The New US Crypto Regulatory Framework: An In-Depth Analysis of Policy Shifts and Market Changes

- 核心观点:美国加密监管转向建设性规则制定。

- 关键要素:

- 《CLARITY法案》明确代币管辖标准。

- 《GENIUS法案》规范稳定币发行框架。

- 行政命令开放退休金投资加密渠道。

- 市场影响:促进行业合规化与机构资金流入。

- 时效性标注:中期影响。

Original author: Sam, IOSG

introduction

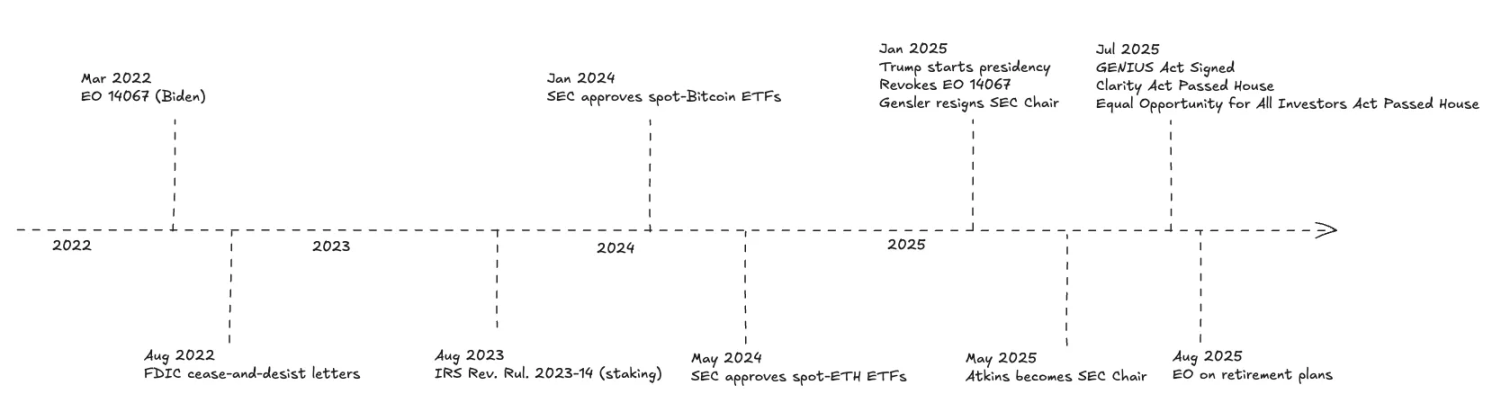

Over the past three years, the United States has seen a significant shift in its stance toward cryptocurrencies—from an early, relatively unfriendly, enforcement-focused approach to a more constructive, rule-based approach. This policy shift is not only a significant driver of widespread cryptocurrency adoption but also a key catalyst for the industry's next phase of growth.

