Inheriting the legacy of Terra, can Mint Cash surpass the glory of UST?

Original - Odaily

Author-husband how

Recently, the rise of USTC has attracted widespread attention. At the same time, the prices of LUNC and LUNA have also been affected by it and have increased to a certain extent. The reason for the increase is not the resurrection of Terra, but the airdrop of Mint Cash, a stable currency project with Terras last wish as its vision. expected.

Mint Cash wants to recreate the original vision of TerraUSD: a stablecoin system that does not rely on traditional financial systems and centralized control. Currently, the mainstream stablecoins in the encryption market, such as USDT, USDC, etc., mostly use US dollars as collateral. And issuance. There is still a lack of stablecoins in the crypto market that use native assets as collateral and are widely adopted. TerraUSD was once considered the leader, but algorithmic stablecoins are prone to a death spiral, and the ending of Terra has confirmed this.

Although Mint Cash was born out of the Terra Classic (formerly Terra) stablecoin mechanism, on this basis, the original mechanism has been optimized to avoid the intensification of decoupling.

Odaily explains the future prospects of Mint Cash by interpreting the white paper of Mint Cash, starting from the Mint Cash mechanism.

Mint Cash’s robust mechanism settings

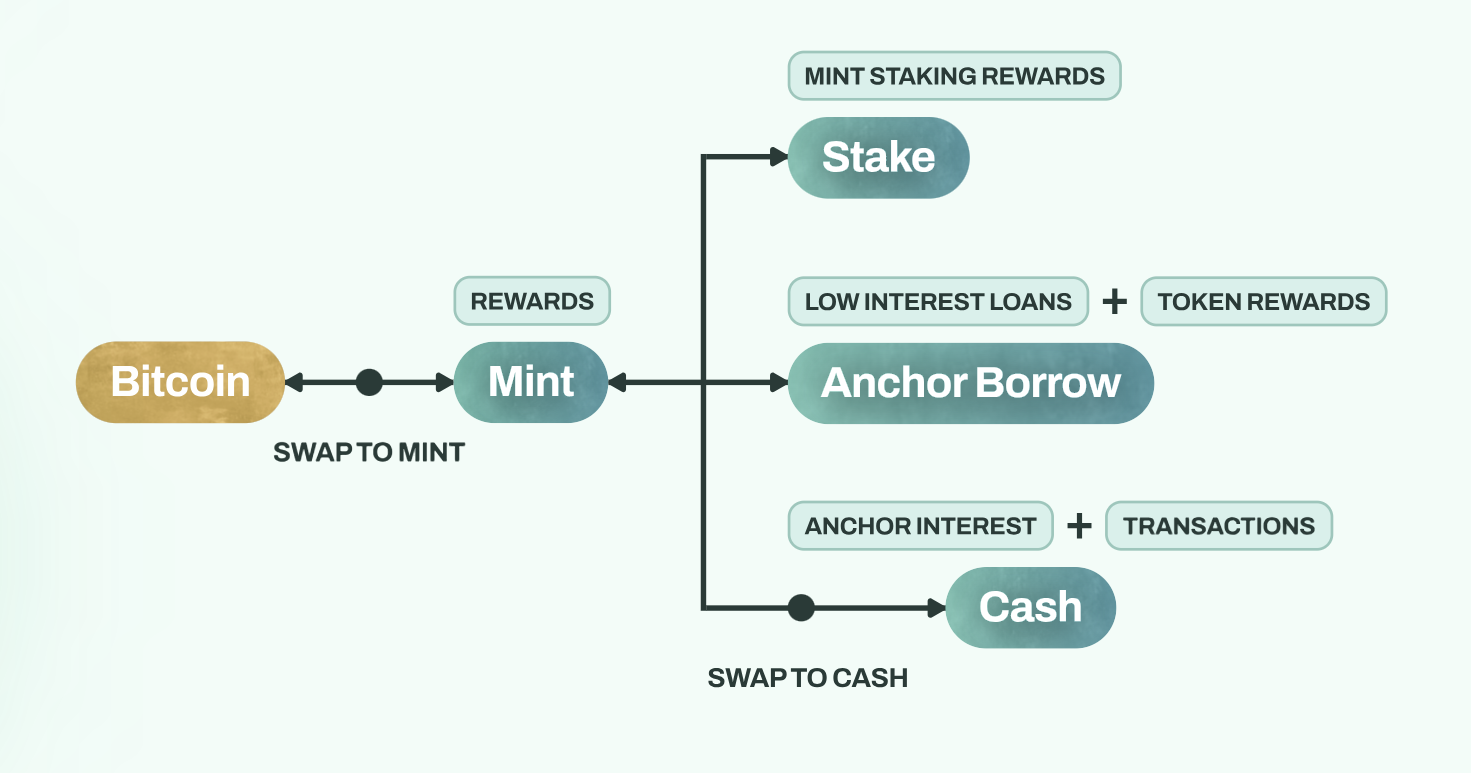

Mint Cash is built on the Terra Core stablecoin system, which features Mint tokens backed by Bitcoin. Mint Cash introduces an automated liquidity management and virtual automated market maker (VAMMS) mechanism that mimics the policies of central banks involved in foreign exchange trading and liquidity provision. Any user can deposit Bitcoin to receive Mint tokens, or they can destroy Mint tokens and exchange them back for the underlying Bitcoin.

The following figure is the flow chart of Mint Cash’s stablecoin mechanism:

The key to a stablecoin lies in the risk resistance of its mechanism. As a stablecoin project built on the basis of Terra Core, Mint Cash has taken the first step to improve the original mechanisms risk. We will start from the perspective of how the Mint Cash mechanism improves risk resistance, and elaborate from four perspectives: the role of Mint tokens, the innovation of the Anchor savings protocol, Mint Cash’s tax policy, and Mint Cash’s foreign exchange loan market.

The key to a stablecoin lies in the risk resistance of its mechanism. As a stablecoin project built on the basis of Terra Core, Mint Cash has taken the first step to improve the original mechanisms risk. We will start from the perspective of how the Mint Cash mechanism improves risk resistance, and elaborate from four perspectives: the role of Mint tokens, the innovation of the Anchor savings protocol, Mint Cash’s tax policy, and Mint Cash’s foreign exchange loan market.

What Mint Token Does

