Fidelity: Feasibility Study of Ethereum as a Digital Asset and Potential Profit Asset

Original Title: Ethereum Investment Thesis: Ethereum's Potential as Digital Money and a Yield-Bearing Asset

Original Author: Fidelity Digital Assets Research

Original Translation: Biscuit, bayemon.eth, ChainCatcher

Abstract

Users can gain practicality from various applications within the Ethereum ecosystem.

Some may ask, "How does practicality translate into value for Ethereum tokens?" In other words, why should investors buy and hold Ethereum tokens instead of solely interacting with the Ethereum network? In our previous article introducing the Ethereum network, we only briefly considered how or why Ethereum tokens have value. In this article, we will explore this question in more depth from an investment perspective and provide a brief introduction to some technical issues.

Main points of this article:

Ethereum can be understood as a technical platform with ETH as a means of payment.

The perceived value of Ethereum is closely related to the supply and demand dynamics of network applications, which have changed significantly since The Merge.

The overall platform usage of Ethereum may transmit value to token holders, meaning that the value of tokens increases with the increasing usage of the Ethereum network and platform.

The investment concept of holding Ethereum is similar to Bitcoin, namely, holding it as a new form of currency.

However, due to the characteristics and network effects of Bitcoin, it is unlikely for other digital assets to surpass Bitcoin and become monetary commodities.

Nevertheless, value is subjective, which does not mean that other competing forms of currency, including Ethereum, cannot exist, especially in specific markets, use cases, and communities.

We will study Ethereum's ability to fulfill the two main functions of currency: the store of value and means of payment.

Currently, Ethereum is not a perfect network and is expected to be upgraded annually, which brings frequent technical risks and unknown variables, thereby reducing its prospects. These unknown factors weaken Ethereum's prospects as a store of value asset.

Although Ethereum can be used for various payment purposes, the instability of its fees remains a barrier to widespread adoption.

We have studied the demand model of Ethereum and found a small relationship between address growth (a measure of adoption rate) and price. Compared to Bitcoin, there is a smaller correlation between address growth (a measure of adoption rate) and price of Ethereum.

After Ethereum switched from PoW to PoS, token holders can now earn returns, with part of the returns coming from the increased network usage. We will study the sources of these returns, as well as various driving factors and risks.

As an income-generating asset, the value of Ethereum can be tested using a cash flow discount model. We have built a simple model to illustrate the assumptions driving this model.

Ethereum and Ether

There is a certain relationship between the digital asset network and its native token, but the "success" of the two is not always completely correlated.

In some cases, the network can provide utility to users, settling a certain number of complex transactions every day, but this does not bring incremental value to token holders. There may be a closer relationship between network usage and token value in other networks. A commonly used term to describe the relationship between network design and token value is token economics, which helps explain how the design of a network or application creates economic value for token holders.

