Buffett Indicator Skyrockets, Bitcoin Stands at a Macroeconomic Crossroads

- Core View: Bitcoin is currently at a critical stage driven by macro liquidity. Its price trajectory will primarily depend on the sequence between credit market stress and policy-driven market rescue actions, rather than any specific narrative.

- Key Elements:

- The current macro environment exhibits a "triple bubble": extreme stock market valuations, real estate suppressed by high interest rates, and private credit surging toward $2 trillion, setting the stage for high volatility in risk assets.

- If the credit market cracks first, triggering a liquidity drought, Bitcoin, as a 24/7 liquid asset, would face severe selling pressure, potentially leading to a 20%-40% decline.

- If policy rescue (e.g., Fed balance sheet expansion, lowering real yields) precedes credit stress, Bitcoin, as a high-beta liquidity asset, would rebound rapidly, outperforming traditional risk assets.

- Current monitoring signals (modest Fed balance sheet expansion, tight high-yield bond spreads, elevated real yields, flat stablecoin supply) indicate a neutral-to-bearish liquidity environment, with the market awaiting a catalyst.

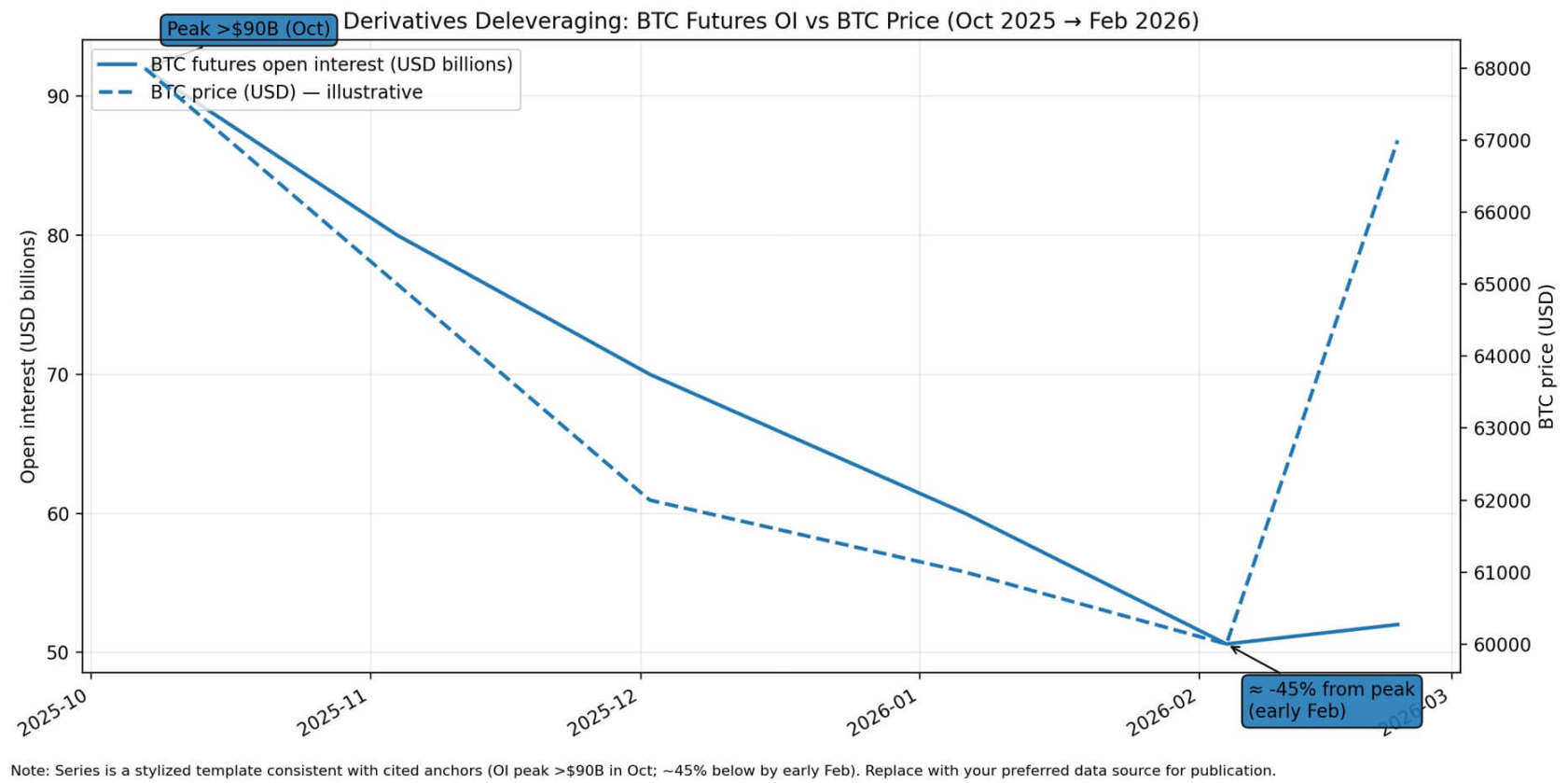

- Bitcoin futures open interest has fallen over 45% from its peak, indicating reduced leverage. However, if credit pressure emerges, there is still room for further selling.

- The tracking framework should focus on credit spreads, the Fed's balance sheet, real yields, and changes in stablecoin market capitalization to determine whether the market is shifting towards a liquidation or rescue mode.

Bitcoin is entering a phase where macro rhythms matter more than narratives.

Equity markets are near historical highs, real yields remain elevated, and credit markets are expanding into increasingly opaque corners of the financial system. These conditions do not guarantee an immediate crisis, but together they form a backdrop for a potential window of high volatility in risk assets.

For Bitcoin, the core question is: will stress manifest within an underlying financial system of elevated asset valuations, and how quickly can policymakers step in to contain it?

Macro strategist Michael Pento describes the current setup as a "triple bubble": equity valuations near historical extremes, real estate suppressed by mortgage rates near 6%, and private credit AUM racing towards $2 trillion. The label is catchy, but the framework is useful because it emphasizes sequence.

If credit cracks first, liquidity evaporates instantly, and Bitcoin is likely sold off alongside other assets. If policy support arrives before a crisis spreads, Bitcoin becomes a high-beta liquidity trade, rebounding faster than traditional risk assets.

Financial systems rarely collapse because valuations are too high. They collapse when credit and bond chains are forced to sell. Bitcoin's 24/7 liquidity means its volatility during panic and bailout rallies is almost more extreme than any other asset.

Recent data shows stress signals are accumulating but have not yet triggered a breakdown.

