Circle is Undervalued: Despite Bill Pressure, Valuation Still Seen at $75 Billion

- Core Viewpoint: Despite recent market concerns and stock price decline triggered by the draft "CLARITY Act," the author's analysis using conservative assumptions suggests that Circle (the issuer of USDC) is currently fairly valued and is poised to benefit from the growth of the stablecoin market, potentially reaching a valuation of $75 billion by 2030.

- Key Elements:

- Significant Market Growth Potential: Conservatively adopting Citi's forecast, the stablecoin market size could reach $1.9 trillion by 2030, with payment convenience being the core growth driver rather than interest.

- Market Share Likely to be Maintained: The author believes Circle has the capability to defend its market position, especially dominating in regulated markets, and conservatively assumes it can maintain its current 25% market share.

- Profit Margins Face Pressure but Show Resilience: Competition may compress its interest income "take rate," but user stickiness (based on convenience and trust) and regulatory constraints (such as the CLARITY Act) may provide support. A conservative assumption is a take rate decline to 0.8%.

- Conservative Valuation Model: Based on the above conservative assumptions ($1.9 trillion market size, 25% share, 0.8% take rate), Circle's estimated after-tax net profit for 2030 is approximately $2.7 billion. Valuing it at a P/E ratio of 28x yields a valuation of $75 billion.

- Clear Upside Potential: If market growth (e.g., reaching $4 trillion), market share increases, or profit margins exceed expectations, Circle's valuation would be significantly higher than this conservative estimate.

Original Author: Matt Hougan, Bitwise

Original Compilation: AididiaoJP, Foresight News

Even considering recent concerns sparked by the CLARITY Act, my conservative estimate suggests Circle could be valued at $75 billion by 2030.

One of the most frequent questions we are asked is: "How can I invest in stablecoins?"

Typically, we suggest focusing on crypto assets that support the stablecoin ecosystem, such as Ethereum, Solana, and Chainlink, or on crypto companies operating in this space, like Circle and Coinbase. Since it's difficult to predict who will benefit most from the rise of stablecoins, some argue that investing in the entire sector is a reasonable approach.

However, among the many options, one opportunity stands out: Circle, the issuer of USDC, the world's second-largest stablecoin. It is the only publicly listed company with a business purely focused on stablecoins. In my view, this is the most direct choice.

So, is Circle a worthwhile investment?

Today is a good day to answer this question, as the stock has recently experienced a significant decline (down 20% on Tuesday) due to news that the latest draft of the CLARITY Act imposes restrictions on platforms paying interest income to stablecoin users. I believe the market's reaction is somewhat excessive.

To illustrate this point, it's necessary to examine Circle's future from a macro perspective.

Three Key Questions Determining Circle's Future Trajectory

1. How Large Will the Stablecoin Market Be?

The first question concerns the potential growth scale of the stablecoin market. There are various predictions, with the most widely cited being the research report from Citigroup. Its "base case" forecast projects stablecoin assets under management to reach $1.9 trillion by 2030; the "bull case" scenario predicts $4 trillion.

The news related to the CLARITY Act does not alter the above base case forecast. To date, interest income has not been a primary driver of stablecoin growth; currently, the vast majority of stablecoins are held in ways that do not generate interest. The widespread popularity of stablecoins lies in their ability to facilitate efficient, reliable global fund transfers, suitable for various scenarios such as trade settlement, lending collateral, and as an alternative to unstable fiat currencies.

Convenience is a core application value of money, and this is precisely where stablecoins excel. Currently, the national average savings account yield in the US is about 0.60%, and the average checking account yield is about 0.07%. Users keep funds in such accounts not for the purpose of pursuing yield. If the global financial system continues to migrate towards blockchain-based infrastructure, I expect stablecoins to play an increasingly important role in this transition, regardless of whether they offer interest.

In my judgment, the base case forecast proposed by Citigroup is actually quite conservative. Nevertheless, to adhere to a conservative analytical principle, we will use $1.9 trillion as the basis for subsequent estimates.

