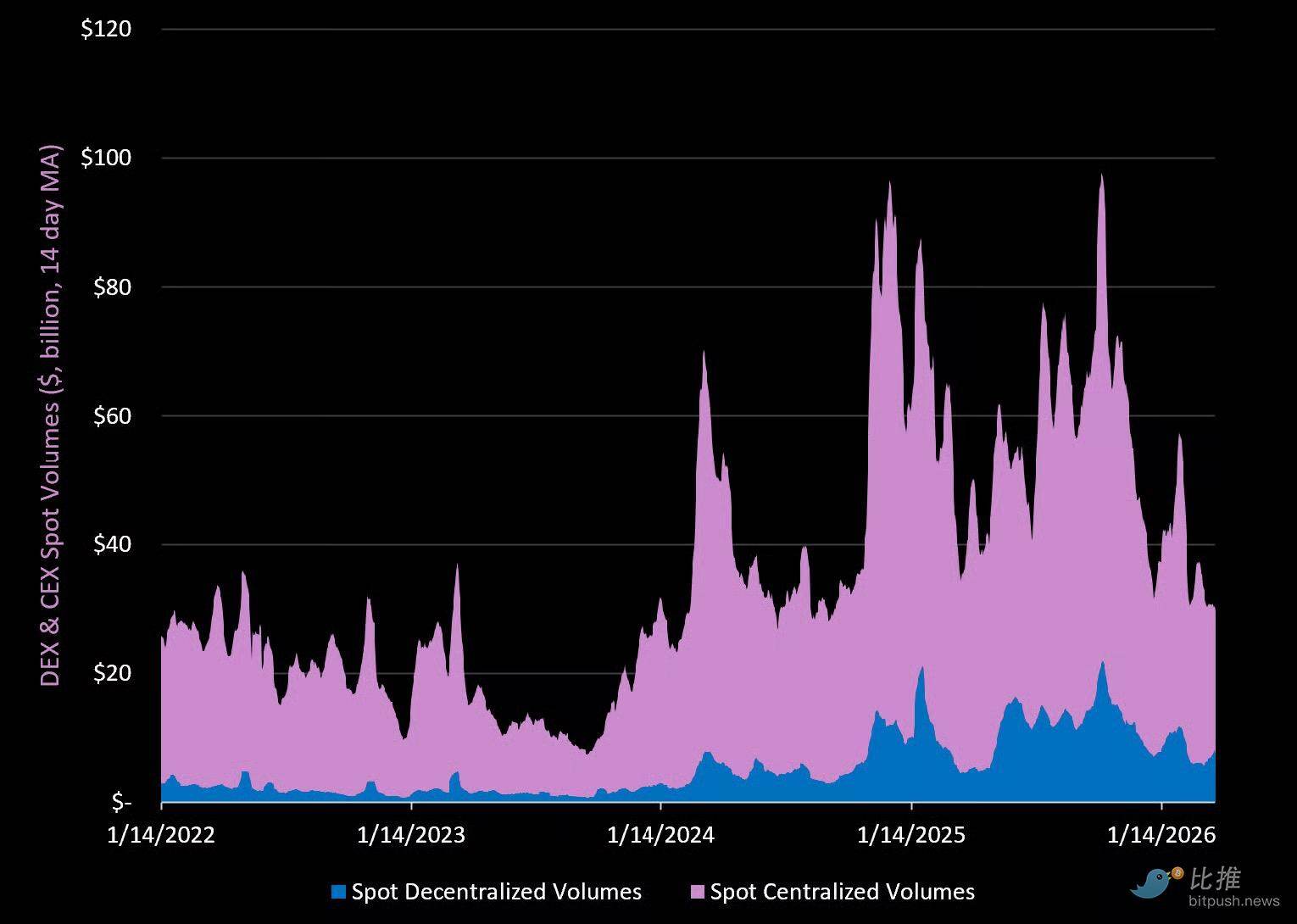

Spot Markets, Data Source: The DeFi Report (Top 10 CEXs & DEXs)

Key Takeaways

- Total spot volume (DEX + CEX) is currently down 70% from its peak in early Q4 last year. CEX volume is down 71%, and DEX volume is down 67%.

- CEX spot volume is currently 1.5x higher than the lows of early '23. DEX volume is currently 9.1x higher than the lows of early '23.