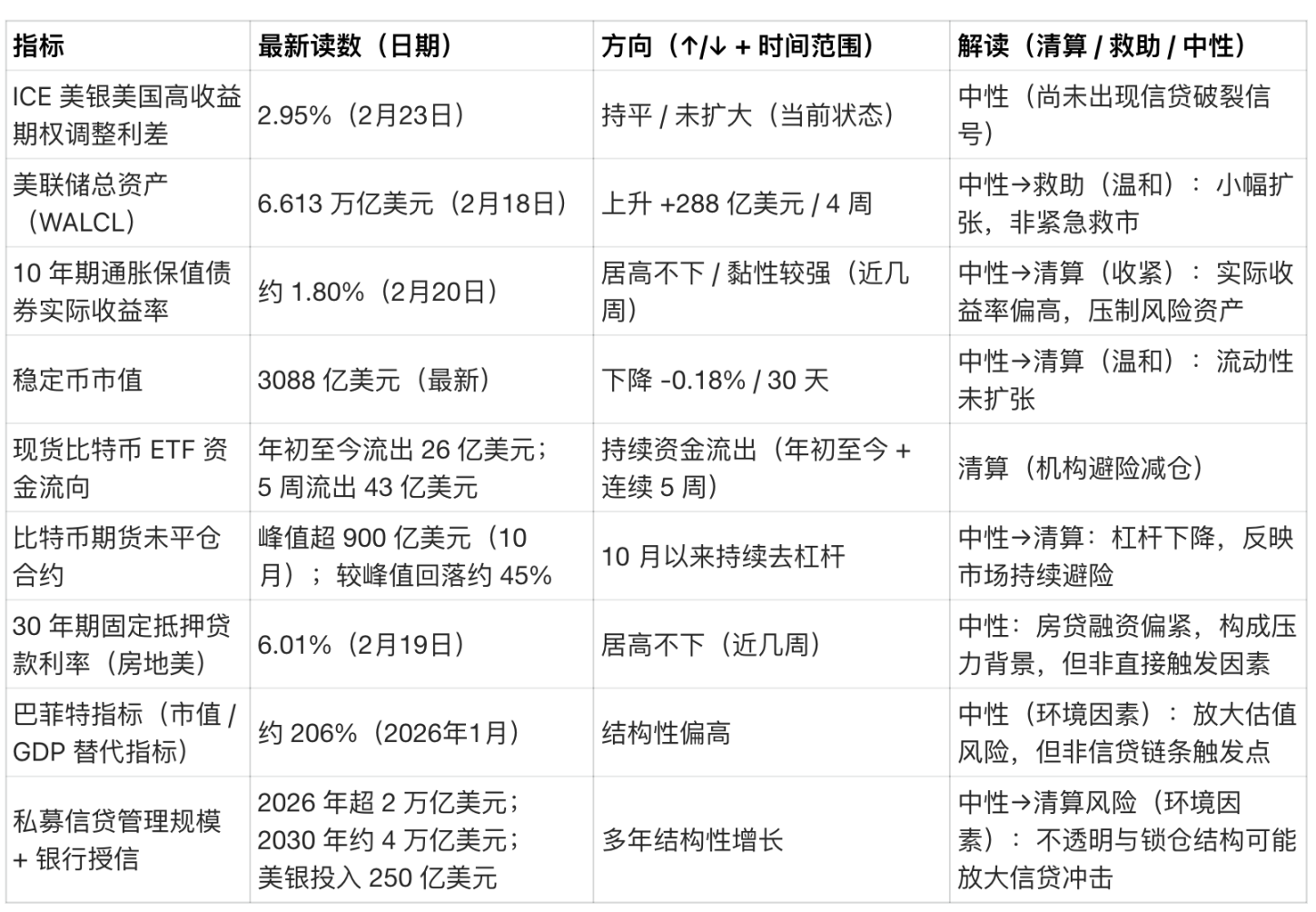

On February 23, the US Bank High Yield Option-Adjusted Spread was 2.95%, still tight compared to crisis periods.

On February 18, the Federal Reserve's balance sheet stood at $6.613 trillion, having expanded by approximately $28.8 billion over four weeks—a moderate expansion, not indicative of emergency liquidity.

On February 20, the 10-year Treasury Inflation-Protected Securities (TIPS) real yield was around 1.80%, a level sufficient to pressure yield-less assets.

The stablecoin market cap is approximately $308.8 billion, with a 30-day change of -0.18%, essentially flat.

Since early 2026, Bitcoin spot ETFs have seen a combined net outflow of approximately $2.6 billion, with outflows of about $4.3 billion over the past five weeks.

Bitcoin Drops First, Reasons Discussed Later

Deflationary liquidations often begin in credit markets, not stock indices.

High-yield bond spreads widen sharply, funding markets come under pressure, volatility spikes—cash becomes the only position everyone wants.

Bitcoin's behavior in such a phase is predictable: perpetual funding rates turn negative, leverage unwinding causes open interest to plummet, liquidity exodus triggers stablecoin supply contraction, and ETF outflows accelerate.

March 2020 serves as a classic reference. During the global liquidity shock, Bitcoin plunged nearly 40% on March 12, sold off alongside stocks, credit, and commodities as market participants scrambled for US dollar liquidity.

A credit-driven liquidation could easily see Bitcoin swing -20% to -40% within days.

