Bitcoin is fluctuating weakly; is a major wave about to hit?

- 核心观点:比特币市场结构脆弱,面临持续抛压。

- 关键要素:

- 长期持有者大量获利了结,实现损失攀升。

- ETF资金持续流出,现货与期货市场流动性低迷。

- 期权市场显示短期下行保护需求增加。

- 市场影响:价格对宏观事件敏感,短期波动风险加剧。

- 时效性标注:短期影响。

Original authors: Chris Beamish, CryptoVizArt, Antoine Colpaert, Glassnode

Original translation by: AididiaoJP, Foresigt News

Bitcoin remains trapped in a fragile range, with unrealized losses increasing, long-term holders selling, and demand continuing to be weak. ETFs and liquidity remain sluggish, the futures market is weak, and options traders are pricing in short-term volatility. The market is currently stable, but confidence remains lacking.

summary

Bitcoin remains in a structurally fragile range, pressured by rising unrealized losses, high realized losses, and significant profit-taking by long-term holders. Nevertheless, demand is anchoring the price above the true market average.

The market's failure to reclaim key thresholds, particularly the cost base for short-term holders, reflects continued selling pressure from recent high-buyers and seasoned holders. A retest of these levels in the near term is possible if sellers show signs of exhaustion.

Off-chain metrics remain weak. ETF inflows are negative, spot liquidity is thin, and futures positions indicate insufficient speculative confidence, making prices more sensitive to macroeconomic catalysts.

The options market exhibited defensive positioning, with traders buying short-term implied volatility (IV) and continuing to demonstrate a demand for downside protection. Volatility surface signals indicated short-term caution, but longer-term sentiment was more balanced.

With the FOMC meeting serving as the last major catalyst of the year, implied volatility is expected to gradually diminish in late December. Market direction will depend on whether liquidity improves and whether sellers will back off, or whether the current time-driven bearish pressure will persist.

On-chain insights

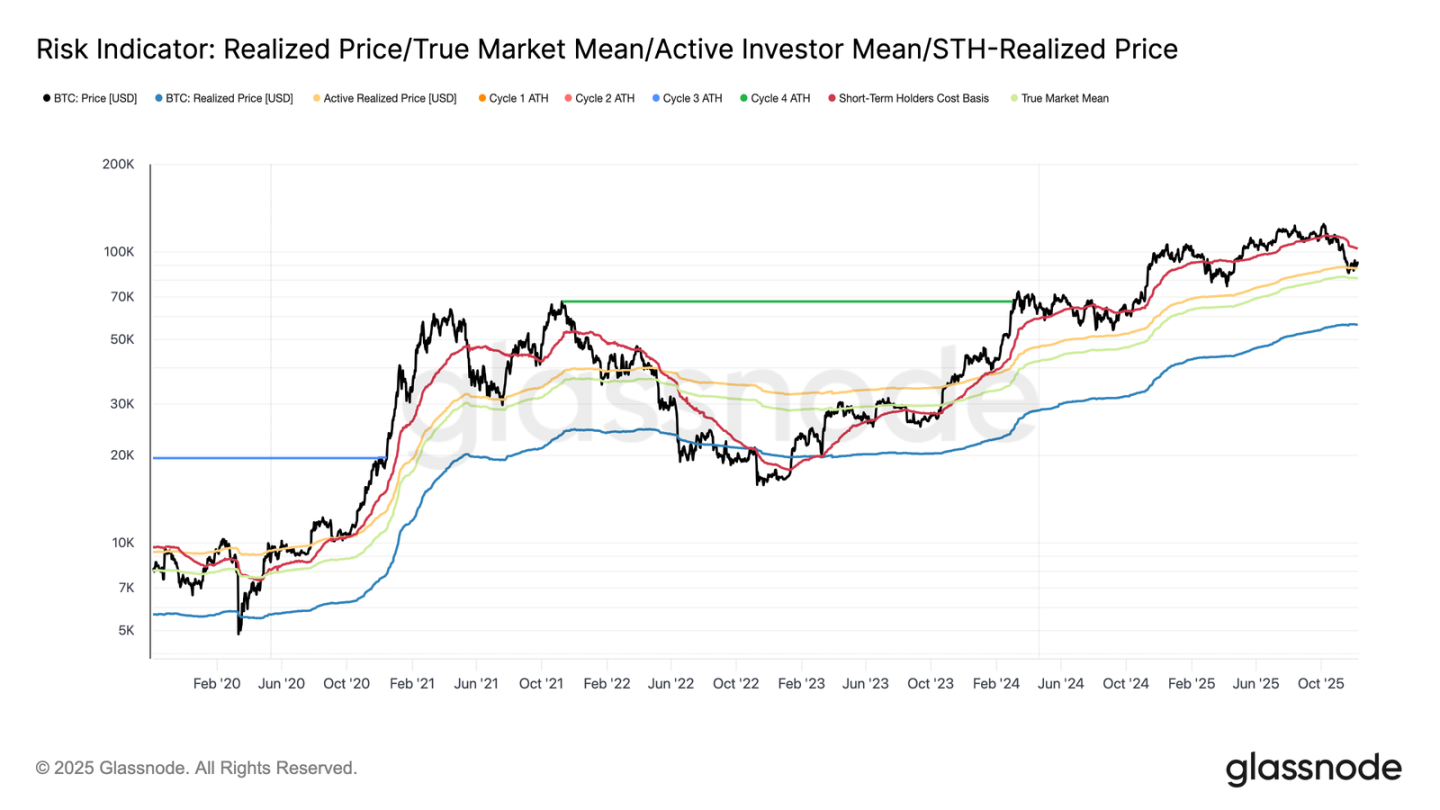

Bitcoin entered the week still confined to a structurally fragile range, with the upper bound at the short-term holder cost base ($102,700) and the lower bound at the real market mean ($81,300). Last week, we highlighted weakening on-chain conditions, thin demand, and a cautious derivatives landscape, all factors that reflect the market landscape at the beginning of 2022.

Although prices are barely holding above the real market mean, unrealized losses continue to widen, realized losses are rising, and long-term investor spending remains high. The key upper limit to reclaim is the 0.75 cost base quantile ($95,000), followed by the short-term holders' cost base. Until then, unless new macroeconomic shocks occur, the real market mean remains the most likely area for a bottom to form.