- DEX volume currently accounts for about 25% of CEX volume—up from about 5% in '22. Uniswap leads with a 38% market share, followed by Meteora (Solana) at 22%. Pancakeswap (BNB Chain) is third at 15%. The most interesting development in the DEX space over the past year has been the rise of private DEXs on Solana—they now account for 53% of Solana DEX volume. HumidiFi is the leading private DEX, currently holding a 3% share across all DEXs.

- Binance still dominates CEX spot markets with a 39% share. MEXC (11%), Gate.io (8%), Bybit (8%), OKX (7%), and Coinbase (7%) all occupy the tier below Binance.

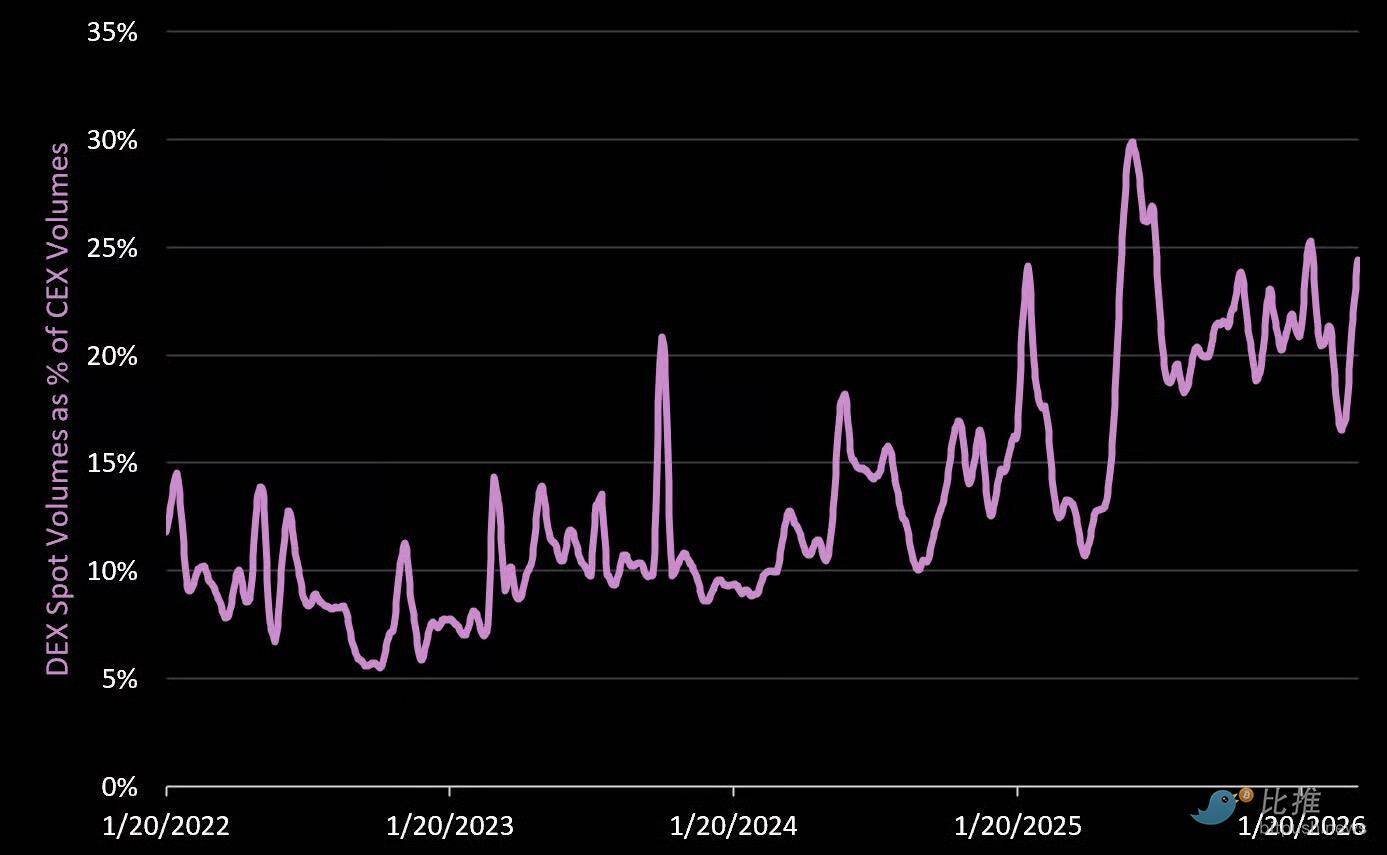

Spot DEX Volume as a Percentage of Spot CEX Volume

DEXs continue to take market share from CEXs during the current bear market. This is also an indicator that the users active today are "crypto-native"—something we expect to see at this stage of the cycle.