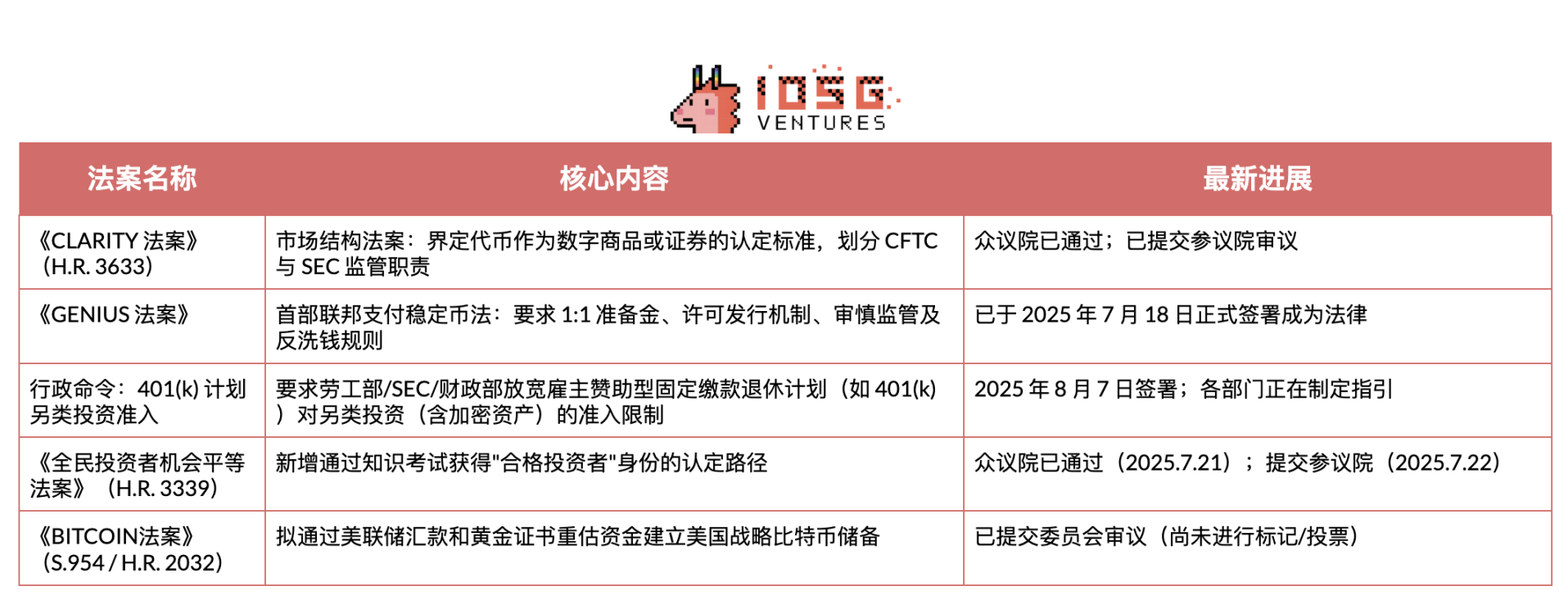

For investors, the following developments should be of particular interest: the GENIUS Act has officially come into effect, establishing a basic regulatory framework for payment stablecoins; the CLARITY Act passed by the House of Representatives will clearly define the standards for tokens to be governed by the U.S. Commodity Futures Trading Commission (CFTC) or the Securities and Exchange Commission (SEC); executive orders are pushing regulators to open up investment channels for 401(k) plans to crypto assets; and the Qualified Investor Examination reform plan passed by the House of Representatives is expected to expand the scope of access for participants in private crypto trading.

CLARITY Act

The CLARITY Act establishes core criteria for blockchain systems to be certified as "mature systems" by the SEC, clearly classifying digital assets as either "digital commodities" (regulated by the CFTC) or securities (regulated by the SEC). If a system is certified as mature, its native token can be traded as a digital commodity under CFTC regulation; other on-chain assets retain their original classification.

What is a "mature system"?

The bill clearly stipulates seven "maturity" criteria:

- System value: Market value is driven by actual adoption/usage, and the value mechanism is basically complete

- Fully functional: transactions, services, consensus mechanisms, and node/validator operations are all running in real time

- Openness and interoperability: The system is open source, and there are no unilateral exclusive restrictions on core activities.

- Programmatic system: rules are enforced by transparent code (no discretionary actions)

- System governance: No single entity/group can unilaterally modify on-chain rules or control ≥20% of voting rights

- Fairness: No special privileges (repair/maintenance/security operations are only allowed through decentralized processes)

- Distributed ownership: Issuer/related parties/related persons hold <20% of the total

The table below summarizes the core differences in the actual regulation of digital commodities (under CFTC jurisdiction) and securities (under SEC jurisdiction). The CLARITY Act framework largely maintains the existing division of regulatory oversight, but provides a clear path for the transfer of assets from SEC jurisdiction to CFTC jurisdiction. Once the underlying chain meets the aforementioned maturity standards, the relevant digital commodity can be transferred to the CFTC regulatory system.

With the statutory framework now established, the real key lies in the specific impact of the CLARITY Act on various crypto sectors.

