CoinGecko report: RWA wave rises, tokenized US debt grew more than 6 times last year

Original source: CoinGecko

Original compilation: 1912212.eth, Foresight News

RWA sits at the intersection between the real world and blockchain, issuers and investors. Being able to act as an effective middleman at the crossroads will be the key to its success. Although it is inevitable to rely on third parties, such as oracles, custodians, credit rating agencies, etc., how to effectively utilize and manage these third parties is still very important for its continued operations.

In 2021 and 2022, private credit markets emerged through unsecured lending platforms such as Maple, Goldfinch and Clearpool, allowing large institutions to borrow funds based on their creditworthiness. However, these protocols suffered significant defaults as a result of the collapse of Luna, Three Arrows Capital, and FTX. As DeFi yields plummet in 2023 and users flock to rising U.S. Treasury bond rates, there has been explosive growth in tokenized Treasury bonds. Providers such as Ondo Finance, Franklin Templeton and OpenEden saw significant inflows as the total value locked in tokenized Treasuries soared from $114 million in January 2023 to $845 million by the end of the year.

The 2024 RWA development report mainly has four points:

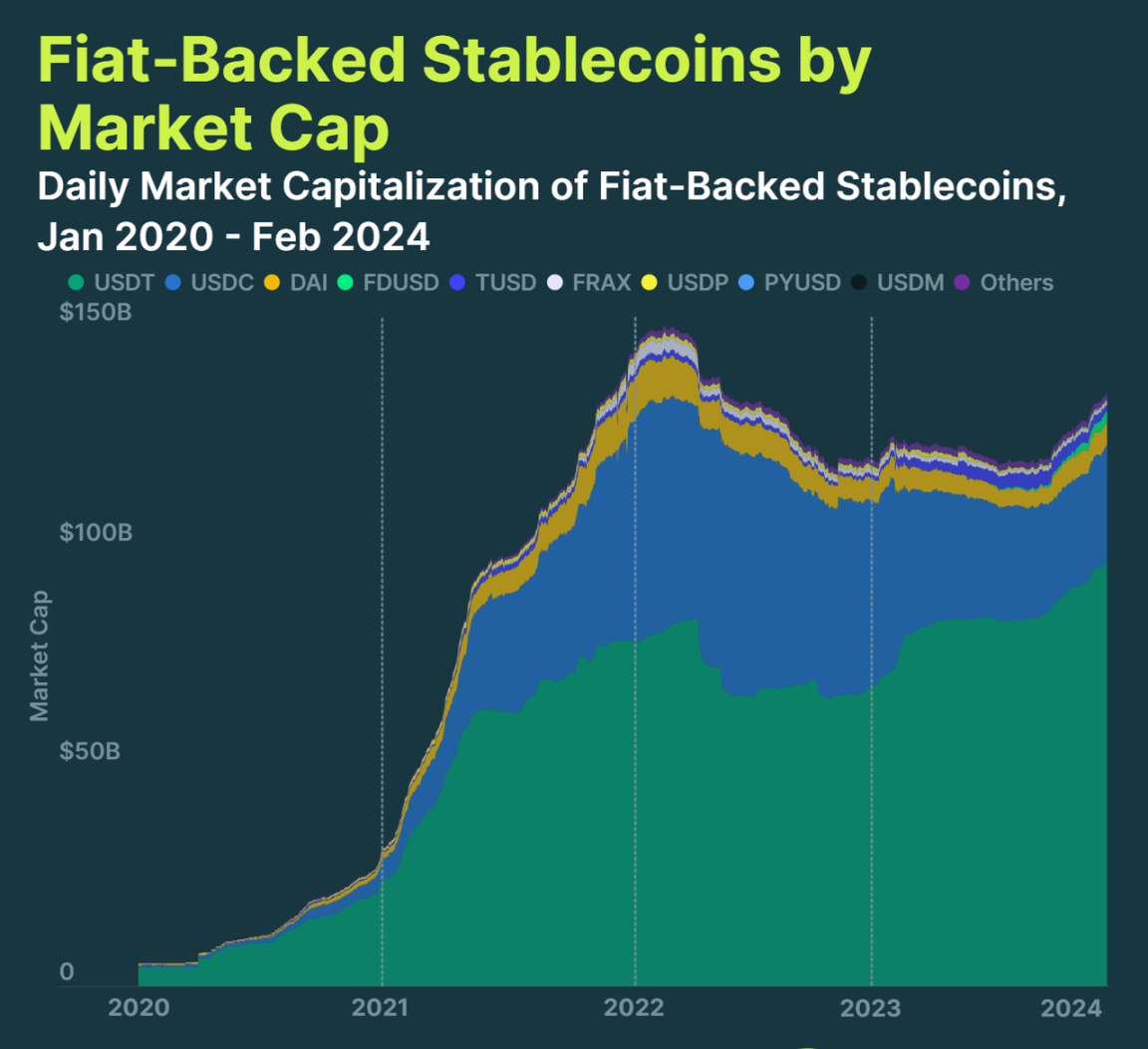

1. Most RWAs are stablecoins pegged to the U.S. dollar.

The top three U.S. dollar stablecoins alone account for 95% of the market, with USDT at $96.1 billion, USDC at $26.8 billion, and DAI at $4.9 billion. USDT continues to dominate, with a market share of 71.4%. Meanwhile, USDC has yet to recover from a sharp decline in market share following its brief decoupling during the U.S. banking crisis in March 2023.

Stable assets other than USD-pegged stablecoins account for only 1% of the market. These assets include other fiat currencies such as Euro Tether (EURT), CNH Tether (CNHT), Mexican Peso Tether (MXNT), EURC (EURC), Stasis Euro (EURS), and BiLira (TRYB).

The market capitalization of stable assets rose rapidly from $5.2 billion in early 2020 to a peak of $150.1 billion in March 2022, before gradually declining throughout the bear market. However, its market value will increase by 4.9% by 2024, from US$128.2 billion at the beginning of the year to US$134.6 billion on February 1.