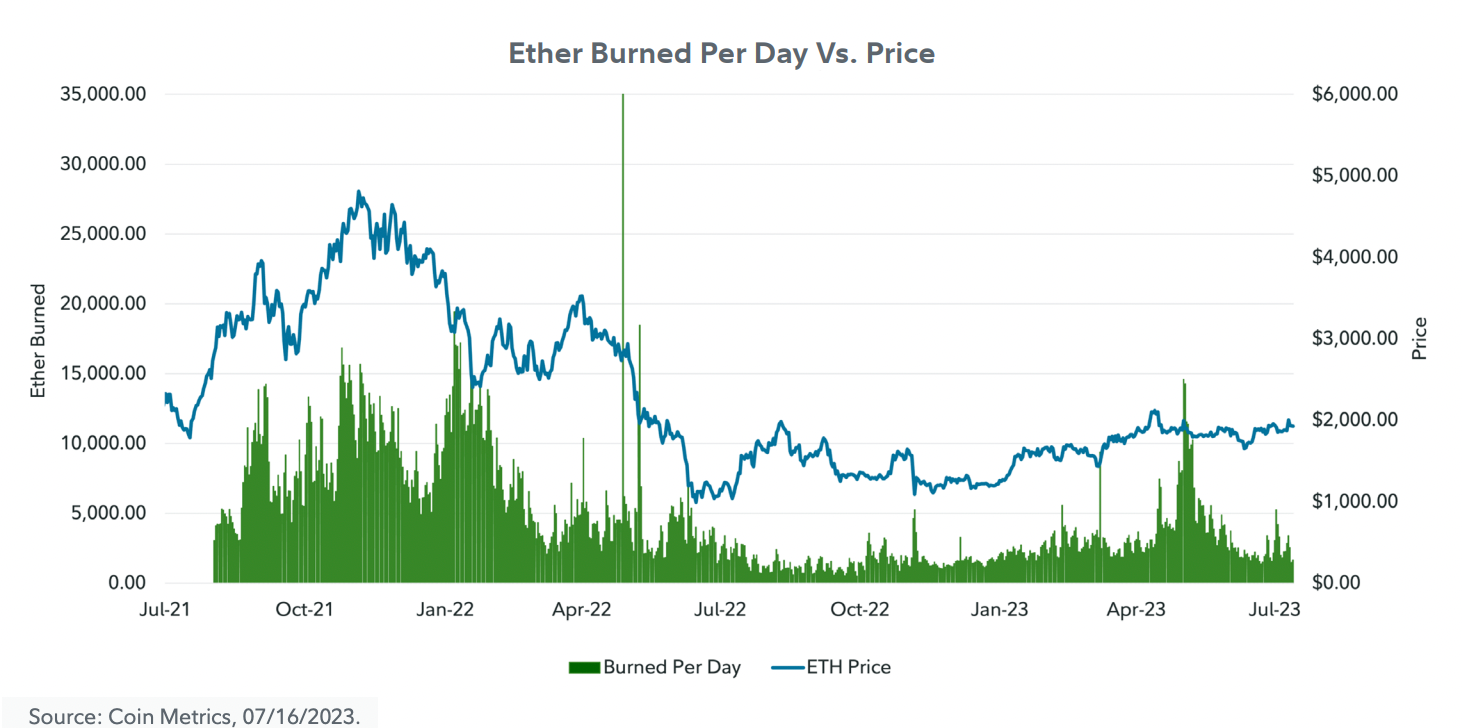

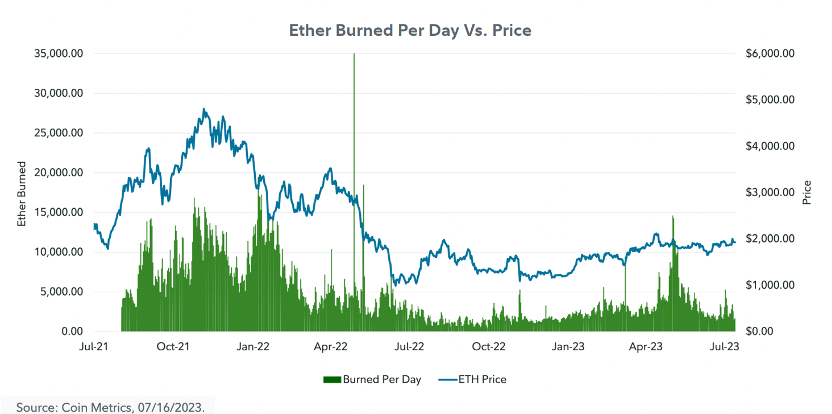

The Ethereum network has undergone significant changes in recent years, which have also led to changes in Ethereum's token economics. In August 2021, the Ethereum Improvement Proposal 1559 (EIP-1559) introduced a mechanism to burn a portion of transaction fees, known as the base fee. Burning Ether, or any other coin, means destroying it, so executing transactions on Ethereum withdraws Ether from circulation.

