LBank Labs: A Panoramic Outlook for the Crypto Industry in 2026

- 核心观点:2026年加密行业将完成结构性重塑,走向成熟与合规。

- 关键要素:

- 高利率环境推动DeFi转向创造真实收益。

- 稳定币成为美元全球输出的战略性金融工具。

- AI Agent与机器人经济实现规模化落地。

- 市场影响:加速行业机构化,模糊传统金融与加密金融边界。

- 时效性标注:中期影响。

introduction

In 2025, the crypto industry will truly mature. Driven by favorable macroeconomic factors, Bitcoin will rise to become a global macro asset, and the crypto market will officially step onto the world stage. Maturity comes with pressure—unprecedented liquidation volumes, pressure on liquidity market makers, and increasing regulatory fragmentation. However, amidst market volatility, the crypto industry is undergoing a profound architectural reshaping: decentralized autonomous technologies (DATs), large-scale on-chain real-world assets (RWAs), intent-centric infrastructure, and a continuously maturing stablecoin system are constantly expanding the boundaries of the crypto economy.

LBank Labs, in partnership with CoinGecko and CoinGape, released the "2026 Crypto Industry Panorama Outlook," providing institutional and professional investors with forward-looking insights and analyzing the key drivers of the next cycle. This report systematically outlines the most influential investment themes of 2026, including evolving macroeconomic trends, next-generation DeFi, stablecoin convergence, prediction markets, and the tokenization of the real-world economy. The synthetic economy is no longer just a future vision, but is being gradually built on top of the blockchain. 2026 will truly reveal who is shaping this new landscape.

Macro Markets and Regulation: Structural Restructuring in the Post-Collapse Era

The market in 2026 operated within a structural environment defined by both "prolonged high interest rates" and a post-crash clearing. With the Federal Reserve maintaining the benchmark interest rate in the 3.00%–3.25% range, a key 3% "risk-free rate" threshold was established for all digital assets. This interest rate level required decentralized finance (DeFi) protocols to create real and sustainable utility and returns, pushing the entire ecosystem away from inflationary token economic models. This high-interest-rate environment contrasted sharply with the European Central Bank's dovish rate-cutting policy, spurring significant carry trade inflows into dollar-denominated stablecoins, further solidifying the dollar's dominance in the crypto economy. Simultaneously, the market structure was fundamentally reset by the "flash crash" that occurred on October 10, 2025. This geopolitically triggered $19 billion liquidation event quickly cleared the market of remaining high-risk speculative leverage, laying the foundation for a subsequent recovery led by well-capitalized institutions and robust protocols focused on real-world applications.

Currently, the global regulatory landscape has clearly diverged into two distinct economic systems. One is the "regulated system," encompassing institutions and projects operating under the US GENIUS Act (National Innovation Act for Stablecoins) and the European MiCA framework. The GENIUS Act is crucial, defining stablecoins as a strategic tool for maintaining the US dollar's status as the global reserve currency and mandating that issuers hold 100% non-collateralizable reserve assets. While this system significantly enhances security, it also raises "return issues" for issuers, thereby driving a sustained increase in market demand for innovative secondary PayFi protocols.

At the other end is the "sovereign market," primarily dominated by highly vertically integrated platforms operating entirely outside the direct regulatory purview of the Federal Reserve. As regulatory paces converge across major Asian markets, this clear structural divergence indicates that the crypto industry is irreversibly moving towards a new global phase driven by institutionalization, compliance, and practical application value.

DeFi Sector: Innovation Evolution and the "Post-AMM Era"

In 2026, the DeFi ecosystem is gradually moving away from its speculative early stages, with Real-World Assets (RWAs) becoming the core source of on-chain returns. The RWA supercycle is not driven by retail investors, but rather stems from institutional-level "financial physics" following the end of the Zero Interest Rate Era (ZIRP). Through legally structured Special Purpose Vehicles (SPVs), tokenized bonds and US Treasury bonds are systematically introduced on-chain, providing the market with predictable and sustainable on-chain returns.

