Polymarket Market Making Bible

- Core Viewpoint: An academic paper constructs a complete market making framework for prediction markets, akin to the Black-Scholes model. Through Logit transformation, jump-diffusion models, and risk factor decomposition, it addresses the core pain point of the current lack of quantitative pricing and risk management tools in prediction market making. This is expected to drive the industry's evolution from intuition-driven to financial engineering-oriented.

- Key Elements:

- The core model employs Logit transformation to map probabilities to an unbounded space and introduces a jump-diffusion model to capture the daily fluctuations and news shocks of beliefs in prediction markets. Its martingale property implies market makers only need to price "uncertainty" (volatility) rather than "direction".

- The framework defines the Greeks for prediction markets (e.g., Delta = p(1-p)) and four types of risk (directional, curvature, information intensity, cross-event). It also performs inventory management based on an improved Avellaneda-Stoikov model, allowing spreads to adjust dynamically according to inventory, volatility, and time remaining.

- The paper proposes and derives pricing formulas for five key derivative products (e.g., belief variance swaps, correlation swaps), providing a toolbox for market makers to hedge tail risks, which is crucial for achieving narrow spreads and high liquidity.

- A complete workflow is constructed for calibrating key parameters (e.g., belief volatility σ_b, jump intensity λ) from noisy market data using Kalman filtering and the EM algorithm. A belief volatility surface is also built, making the model practically usable.

- Experimental validation shows the model significantly outperforms methods like random walk, GARCH, and direct modeling in probability space in terms of prediction error, especially near extreme probabilities, proving the necessity of modeling in Logit space.

Original Title: Toward Black-Scholes for Prediction Markets: A Unified Kernel and Market-Maker's Handbook

Original Source: Daedalus Research

Translation, Annotation: MrRyanChi (X: @MrRyanChi)

On the very first day of founding @insidersdotbot, a user asked me if it was possible to conduct market making through our product. With the launch of Polymarket's market maker incentive program, discussions about market making in various groups have become even more heated.

However, just like arbitrage, market making is a discipline that requires rigorous mathematics for discussion; it's definitely not money that can be earned simply by placing orders on both sides and providing liquidity. Market makers for traditional crypto futures have already made a fortune, yet market makers for prediction markets are still in their infancy, with vast profit opportunities existing.

Coincidentally, a while ago, recommended by a certain quantitative trading expert, I came across an academic paper by @0x_Shaw_dalen for @DaedalusRsch. It very comprehensively explains the entire logic of Polymarket market making strategies and how to specifically execute these strategies.

This original text is 100 times more technical than the last one, so I've also done an extensive amount of rewriting, research, and analysis, striving to ensure that everyone can understand the full picture of prediction market making without needing to look up additional information.

Whether your goal is to become the next big whale in prediction markets or to achieve significant results through airdrops and liquidity incentives, you need a thorough understanding of institutional-level market making techniques, and that's precisely what this article can do for you.

Preface

Before we begin, let me ask you two questions.

The first one: You are market making on Polymarket. The "Trump wins the election" contract is currently at $0.52. You have placed a buy order at $0.51 and a sell order at $0.53. Suddenly, CNN reports a major piece of news. How much should you adjust your spread? $0.02? $0.05? $0.10?

You don't know. Nobody knows. Because there's no formula telling you "how many percentage points of spread is this news worth."

The second one: You are simultaneously market making in three markets: "Trump wins Pennsylvania," "Republicans win the Senate," and "Trump wins Michigan." On election night, the results from the first key state come in. All three markets experience violent fluctuations simultaneously. Your entire portfolio loses 40% in 3 minutes.

You review it afterward and realize the problem wasn't misjudging the direction, but that you simply had no tools to measure the risk of "these three markets moving simultaneously."

These two problems were solved in the traditional options market back in 1973.

In 1973, the Black-Scholes formula gave everyone a common language. Market makers knew how to price spreads (implied volatility). Traders knew how to hedge the interconnected risk of multiple positions (the Greeks and correlation). The entire derivatives ecosystem, from variance swaps, the VIX index, to correlation swaps, was built on this foundation.

Earlier, I was fortunate to witness the wisdom of the inventors of the BS model at the Chinese University of Hong Kong.

But in 2025's prediction markets? Market makers adjust spreads based on intuition. Traders judge volatility based on gut feeling. No one can precisely answer "what is the belief volatility of this market?"

Today's prediction markets are the options market before 1973.

And this isn't just a theoretical problem; it's a real money problem.

Polymarket now has a complete market maker incentive system [15][16], with over $10M in incentives allocated to market makers. But the question is: if you don't have a pricing model, how do you know how tight the spread should be?

Set it too wide, and you don't get the rewards (because others are tighter than you).

Set it too narrow, and you get sniped by informed traders.

