Stablecoins are not necessarily enemies of banks; they can be a cash cow.

- Core Viewpoint: Ubyx, founded by former Citigroup executive Tony McLaughlin, aims to build a Visa-like, multi-issuer universal clearing network for stablecoins. It redefines stablecoins as "negotiable instruments" rather than crypto assets, thereby generating fee income for banks and addressing their fears of "deposit outflows."

- Key Elements:

- Founder Background: Tony McLaughlin is a former Managing Director at Citigroup who led the design of the Regulated Liability Network (RLN). He later shifted to public chain solutions, believing private chains face "cold start" challenges.

- Core Analogy: Compares stablecoins to "American Express traveler's checks," emphasizing their essence as negotiable instruments promising redemption at face value. The key is establishing a clearing network that guarantees face-value redemption, not the technology itself.

- Business Model: Ubyx adopts a "collection model." Banks redeem stablecoins for clients at face value through its network and collect fees. Banks do not bear balance sheet risk. It is projected to create tens of billions in annual revenue for the banking industry.

- Market Validation: Secured diversified capital investments from Galaxy Ventures, Founders Fund, Coinbase Ventures, and Barclays Bank, among others. Investors include several stablecoin issuers, creating a "investor-as-user" network effect.

- Potential Challenges: Faces competition from large issuers like Circle building their own proprietary networks, as well as regulatory uncertainty regarding whether stablecoins should accrue interest. This directly impacts market growth speed and bank participation incentives.

Original Author: James, Head of Ecosystem at the Ethereum Foundation

Original Compilation: Chopper, Foresight News

Last year, I first spoke with Tony McLaughlin, not long after he had left Citigroup to found Ubyx. What struck me most was this: a person who had spent 20 years at one of the world's top-tier banks spoke about public blockchains with the conviction of a crypto-native, yet every argument was grounded in the real mechanics of check clearing and correspondent banking.

As a payments industry veteran, McLaughlin genuinely believes the infrastructure he spent his career building is about to be replaced.

McLaughlin isn't the startup founder you might imagine. He's a seasoned payments executive from one of the world's largest banks, and his approach to building a company reflects that: propose an idea, take it to market, and let the market tell you if you're right or wrong.

How can stablecoins truly become ordinary money? The kind that appears in your bank account, equivalent to cash.

His answer involves a piece of infrastructure so mundane that most in crypto have never thought about it, and those in traditional banking haven't yet realized they need it.

Building the System, Then Walking Away

First, a brief overview of McLaughlin's career trajectory, as his background is crucial to this story.