2. What Market Share Will Circle's USDC Capture?

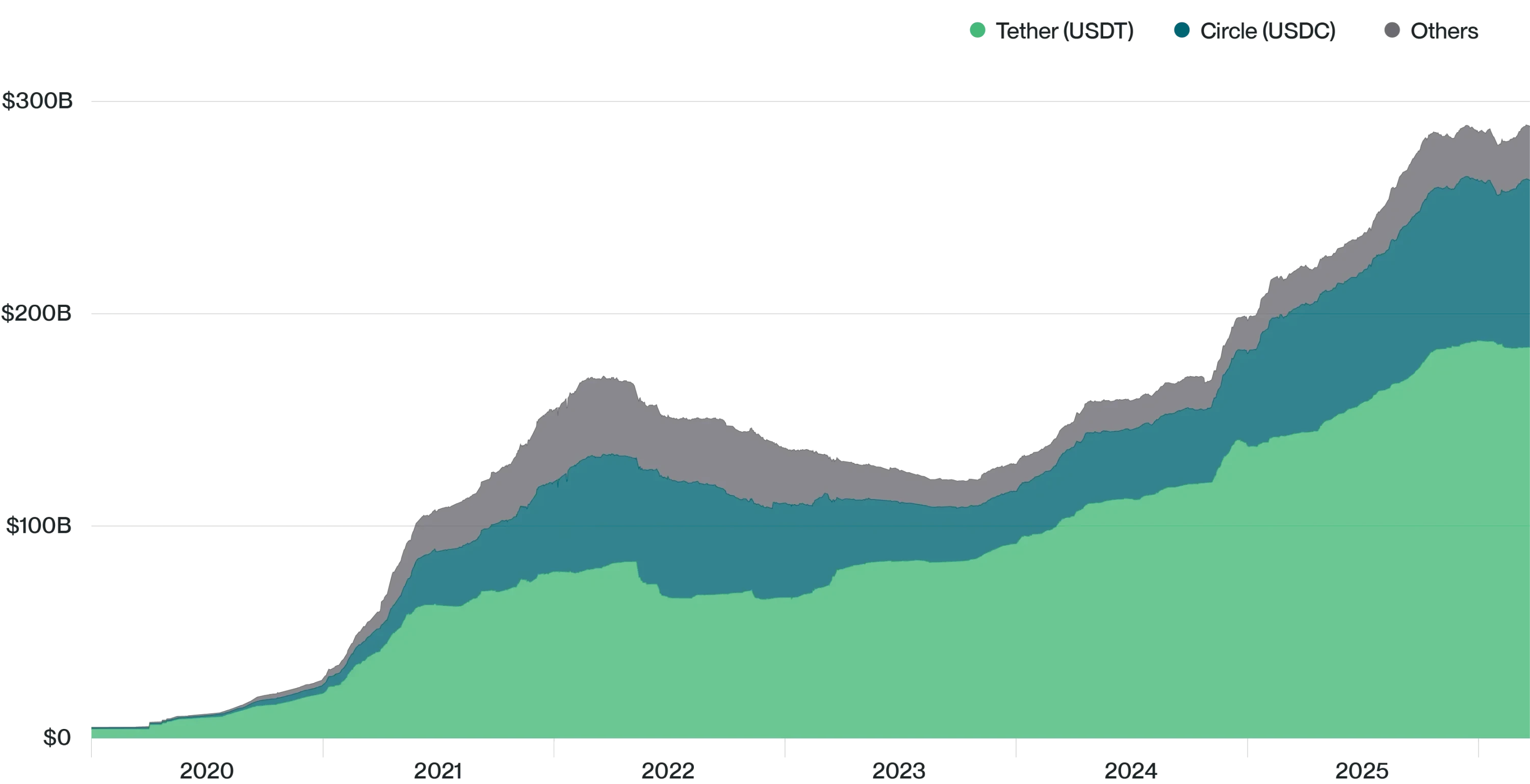

Currently, Circle's USDC accounts for 25% of the total stablecoin market, trailing behind Tether's USDT.

(Why not invest in Tether? Because Tether is a private company and cannot be invested in publicly.)

Stablecoin Market Cap Distribution

Source: Bitwise Asset Management, data from The Block. Data coverage period: January 1, 2020, to March 23, 2026. Note: "Other" includes BUSD, crvUSD, DAI, FDUSD, FEI, FRAX, GHO, GUSD, LUSD, MIM, PYUSD, TUSD, USDD, USDe, USDP, and USDS.

A common view is that as large institutions like US Bank, Stripe, and Wells Fargo enter the stablecoin space, Circle's market share will gradually decline.

I have reservations about this. Historical experience shows that innovative companies often defend their early market leadership positions quite well.

For example:

- In 1976, the world's first index fund was created by the then little-known Vanguard Group. Today, Vanguard is the leader in global passive asset management.

- In 1993, the first US exchange-traded fund, SPY, was launched by State Street, which was not a giant in the asset management industry at the time. To this day, SPY remains the world's most actively traded ETF, with assets under management exceeding $650 billion.

- In 1996, the first series of international ETFs was launched by a little-known asset management firm called Barclays Global Investors. The company was later acquired by BlackRock for $12 billion, and its business evolved into iShares, which now has $5 trillion in assets under management.

We are already seeing initial signs of Circle fending off competition from well-known companies: In 2023, the global digital payments giant PayPal launched its stablecoin PYUSD with great fanfare, but the product received a lukewarm market response. Currently, PYUSD's market share is just over 1%.