This deep integration significantly improves the efficiency of financial infrastructure, shortening the traditional bond settlement cycle from T+2 to less than 10 minutes, making on-chain execution an essential efficiency requirement that large banks cannot ignore. At the same time, dynamic DeFi protocols are rapidly merging with Web2 digital banks. More and more fintech companies are routing back-end yields to compliant DeFi liquidity pools, providing retail users with high-yield savings products through "invisible DeFi."

This trend is blurring the lines between non-custodial wallets and traditional bank accounts, sparking fierce competition over user entry points and interfaces. DeFi is no longer present in an explicit form, but rather embedded in the mainstream financial system as infrastructure.

This structural shift is accompanied by a technological revolution centered on specialization and performance. The era of general-purpose Layer-1 blockchains has ended, replaced by specialized blockchains built around deep performance optimization and tailored to specific application scenarios. Hyperliquid is a prime example of this trend, successfully bridging the long-standing performance gap between centralized exchanges (CEXs) and decentralized exchanges (DEXs) by completely migrating its order book on-chain. Hyperliquid adopts an "Apple-like" vertical integration path, simultaneously building the blockchain itself, the exchange system, and token standards, thereby eliminating dependence on external ecosystems and directly challenging traditional centralized exchanges in terms of pure performance. With a final confirmation time of 0.2 seconds, it achieves transaction speed and execution efficiency approaching that of centralized systems. While RWA introduces traditional financial returns on-chain, Ethena has successfully expanded crypto-native returns into "internet bonds." Its Delta-neutral strategy—long staking of ETH while simultaneously shorting perpetual contracts—stabilizes the return structure while circumventing the GENIUS Act's stablecoin reserve requirements. Currently, this mechanism has generated a floating annualized yield of approximately 8%–12%. This "internet bond" is becoming an independent risk-free yield benchmark within the crypto ecosystem, serving as a native crypto reference rate distinct from the federal funds rate, and is gradually evolving into the default "current account" for institutional funds in the DeFi ecosystem.

Stablecoin Sector: A Diverging Development Path

By 2026, stablecoins had clearly completed their transformation from a medium of exchange to a systemic settlement layer on the internet, with transaction volume comparable to that of global bank card networks. This maturation fundamentally stems from the "sponge effect" of the GENIUS Act. This act requires regulated stablecoin issuers to use short-term U.S. Treasury bonds as reserve assets, formally integrating stablecoins into the global dollar export system at the institutional level, and generating a price-insensitive structural demand of up to $150 billion at the short end of the U.S. yield curve. In a multipolar global landscape, stablecoins have thus evolved into a strategic financial tool serving U.S. debt financing.

The core contradiction in this system lies in the "yield issue." Because the GENIUS Act prohibits regulated stablecoin issuers (such as USDC) from paying interest to holders, the market structurally separates the "monetary attribute" (the stablecoin itself) from the "source of yield" (DeFi protocols). This separation has given rise to "PayFi" (payment finance) applications, where users deposit zero-interest stablecoins into various protocols to earn yields in other on-chain scenarios. As a result, funds are continuously flowing from the traditional banking system to crypto-financial infrastructure, which offers 24/7 availability and higher capital efficiency.

The current market presents three distinct issuer strategies, with clear winners emerging at the payment channel level. Tether (USDT) is no longer limited to stablecoin issuance but is leveraging its massive float to transform into a diversified alternative asset management platform, investing over $5 billion in AI computing power and commodity trade financing, thereby significantly reducing its reliance on the US banking system. In contrast, Circle (USDC) has chosen to fully embrace the banking system, promoting deep compliance and integration with traditional finance.

Meanwhile, regulated markets are facing challenges from non-USD stablecoins. For example, Euro stablecoins compliant with MiCA requirements (such as EURC) are gradually gaining adoption in Europe due to a wave of delistings. In emerging markets, the trend of "crypto-dollarization" continues to accelerate. At the same time, the PayFi technology stack, represented by PYUSD issued by PayPal on Solana, has established a clear advantage in the fields of micro-payments and cross-border remittances thanks to its tiered transaction fees and confidential transfer protocols geared towards B2B scenarios.