Time is unfavorable for the bulls.

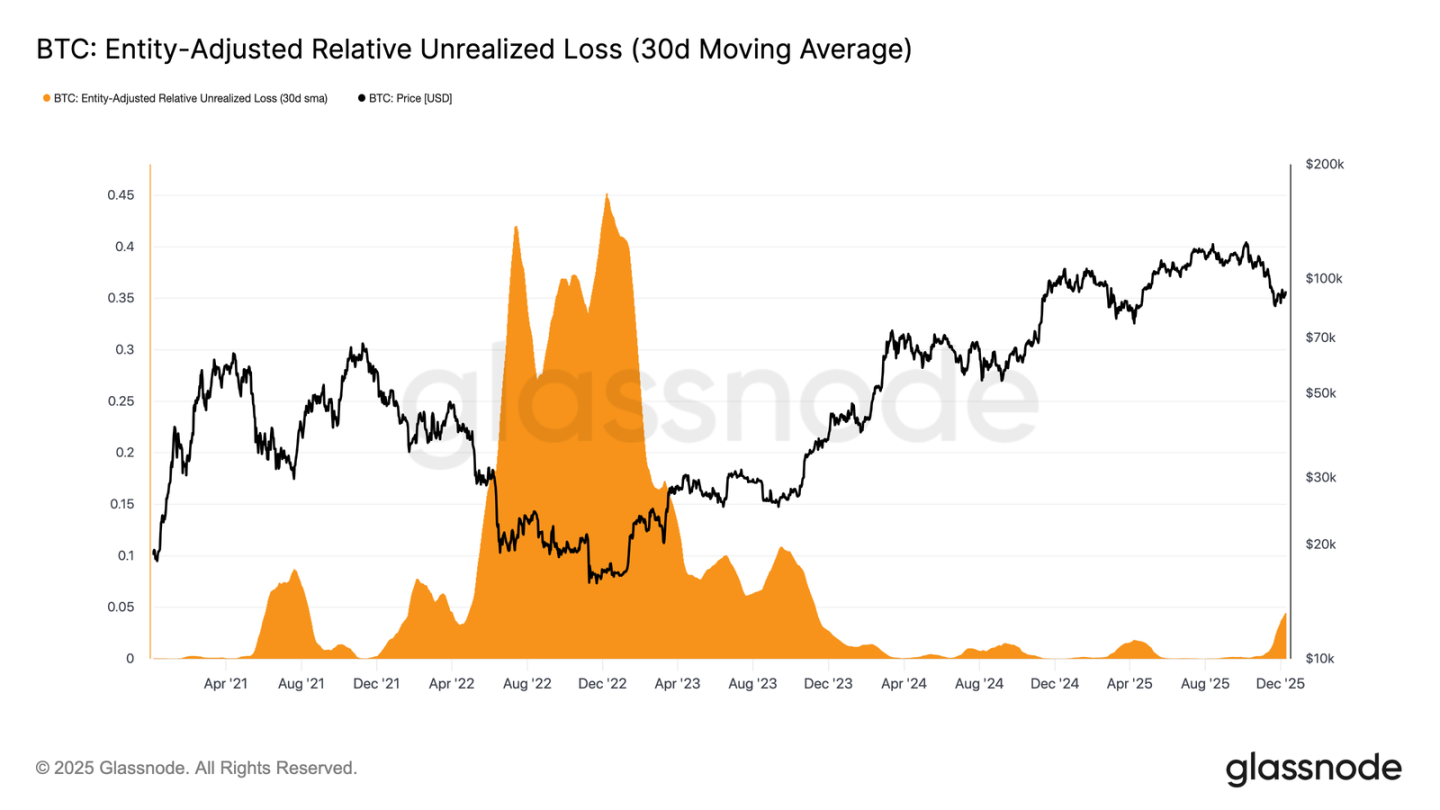

The market remains in a mildly bearish phase, reflecting the tension between moderate capital inflows and continued selling pressure from buyers at higher levels. As the market lingers within a weak but bounded range, time becomes a negative force, making unrealized losses more difficult for investors to bear and increasing the likelihood of realized losses.

The relative unrealized loss (30-day simple moving average) has climbed to 4.4%, after nearly two years remaining below 2%, marking a shift from a frenzied phase to one of increased stress and uncertainty. This indecisiveness currently defines the price range, and resolving this issue requires a new wave of liquidity and demand to rebuild confidence.