Of course, there are also cases where large companies catch up later and squeeze out pioneers. For example, in the money market fund space, fast followers like Fidelity, Vanguard, and Federated Hermes captured most of the market share from the original innovator, Reserve Fund Group. This is worth noting, especially considering the similarity between money market funds and stablecoins: both take in US dollar funds and invest them in high-quality short-term securities like US Treasuries.

Nevertheless, I still don't believe large banks can easily crush Circle. I think Circle's market share also has the potential to expand. After all, although Circle "only" holds a 25% share of the overall stablecoin market, its share in the regulated stablecoin segment is much higher (Tether's USDT primarily dominates the offshore market). While it's difficult to obtain precise data on Circle's share in the regulated market, I estimate it exceeds 80%. If one believes that the growth in stablecoin AUM will primarily come from regulated markets (because banks, fintech companies, and large enterprises tend to prefer onshore, regulated stablecoins), then Circle's market share could significantly exceed its current 25% level.

However, for the sake of conservatism in this analysis, I will balance these two forces and assume Circle merely maintains its current 25% market share going forward.

3. What Are Circle's Profit Margins?

The last question is the most complex and crucial: How much yield can Circle extract from its deposit assets?

Currently, Circle retains all interest income generated from the US Treasuries backing USDC. At current interest rate levels, this means its $80 billion in managed assets can generate approximately 4% yield annually.

However, this figure does not fully reflect Circle's actual revenue-generating ability, as it must also consider the distribution fees it pays to acquire managed assets. For example, USDC was co-developed with Coinbase and serves as the flagship stablecoin on that exchange. Under the relevant agreement, Circle pays all interest income generated from USDC held on the Coinbase platform to Coinbase, which then passes most of it on to users. Circle also has distribution agreements with other exchanges. Circle's rationale for this is that by paying fees to certain distribution channels, it can initiate a virtuous marketing cycle, attracting assets to flow directly, at which point Circle can capture a higher proportion of the revenue or monetize the assets in other ways in the future.

Overall, Circle currently pays about 60% of its revenue to distribution partners. This means, at current interest rates, its actual "take rate" is approximately 1.6%.

Is this level sustainable? Two major factors need consideration.

The first is the level of interest rates. Circle's interest income is directly tied to market benchmark rates. Fed rate hikes would benefit Circle, while rate cuts would be a headwind.

The second is the competitive landscape. If one envisions a market with hundreds of stablecoins where users can freely switch between USDC, WFUSD, BAUSD, PYUSD, etc., Circle's ability to maintain its interest income would be constrained. Basic economic principles suggest competition compresses profit margins.

However, I am skeptical of this. Markets that should theoretically be "perfectly efficient" often are not in reality. Charles Schwab earns billions of dollars annually from the spread between the interest it pays depositors and the interest it earns on deposits, despite customers being able to easily switch to higher-yielding alternatives. But customers don't always act because the core of their value proposition isn't yield, but convenience, trust, and business integration. USDC is similar in many ways: users hold USDC primarily for its broad applicability and credibility, not for interest returns. This user stickiness won't disappear overnight.

I would also point out that the current draft of the CLARITY Act might actually have a positive impact on Circle's profit margins, as it makes distributing interest income to stablecoin holders more difficult.

Overall, I believe Circle will face greater margin pressure in the future as competition intensifies. The company may even need to adjust its revenue model, which is a direction Circle is actively pursuing. For the purposes of this analysis, I will assume its take rate halves, dropping to 0.8%.

Conclusion

Answering these three questions does not cover the entirety of Circle's business. As mentioned earlier, Circle has launched its own blockchain, continues to innovate in payment technology, and its non-interest revenue is growing rapidly. But I believe examining the company through these three questions allows for an effective 80/20 analysis of its stock value.

Based on the above conservative estimates—a $1.9 trillion market size, a 25% market share, and a 0.8% take rate—the revenue after distribution costs but before other expenses would be $3.8 billion. Currently, the company's actual operating expenses are relatively low, at $144 million in 2025. This means that even if these costs double or triple by 2030, there would still be about $2.7 billion in post-tax net profit. Valuing Circle at the S&P 500's current average price-to-earnings ratio (28x) would make it a $75 billion company.

This figure is quite telling, approximately double the company's current value. This performance is decent, but considering market volatility, whether it's worth investing in may require further weighing.

It should be noted that at every step of the above analysis, I chose conservative assumptions. If stablecoin growth meets Citigroup's bull case expectations, or if Circle's market share grows (as it has recently), or if the company can maintain its current take rate or develop new revenue streams, the valuation outcome would be significantly higher.

Overall, I can envision scenarios where Circle's value by 2030 is far higher than my rough estimate, and also scenarios where it is lower. I believe the value of this analysis is that it indicates Circle's current valuation is within a reasonable range. If stablecoin development aligns with general market expectations, then even using quite conservative assumptions, Circle can still be seen as an attractive investment target.