Against the backdrop of significant differentiation within the stablecoin system, emerging issuers are accelerating productization and scaling through collaborations with leading exchanges, with World Liberty Financial (WLFI) being a prime example. In August 2025, LBank, as one of the first centralized exchanges (CEXs) to partner with WLFI, launched its USD-pegged stablecoin USD1 and simultaneously introduced a points-based loyalty system based on USD1. Users can accumulate points and earn additional rewards through USD1 spot trading, holding, and staking. These points can be used within the WLFI ecosystem for reward redemption and governance token airdrops, thus transforming stablecoin usage into long-term participation incentives. Simultaneously, LBank further launched USD1 investment products, allowing users to connect USD1 to DeFi protocols for higher yields, effectively alleviating the structural pain point of "stablecoins not generating interest" within a compliant framework. Through the triple linkage of trading, incentives, and returns, this collaboration not only significantly improves the global circulation efficiency of USD1 but also provides retail users with a clear path to smoothly transition from payment-type stablecoins to yield-generating PayFi assets.

Ultimately, regulatory arbitrage regarding the "yield issue" has been resolved through two clear paths: first, a permissioned system for institutions, and tokenized government bond products that generate returns (such as the BlackRock model); second, encapsulated tokens for retail users, i.e., building yield-generating derivative versions on top of stablecoins. As a result, simply holding native stablecoins that do not generate interest is gradually losing its appeal to end users.

The Rise of PayFi in the Payment Sector

PayFi has become the most representative growth sector in 2026, demonstrating the deep integration of payment mechanisms and DeFi's time value capabilities, creating entirely new financial products that are difficult to achieve in the traditional financial system. In essence, PayFi is the practical application of "programmable money," automating the management of the timing and triggering conditions of fund flows through smart contracts.

In B2B scenarios, PayFi's most influential applications include invoice factoring and supply chain finance. Liquidity pools can provide enterprises with real-time advances of stablecoin funds based on tokenized invoices, thereby releasing working capital that was previously locked up with a 60-90 day payment cycle, directly introducing the "time value of money" into the on-chain system. Meanwhile, streaming payroll is gradually replacing the traditional payday model, enabling payments to employees on a second-by-second basis, significantly improving the efficiency of capital turnover and the velocity of money circulation.

In the evolution of new banking systems, the DeFi-as-a-Service (DaaS) model is playing a crucial role. New crypto-friendly digital banks (such as Revolut, Juno, and Xapo) are no longer just payment gateways, but are gradually evolving into full-stack DeFi service providers. By 2026, these institutions will act as trusted "curators" by abstracting wallet management and gas fees, directly integrating back-end lending protocols like Morpho and Aave into their user interfaces.

Under this architecture, the new type of bank can provide users with "disposable yield-generating accounts," meaning that users' idle funds are automatically routed to low-risk, over-collateralized DeFi vaults to earn institutional-grade yields (approximately 4%–5% annualized), while still allowing for instant spending via debit card. In this model, the new bank acts as a distribution layer for DeFi protocols, achieving inclusive access to global on-chain yields while retaining the familiar user experience of traditional banking applications.

The adoption logic by merchants and enterprises is entirely driven by economic efficiency, namely cost and speed. In the cross-border B2B payment sector, stablecoins have gradually become the default settlement channel, completing clearing within seconds at a fraction of the cost of traditional systems, thus bypassing the high fees and long delays of the SWIFT network. Merchant access is virtually frictionless, with professional service providers handling stablecoin processing and settling fiat currency into the merchant's bank account, making the blockchain payment channel virtually "invisible" to the merchant. This overwhelming efficiency advantage is forcing traditional banks to integrate stablecoin channels into their corporate financial services systems. Furthermore, multinational corporations are accelerating the adoption of on-chain cash management solutions, using stablecoins to achieve 24/7 instant liquidity transfers between their global subsidiaries, fundamentally eliminating the long-standing "cash stagnation" problem in the traditional banking system.