Pledge Service

Under the CLARITY Act framework, pure on-chain staking—the act of running a validator/sequencer and issuing native rewards—does not require registration with the SEC. This “safe channel” covers validator/node operations and the distribution of protocol rewards to end users.

However, this exemption does not apply to fundraising through the minting or sale of new types of staking derivative tokens. Projects must still obtain mature blockchain certification in a timely manner and maintain anti-fraud and information disclosure obligations.

Looking back at the MetaMask/Lido/Rocket Pool incidents: Non-custodial, ministerial-style reward distribution models (note: simply enforcing the protocol's established rules without independent decision-making authority) are more consistent with the CLARITY Act's safe zone standards. However, models like Kraken's, which utilize pooled funds, custodial arrangements, and revenue commitments, would still be considered securities offerings and, if reopened without rectification, would face the same regulatory challenges.

Regarding Liquidity Staking Tokens (LSTs): 1:1 certificates that solely reflect user staked assets and protocol rewards fall under the category of ministerial end-user distributions. However, models involving strategic selection (such as re-staking/AVS distributions), stacking of points/extra income, or the issuance of asset management tokens/share certificates that pool and redistribute income constitute managed investment propositions and remain under SEC jurisdiction unless an exemption is met.

Decentralized Exchanges (DEX)

DEXs offering pure on-chain spot trading of native blockchain tokens (such as BTC, ETH, governance or utility tokens) are exempt from exchange registration. Operating a DEX's core smart contracts, order book logic, matching engine, or AMM factory is not considered "exchange" activity under the Securities Exchange Act—and therefore does not require exchange or broker registration for spot trading of exempt tokens.

However, platforms involving derivatives (futures, options, perpetual contracts), security tokens (on-chain stocks), or real-asset tokens (such as gold) are still fully regulated by the SEC or CFTC.

Payments of protocol fees to liquidity providers (LPs) or other users who contribute work/assets fall under the CLARITY Act's DeFi exemption. Importantly, the Act does not change the criteria for determining securities. If a governance token (such as UNI) distributes cash or earnings to holders solely for holding them, it would constitute a profits interest and likely qualify as a security under the Howey test (the expectation of profit from the efforts of others). Profit distributions and secondary trading of tokens in such circumstances would fall under SEC oversight.

Decentralized stablecoins

The Collateralized Debt Position (CDP) model (locking collateral to mint USD-pegged tokens) is subject to SEC jurisdiction during its launch phase: tokens redeemed for value are considered investment contracts until the protocol receives blockchain maturity certification. Early-stage teams can still raise funds under the initial offering exemption under the CLARITY Act—up to $50 million over a rolling 12-month period—but must comply with crypto-specific disclosure obligations and a four-year lifecycle anti-fraud responsibilities. Once governance is fully on-chain and no single entity controls ≥20% of voting rights or collateral, the protocol can apply for mature certification. Thereafter, the governance token and minting/burning mechanism will fall under CFTC digital commodity regulation and will no longer be subject to SEC securities rules.

The Delta Neutral model is different: because it relies on crypto collateral plus derivatives risk exposure and profit distribution mechanism, even if the underlying chain is mature, it does not fall within the spot commodity exemption of the CLARITY Act; nor does it comply with the "licensed payment stablecoin" system framework of the GENIUS Act.

Lending business

Lending is considered credit, not spot trading, and therefore does not fall under the spot commodity exemption of the CLARITY Act. Interest-bearing certificates of deposit that are pooled with funds are considered securities unless an exemption (Regulation D or Regulation S) is invoked.

Yield Aggregator

The aggregator contract is tamper-proof and non-custodial (no single entity can unilaterally modify it) and does not require registration as a trading platform or intermediary.

However, any governance token or treasury share certificate that grants holders rights to future returns constitutes an investment contract upon issuance. Furthermore, complex custodial strategies may trigger multiple registration requirements: if rebalancing or control is off-chain or held by a centralized operator, the project will lose its DeFi exemption and re-trigger the compliance obligations of brokers/dealers or exchanges.