More interestingly, DeFi protocols as a category generate more revenue than Layer 1 blockchains, yet account for only 2% of the total crypto market cap today (L1s account for ~80%).

Currently, several DEXs on The Watch List are trading within our "Fair Value" and "Deep Value" ranges.

CEX + DEX Volume as a Percentage of Nasdaq

One of the lesser-reported events of the last cycle was that during the "meme coin frenzy" last January, crypto volume briefly gave Nasdaq a run for its money—crypto volume spiked nearly 3x to $90 billion daily (90% of Nasdaq volume at the time).

Today, the crypto market generates about 20% of Nasdaq's volume.

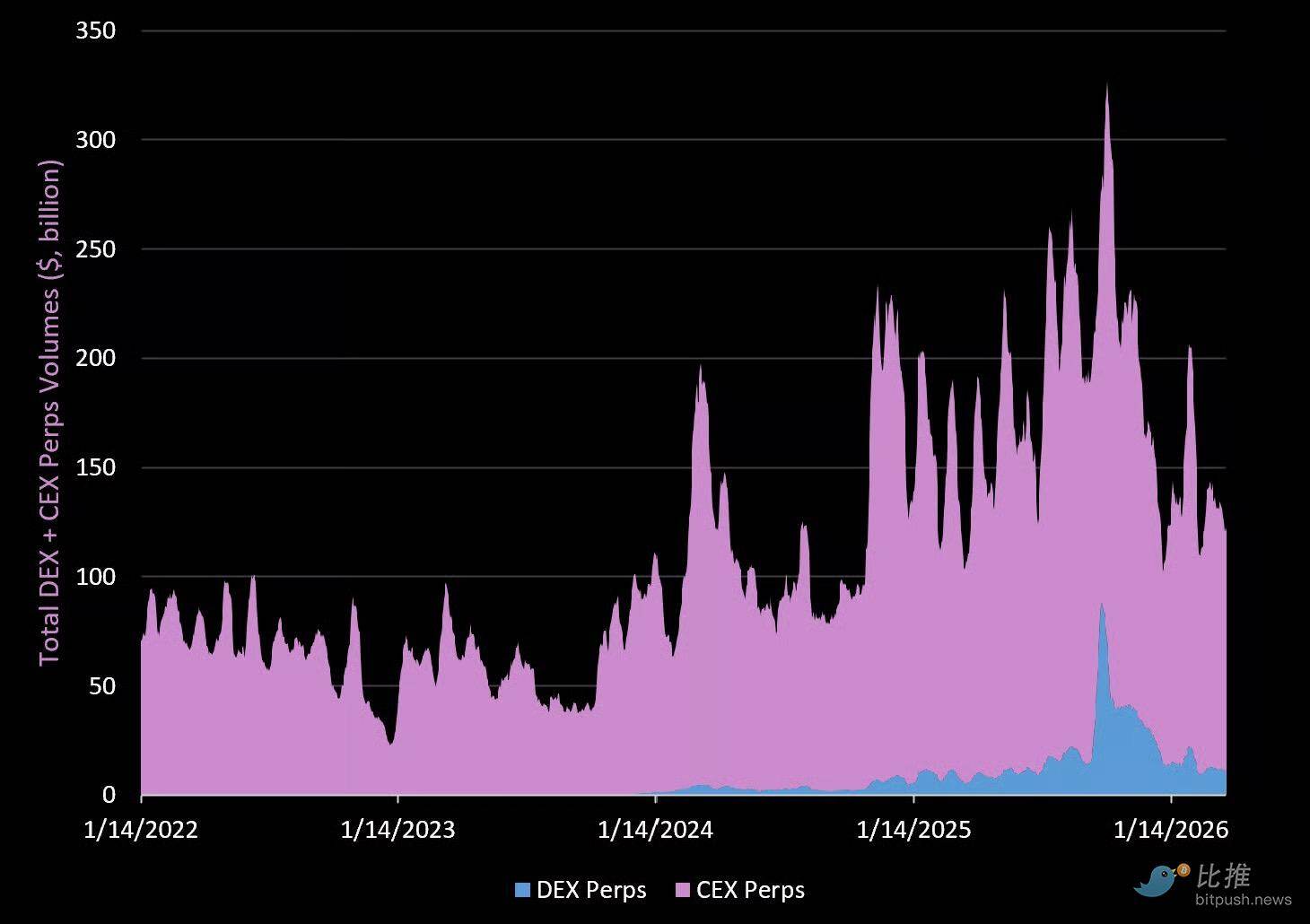

Perpetuals Market

Volume

Key Takeaways

- Total Perpetuals (Perps) volume is currently down 63% from the highs set in Q4 last year. CEX perps volume is down 57%, and DEX perps volume is down 84%.

- Perps volume is currently 4x daily spot volume, highlighting its appeal to retail traders.

- DEX perps volume currently accounts for 9.3% of CEX perps volume, up from 4% in early 2025.

- Hyperliquid currently accounts for about 60% of DEX volume and 4.6% of total (DEX + CEX) perps volume.

- On the CEX perps volume front, Binance is king this year with a 43% share. OKX has 20%, followed by Bybit and Gate (13%), and Coinbase International (5%).