Without a model, you're like a blind man touching an elephant—make a little profit from rewards if you're lucky, lose your principal if you're unlucky.

Until I saw Shaw's paper [1].

What it essentially does is: write a complete set of Black-Scholes for prediction markets. Not just a new pricing formula—but a complete set of market making infrastructure: from pricing to hedging, from inventory management to derivatives, from calibration to risk management.

As a Polymarket trader and the founder of the @insidersdotbot trading platform, I've had in-depth exchanges over the past year with numerous market maker teams, quantitative funds, and developers of trading infrastructure. I can tell you: this paper solves precisely the questions everyone is asking but no one can answer.

If you don't know what Black-Scholes is, that's okay. This article will explain it from scratch; you don't need much foundational knowledge about market making.

If you do know, you'll be even more excited because you'll realize what this means: implied volatility, the Greeks, variance swaps, correlation hedging—all the tools from the traditional options market are about to enter prediction markets.

After reading this article, you'll have a complete market making and pricing framework, upgrading you from "setting spreads by gut feeling" to "setting spreads with formulas."

Chapter 1: The First Stop for Volatility Pricing - The Black-Scholes Model

Before talking about prediction markets as event contracts/binary options, we must first understand one thing: what exactly did Black-Scholes do? And why is it so important?

Before 1973: Options = Gambling

Before 1973, options trading was basically like this:

You think Apple stock will rise, and you want to buy the right to "buy Apple at $150 one month later" (a call option).

The problem arises: How much is this right worth?

Nobody knew.

The seller says: "$10." The buyer says: "Too expensive, $5." They finally settle at $7.50.

This was options pricing before 1973—haggling. No formulas, no models, no concept of a "correct price." Everyone was guessing.

The essence of an option is: using a small amount of money to buy a chance of "if I'm right."

The Core Insight of Black-Scholes

In 1973, Fischer Black and Myron Scholes published a paper [2], proposing a seemingly simple idea:

The price of an option depends only on one thing you don't know—volatility.

It doesn't depend on whether the stock will rise or fall (direction). It doesn't depend on how much you think it will rise (expected return). It depends only on how much it will fluctuate.

Why? Because they proved one thing: If you hold an option, you can "replicate" the payoff of that option by continuously buying and selling the underlying stock. The cost of this replication process depends only on volatility.

We can understand this with middle school math:

Imagine you're playing a coin game. Heads you earn $1, tails you lose $1. Someone sells you "insurance": If the final result is a loss, the insurance company covers it. How much is this insurance worth?

The key isn't whether the coin is "fair" (is the probability of heads 50%). The key is how large the fluctuation is per flip.

If each flip is ±$1, the insurance is cheap. If each flip is ±$100, the insurance is expensive.

Greater volatility → More expensive insurance → More expensive option. It's that simple.

What Black-Scholes did was turn this intuition into a precise formula.

Why Did This Change the Market Making Model?

Before Black-Scholes: Options were gambling. Traders priced by intuition, with no common language.

Black-Scholes established a complete consensus for options:

A common language was born. Everyone started quoting using "implied volatility." You no longer said "this option is worth $7.50"; you said "the implied volatility of this option is 25%." It was as if everyone suddenly started speaking the same language.

Risk could be decomposed. The risk of an option was broken down into several independent "dimensions"—Delta (directional risk), Gamma (acceleration risk), Vega (volatility risk), Theta (time decay). These are called the Greeks. Market makers could precisely hedge each dimension of risk.

A derivatives layer emerged. With a common language, you could build new products on top. Variance swaps (betting on volatility size), correlation swaps (betting on the linkage between two assets), the VIX index ("fear index")—all of these are "descendants" of Black-Scholes.

CBOE was established. The Chicago Board Options Exchange was founded in 1973—the same year as the Black-Scholes paper. This is no coincidence. With a pricing formula, options could be traded in a standardized way [3].

In other words, Black-Scholes turned options from "gambling" into "financial engineering." It's not just a formula—it's the starting point for an entire infrastructure.

Comparison before and after 1973.

Now, Market Making in Prediction Markets is in the Pre-1973 Era

In 2025, the monthly trading volume of prediction markets surpassed $13 billion [9]. NYSE's parent company ICE invested $2 billion in Polymarket at an $8 billion valuation [7]. Kalshi and Polymarket together hold a 97.5% market share.

But—

How do market makers price spreads? By intuition.

How do traders judge if a contract's volatility is "expensive" or "cheap"? By feeling.

How do you hedge the linkage between two correlated markets? No standard tools.

A news shock hits, how should the spread be adjusted? Everyone has their own crude method.

This is the options market before 1973.

And what the model in this paper does is: write a Black-Scholes for prediction market makers.

Chapter 2: Logit Transformation - Adapting the BS Model for Prediction Markets

First Question: How Are Prediction Markets Different from Stock Markets?