ETF pledge business

The CLARITY Act provides support at the fundamental level: it is the first legislative act to clarify that staking rewards are “end-user distributions” (not securities) and allows networks to transfer their native tokens to CFTC regulation once they are certified as mature. This removes core securities law barriers to funds routing protocol proceeds within their own funds.

However, ETFs are still subject to fund regulations. These include two key constraints: First, the Investment Company Act's liquidity rule (Rule 22e-4) stipulates that "illiquid assets" may not exceed 15% of net asset value; an asset is classified as illiquid if it cannot be liquidated at approximately its book value within seven calendar days. Native collateral positions with unbundling/exit queuing mechanisms often fall into this category.

Secondly, if the product is a registered open-end ETF, it must adhere to the diversification requirements of the Investment Company Act of 1940: the well-known 75/5/10 rule, which means that staking exposure and validator relationships cannot be concentrated in a single "issuer" or operator. In practice, this requires a multi-validator split strategy and precise sizing to ensure that at least 75% of assets do not exceed the 5%/10% thresholds for any one counterparty. (Some crypto ETPs circumvent this restriction through non-'40 Act structures, but most staking ETFs are still registered under the '40 Act and use Cayman Islands subsidiaries.)

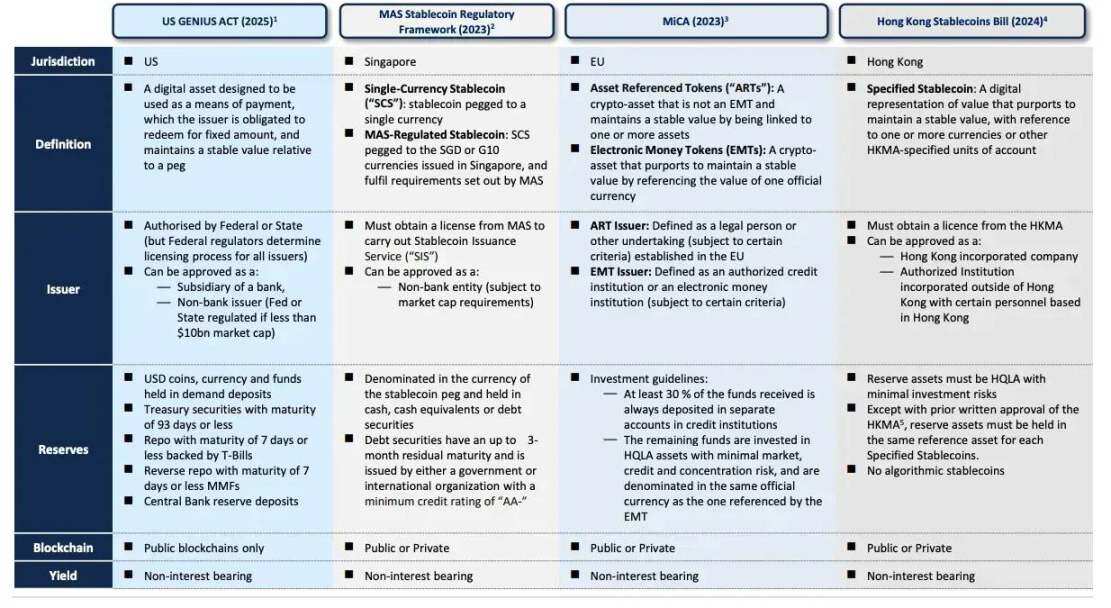

GENIUS Act

In July 2025, the United States officially enacted the GENIUS Act, the first federal law to comprehensively regulate stablecoins.

The bill limits issuance to regulated entities and establishes core rules for prudent operations, code of conduct, anti-money laundering, and bankruptcy resolution. Its core entry threshold is: "Except for licensed payment stablecoin issuers, no entity may issue payment stablecoins in the United States."