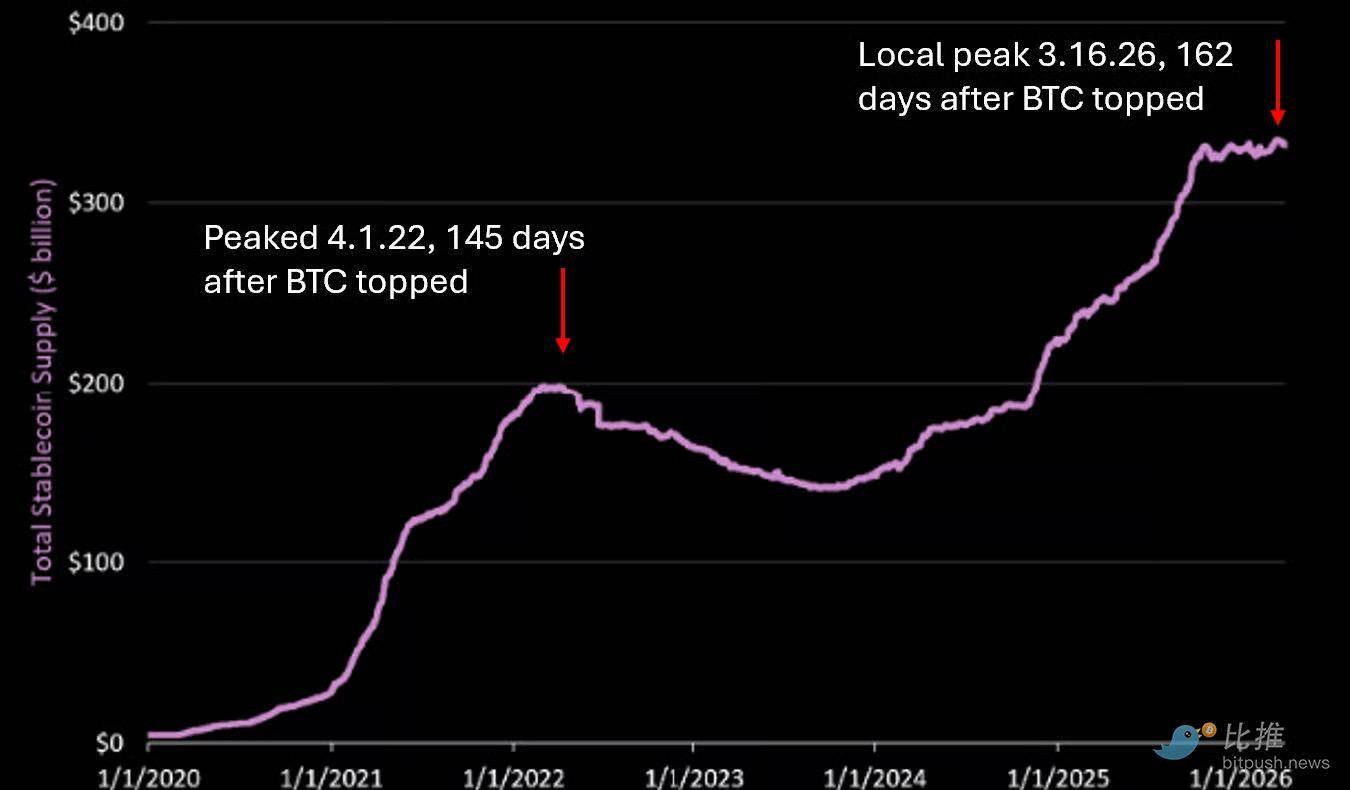

Stablecoins

Everyone is bullish on stablecoins, and so are we. Supply has grown by $192 billion over the past 2.5 years (now $333 billion). But we also believe this chart may be topping out for now.

Why?

- In the '21 cycle, stablecoin supply peaked on April 1, 2022 (nearly 5 months after BTC peaked and after being flat for over 3 months. USDC didn't peak until July '22).

- In the current cycle, we hit a local peak on March 16, 2026 (again, 5 months after BTC peaked).

- We've been flat for 5 months now due to:

- Stagnant fiat inflows into crypto (market is in "risk-off" mode).

- Deleveraging (real-world payments still make up a very small portion of stablecoin transactions).

- Declining reflexive yields in DeFi (no incentive to hold stablecoins given on-chain risks).

So far, we've only seen growth slow (supply flat for 5 months).

The next phase, in our view, is fiat redemptions.

After peaking in April 2022, it took stablecoin supply 2.5 years to reclaim that level. No one expects that to happen again this cycle (due to regulation). But regulation doesn't create demand for stablecoins in a "risk-off" environment.

Key Takeaways

- Regulation alone doesn't create new use cases, applications, banked stablecoins, and new payroll solutions. Those will come later.

- Furthermore, the GENIUS Act prohibits stablecoin issuers from sharing profits with holders. This may be good for Circle's and Tether's business models but doesn't help crypto end-users.

- Because of this, we believe regulation (as currently structured) will benefit offshore "yield-bearing stablecoins" like Ethena's USDe in the next market expansion.

- Finally, Tether recently hired KPMG, one of the Big Four accounting firms, as its auditor. The company hinted at IPO plans, and this move seems aligned with those plans. We also expect Tether to launch a US-compliant stablecoin and seek to build services around it.

- It's unclear what those services will be. But our view is that the winner of the stablecoin race will win by wrapping "sticky services" around the stablecoin. This could be payroll management, payments, remittances, and e-commerce, or it could be lending and banking.