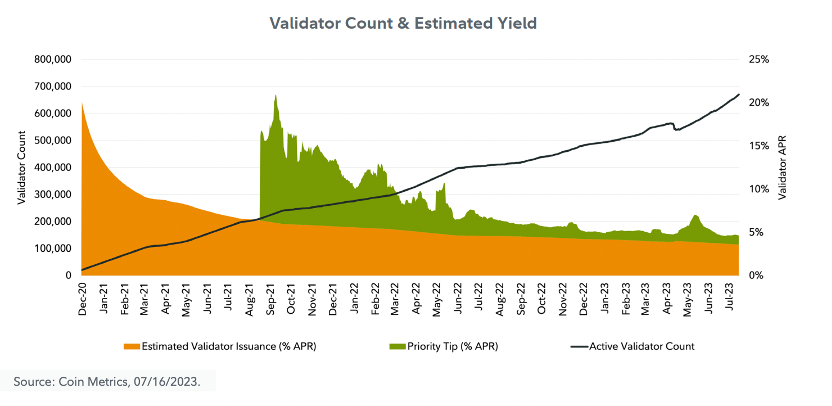

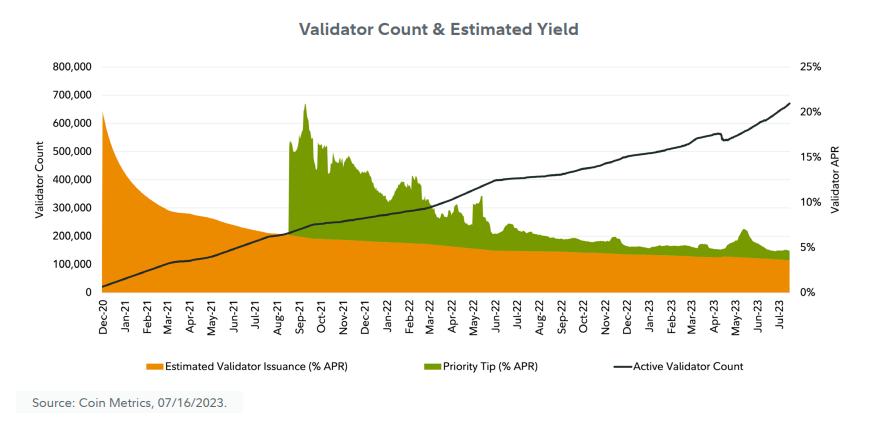

In addition, the transition from Proof of Work (PoW) to Proof of Stake (PoS) in September 2022 reduces the network's token issuance rate and allows entities to earn income through tips, issuance, and Maximum Extractable Value (MEV). The previous upgrades to Ethereum fundamentally changed its token economics and also altered people's perception of the relationship between the Ethereum network and its tokens.

Token Economics: Accumulation of Ether Value

The token economic model of Ether usually involves three ways of converting quantity into value. When conducting transactions on Ethereum, all users need to pay basic fees, priority fees (tips), and generate additional value for other participants through MEV (Maximum Extractable Value), which is the maximum value that validators can obtain by including, excluding, or changing the order of transactions during the block production process. Basic fees are paid in Ether and are destroyed when included in a block (transaction bundle), thereby reducing the circulating supply of Ether. Priority fees are paid to validators, individuals or entities responsible for updating the public ledger and maintaining consensus. When a new block is generated, validators who receive income prioritize the highest priority transactions. Finally, potential MEV opportunities (usually arbitrage) are submitted by different users and most of the value is transferred to validators through the highly competitive MEV market in the current state.

The value accumulation mechanism can be seen as the network's "revenue" being used for different purposes. Firstly, the destruction of basic fees puts deflationary pressure on the total supply, benefiting existing token holders. Secondly, priority fees and MEV come from users and are distributed to validators in exchange for their services. Although these relationships are nonlinear, an increase in platform usage means more destruction and higher returns for validators.