Predicting Market Tracks: The Formation of Corporate Hedging Layers

By 2026, the prediction market industry had completed its transformation from an unregulated "flash casino" to an event-driven contract version of the "New York Stock Exchange." The key turning point came from the re-entry of the US market: platforms such as Polymarket received non-action letters from the US Commodity Futures Trading Commission (CFTC) and acquired licensed exchanges; at the same time, Kalshi had integrated with mainstream brokerage platforms such as Robinhood, enabling event contracts to directly reach more than 25 million retail user accounts.

While political events still drive trading volumes in certain cycles, the real growth engine has shifted to high-frequency, sustainable sources of liquidity. Sports betting has become a new core driver of trading volume, while the rise of corporate earnings derivatives has made prediction markets a daily tool for fundamental investors for the first time. Traders can now position themselves long or short based on whether a company exceeds its earnings per share expectations by $0.03, transforming prediction markets from event-driven products into high-frequency financial instruments.

On the technological front, prediction market infrastructure is rapidly evolving towards higher performance and automation. The rising demand for settlements within 15 minutes for assets like BTC and ETH is sparking an "oracle race," with the market increasingly favoring low-latency solutions (such as Chainlink and Pyth) for instant price confirmation, rather than relying on longer-term, but more secure, dispute resolution mechanisms. Against this backdrop, a significant proportion of trading volume is now handled by AI agents and automated trading models, and prediction markets are gradually moving beyond a primarily human-driven trading model.

The competitive landscape has also clearly diverged. One type is the "Las Vegas model," represented by Kalshi, whose core advantages lie in compliance, deep integration with the fiat currency system, and providing deposit interest-bearing services to users through its regulated status. The other type is the "DeFi model," represented by Polymarket, which dominates in terms of pure trading volume by leveraging its native crypto innovation capabilities and highly liquid trending events.

At the same time, new risks are emerging towards 2026, including wash trading, oracle attacks, and ongoing regulatory friction stemming from the fragmentation of state and regional laws. These factors continue to require platforms to maintain high vigilance in governance mechanisms and technical safeguards to ensure the long-term stable operation of the prediction market while it scales up.