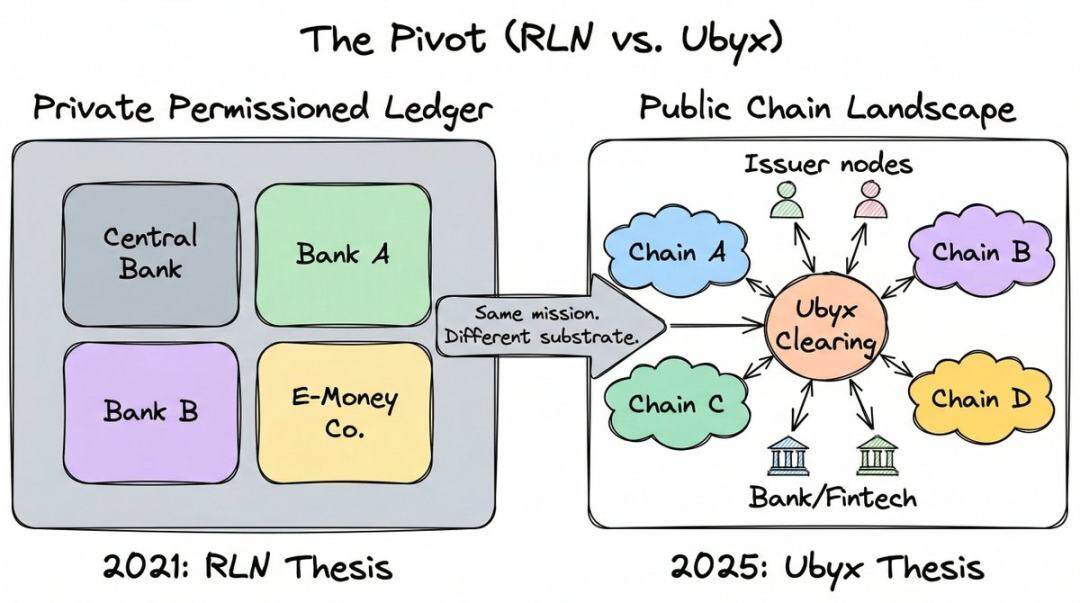

He spent nearly 20 years at Citigroup, rising to Managing Director in Treasury and Trade Solutions, focusing on emerging payments. During this time, he became the principal designer of the Regulated Liability Network (RLN), arguably one of the most influential institutional-grade blockchain concepts of the past five years.

The RLN proposed a shared, private ledger where central banks, commercial banks, and e-money institutions could all issue tokenized liabilities on the same platform—a regulated industry's response to public cryptocurrencies.

McLaughlin completed proofs-of-concept with the Federal Reserve and UK Finance, and the idea influenced work at the Monetary Authority of Singapore. The Bank for International Settlements (BIS) also acknowledged the RLN as inspiration for its "unified ledger" concept. The Agorá project, uniting seven central banks and over 40 financial institutions, adopted a similar architecture. By any measure, this was heavyweight infrastructure.

Then, McLaughlin resigned, walking away from the project entirely.

For years, he had worked to argue that private, permissioned chains were the future of regulated money. The technology itself wasn't the problem; the problem was that no one could solve the cold-start dilemma.

You ask all the world's major banks and central banks to join a network that doesn't yet exist, and no one wants to move first. In a podcast, he called it the "bootstrapping problem": you have to start the network for others to use it, but no one wants to help you start it because no one is using it yet.

Public chains solved this long ago. They have users, liquidity, and developers. The cold start is a thing of the past.

The moment of clarity for him came during the 2024 US election. Observing the political direction, he concluded that stablecoin regulation was inevitable, meaning banks would eventually be allowed to operate on public chains because that's where stablecoins are. The GENIUS Act, signed into law in July 2025, proved him right.

He described the decision in his characteristically blunt way: "From that day, I decided I would never spend another second of my life trying to push private permissioned chains."

He left Citigroup and founded Ubyx in March 2025.

The Banking Misconception About Stablecoins

On March 3, 2026, President Trump publicly accused US banks of "sabotaging" the GENIUS Act and "holding hostage" his crypto agenda. The core of the conflict was yield.

Banks have been lobbying heavily against interest-bearing stablecoins, arguing they would siphon deposits away from the traditional banking system. The Bank of England has considered holding caps on stablecoins for the same reason.

The fear is real: global stablecoin issuance has surpassed $300 billion. If this represents deposits leaving commercial bank balance sheets, the impact on lending capacity would be immense.

But McLaughlin believes the question is being asked backwards. For the past year, he has stuck to one argument in every forum and podcast: stablecoins are not a threat to deposits; they are a massive revenue gift.

The starting point of the misconception is how people categorize the instrument.