Investment firm VanEck noted in early February 2026 that Bitcoin futures open interest peaked above $90 billion in October 2025 and has since shed over 45% of that leverage. If credit stress truly emerges, there is still room for further forced selling.

Rating agency Moody's expects private credit AUM to exceed $2 trillion in 2026 and approach $4 trillion by 2030. According to Reuters, Bank of America has deployed $25 billion into this space.

This growth concentrates credit risk in structures with lower transparency, longer lock-ups, and weaker covenant protections.

Once a credit event triggers forced asset sales in private credit portfolios, the ripple effect impacts public markets through margin calls and collateral pressure. Bitcoin, as the most liquid, 24/7 traded risk asset, disproportionately absorbs the selling pressure.

Bitcoin futures open interest has declined by approximately 45% from its peak of over $90 billion in October 2025 to levels seen in early February 2026, while the Bitcoin price fell from around $68,000 to near $60,000 before rebounding to around $67,000

Bitcoin Will Front-Run Policy Bailouts

The opposite script begins with clear policy support.

Fed balance sheet expansion, emergency tools deployed, real yields falling. Bitcoin's reaction in this environment is equally predictable: funding rates and basis normalize, returning liquidity drives stablecoin supply growth, ETF flows stabilize or turn positive, and open interest re-accumulates.

In a clear bailout environment, Bitcoin often behaves as a high-beta liquidity asset, recovering faster than traditional risk assets because it carries no credit risk and has no potential for earnings shocks. It is a liquidity claim on a fixed-supply monetary asset that benefits when real yields fall.