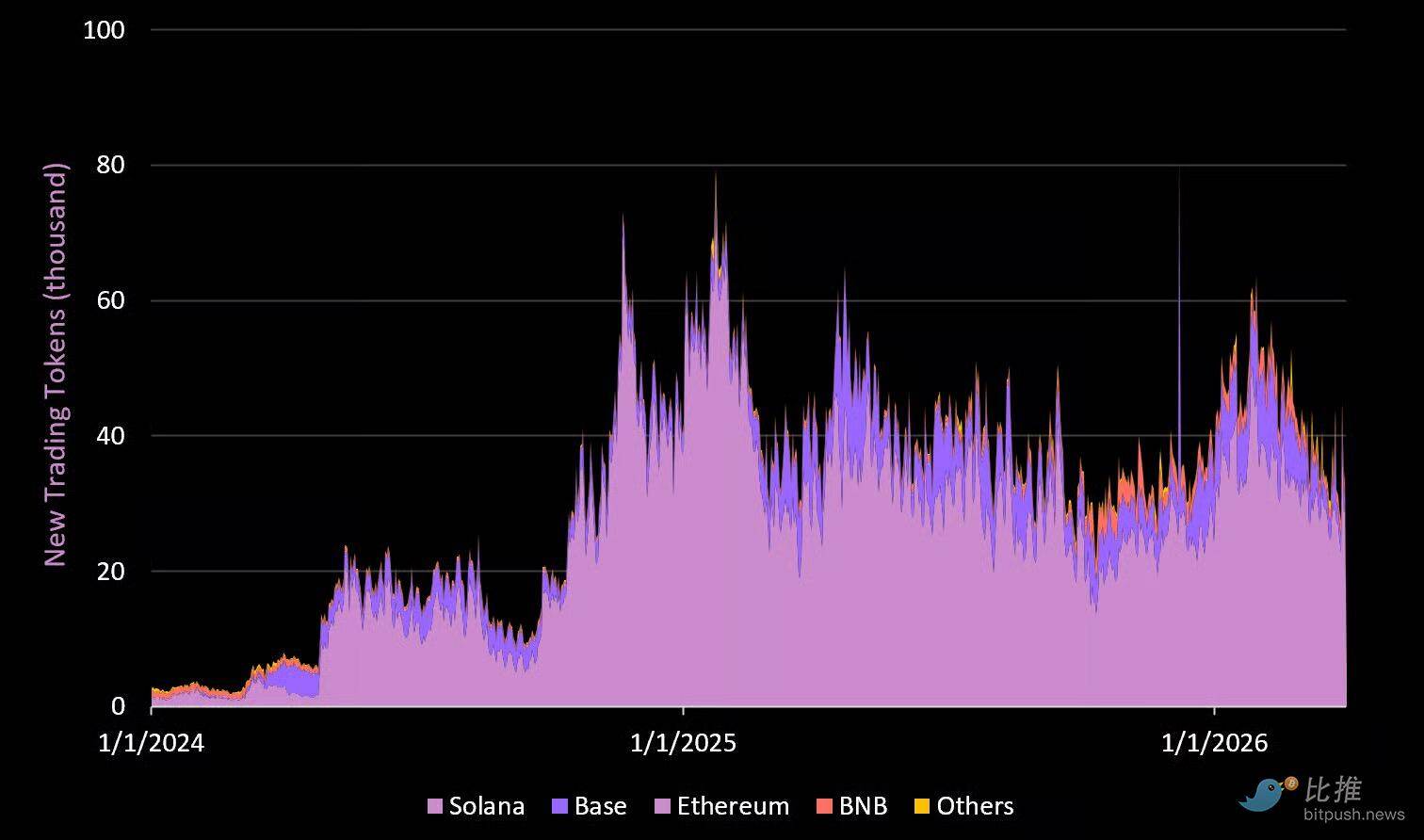

New Trading Tokens & Trading App Revenue

New Trading Tokens by Chain

Key Takeaways

- In every crypto cycle, a new "use case" helps bring new users into crypto. In the past cycle, it was the rise of launchpads on Solana and the ensuing meme coin trading.

- Many have strong opinions about meme coins. We think that's a mistake. Our approach is simply to observe the market. We believe there is product/market fit (PMF) here because there is demand for the "gamified" experience provided by top apps.

- The number of new trading tokens is currently down 53% from its peak in early 2025.

- Solana (via Pump Fun) currently commands an 83% market share, followed by Base at 10%.

- Pump Fun (one of the most profitable apps of the last cycle) has seen relatively stable revenue performance during the bear market. Currently, the app generates about $1.2 million in daily revenue across its Launchpad, DEX, and Padre (trading app). At the peak of the last cycle, its daily revenue was about $2.9 billion.

- We believe meme coins and trading apps are here to stay. More on the latter below.