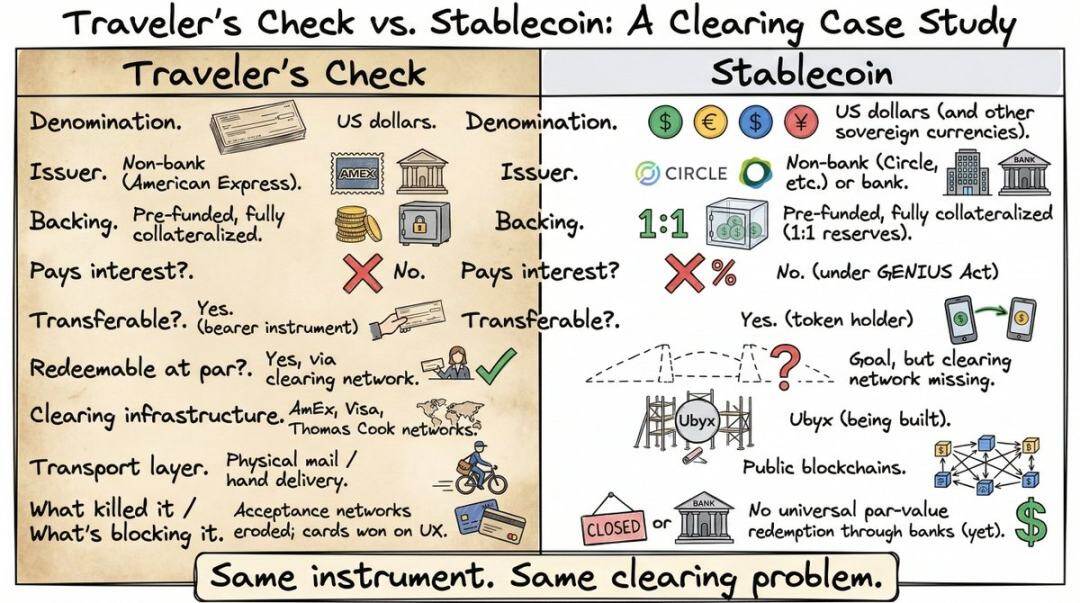

He says, "If regulators define a stablecoin as a 'crypto asset pegged to fiat currency,' I think they are making a fundamental mistake. To me, that's like saying 'a check is a piece of paper pegged to fiat currency.'"

His point is that regulators are making a mistake with stablecoins they would never make with checks: they are defining the instrument by its technology (a crypto token) rather than by its actual function (a promise to pay at face value). The technology is incidental; the promise is core.

Writing "I owe you $10" on a clay tablet, a piece of paper, or an ERC-20 token on Ethereum—the legal instrument is the same. What matters is who makes the promise and whether it is enforceable.

In his framework, a stablecoin is not a novel crypto-native creation. It is the latest manifestation of one of the oldest instruments in commercial law: the negotiable instrument.

He analogizes it to the American Express Travelers Cheque of 1891.

If you're under 35, you may have never used or even heard of them. Before debit cards and ATMs blanketed the globe, travelers cheques were the primary way people carried cash abroad. You purchased them from American Express or a bank before your trip, prepaying the face value. You could then spend them like cash anywhere in the world, with merchants or local banks accepting them at face value because the clearing network guaranteed they would get paid by the issuer.

I remember using them backpacking in Asia, and thinking about it now gives me a headache: queuing at bank counters, signing and countersigning, waiting for the clerk to call the issuer, with terrible exchange rates. No wonder they vanished almost overnight once bank cards became ubiquitous.

But their attributes are identical to stablecoins: a dollar instrument, non-bank issued, pre-funded, fully collateralized, non-interest-bearing, transferable to the bearer, redeemable at face value.

McLaughlin's analogy is correct, but most listeners didn't truly grasp it. Most people don't see the clearing problem for stablecoins precisely because most never used the tool that solved it back then. Travelers cheques are gone, and the clearing infrastructure behind them is forgotten history. So when McLaughlin says "stablecoins need what travelers cheques had," listeners nod politely but don't truly understand.

Once you view it through this lens, the question is no longer: "How do we protect deposits from stablecoins?" It becomes: "How do we handle stablecoins like we've handled every other negotiable instrument for the last 200 years?"

The Dull but Crucial Part

Travelers cheques were accepted globally at face value not because the paper was special, but because American Express, Visa, Thomas Cook built clearing networks guaranteeing any merchant in any country could exchange the cheque for cash at face value.

When the acceptance network crumbled, usage of travelers cheques collapsed. The instrument didn't fail; the channel did.

Stablecoins are in the exact same position now. They can cross borders on public chains in seconds, but there is no universal mechanism to redeem them at face value through a regulated financial institution.