Investment Argument 1: Becoming a Widely Accepted Digital Currency

The common view is that the best way to understand Ethereum is as an emerging currency product. The question raised by this view is whether Ethereum's native token can also be considered as a currency. Simply put, Ethereum may face more challenges in becoming widely accepted as a form of currency in comparison to Bitcoin, which has more advantages. As shown below, Ethereum shares many similarities with Bitcoin and other currencies in many aspects; however, it differs from Bitcoin in terms of scarcity and record history. Technically, Ether has infinite supply parameters that are maintained within a certain range based on the number of validators and the destruction situation. Although these parameters are strictly controlled by the Ethereum network, they do not equate to a fixed supply plan and may experience unpredictable fluctuations based on different directions of underlying components. The historical record of digital assets is not only related to the duration of "creation" but also to the time of "determination". Since Ethereum undergoes network upgrades approximately once a year, the updates and audits of the code take a long time and, more importantly, require the attention of developers to rebuild its history. Although the concept of the probability guarantee of code execution over time is specific to digital assets, it is undoubtedly crucial for gaining the trust of stakeholders.

Many viewpoints believe that Bitcoin is currently the safest, most decentralized, and most robust digital currency, and any "improvements" need to be weighed, so there are few other digital assets that can surpass Bitcoin in the aspect of "currency products". Although network effects are crucial in the blockchain ecosystem, Bitcoin, as a currency commodity, has a seemingly "unbeatable" position in this regard. However, this does not mean that other forms of currency cannot exist, especially for different markets, use cases, and communities. More specifically, there are no use cases in the Bitcoin ecosystem that can be achieved on the Ethereum network, such as facilitating more complex transactions and giving it a unique, currency-like utility, which should be included in comprehensive considerations. Although Ethereum is commonly used to transfer value between addresses, its role as a user executing smart contract logic is what sets it apart as a token.

The physical world and the digital world seem to be converging. As we see from leading tech companies, an application that provides unique services to users will bring network effects and demand. Mainstream applications widely used on Ethereum naturally lead to increased demand for Ether, which is why this long-term trend may be one of the most attractive cases for considering Ether as a potential alternative currency.

In fact, there have been some notable Ethereum integration cases in the cryptocurrency and traditional finance sectors:

MakerDAO purchases $500 million of Ethereum

European Investment Bank issues bonds on the blockchain

House sold in the form of NFT in the United States

Franklin Templeton Money Market Fund uses Ethereum and Polygon to process transactions and record share ownership

The integration of the Ethereum ecosystem with real-world assets has begun. However, it may take many years of improvement, regulatory clarity, education, and time to get the public to start trading on Ethereum or competitive platforms. Therefore, Ethereum may still be a niche form of currency until then.

In addition, regulation is the most controversial topic regarding how Ethereum may shape the future. Although it is a permissionless blockchain, many centralized exchanges that hold and stake Ethereum are located in the United States, which means any guidance provided to validators or investors within that jurisdiction can greatly impact valuation and network status. There have been recent regulatory enforcement actions and the closure of banks and Kraken's staking service related to cryptocurrencies in the United States. Therefore, regulatory risk is one of the most serious obstacles Ethereum may face in the short term.