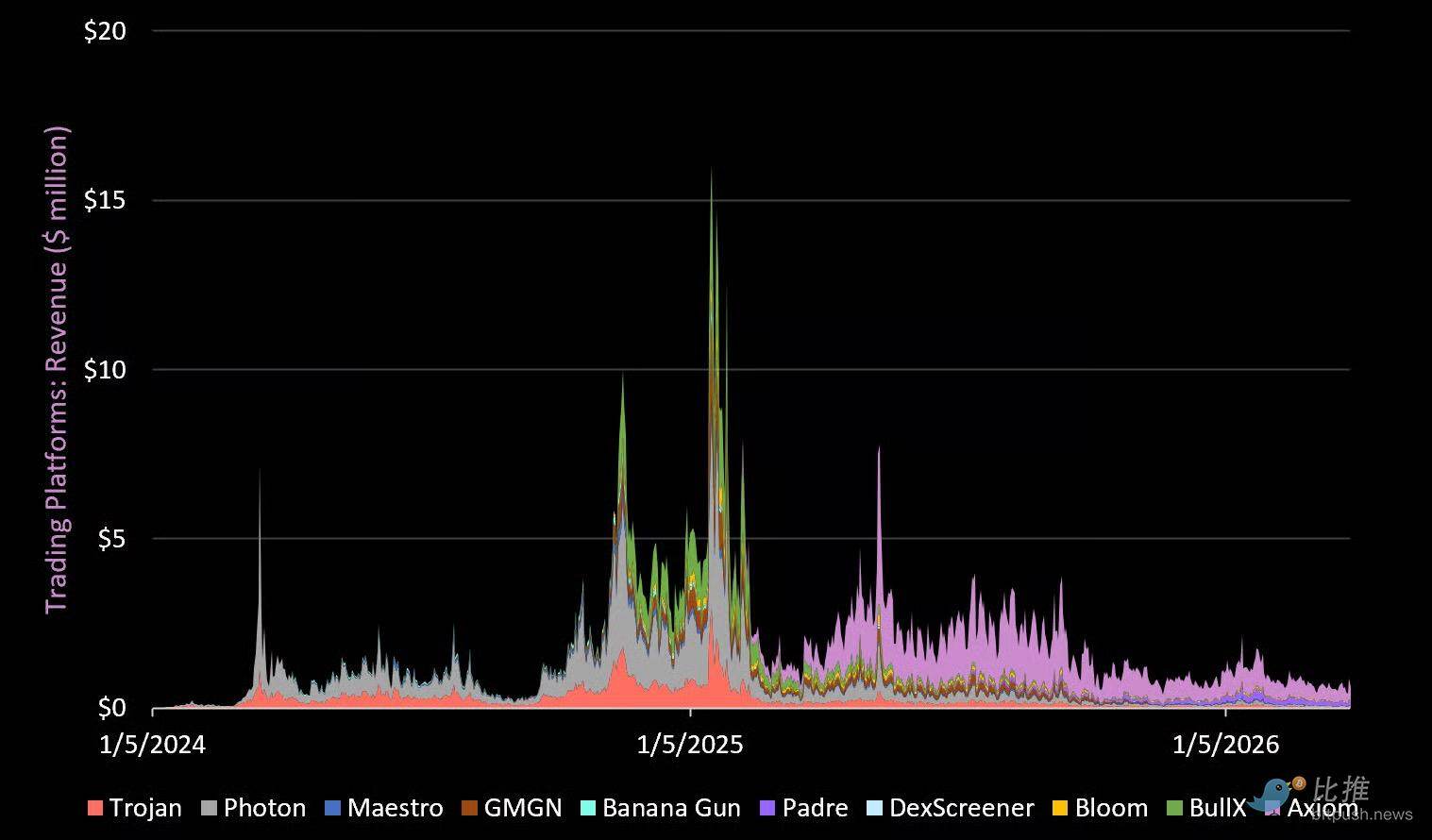

Trading App Revenue

Trading App Revenue

Key Takeaways

- Trading bots/apps were one of the most successful applications of the last cycle. At one point, they generated over $10 million in daily revenue. Total revenue is currently down 94% from its peak in early 2025.

- In early 2025, Axiom emerged, capturing significant market share by integrating wallet, trading, and social experiences into a user-friendly interface (while leveraging underlying decentralized infrastructure).

- Axiom (Q1 revenue: $34 million) currently holds a 68% market share in this category. Padre (acquired by Pump Fun) is second with 18%.

- We believe the crypto trading experience Axiom has built is the ultimate "crypto game." In our view, speculative meme coin trading is exactly that.

- With Pump Fun launching Pump Swap (DEX) last year and acquiring Padre (trading app), it's clear they are trying to own the entire end-to-end experience in this space.