According to the bill, the issuer must hold 100% of the reserve assets, which are limited to the following three categories:

- US dollars or Federal Reserve bank deposits

- U.S. Treasury bonds with a maturity of 93 days or less

- Treasury-backed overnight repurchase agreements

Pursuant to Section (7)(A) “Restrictions on Payment Stablecoin Activities”, a licensed issuer may only conduct the following activities:

- Issuing payment stablecoins

- Redeem payment stablecoin

- Managing relevant reserve assets (including buying, selling, holding, or providing custody services for reserve assets in accordance with the law)

- Provide stablecoin, reserve asset or private key custody services in accordance with the law

- Carry out related business that directly supports the above activities

This strict list has a clear regulatory intent: to ensure redemption security by isolating stablecoin operations from high-risk activities. The bill specifically stipulates that "payment stablecoin reserve assets may not be pledged, re-hypothecated, or reused." This means that even if banks use assets denominated in their own tokens, they cannot include them in the reserve collateral for loan operations.

As the GENIUS Act clarifies issuance qualifications and reserve rules, multiple industries have begun to shift from pilot projects to large-scale applications:

- Banking: While facing competition from tokenized cash for deposits, banks, due to their advantageous regulatory structures, are natural issuers. The most likely path forward is through bank subsidiaries or strictly regulated bank-tech partnerships, starting with enterprise use cases, whitelisted counterparties, and conservative liquidity management policies, with the goal of replacing potential deposit losses with stablecoin revenue.

- Retail: Large merchants view stablecoins as a tool to reduce card fees and shorten settlement cycles. Early implementation will rely on licensed issuers and closed-loop redemption systems, promoting them through settlement discounts rather than interest payments, and directly integrating with ERP and payment systems to improve capital turnover efficiency.

- Card schemes: Visa and Mastercard will integrate stablecoins into new settlement channels while retaining their authorization, fraud prevention, and dispute resolution infrastructure. This move enables weekend and near-real-time settlement without requiring merchant front-end changes, driving a shift in revenue models toward tokenization, compliance, and dispute management services.

- Fintech: Payment processors and wallet platforms are launching stablecoin accounts, cross-border payments, and on-chain settlement products that support bank-grade KYC, sanctions screening, and tax reporting. Competitive advantage will lie in operational control systems that conceal blockchain technology complexity, provide reliable fiat currency channels, and meet corporate procurement and audit requirements.

As the US rules system becomes established, similar frameworks are emerging in many parts of the world (such as Hong Kong's Stablecoin Ordinance), and more stablecoin regulations are expected to be introduced one after another.

▲ TBAC Presentation, Digital Money

Other policy trends

New Retirement Plan Investment Policy

The executive order "Expanding Access to Alternative Assets for 401(k) Investors," signed in August 2025, aims to expand the investment options for employer-sponsored retirement plans and allow retirement savers to allocate alternative assets such as digital assets through actively managed investment vehicles.

As an executive branch, the Department of Labor is required to reassess its Employee Retirement Income Security Act (ERISA) guidance within six months. It is expected to introduce ERISA-compliant safeguards, reaffirming the neutral, case-by-case prudential standard and providing a safe harbor checklist.

While the SEC, an independent agency, is not directly subject to executive orders, it can promote access through rulemaking: clarifying qualified custodian standards, improving crypto fund disclosure/marketing regulations, and approving retirement plan-friendly investment vehicles.

Currently, most 401(k) plans still don't include crypto assets in their core menus. This is primarily achieved through self-directed brokerage windows, where participants can purchase spot Bitcoin ETFs (some plans also include Ethereum ETFs), with a few providers also offering limited "crypto asset windows." In the short term, compliance will be limited to regulated ERISA-compliant products: spot BTC/ETH ETFs and professionally managed funds with structured crypto allocations. Because 401(k) committees adhere to ERISA's "prudent investor" principle, it's difficult to demonstrate that single volatile tokens, self-custody, or staking/DeFi yields are suitable for average savers. Most tokens and yield strategies lack standardized net asset value calculations, stable liquidity, and clear custodial audit trails. Furthermore, their legal status is unclear, and inclusion in plans could trigger SEC/DOL scrutiny and the risk of class action lawsuits.

Equal Opportunity for All Investors Act

The bill proposes to create a new "accredited investor" designation path by establishing an SEC knowledge exam. The House of Representatives passed the bill on July 21, 2025, and the Senate accepted it for deliberation on July 22.