Increased losses

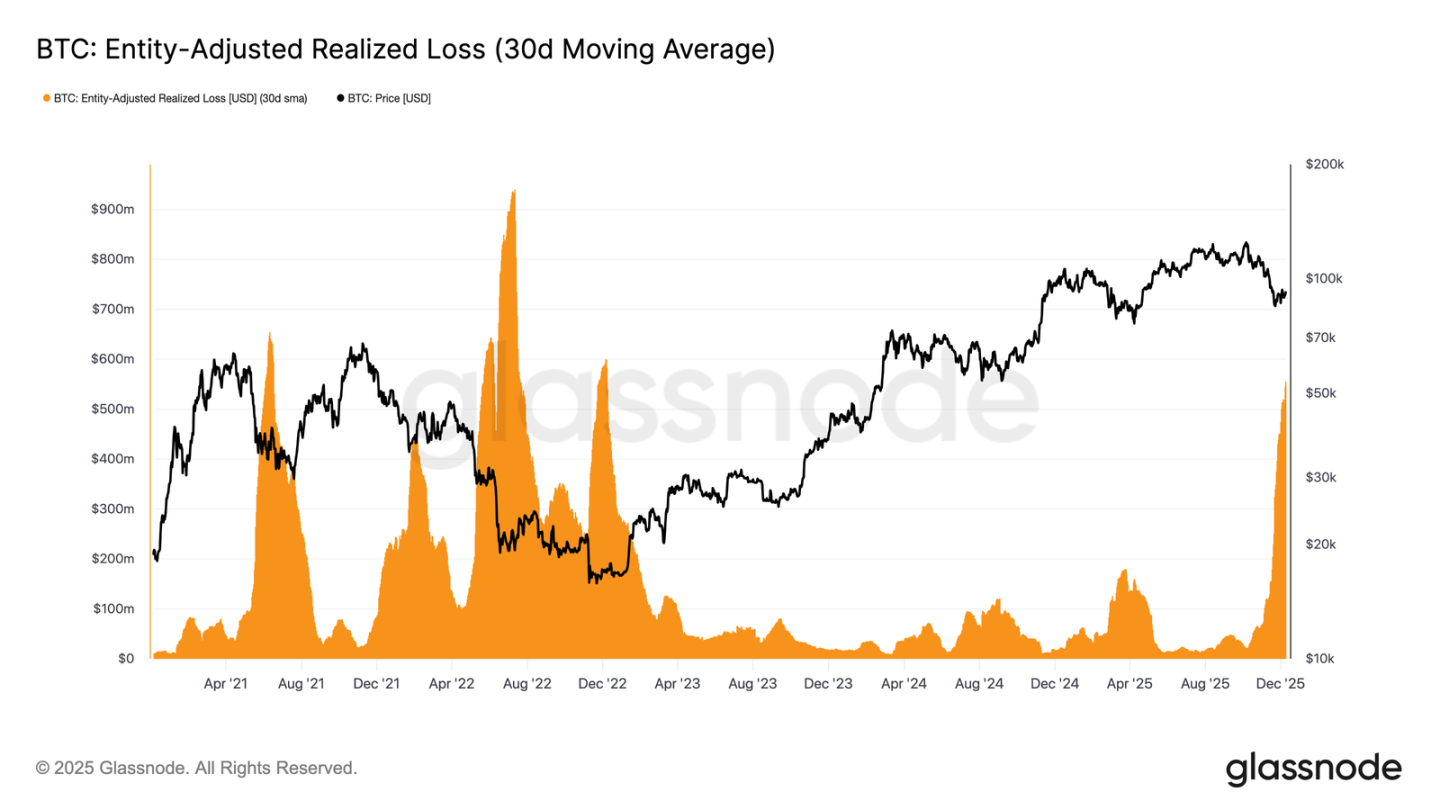

This time-driven pressure is even more pronounced in spending behavior. Although Bitcoin has rebounded from its November 22 low to around $92,700, losses have continued to climb after a 30-day simple moving average correction, reaching $555 million per day, the highest level since the FTX crash.

Such high realized losses during a period of moderate price recovery reflect the growing frustration of those who bought at high levels, choosing to capitulate rather than hold through the rally as the market strengthens.

Obstacles to Reversal

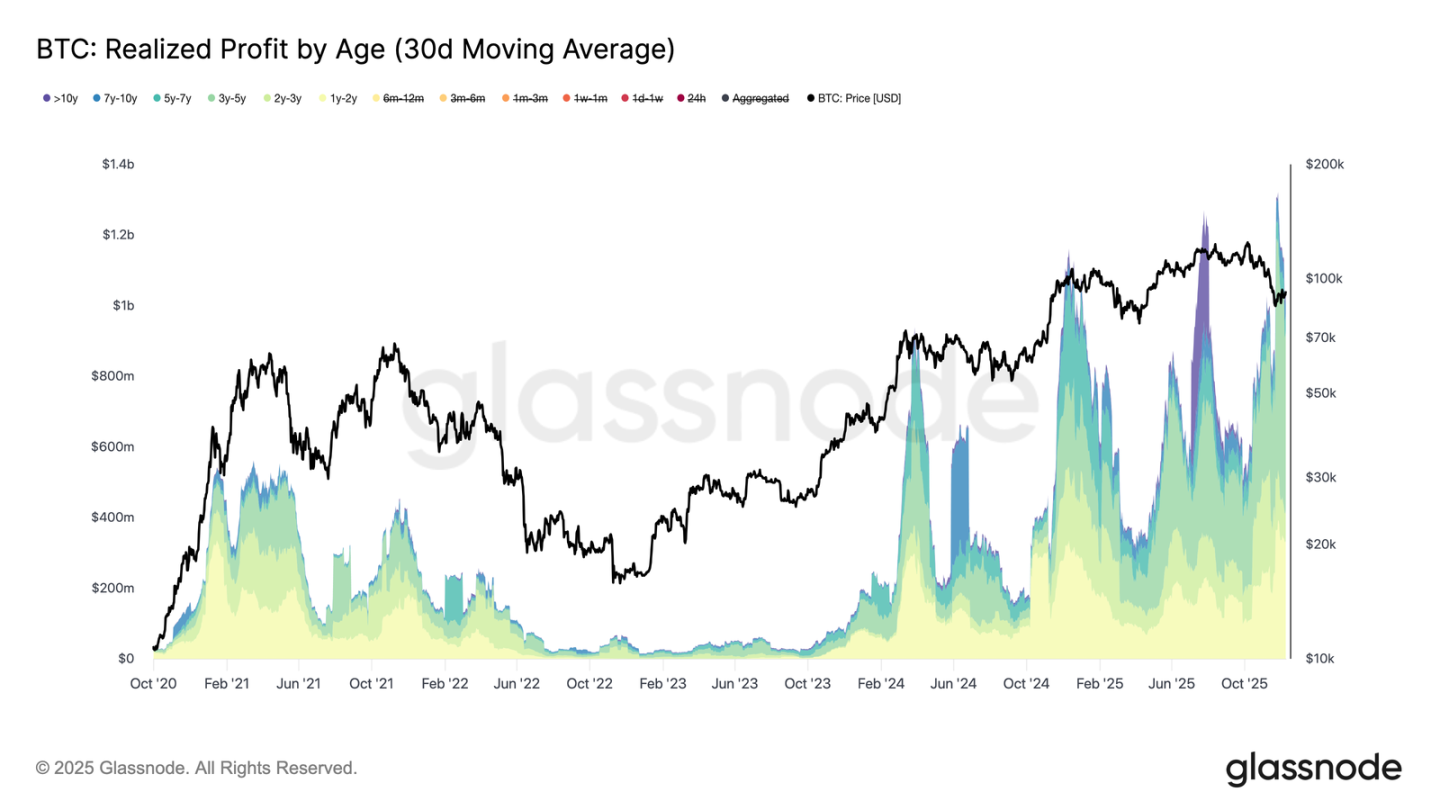

Rising realized losses have further hampered the recovery, especially when they coincide with a surge in realized profits by seasoned investors. In the recent rally, realized profits (the 30-day simple moving average) held for more than a year exceeded $1 billion per day, peaking at a new all-time high of over $1.3 billion. These two forces—capitulation by high-level buyers and substantial profit-taking by long-term holders—explain why the market is still struggling to regain the cost basis for short-term holders.