Ethereum as a Store of Value

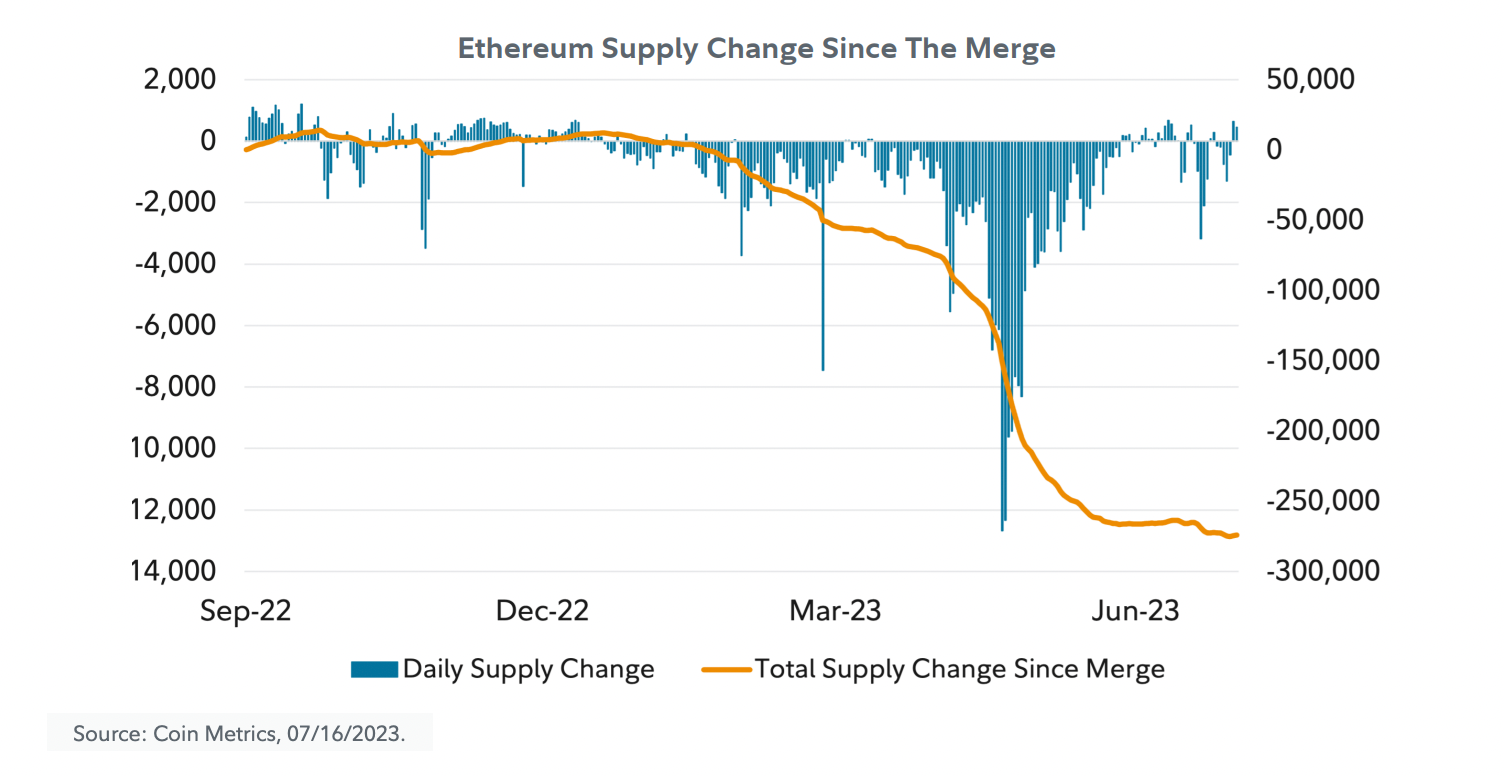

In order to be a qualified store of value, a token needs scarcity or a high inventory/circulation ratio. As of July 2023, Ethereum has a higher inventory-circulation ratio than Bitcoin. Since The Merge, this dynamic has become a focal point, significantly reducing the issuance of Ether as shown below.

We have already elaborated on one of Bitcoin's core value propositions, which is its maximum fixed supply of 21 million Bitcoins, with no supply plan that is unlikely to change. Bitcoin's supply plan is written in its code and implemented through social consensus and incentives of network participants. So how does Ethereum's supply plan work? As mentioned above, rather than calling Ethereum's issuance a "plan," it is more like a balance between a set of parameters. In fact, two variables determine the total supply of Ethereum, making it difficult to assess future supply:

1. Issuance: The issuance of Ethereum is determined by the number of active validators and their performance. As the issuance of Ethereum increases with the total staked amount, the growth rate gradually decreases. Since Ethereum's issuance is linked to the staked amount, this part is less prone to drastic fluctuations. The Ethereum protocol has set limits on the number of validators that can enter and exit staking, aiming to ensure the protocol's security and a stable issuance rate over time.