Early token pre-sales, crypto venture capital, and most private rounds in the United States rely on Regulation D, which currently limits participation to accredited investors. The knowledge-based exam path will overcome wealth/income thresholds, allowing investors with specialized knowledge but not necessarily wealth to legally participate in private crypto financing.

Opponents argue that expanding access to the opaque and illiquid private equity market could exacerbate investment risks. The bill's fate in the Senate will depend on the rigor of the exam and the adequacy of safeguards. Even if passed, the SEC would need one year to design the exam and 180 days to implement it through FINRA, meaning it would not take effect immediately.

BITCOIN Act

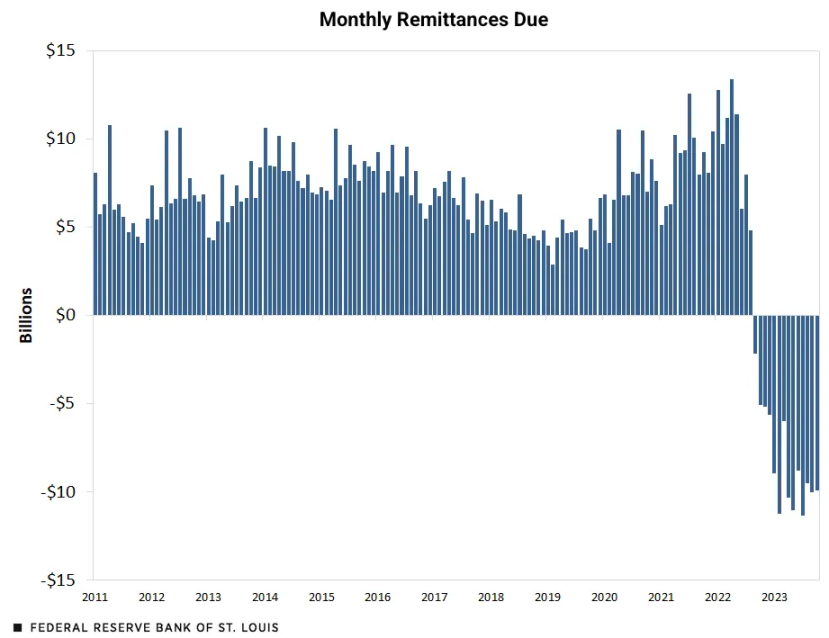

The BITCOIN Act (S.954), introduced by Senator Cynthia Lummis on March 11, 2025, proposes establishing a U.S. strategic Bitcoin reserve. The bill requires the Treasury to purchase 200,000 BTC annually (over a five-year period, for a total of one million) and impose a 20-year lock-up period (during which sales, swaps, or pledges are prohibited). After 20 years, gradual sales (limited to 10% of holdings every two years) may only be recommended to reduce federal debt. The bill also stipulates that confiscated BTC must be transferred to the strategic reserve after the judicial process is concluded.

Funding does not rely on new taxes or government bonds, but rather through: (1) the first $6 billion of the Federal Reserve's annual remittances to the Treasury between fiscal years 2025 and 2029 will be used first to purchase Bitcoin; and (2) the book value of the Federal Reserve's gold certificates will be revalued from $42.22 per ounce to the market price (approximately $3,000 per ounce), with the increased value first injected into the Bitcoin program.