AI Agent Track: The Emergence of the Agentic Economy

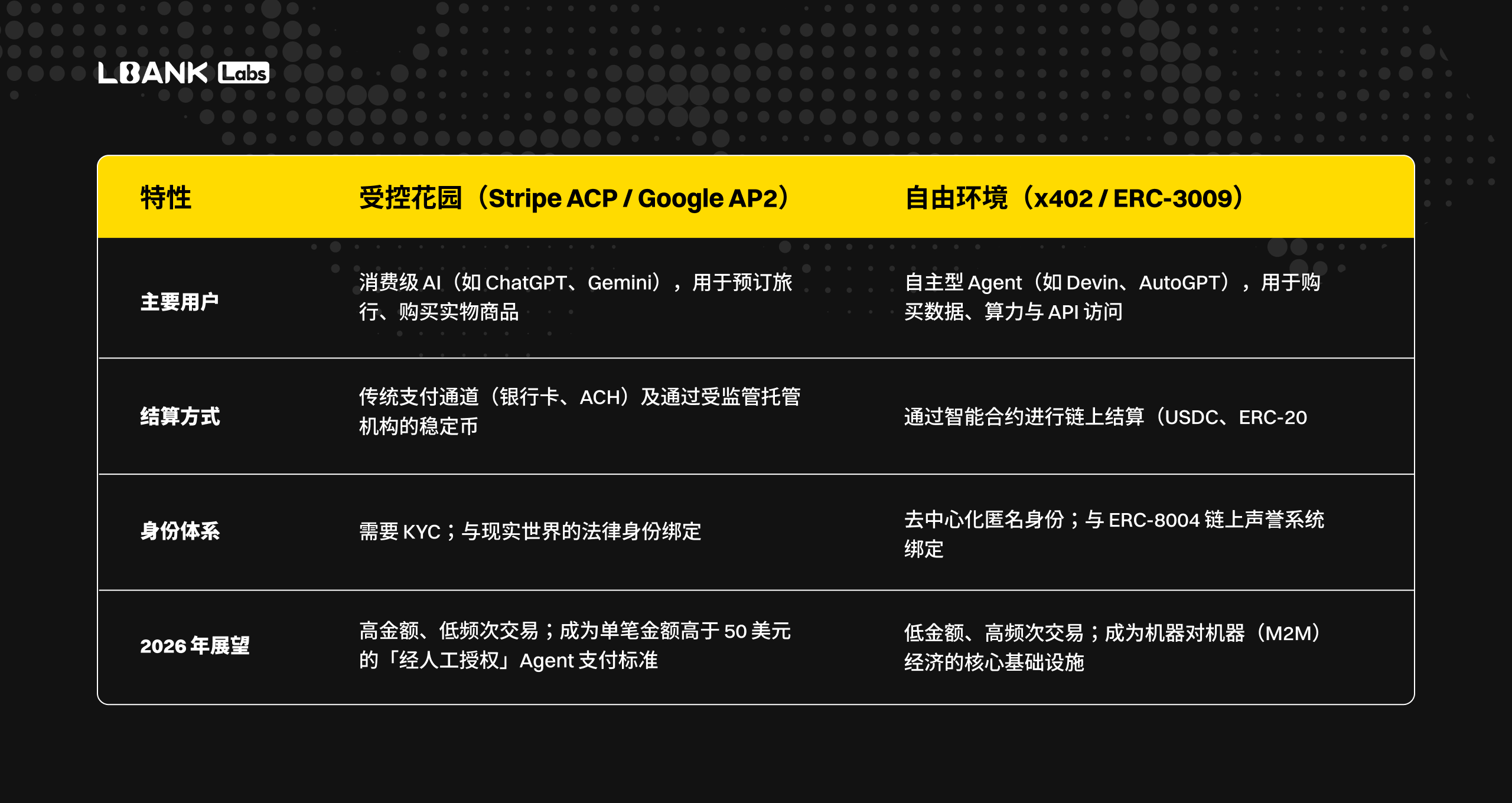

In 2026, the Agent economy achieved its first large-scale deployment. From initial prototype systems with cumbersome pay-per-use experiences, it evolved into production-grade infrastructure driven by delayed settlement and automated trust mechanisms, virtually invisible to users. A key breakthrough came from the potential x402 V2 mechanism: matchmakers could batch aggregate thousands of micro-requests (e.g., $0.001 per token, per API call, or per search result) and settle them through a single on-chain transaction, thereby reducing costs by orders of magnitude and sparking fierce competition among dedicated clearinghouses—some focusing on extreme speed, others prioritizing zero-knowledge privacy.

In this process, LBank took the lead in targeting the AI Agent payment track driven by the x402 protocol and launched several x402 protocol concept tokens, including BNKR (maximum increase of 996%), PING (989%), ZARA (347%), X420 (291%), SANTA (250%), and AURA1 (240%). Through continuous and intensive new product launches and in-depth support, LBank seized the narrative inflection point, becoming the preferred channel for early investors and taking a leading position in the acceleration of the x402 ecosystem. Moreover, LBank launched zkPass and initiated the BoostHub activity, accelerating the formation of real transaction scenarios and on-chain payment needs, and promoting the x402 protocol from proof of concept to high-frequency and sustainable use.

The same technological framework also resolves the long-standing structural conflict between AI labs and content owners. The traditional robots.txt mechanism has gradually become ineffective, replaced by a dynamic "pay-per-crawl" pricing list, enabling AI agents to negotiate the content they need in real time and pay only for the tokens actually consumed. This model fundamentally eliminates the subscription burden for both parties, allowing content acquisition and value exchange to return to a refined, on-demand, and programmable economic logic.