2. Burning: Since Ethereum blocks can only perform a limited amount of computational work every 12 seconds, the Ethereum network needs to meet the demand for block space through burning. Burning is a highly volatile operation, making it difficult for us to accurately predict Ethereum's future supply. Burning acts as an incentive pendulum, rarely staying the same from one block to another. The protocol specifies the Gas Fee that each block should contain. If a block's gas is higher or lower than the target value, it will cause a correspondingly nonlinear adjustment of the base fee for the next block. When on-chain transactions are highly active, it may lead to drastic fluctuations in transaction fees. Therefore, it also serves as a security mechanism intended to prevent malicious actors from sending unlimited amounts of junk information to the network.

In short, the supply of Ethereum is not based on a fixed plan, and the two components of its monetary policy are likely to change. However, based on the current structure of Ethereum, it can be determined that the total supply of Ethereum will at most result in an annual inflation rate of about 1.5%. This assumes that 100% of the current supply is staked and not destroyed, which means no transactions occur on Ethereum. As shown in the graph, maintaining Ethereum's normal issuance or keeping inflation at a lower level does not require a significant amount of destruction. In fact, higher destruction rates often lead to net contraction or a decrease in the total supply of Ethereum.

Some argue that the future supply of Ethereum is correlated with the number of active validators (issuance) and the demand for transaction execution (destruction), with the latter being relatively unpredictable in the long term. Additionally, upgrades to Ethereum could directly impact the amount of destruction or issuance on the base layer, so the current metrics still cannot effectively predict future supply levels. For example, the Shanghai/Capella upgrade reduces risks associated with staking and may increase the total issuance due to higher staking participation rates. On the other hand, data availability scaling (upgrades aimed at increasing transaction throughput) and the maturation of Layer 2, i.e., independent blockchains built on top of Ethereum, could change the dynamic of destruction and demand in unpredictable ways.

Furthermore, independent Layer 1 public chains with final sovereignty and native tokens still do not have the same level of iteration and development time as Ethereum. As dApps migrate to other Layer 1s and interoperate with other blockchains, investors should closely monitor the transfer of users and traffic. For NFTs or blockchain games, users may not necessarily need the higher level of decentralization and security provided by Ethereum's base layer.

If users are willing to sacrifice certain components of the impossible trinity for scalability, some user-driven value is likely to accumulate outside of Ethereum. Given that the economy of smart contract platforms might inherently be multi-chain, investors should consider which narratives will persist on the Ethereum chain in the long term, and which will exist elsewhere.

Another key factor in distinguishing Ethereum from other on-chain assets is the future upgrades to the supply plan itself. Parts of the roadmap such as EIP-1559 and MEV Burn explicitly indicate the impact that destruction may have on the supply mechanism. While it is still unclear what exact implications these upgrades may bring, Ethereum has already formed a distinct value proposition in terms of its supply plan, which will not change in the long term, in contrast to Bitcoin.

In conclusion, although many believe Ethereum could be the next "supermodel currency," it is still too early to reach such a conclusion under the current unstable supply model of Ethereum. While the usage of the Ethereum platform can deliver value to token holders, the so-called value for Ethereum, which is still in its early stages, is a subjective judgment derived from users.

ETH as a Payment Method

ETH is used as a payment method, but these payments are limited to digital native assets.

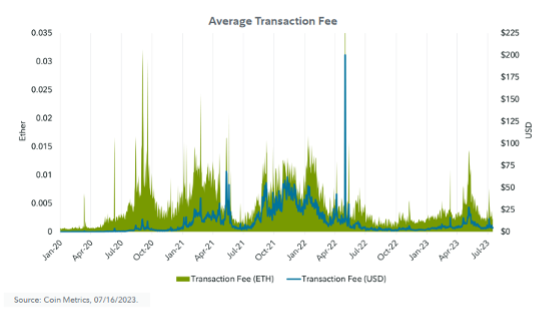

Most Ethereum transactions are typically finalized within 13 minutes, which makes Ethereum settlement faster than Bitcoin's six blocks (one hour) probabilistic guarantee. Ethereum finality means that a transaction is included in a block and cannot be changed without a significant reduction in ETH. This mechanism makes Ethereum attractive for payment assets in terms of final settlement time, but there are still obstacles to overcome in terms of payment usability. The ability to soar is largely due to user experience and persistently high transfer fees.