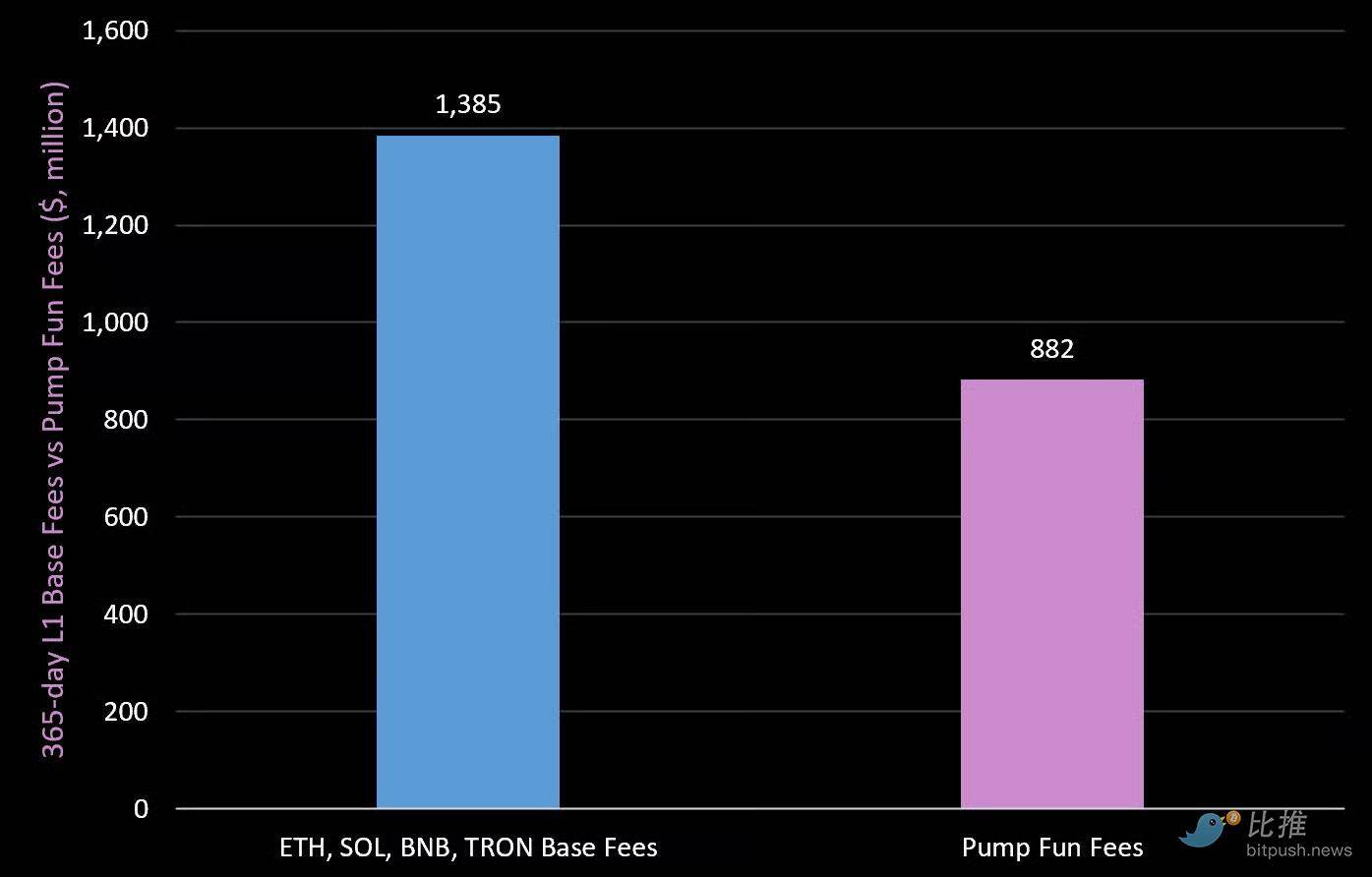

365-Day L1 Base Fees vs. Pump Fun Fees

Value is clearly moving up the tech stack, and we are seeing many apps launched by small teams rapidly scaling to hundreds of millions in revenue. We expect this trend to continue in the next market expansion, as top L1s now have the infrastructure and distribution capabilities to help the best builders launch and scale quickly.

Concluding Thoughts

The market is down. Sentiment is terrible, degens are licking their wounds, and the tourists have returned to their regular lives.

In other words, the tide has gone out.

That's why this is the best time to analyze the market.

Most crypto assets will never return to their all-time highs. But at the same time, the next 10-20x opportunity is hiding in plain sight. Oversold. Forgotten.

Until it explodes again.

That's why we are doing some of our most important research work right now. We are doing this work now so we are prepared when the next "fat pitch" arrives.