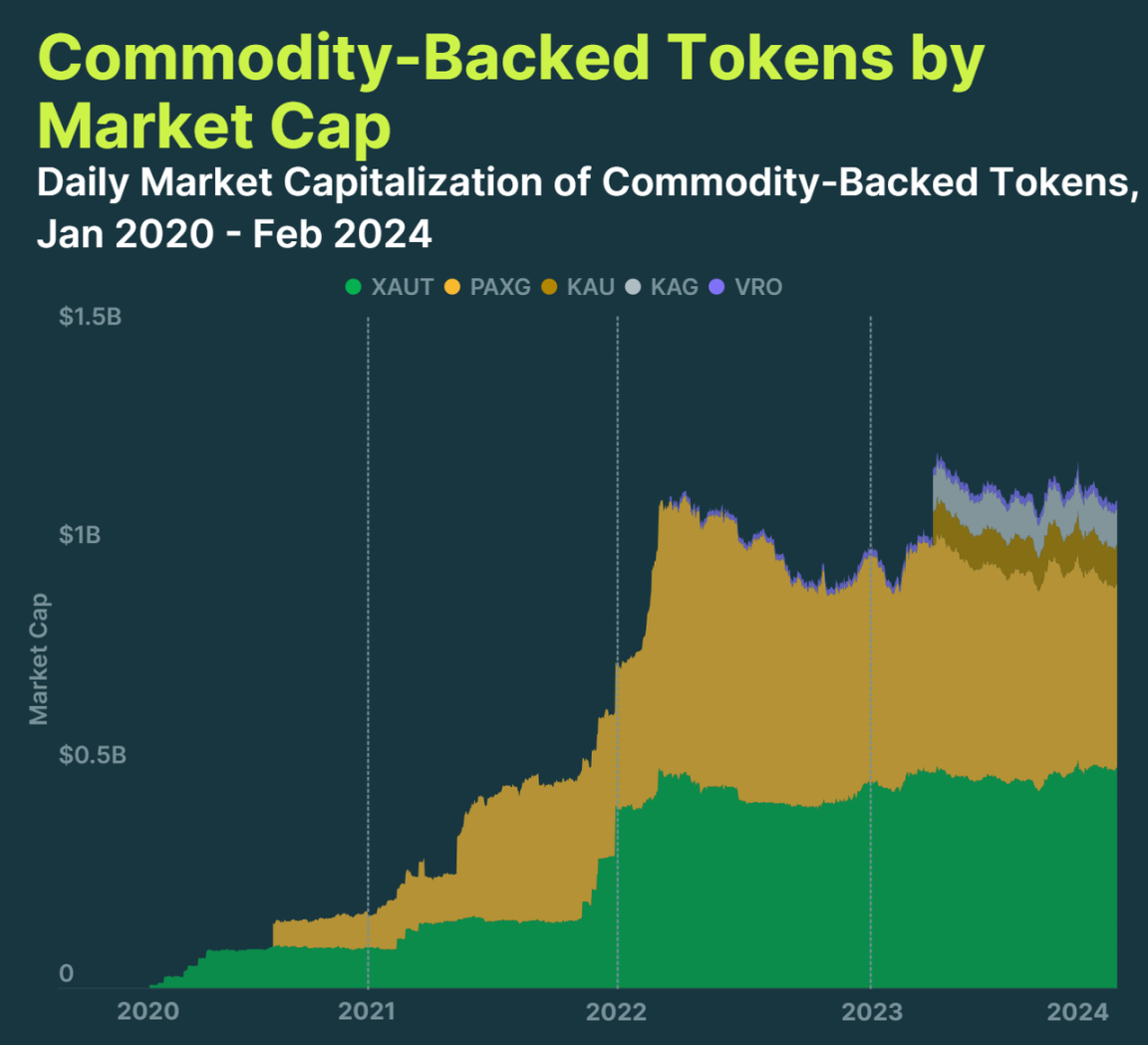

2. The market value of commodity-backed tokens reached US$1.01 billion, and gold remains the most popular commodity

Tokenized precious metals such as Tether Gold (XAUT) and PAX Gold (PAXG) account for 83% of the market capitalization of commodity-backed tokens. Tokens like XAUT and PAXG are backed by one ounce of physical gold, while Kinesis Gold (KAU) and VeraOne (VRO) are backed by one gram of gold.

While tokenized precious metals dominate, tokens backed by other commodities have also been launched. For example, the Uranium 308 project released tokenized uranium, with the price pegged to the price of 1 pound of U3O8 uranium compound. It can even be redeemed, but first requires passing strict compliance protocols.

Although the market value of commodity-backed tokens reaches $1.1 billion, it only accounts for 0.8% of the market value of fiat-backed stablecoins.