However, despite such significant selling pressure, prices have stabilized and even slightly recovered above the true market average, indicating that sustained and patient demand is absorbing the sell-off. This potential buying pressure could drive a retest of the 0.75 quantile (approximately $95,000) and even the cost basis for short-term holders if sellers begin to dry up in the short term.

Off-chain insights

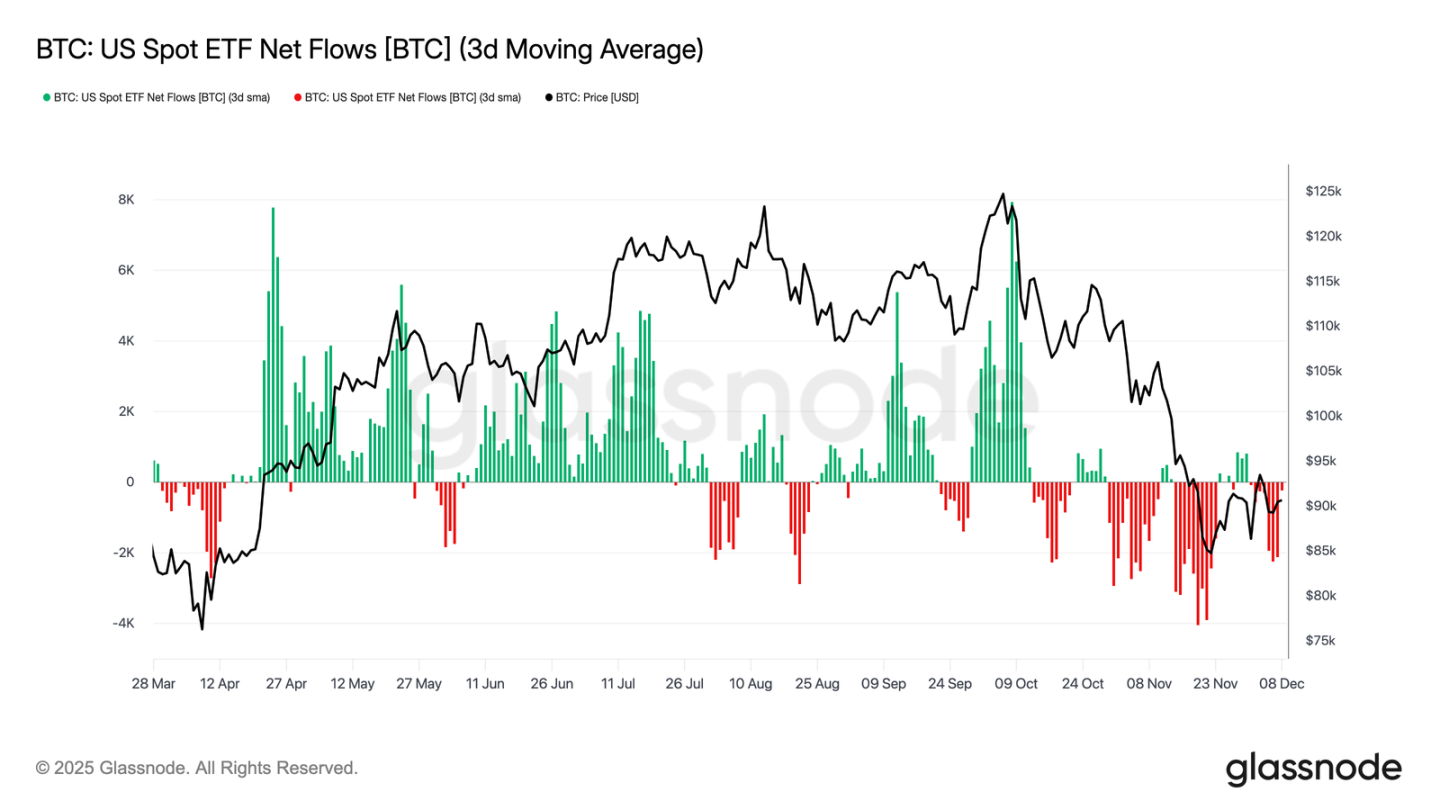

ETF Dilemma

Turning to the spot market, US Bitcoin ETFs experienced another quiet week, with the three-day average net inflow remaining negative. This continues the cooling trend that began in late November, marking a significant departure from the strong inflow mechanism that supported the price rally earlier this year. Redemptions from several major issuers remained stable, highlighting a more risk-averse stance from institutional allocators amid broader market instability.

As a result, the demand buffer in the spot market has thinned, reducing immediate buyer support and making prices more susceptible to macroeconomic catalysts and volatility shocks.