▲ https://www.stlouisfed.org/

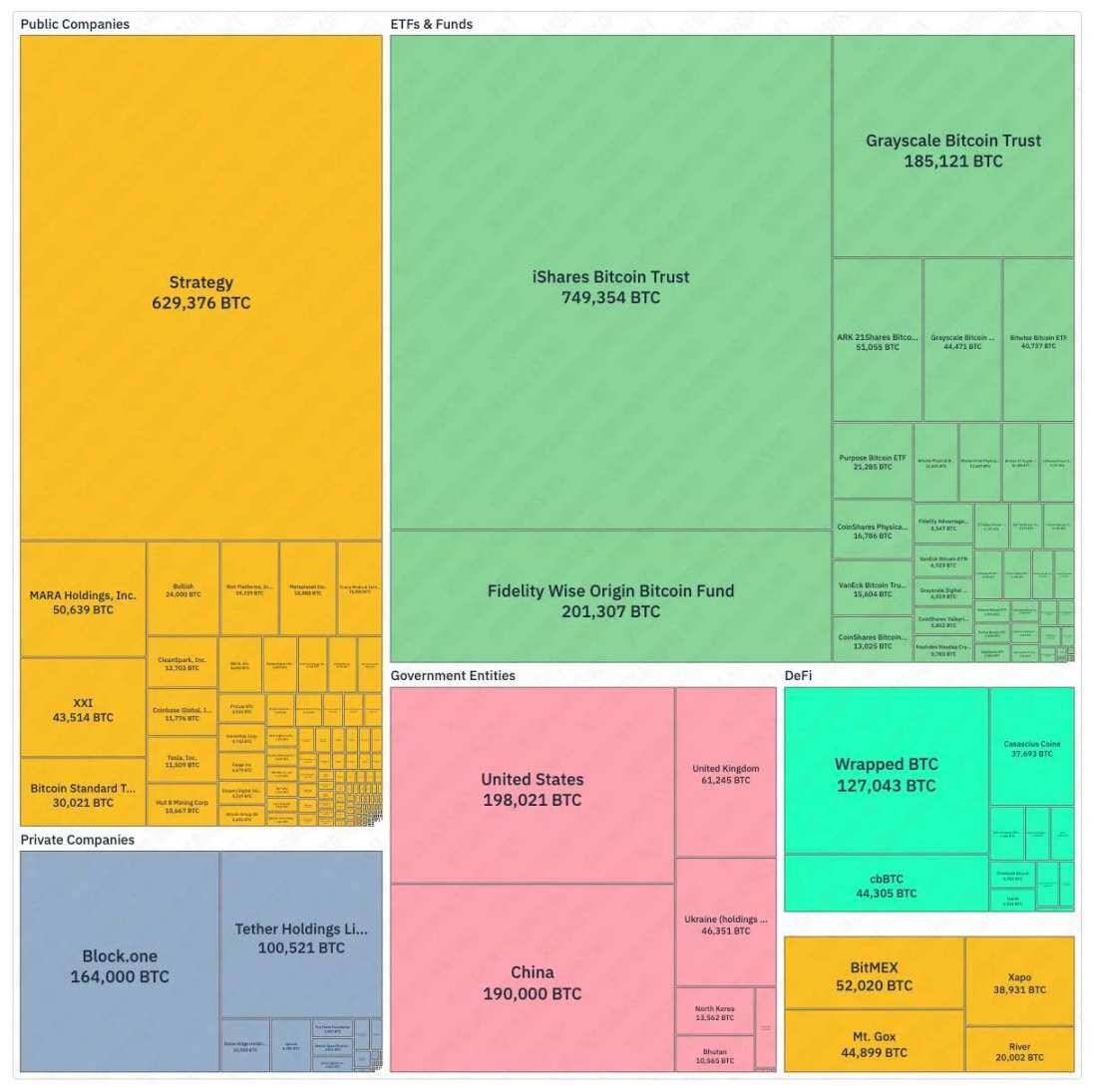

If fully implemented, the US will have purchased a cumulative 1 million BTC (approximately 4.8% of the 21 million BTC cap). By comparison, MicroStrategy, the largest publicly traded company currently holding Bitcoin, holds 629,000 (approximately 3%). This reserve size would surpass the holdings of any single ETF, and even significantly surpass the total holdings of all ETFs (approximately 1.63 million) as reported by bitcointreasuries.net.

By elevating Bitcoin to strategic reserve asset status, the United States will grant it unprecedented legitimacy. This official endorsement could shift the stance of institutional investors who have been hesitant due to regulatory uncertainty. If the United States takes the lead, other countries could follow suit. All of these effects will create a powerful driver of Bitcoin's price: five years of sustained purchases will create substantial demand, and combined with the supply shock created by a 20-year lock-up period, it is likely to lead to global capital allocation.