As an indispensable part of the Mint Cash stablecoin system, Mint tokens not only serve as certificates for Bitcoin collateral, but also as collateral for redemption of Cash stablecoins. However, the real core role of Mint tokens is as a risk buffer medium.

Using AAVE as an example, normal users who participate in lending need to mortgage ETH to lend stablecoins, but if the price of the collateral drops, they may face the risk of liquidation.

In the same way, Mint Cash, as a stablecoin project, uses Bitcoin, whose price fluctuates more than legal currency, as collateral. If the price of Bitcoin fluctuates too much, it will cause the value of the stablecoin system to become unanchored. This is also the case for most stablecoins. The reason why projects use legal currency or government-backed stablecoins as collateral.

To do this, the Mint Cash system attempts to replenish the liquidity gap between BaseSatoshis (the number of Bitcoins in the system) and BaseCollateralInput (the amount of collateral input) every CollateralPoolRecoveryPeriod. When BaseSatoshis is extremely low or extremely high relative to BaseCollateralInput, the system will control the outflow and inflow of capital within the system by adjusting virtual slippage to maintain the stability of the system. This allows Mint to act as an asset buffer, temporarily covering sudden systemic shocks that may be caused by collateral deposits and withdrawals.

In addition, the exchange of Mint tokens and Cash stablecoins relies on the fair market value of Mint determined by the verifier. The calculation factors include the total value of locked Bitcoin collateral, Mint staking rewards, and the total value of all minted Cash stablecoins. Value, pegged borrowing rate and utilization rate of all Cash stablecoins denominated in SDR, etc.

Mint tokens are interchangeable with multiple Cash stablecoins, each pegged to a different fiat currency. For example, the flagship Cash stablecoin is CashSDR, which reflects the value of the International Monetary Fund SDR, and there are multiple Cash stablecoin variants such as CashUSD, CashEUR, CashGBP, and others.

Innovation in Anchor Savings Protocol

Mint Cash provides a high-yield savings account as a solution for adjusting token demand through a savings protocol Anchor Sail (formerly Terras savings protocol Anchor). The goal of the protocol is to ensure the stability of tokens within the system while providing a liquidity management mechanism to maintain market liquidity.

The main functions of Anchor in Mint Cash have two aspects:

As a multi-token basket product, Anchor can act as a multi-token hedging tool: Anchor contains a variety of tokens, so it can be used to hedge the value and interest rate risks of tokens. For example, if a certain token declines in value or interest rates fall, this may be offset by an appreciation in value or rising interest rates for other tokens in the basket. In this way, Anchor provides a level of stability, both in terms of value and interest rates.