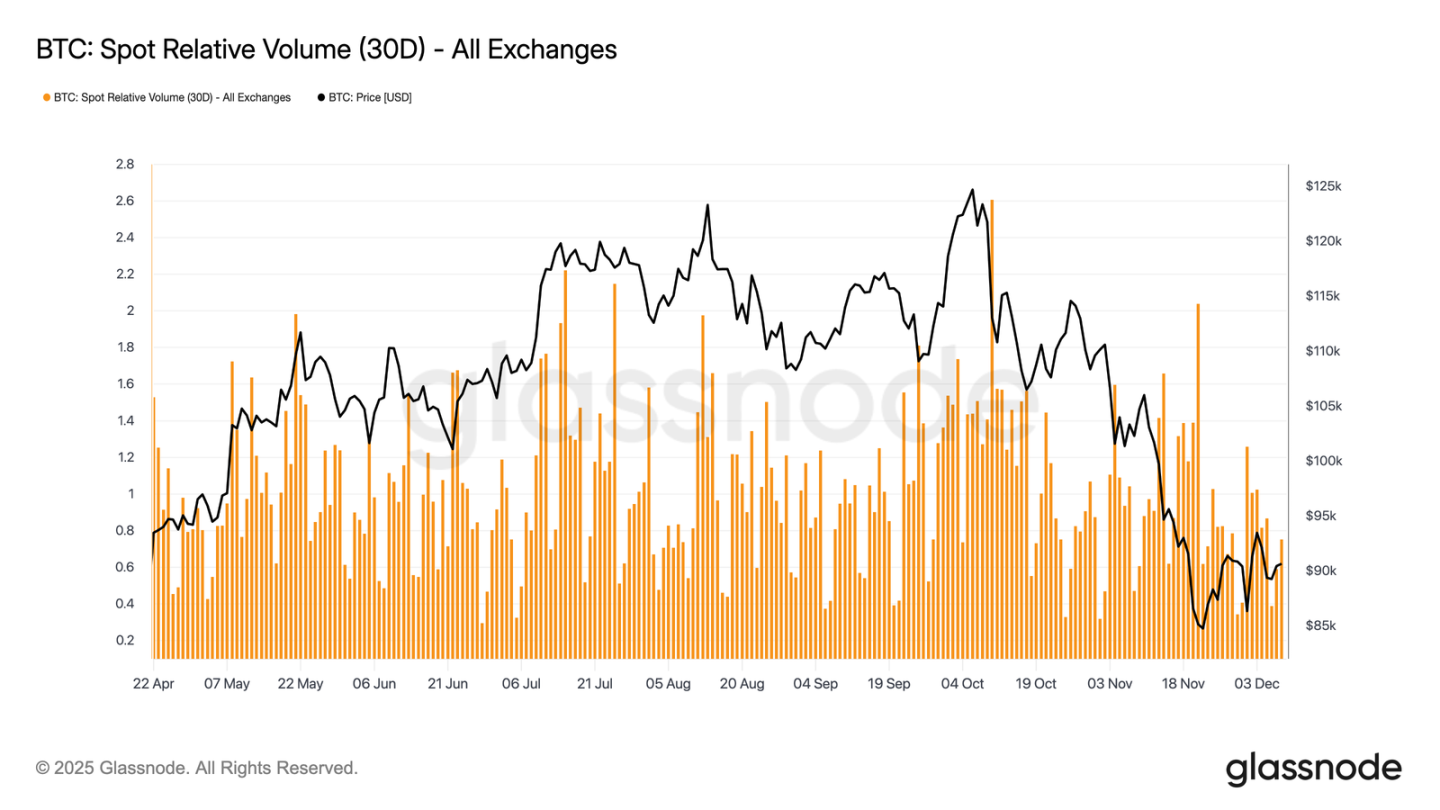

Liquidity remains sluggish

Parallel to the weak ETF inflows, Bitcoin's spot relative volume continues to linger near the lower end of its 30-day range. Trading activity has weakened throughout November and December, reflecting both price declines and decreased market participation. The contraction in volume reflects a more defensive market positioning overall, with fewer liquidity-driven flows available to absorb volatility or maintain directional movement.

With the spot market calming down, attention is now turning to the upcoming FOMC meeting, which, given its policy tone, could be a catalyst for revitalizing market participation.

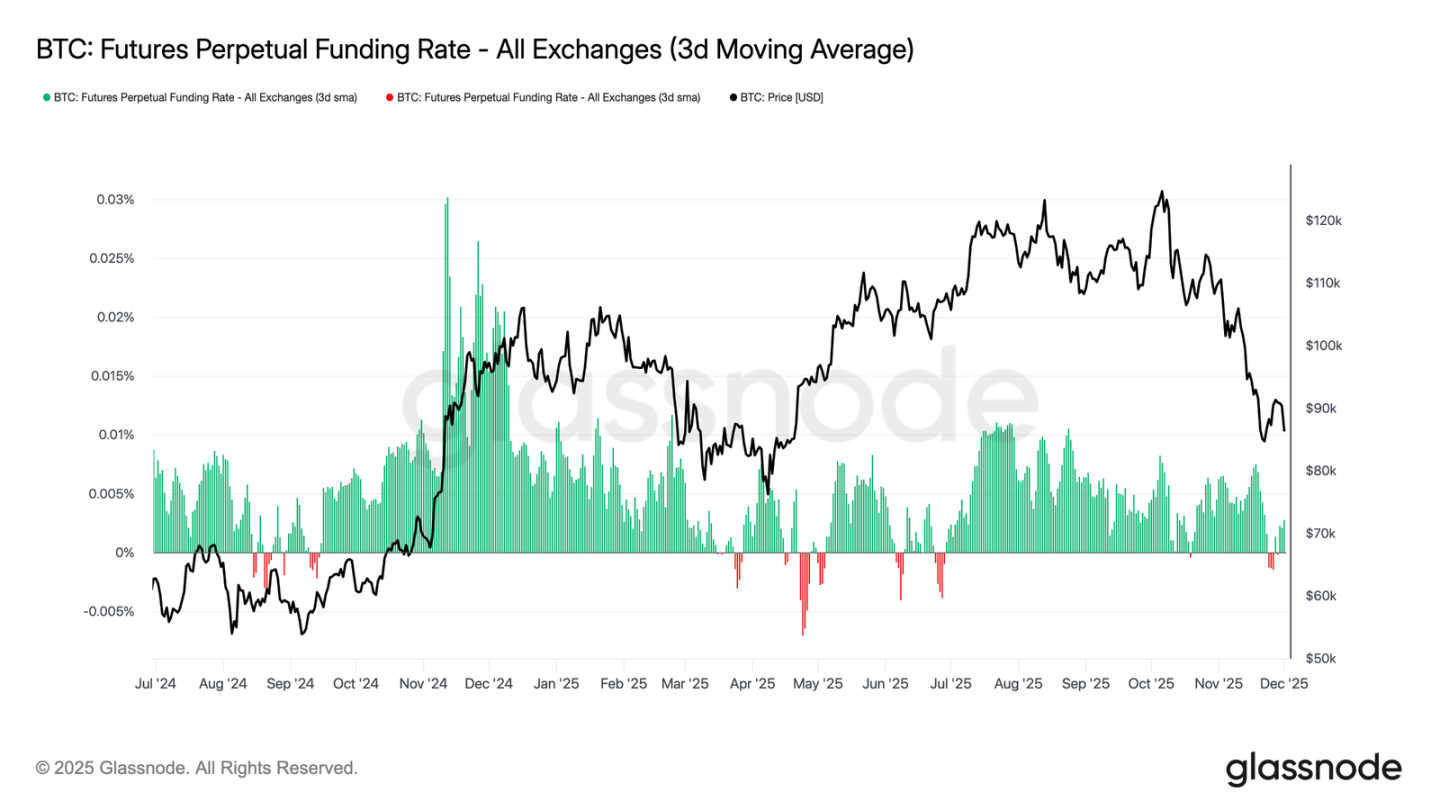

The futures market is sluggish.