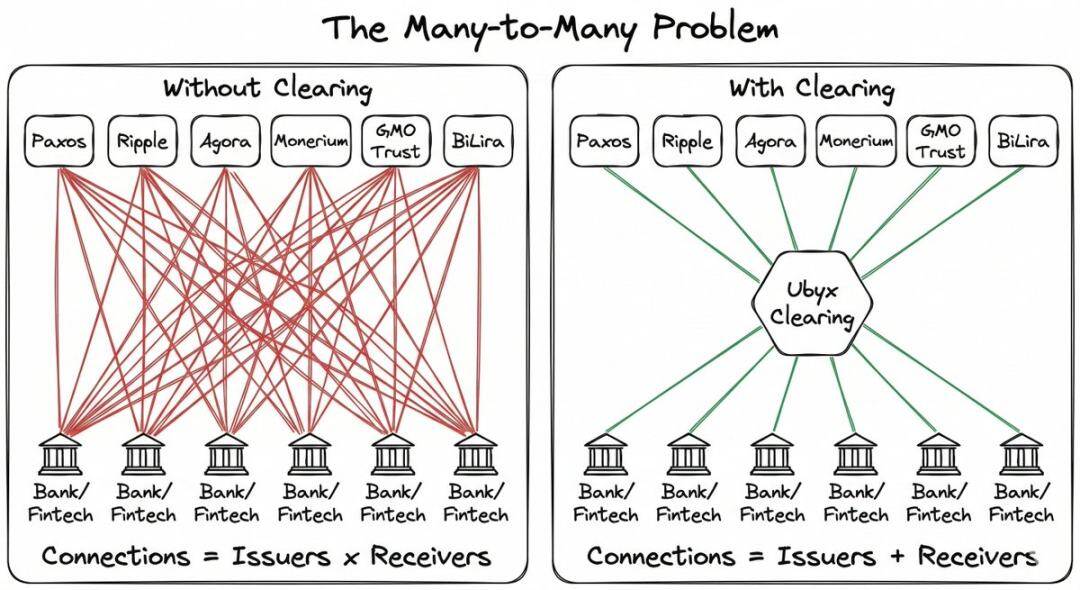

If you're a stablecoin issuer, you must build your distribution network from scratch, negotiating bilateral deals one by one. If you're a bank wanting to accept stablecoins for clients, you must negotiate separately with each issuer. The complexity grows exponentially.

McLaughlin's favorite example is credit cards. There are thousands of banks issuing credit cards globally, which sounds like it should be a mess. But you almost never walk into a store and are told, "Sorry, we don't take your card."

This fragmentation is invisible to the user because Visa and Mastercard sit in the middle, making every card work everywhere.

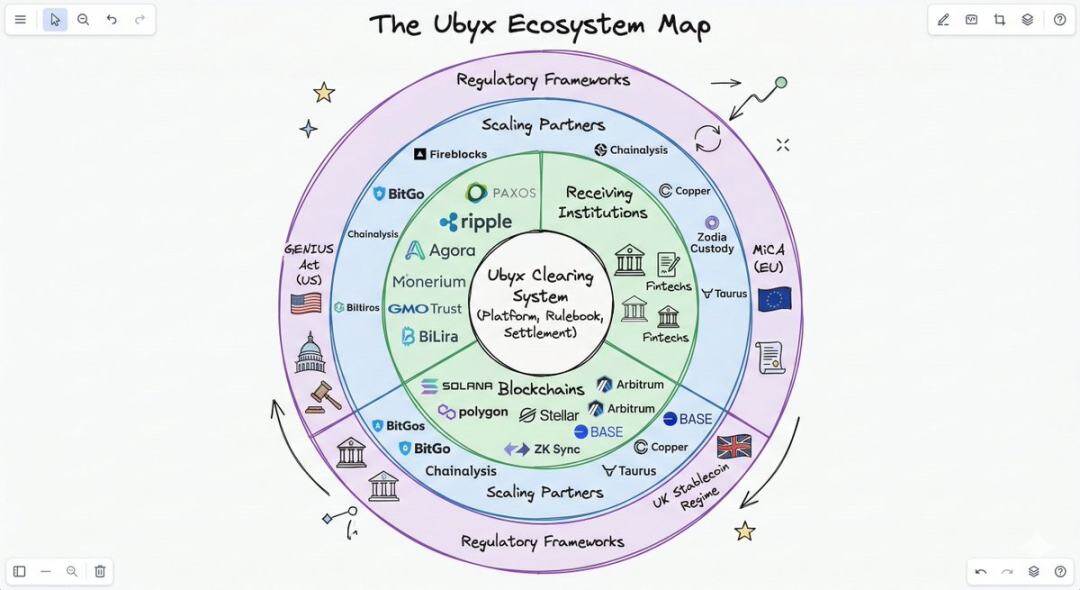

Stablecoins have the fragmentation but lack the clearing network. This is precisely the gap Ubyx aims to fill.

How Clearing Actually Works

The mechanism design is simple, and its difference from crypto exchanges is the core point.

On an exchange, stablecoins are bought and sold at floating market prices, with no guarantee of face value redemption. Exchanges are trading venues; if demand drops, the price follows.