Stock prices can theoretically rise from $0 to infinity. Apple can go from $150 to $1500, or drop to $0.

Prediction market contract prices are always between $0 and $1.

The price of the YES contract for "Trump wins the election" is the market's perceived probability of that event happening. $0.60 = the market believes there's a 60% chance it will happen.

This difference seems minor, but it creates a huge mathematical problem:

You cannot directly apply Black-Scholes.

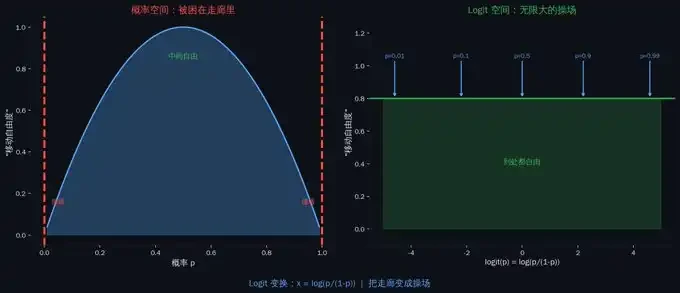

Why? Because Black-Scholes assumes prices can move freely along the entire number line (technically the positive half-line). But probability is "trapped" between 0 and 1. When probability approaches 0 or 1, its behavior becomes very strange—changing slower and slower, getting more "sticky" at the boundaries.

Imagine running in a hallway. In the middle of the hallway, you can run freely. But the closer you get to the walls, the more you have to slow down, or you'll crash. Probability is the same—the closer to 0 or 1, the more difficult it is to "move." Going from $0.50 to $0.55 is easy (one piece of news is enough), but going from $0.95 to $1.00 is extremely difficult (requires almost certain evidence).

Solution: Logit Transformation - Turning the Hallway into a Playground

The first key step of the paper: Don't model the probability p directly; instead, model its logit transformation.

What is logit?

x = log(p / (1-p))

It transforms probability p into "log-odds." Let's look at a few examples:

· p = 0.50 (fifty-fifty) → x = log(1) = 0

· p = 0.80 (very likely) → x = log(4) = 1.39

· p = 0.95 (almost certain) → x = log(19) = 2.94

· p = 0.99 (extremely certain) → x = log(99) = 4.60

· p = 0.01 (almost impossible) → x = -4.60

The finite interval of probability from 0 to 1 is mapped onto the entire number line from -∞ to +∞.

The hallway becomes a playground. The "stickiness" of probability near 0 and 1 disappears. Now you can freely use all traditional mathematical tools on x.

You may have seen the Logit transformation before: It's the inverse of the sigmoid function in machine learning. Sigmoid compresses any number into the 0-1 range (used to predict probability). Logit does the reverse: "unfolds" the probability between 0-1 onto the entire number line.

Why do this? Because probability behaves "awkwardly" near 0 and 1—going from 0.95 to 0.96 and from 0.50 to 0.51, while both are increases of 0.01, represent completely different amounts of information. The logit transformation flattens out this "non-uniformity." In logit space, equal changes represent equal amounts of information shock.

Logit Transformation

Jump Term, Diffusion, and Drift: The Jump-Diffusion of Belief

Now we are in logit space. Immediately after, the paper proposes the core rate of change model as follows:

dx = μ dt + σ_b dW + Jump Term

Don't be intimidated by the formula. Three parts, each should become an intuition in your market making process:

Diffusion (σ_b dW): This is the belief volatility. The speed at which probability changes slowly in the absence of major news, due to continuous information flow (poll updates, analyst comments, social media sentiment). This is the "implied volatility" of prediction markets—the core concept of this entire article. Market maker spread pricing, derivative pricing, risk management—all revolve around this σ_b.

Jump Term: Sudden probability shifts caused by breaking news. A key mistake in a debate, an unexpected policy announcement, a sudden withdrawal—these are not "slow diffusion" but "instantaneous jumps."

Drift (μ): The "natural trend" of probability over time. But here's a key point—the drift is not free; it is completely locked. Let's explain why below.

Imagine you're watching election polls.

Most of the time, support rates change by 0.1-0.3 percentage points per day—this is diffusion (σ_b dW). Like ripples on water, continuous but gentle.

Then one night, a candidate says something disastrous in a debate. Support plummets overnight from 55% to 42%—this is a jump. Like a rock thrown into the water.

This model captures both "ripples" and "rocks." Traditional Black-Scholes only has ripples (pure diffusion), no rocks (jumps). The model in this paper is more complete—because news shocks in prediction markets are far more frequent and severe than in stock markets.

Jump-Diffusion Model

Drift is Locked: The True Alpha for Market Makers

This is one of the most ingenious parts of the entire paper.

In traditional Black-Scholes, there is a famous conclusion: Option pricing does not require knowing whether the stock will rise or fall. You don't