Anchor solves the initial adoption problem by providing efficient lending services: traditional interest rate models assume there are certain operating costs and overheads between deposit rates and lending rates, but smart contract-based token markets have no such overhead. Therefore, Anchor can provide higher deposit interest at similar interest rates, thereby attracting more capital to enter and use new tokens.

Overall, in Mint Cash, Anchor’s main role is to hedge risks, provide stability, and solve initial adoption issues, thereby promoting the stability and development of the entire system.

Mint Cash Tax Policy

In the Mint Cash system, tax policy is a key part of its stabilization mechanism. Mint Cash follows the example of Terras transaction tax mechanism and adds a property tax mechanism to levy property tax on accounts that have not conducted transactions for a period of time or whose transaction amount is below a certain value. The goal of this tax policy is not to increase government revenue, but to maintain the stability of the token.

Mint Cash’s tax policy has two main components:

Taxes on Transactions: Every transaction is subject to a certain percentage of tax. The purpose of this tax policy is to curb excessive market liquidity and prevent market bubbles by increasing transaction costs.

Taxation on property: Property taxes are levied on accounts that do not conduct transactions within a certain period of time (for example, a tax cycle) or where the transaction amount is below a certain value. The purpose of this tax policy is to encourage market liquidity and prevent funds in the market from being idle for a long time.

Additionally, Mint Cash’s governance mechanism includes a Treasury Committee, which is given the power to determine certain important token policy parameters, such as interest rates, tax rates, and borrowing rates. This governance mechanism allows Mint Cash to make decisions quickly when necessary to maintain the stability of the token.

Mint Cash’s Forex Loan Market

Mint Cash’s FX Loan Market is a marketplace that allows users to borrow one stablecoin using another stablecoin as collateral. It is a synthetic market, meaning it does not need to provide upfront liquidity, pay actual interest, or liquidate collateral.

The market sets parameters for minimum liquidity and maximum borrowing amounts for all stablecoins. The market should hold at least a certain amount of a specific stablecoin to deal with risk and liquidity management; for a specific stablecoin, the borrowing amount cannot exceed the set maximum borrowing amount.

The three main functions of this market are: borrowing, repayment and liquidation.

Borrowing: When a user wants to borrow money, the market performs a transaction internally to convert the funds into an LTV (loan to value) set by the user. The LTV should be lower than the set maximum LTV while maintaining sufficient liquidity.

Repayment: When a user wants to repay a loan, the opposite of borrowing is performed.

Liquidation: A loan may be liquidated when its LTV exceeds a set maximum LTV. Anyone can query the loan list and perform liquidation operations on loans that require liquidation.

Additionally, both the Treasury Committee and the protocol governance have the authority to determine these parameters, including the borrowing rate for each stablecoin pair. This is important because the borrowing rates between different stablecoins determine their effective interest rates.

Mint Cash’s unique airdrop mechanism

According to the Mint Cash team leader, holding UST or LUNA before the crash on May 10, 2022; the specified amount of USTC was locked and destroyed through Mint Cash’s airdrop. Both of the above methods are possible. The second method may be to set USTC to 1 USD in exchange for equivalent Mint.

As soon as the airdrop information came out, the price of USTC soared, reaching a maximum of 0.07 USDT. If according to what the project team said, there is still room for growth, but there is a high probability that it will not return to the anchor level. This is just a short-term speculative behavior.

This move by the project side has brought a lot of attention to Mint Cash. As early as early October this year, Mint Cash had already released a white paper, but it was not popular. After this move, the popularity of the project instantly increased.

In fact, we still have some doubts about the airdrop. According to the project white paper, it uses Bitcoin as collateral to generate Mint tokens, which are then exchanged for Cash stablecoins through Mint tokens. However, the airdrop exchanges USTC for the same value as 1 US dollar. Token Mint, does the project need to put in the Bitcoin collateral itself?

But all this will have to wait until the specific details are released. It is expected that the project team will use high interest rates to attract everyone to deposit Bitcoin when it is launched, so as to achieve the frequency of use of Mint to exchange Cash stablecoins.

To sum up, USTCs rise may be just a flash in the pan. But will the operation of the Mint Cash project team be the future method of currency issuance of the Terra ecological project? It is not a possibility that this move will bring TerraUSD back on track.

Back to the Mint Cash project itself, its mechanism design is relatively complete and its risk resistance is relatively high. Although this operation has increased the popularity of the project, long-term stability requires the support of the ecosystem behind it. The project has not yet been officially launched, and everything is possible variable.