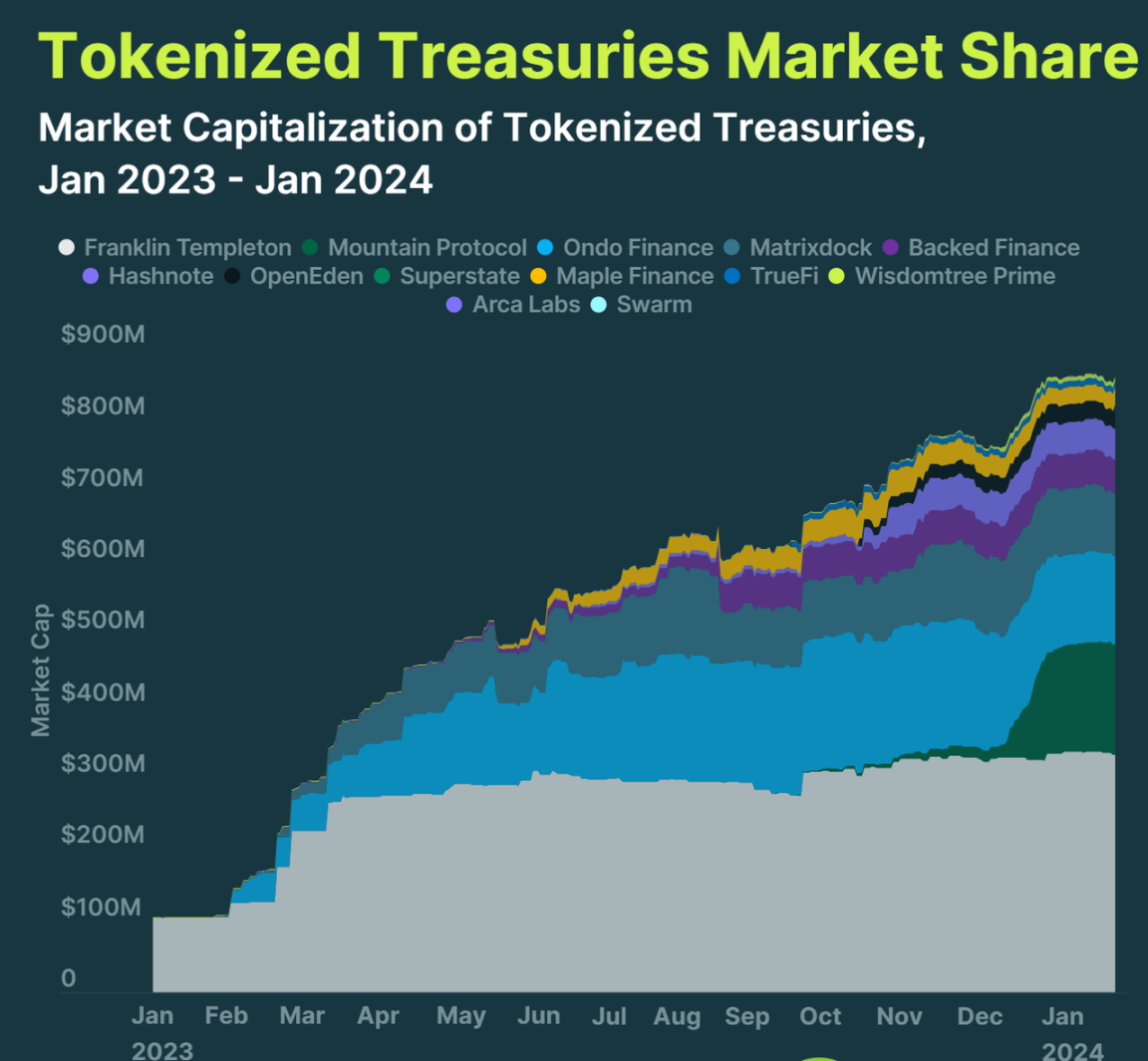

3. Tokenized U.S. bond products increased by 641% in 2023 and are currently worth over US$861 million

Tokenized U.S. Treasuries surged in popularity during the bear market, with their market capitalization increasing by 641% from $114 million to $845 million in 2023. However, this momentum has stalled since 2024, with growth of 1.9% in January and a market capitalization of $861 million.

Franklin Templeton is currently the largest issuer of tokenized U.S. Treasury bonds, with the U.S. Government Monetary Fund issuing $332 million in tokens on its chain. This gives it a market share of just over 38.6%.

Yield stablecoin issuers such as Mountain Protocol and Ondo Finance are also popular. Since its inception in September 2023, Mountain Protocol has minted $154 million in USDM tokens as of February 2024, while Ondos yield stablecoin USDY has a market capitalization of $132.4 million.

Most tokenized vaults are based on Ethereum, which holds 57.5% of the market share. However, companies such as Franklin Templeton and Wisdomtree Prime have chosen to issue on Stellar and currently hold a dominant 39% share of Stellar.