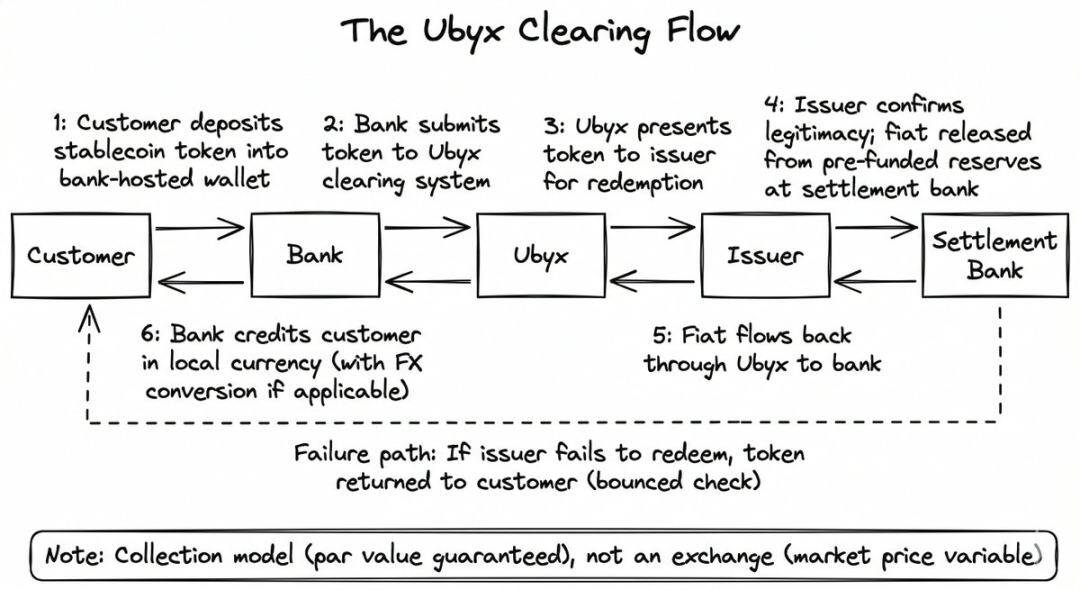

Ubyx doesn't do that. It operates on a collection model, not a trading model. The goal is redemption at face value, just like depositing a check at your bank.

You don't care who issued the check or which bank it's from. You give the check to your bank, your bank credits you at face value, and behind the scenes, the clearing system collects the money from the issuing bank. If the check bounces, the bank returns it to you. Simple.

Ubyx's process is the same:

- A customer deposits a stablecoin (e.g., USDC) into the bank's custodial wallet.

- The bank submits the token to Ubyx.

- Ubyx forwards it to the issuer (Circle, in this example).

- The issuer validates the token's legitimacy and releases fiat currency from pre-funded reserves at a settlement bank.

- The dollars flow back through Ubyx to the accepting bank, which credits the customer (typically converting to local currency after a forex spread).

If the issuer fails to pay, the bank returns the token to the customer, just like a bounced check. The bank takes no balance sheet risk during the clearing process.

McLaughlin describes the system as a "black box" with three modes:

- Stablecoin in, cash out (redemption)

- Cash in, stablecoin out (issuance)

- Stablecoin A in, Stablecoin B out (exchange)

It's designed to be issuer-agnostic, chain-agnostic, and currency-agnostic. At launch, issuers include over a dozen like Paxos, Ripple, Agora, Transfero, Monerium, GMO Trust, BiLira, covering USD, GBP, EUR, and emerging market currencies across multiple public chains.

For banks, the technical integration cost is deliberately kept minimal. Most banks won't build their own blockchain infrastructure, and even if they did, they'd face the problem of getting other banks to trust it.

$36 Billion

This is where the deposit fear narrative flips.

McLaughlin's rough math: Assume the stablecoin market reaches $1 trillion (it's currently $300B and growing). Conservatively assume 0.5% of circulating tokens are redeemed daily, leading to roughly $1.8 trillion in annual redemption volume.

If banks charge a 100 basis point fee, plus a 100 basis point cross-border forex spread, the annual revenue pool would be $36 billion.

These are his assumptions, and the math is roughly correct. For any bank, the question is simply: how much do you want?