▲ bitcointreasuries.net

However, the BITCOIN Act has only been submitted to the Senate Banking Committee and has yet to be reviewed or voted on. Its progress lags far behind the CLARITY Act, which has already passed the House of Representatives, and the already enacted GENIUS Act. On a practical level, the bill touches on core issues of Federal Reserve independence and budgetary politics: it mandates the purchase of one million Bitcoins, locked up for 20 years, financed through Federal Reserve remittances and gold revaluation. The bill currently enjoys primary Republican support, but major decisions involving the balance sheet typically require bipartisan consensus for Senate passage. More critically, directing future Federal Reserve remittances to Bitcoin purchases would reduce fiscal revenue that could be used to reduce borrowing, potentially exacerbating budget deficit risks.

ETF

The clearest signal of a shift in policy direction was the SEC's approval of spot crypto ETFs after years of delay. In January 2024, the agency made history by approving several spot Bitcoin ETPs and immediately launching trading, driving Bitcoin to a record high in March and attracting mainstream capital. By July 2024, spot Ethereum ETFs were trading in the US, with major issuers launching funds that directly hold ETH.

The SEC has also demonstrated an openness to assets beyond Bitcoin and Ethereum: it is actively processing applications for other crypto ETFs and working with exchanges to develop common listing standards to streamline future approvals. Positive progress has also been made in the staking sector, with the SEC recently clarifying that "agreement staking activities" do not constitute securities offerings under federal securities laws.

Development of the US prediction market

In early October 2024, a federal appeals court approved the pre-election launch of the prediction market platform Kalshi, significantly increasing market participation. The CFTC subsequently continued to advance its rulemaking on event contracts, holding a roundtable meeting in 2025. While no timeline has been set, further guidance or final rules are possible.

Polymarket, through its subsidiary QCX LLC (now Polymarket US), has received CFTC-designated contract market status and announced the acquisition of the QCEX exchange, stating that US access will be available "in the near future." If integration and approval proceed smoothly, and the CFTC ultimately expresses openness to political contracts, Polymarket may be able to participate in the 2026 US election prediction market. The platform is reportedly exploring issuing its own stablecoin to capture Treasury yields from the platform's reserves, but currently, user returns primarily come from market making/liquidity rewards rather than real-world asset returns on idle funds.

in conclusion

US policies are the primary lever shaping market structure and capital access, and thus have a decisive influence on Bitcoin prices. The SEC's approval of a spot ETF on January 10, 2024, opened up mainstream funding channels and propelled Bitcoin to a record high in March 2024. The friendly policy environment created by Trump's election victory in November 2024 further pushed prices to a new peak in July-August 2025. Future trends will depend on the standardization of regulations and infrastructure.

Baseline Scenario: Policy implementation continues. Regulators implement the GENIUS Act, the Department of Labor develops ERISA safeguards, and the SEC gradually approves ETFs and pledge mechanisms. Access to stablecoins expands through brokerage windows and registered investment advisors (RIAs), while banks and card schemes expand stablecoin settlement applications.

Optimistic scenario: The Senate advances the market structure bill, the first batch of "mature blockchain" certifications are issued without significant objections, and the Department of Labor provides a safe harbor. Banks issue licensed stablecoins on a large scale, and the ETF product menu continues to expand. This will accelerate pension/RIA allocations, increase liquidity depth, and lead to a revaluation of compliant, truly decentralized assets.

Pessimistic scenario: Legislative progress stalls – all pending bills remain unaddressed. The SEC delays or rejects amendments to collateralized ETFs. Bank regulators take a hard line on GENIUS Act implementation, slowing large-scale issuance; and major record-keepers restrict brokerage window access.

Regardless of the scenario, the following hard indicators will serve as key signals: the number of licensed stablecoin issuers and settlement volume, the approval of the first batch of mature certifications and SEC objections, the scale of net inflows into ETFs and the proportion of 401(k) plans with brokerage windows, and the progress of bank/card scheme settlement pilots transitioning to full-scale operations. These indicators will reveal whether the US crypto market is evolving towards a regulated financial system or relapsing into contraction.