Continuing the theme of low market participation, the futures market also showed limited interest in leverage, with open interest failing to substantially rebuild and funding rates remaining near neutral. These dynamics highlight a derivatives environment defined by caution rather than confidence.

In the perpetual futures market, funding rates hovered near zero to slightly negative this week, highlighting the continued withdrawal of speculative long positions. Traders maintained a balanced or defensive stance, exerting little directional pressure through leverage.

Due to sluggish derivatives activity, price discovery is more driven by spot fund flows and macroeconomic catalysts than by speculative expansion.

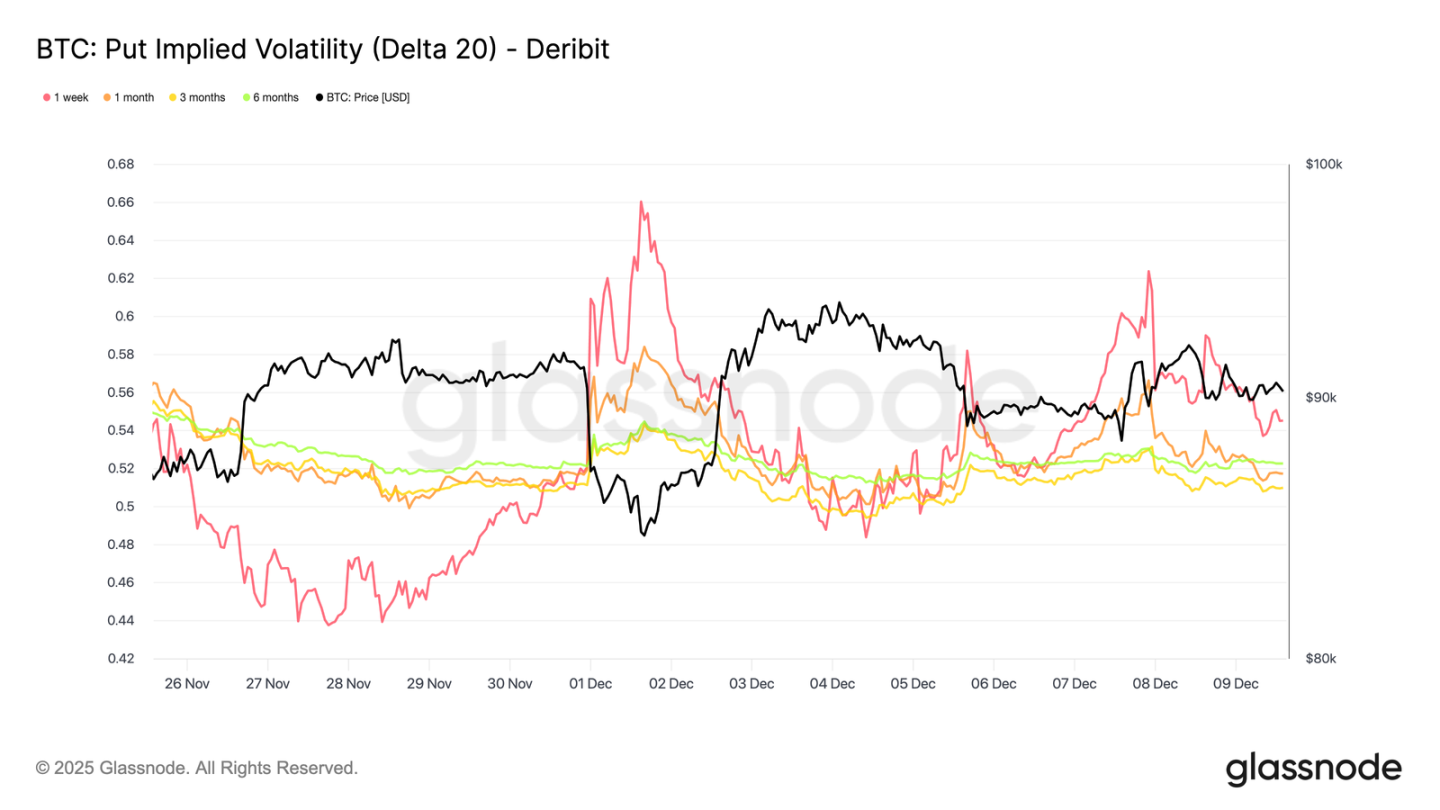

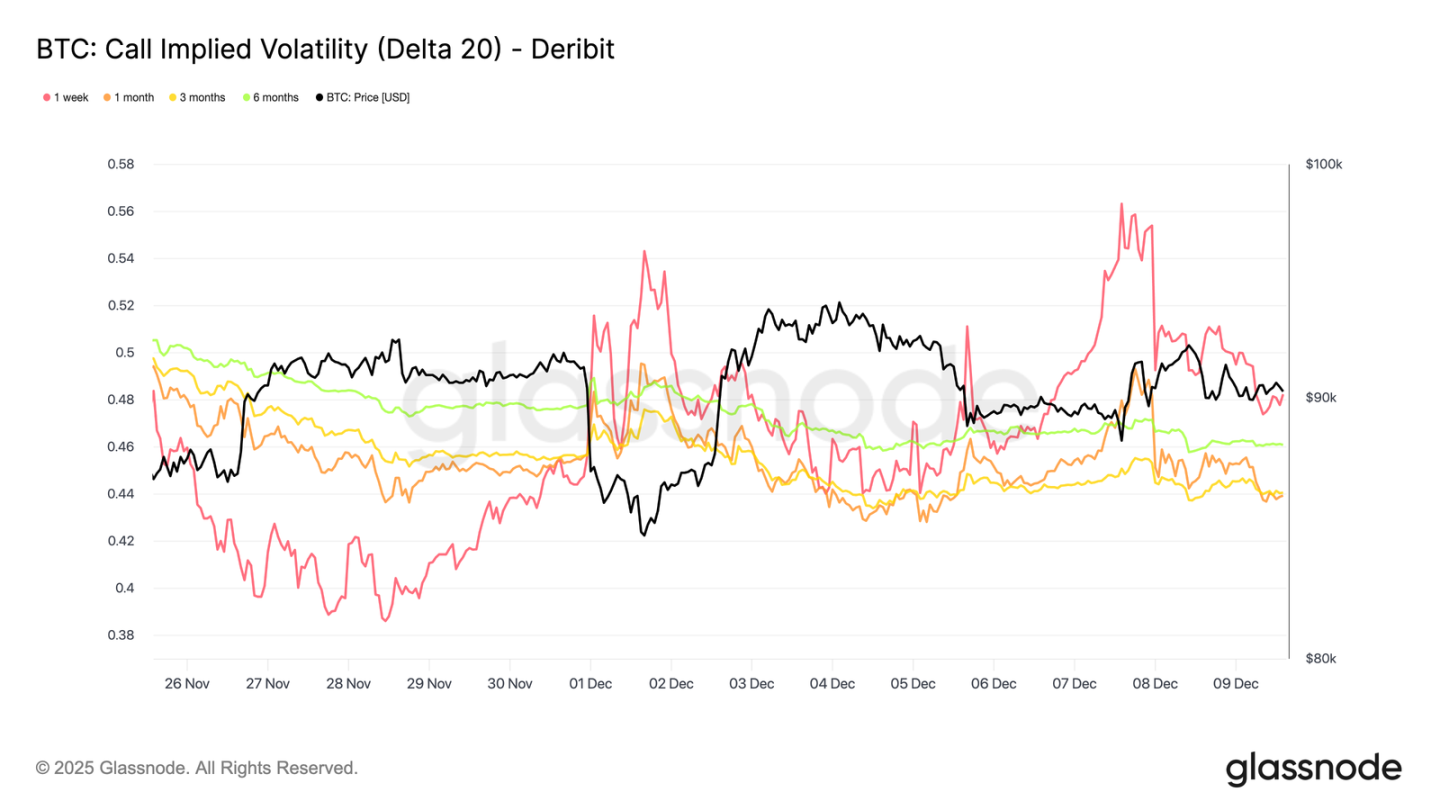

Short-term implied volatility surges

Turning to the options market, the lackluster spot activity for Bitcoin contrasts sharply with the sudden surge in short-term implied volatility, as traders position themselves for larger price movements. Interpolated implied volatility (estimated by fixing the Delta value rather than relying on the listed strike price) reveals more clearly the pricing structure of risk across different maturities.

On 20-Delta call options, the implied volatility (IV) for the one-week term rose by about 10 volatility points compared to the previous week, while longer-term terms remained relatively stable. The same pattern was observed on 20-Delta put options, with short-term downside IV increasing while longer-term terms remained flat.

Overall, traders are accumulating volatility where they anticipate stress, preferring to hold convexity rather than sell ahead of the December 10 FOMC meeting.