The March 2023 banking turmoil is the template. As markets anticipated a dovish policy pivot, Bitcoin rose 26% in a week and about 40% in ten days, front-running the Fed's eventual liquidity support.

In February 2026, Bitcoin surged from around $60,000 to over $70,000 in a single day, marking its largest single-day gain since March 2023, highlighting that macro risk sentiment remains the dominant driver during stress windows.

In March 2020, Bitcoin crashed alongside all assets, but the Fed also cut rates to zero within weeks, launched unlimited quantitative easing, and established emergency lending facilities.

Bitcoin recovered from its March 12 low and rose fivefold over the next year as real yields remained deeply negative and fiscal spending expanded massively.

The lesson: Bitcoin's reaction beta to liquidity cycles is almost higher than any other asset; timing matters more than narrative.

A flowchart illustrates Bitcoin's three potential paths under triple bubble pressure: a 20% to 40% sell-off triggered by credit rupture, a high-beta rebound sparked by policy rescue, or price oscillation between safe-haven pressure and monetary debasement narratives in stagflation

When Neither Path Prevails

The most chaotic scenario is: stubborn inflation, bond markets demanding higher term premiums, and persistently high real yields, which limit policymakers' ability to provide swift bailouts without reigniting inflation fears.

In this environment, Bitcoin gets stuck in a range. Safe-haven pressure and debasement hedge narratives pull against each other. Rallies fade when real yields stay high or policy support falls short of expectations.

The 10-year TIPS yield at 1.80% is far above the zero or negative real yields seen during Bitcoin's strongest rallies.

The Freddie Mac 30-year fixed mortgage rate averaged 6.01% on February 19.

The Buffett Indicator (Total Market Cap / GDP) is approximately 206%, which, according to Advisor Perspectives data, is at the highest level in the indicator's history. This suggests little room for further equity valuation expansion unless earnings grow or discount rates fall.

If credit stress arrives but policy does not pivot quickly, Bitcoin gets stuck in a choppy pattern—neither being liquidated nor bailed out.

A Framework for Tracking Market Shifts

A simple tracking framework updates four indicators weekly:

- Change in the Fed's total assets over 4–8 weeks;

- 30-day change in stablecoin market cap;

- 2–4 week change in high-yield bond spreads;

- 2–4 week change in the 10-year real yield.

When indicators deteriorate sharply, Bitcoin tends to swing like a high-beta asset in liquidity events;

When indicators improve and reflation expectations rise, Bitcoin tends to outperform.

Current readings suggest a neutral-to-negative liquidity environment.

- Fed balance sheet expanding slightly but not flooding;

- Stablecoin supply flat or slightly down;

- Credit spreads still tight;

- Real yields high and sticky;

- Bitcoin spot ETFs seeing persistent outflows;

- Derivatives open interest nearly halved from its peak.

The market setup feels like it's waiting for a catalyst: either credit stress triggering a liquidation or policy support restarting the liquidity trade.

Signals Appear in the Credit Chain

An actionable monitoring framework focuses on the credit and crypto plumbing:

- High-yield bond spreads rising from lows → Credit market confidence waning;

- US Treasury volatility and term premiums rising → Bond markets pricing in policy constraints;

- Fed balance sheet flat/declining while spreads widen → Confirming no backstop.

Crypto-side signals:

- Open interest dropping sharply → Forced selling;

- Stablecoin market cap contracting → Liquidity exiting;

- ETFs seeing persistent outflows → Institutional de-risking.

Bailout confirmation signals:

- Fed total assets rising noticeably on a weekly basis → Active liquidity provision;

- 10-year TIPS yield falling → Real yields declining;

- Stablecoin supply growth + normalized derivatives funding rates → Crypto liquidity returning.

The shift from liquidation to bailout is often swift. March 2020 is the example: Bitcoin crashed and then rebounded within weeks as policy support landed.

The greatest value of the triple bubble theory is not predicting a crisis, but providing a sequential framework.

Credit rupture triggers liquidation, Bitcoin gets sold cheaply;

Policy bailout brings a liquidity explosion, Bitcoin front-runs traditional assets.

The current macro setup—overvalued assets, high real yields, tight credit spreads, flat stablecoin supply, persistent ETF outflows—suggests the market has priced in stress but has not yet seen a credit chain breakdown forcing a sell-off.

Bitcoin's next major move depends not on whether bubbles exist, but on whether credit cracks first or the Fed bails out first.