The long-standing bottleneck of trust is being completely resolved through the "reputation as collateral" mechanism. ERC-8004 has evolved from an early draft into a de facto credit scoring system: agents with a good payment history (whose behavior is recorded immutably via x402 logs) can obtain a credit line of Net-30 or Net-60 from the matchmaker, thus eliminating the need for immediate upfront payments for every transaction.

Meanwhile, users only need to grant limited permissions once via an ERC-7710 session key. The entire "protocol mezzanine"—including the ERC-8004-based discovery mechanism, the agent-to-agent negotiation process, and payment settlement via x402—is then hidden behind a single "Agent Authorized" switch. The wallet no longer appears in the user interface; the software automatically and seamlessly pays for the computing power, data, and services required to complete the task.

In this model, the Agent economy is no longer just a demonstration phase, but has officially become the default operating mode. Payment, trust, and execution are integrated into the infrastructure layer capabilities, enabling Agents to operate continuously with minimal user intervention, thus accelerating the large-scale implementation of the decentralized smart economy.

Robotics Track: DePAI and the Machine Economy

By 2026, the integration of cryptography and robotics will evolve from sporadic DePIN experiments into a true machine economy, driven primarily by the widespread adoption of the x402 protocol (HTTP 402 Payment Required). This simple and universal standard enables, for the first time, robots and AI agents to autonomously discover, negotiate, and make payments in the real world, acquiring resources such as electricity, bandwidth, maintenance services, or takeoff and landing permissions in real time through on-chain micro-settlement. Settlement assets are primarily in the form of stablecoins.

Under this system, unmanned delivery drones can automatically recharge at any solar power station, warehouse robots can dynamically lease ground space from competing facilities, and autonomous vehicles can bid for road priority rights in real time, all without the need for manual subscriptions or off-chain billing. The era of closed, isolated robot swarms is coming to an end, replaced by open, freely collaborative hardware networks, where machines themselves act as independent economic entities, autonomously earning and spending.

With the rise of "agent-based commerce," the boundary between software agents and physical robots will become increasingly blurred. AI agents will routinely employ physical hardware to perform real-world tasks and pay robot swarms through smart contract escrow mechanisms—a process that can be coordinated at layers such as Virtual Protocol and OpenMind's FABRIC. Simultaneously, high-value robotic equipment will be tokenized as yield-generating assets. Investors can hold shares in drone delivery networks or cleaning robot swarms in specific cities (such as New York or Singapore) and automatically receive rewards allocated to token holders after settling operating costs via x402.

From an ecological perspective, the machine economy will exhibit a clear division of labor: Base will dominate in terms of agent intelligence and complex collaboration; Solana will handle high-frequency micro-payments involving massive, sub-tiered costs between machines; and Peaq will serve as the authoritative ledger for verifying device identity and physical workload. Together, these three constitute the "nervous system" of the emerging robotic economy, supporting the DePAI-driven machine economy towards large-scale operation.

Jointly issued by:

About CoinGecko

Since its founding in 2014, CoinGecko has been the world's largest independent cryptocurrency data aggregation platform, trusted by millions of users worldwide. CoinGecko provides a 360-degree view of the market, offering reliable data support for over 19,000 cryptocurrencies listed on more than 1,400 exchanges globally. Whether it's price tracking, market trend analysis, or application development, CoinGecko is committed to providing users with insights that accelerate their decision-making and exploration in the crypto market.

About CoinGape

CoinGape is a leading independent cryptocurrency news and content platform founded and operated by a team of passionate cryptocurrency enthusiasts. The team focuses on in-depth exploration of the blockchain ecosystem and envisions the prosperous future of decentralized finance (DeFi), consistently upholding journalistic professionalism and core media ethics to provide readers with accurate and reliable crypto industry information. For its high level of transparency and integrity in crypto news reporting, CoinGape won the Crypto Media Award at the Global Blockchain Show in 2024 and was the runner-up in the Blockchain Life awards. Market analysis, the latest pre-sale project updates, crypto funding news, podcast content, and other related areas are all core focuses of CoinGape, ensuring that information is accurate, easy to understand, and maintains an objective and neutral stance.