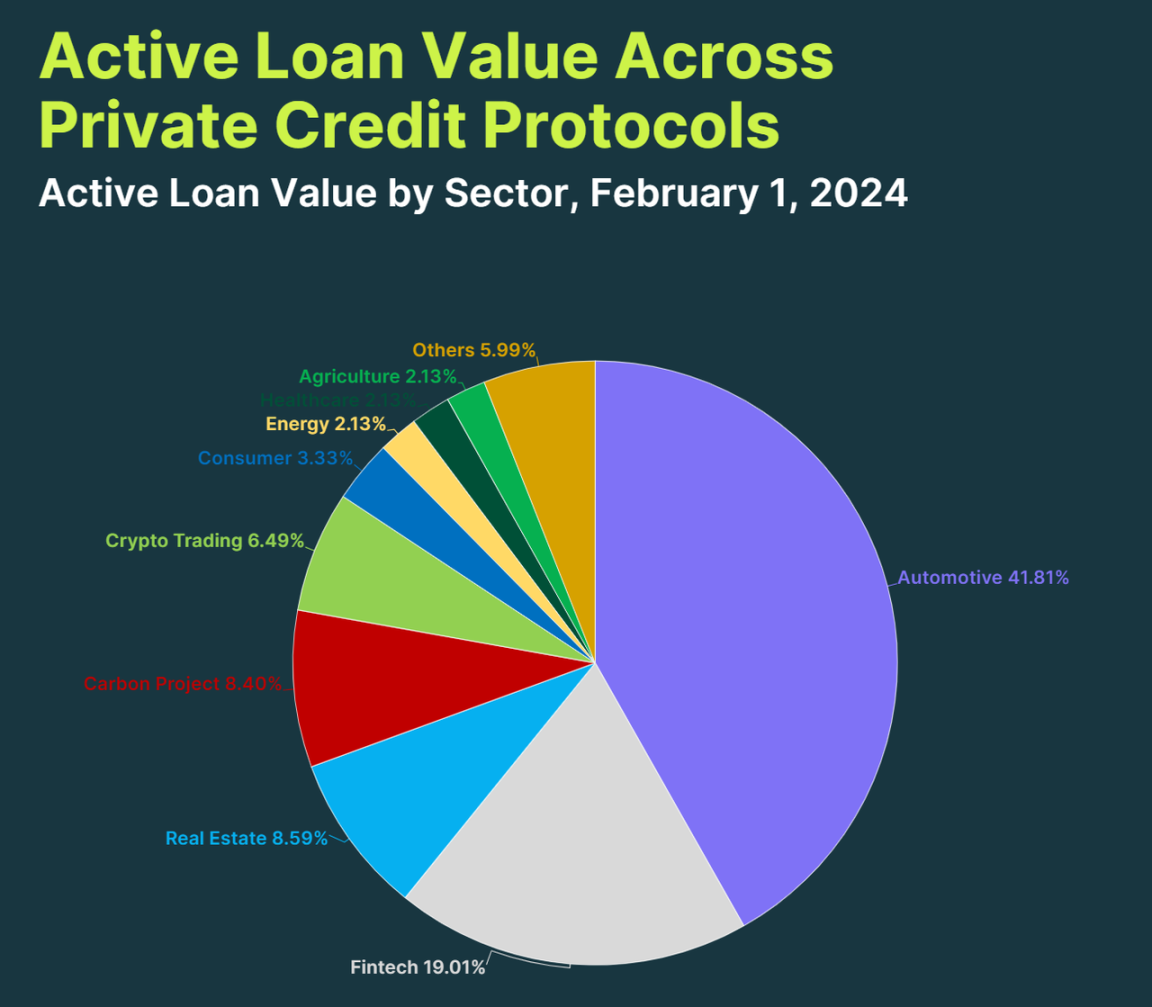

4. Private credit demand is mainly concentrated in the automobile industry, accounting for 42% of all loans

Of the $470.3 million in outstanding loans issued by private credit agreements, 42%, or $196 million, was for auto loans. Meanwhile, debt in the fintech and real estate sectors accounted for only 19% and 9% respectively.

Auto loans grew significantly in 2023, with 60 loans originating over $168 million.

A total of 840 loans were received in the real estate and cryptocurrency trading sectors, but only 10% of the loans are currently active. The rest have been repaid and some have defaulted. Notably, 13 loan defaults occurred in the cryptocurrency trading space following the collapse of Terra and Three Arrows Capital.

Statistical borrower data shows that most companies are from emerging markets such as Africa, Southeast Asia, Central and South America. 42 loans (40.8% of all loans) originated from Africa.