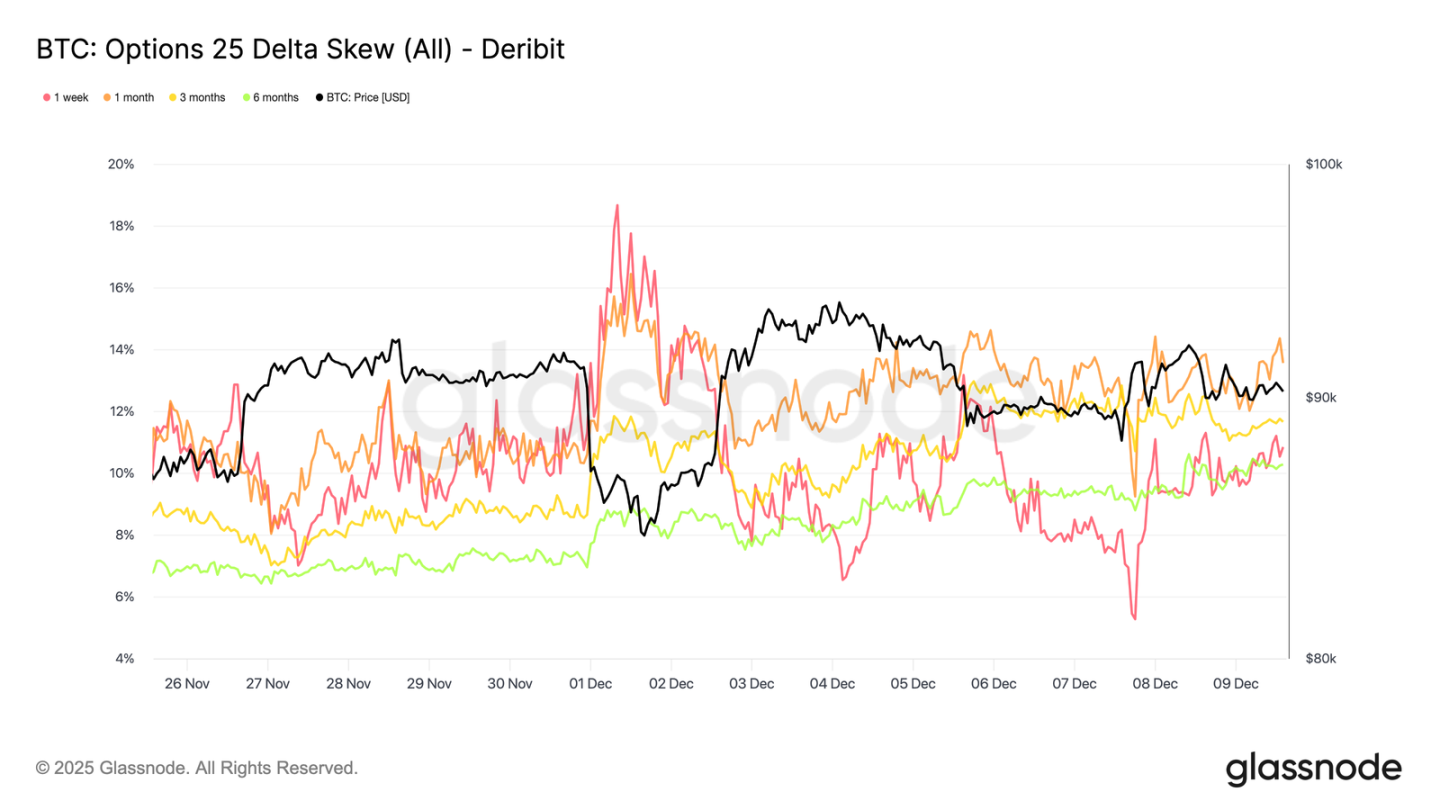

Downward demand returns

Coupled with the rise in short-term volatility, downside protection has once again gained a premium. The 25-delta skewness, which measures the relative cost of put options compared to call options with the same Delta value, has climbed to about 11% over a one-week period, indicating a significant increase in demand for short-term downside insurance ahead of the FOMC meeting.

Skewness remains tightly clustered across all maturities, ranging from 10.3% to 13.6%. This compression suggests that the preference for put protection is across the entire curve, reflecting a consistent risk aversion rather than isolated pressures limited to the short end.

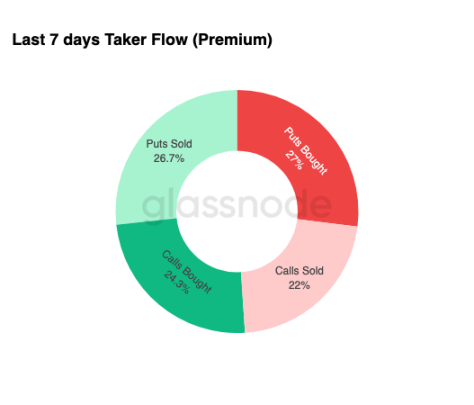

Volatility accumulation

Summarizing the options market situation, weekly fund flow data reinforces a clear pattern: traders are buying volatility, not selling it. Option premiums account for the dominant portion of total notional fund flows, with put options slightly leading. This doesn't reflect a directional bias, but rather a state of volatility accumulation. When traders simultaneously buy options at both ends, this signals hedging and convexity-seeking behavior, rather than sentiment-based speculation.

Combining rising implied volatility with a downward bias, fund flows suggest that market participants are preparing for volatile events, with a downward bias.

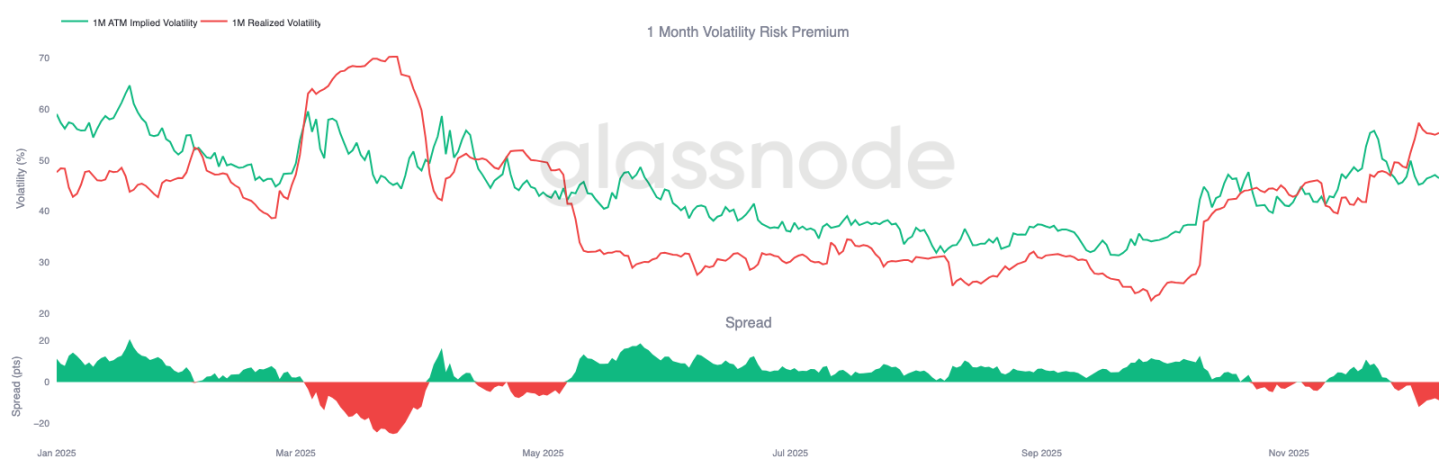

After FOMC

Looking ahead, implied volatility has begun to ease, and historically, once the last major macroeconomic event of the year has passed, implied volatility tends to compress further. With the FOMC meeting on December 10th serving as the last meaningful catalyst, the market is preparing to transition to a low-liquidity, mean-reverting environment.

Following the announcement, sellers typically re-enter the market, accelerating the decay of implied volatility (IV) before the end of the year. Barring any hawkish surprises or significant shifts in guidance, the path of least resistance points to lower implied volatility and a flatter volatility surface, continuing into late December.

in conclusion

Bitcoin continues to trade in a structurally fragile environment, with rising unrealized losses, high realized losses, and significant profit-taking by long-term holders collectively anchoring price movements. Despite persistent selling pressure, demand remains resilient enough to keep prices above the true market average, indicating that patient buyers are still absorbing the sell-off. If signs of seller exhaustion begin to emerge, a move towards $95,000—the cost basis for short-term holders—remains possible in the near term.

Off-chain conditions echo this cautious tone. ETF flows remain negative, spot liquidity is sluggish, and the futures market lacks speculative participation. The options market has strengthened its defensive stance, with traders accumulating volatility, buying short-term downside protection, and positioning themselves for upcoming volatility events ahead of the FOMC meeting.

Overall, the market structure suggests a weak but stable range, supported by patient demand but constrained by persistent selling pressure. The short-term path depends on whether liquidity improves and whether sellers will back off, while the long-term outlook hinges on whether the market can reclaim key cost base thresholds and emerge from this time-driven, psychologically stressful phase.