For non-US banks, the economics are especially enticing. Every dollar stablecoin that enters the European or Asian banking system and is converted to local currency is pure forex income for the accepting bank. Forex is "high-margin" business for banks.

For the past year, McLaughlin has called offshore stablecoins a "gift" in every forum.

The alignment of this model with central bank objectives makes it more compelling than just a revenue calculation.

When stablecoins are redeemed through regulated entities into custodial wallets, they become visible to tax systems, pass AML/KYC screening, and are converted into local currency sitting on a local bank's balance sheet. Central banks get compliance and monetary transparency, commercial banks get fee income and expand their balance sheets, and customers get face-value conversion.

McLaughlin's advice to bank CEOs is very specific: accept first, issue later. "With stablecoins, it's better to receive than to issue. Why? Because you can make a lot of money by receiving."

The most straightforward business logic lies in accepting and exchanging third-party stablecoins. Once a shared acceptance network is built, and any bank can clear any stablecoin like a Visa transaction, the barrier to issuance plummets.

Then, issuing your own stablecoin becomes as simple as issuing a credit card. You don't need to build the acceptance network; you just plug into it.

Who Believes This Argument

Ubyx's shareholder list is worth examining because the names tell you which forces believe it.

Ubyx closed a $10 million seed round in June 2025, led by Galaxy Ventures. The rest of the round is a "dream team" of investors who typically wouldn't appear on the same cap table: Peter Thiel's Founders Fund, Coinbase Ventures, VanEck, LayerZero.

Silicon Valley libertarian capital, a top crypto exchange, a large traditional asset manager, all investing in stablecoin clearing infrastructure. Multiple investors are also network participants: Paxos and Monerium are both investors and issuers on the network; Payoneer and Boku invested as strategic partners.

This "investor-as-network-user" structure is deliberate. McLaughlin explicitly compares it to the early equity structure of Visa and Mastercard: the banks using the network own the network.

In January 2026, Barclays made a strategic investment. This is the UK's second-largest bank by market cap and its first-ever investment in a stablecoin company. Ryan Hayward, Barclays' Head of Digital Assets & Strategic Investments, stated: "Interoperability is key to unlocking the full potential of digital assets."

The subtext: one of Europe's most systemically important banks understood the logic of stablecoin clearing and decided to vote with its wallet.

A month later, AB Xelerate, the fintech accelerator of Arab Bank, also made a strategic investment. Now, US venture capital, a European bank, and Middle Eastern financial infrastructure are all betting on the same direction.

What Could Go Wrong?

Circle launched its own Circle Payments Network in mid-2025, providing proprietary infrastructure for USDC settlement. Circle has the scale to build its own distribution system.

The market question is: will it be a single-issuer network (Circle's path) or a multi-issuer clearing system (Ubyx's path)? McLaughlin's argument is that history favors diversified clearing models. But Circle's first-mover advantage and dominant market share are realities.

The yield battle between banks and crypto companies remains unresolved. The US Office of the Comptroller of the Currency's (OCC) proposed rule draft includes a rebuttable presumption against yield mechanisms for stablecoins.

If yield is prohibited, banks can breathe a sigh of relief, as stablecoins would remain less attractive than savings accounts for people parking cash. But it also means stablecoin use cases would be confined to payments and settlement, a smaller market, slowing Ubyx's growth.

If yield is allowed, the stablecoin market would explode, directly competing with deposits, money market funds, and Treasuries for idle cash. Banks would have every reason to build infrastructure rapidly, both defensively (to prevent client flight) and offensively (to capture forex and fee revenue).

Ubyx promises an open-source rulebook and eventual DAO governance via a token. This aligns philosophically with the decentralized networks it connects, but it remains an untested model for the regulated financial market infrastructure banks rely on.

Summary

The first phase of McLaughlin's career was defending the fiat system against the crypto challenge. The second phase was building private chains for banking. In the third phase, he concluded private chains couldn't solve the adoption problem.

The change lies in his view of where the money sits. On public chains, in wallets, cleared through a piece of infrastructure that makes every regulated stablecoin as reliable and innocuous as a check.

He believes the key to the entire transition lies in one sentence: Banks can treat stablecoins like they treat checks.

If a credible authority says that sentence, then every bank and fintech company globally would instantly know what to do. Ubyx is betting someone will say it soon.