Note: Reduction refers to the partial destruction of a validator's stake and the mandatory removal of the validator from the network. This occurs in response to dishonest proposals or block proofs in the network.

Since the Ethereum merge, the network fees consumed by NFT payments rank second, only behind DeFi-related transactions. NFTs are priced in ETH and inherently experience price fluctuations. For sellers who sell an NFT for 1 ETH, this amount represents a significant difference in purchasing power, depending on the market price of ETH. This difference can reduce the transaction experience (mainly for the seller) and is a common reference case in many digital asset claim payment use cases.

Although Ethereum has a wide range of transaction scenarios, direct value transfers account for a large portion of network usage; since the merge, the ETH consumed by peer-to-peer transfers ranks third on the leaderboard. The biggest issue affecting Ethereum payment use cases is the volatility of transaction fees. Ethereum's dynamic fee model makes fees easily and dramatically increase. The variable pricing of transactions can limit payment use cases, thus, an unreliable cheap value transfer network reduces the user experience of Ethereum.

Users often need to make these decisions: whether to transact at the current high cost or wait until network activity subsides. This variable forces developers to be creative in maximizing transaction speed and efficiency that meet user preferences.

In addition, if more real-world assets enter the blockchain, the payment of these assets may use ETH, stablecoins, or other tokens. If these innovations are combined with the lower fees provided by Layer 2 platforms, they can create an attractive future for payments on the Ethereum network.

Network data shows that ETH is used as a means of payment. Although it is used for payments of native digital assets, the potential of Ethereum as a payment network has not yet fully peaked due to fees and price volatility that can result in a poor user experience.

With Ethereum developers seeking to optimize the network for future use cases, this concept will permeate throughout the subsequent market analysis. Whether ETH becomes a mainstream payment method will largely depend on how quickly the community can overcome obstacles such as usability, associated real-world assets, as well as secure and low-cost transfer options.

Assessing ETH from a Demand Perspective

As applications on the Ethereum network require payment in ETH, increased adoption of the Ethereum network may result in a rise in ETH prices and an increase in value for Ethereum token holders due to supply and demand mechanisms. Furthermore, as Ethereum scalability progresses, investors should consider reevaluating the demand-side model. Assessing where new users are coming from and the use case trends they are seeking can have an impact on investments.

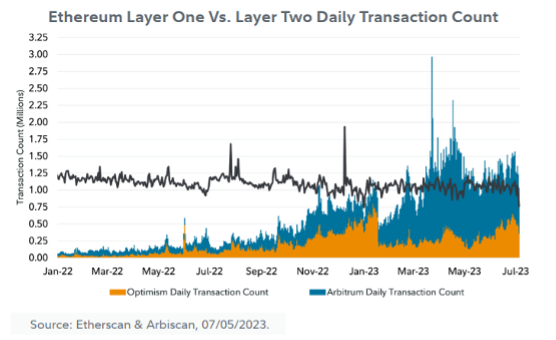

The following figure illustrates the process of value accumulation at the base layer (Optimism), where Layer 2 blockchains conduct transactions and ultimately convert network usage into the value of ETH. Arbitrum, on the other hand, is built on top of the network, handling transaction execution and relying on the base layer for security and transaction confirmations.

Despite being in a bear market, Ethereum's daily transaction volume remains stable at around 1 million, while the price of ETH has already decreased by 52% since the beginning of 2022. Additionally, Layer 2 transaction volume has increased while Layer 1 transaction volume remains unchanged. This may indicate a certain level of stickiness in the base layer, with new demand coming from Layer 2. These signs suggest that even as Layer 2 becomes more mainstream, value will continue to accumulate at the base layer.

Measuring ETH's demand as a monetary asset may be challenging. Metcalfe's Law is a popular economic model that demonstrates the relationship between address growth, representing Bitcoin's demand and price. In comparison to Bitcoin, we find less correlation between ETH demand and price.

In short, if Bitcoin is primarily understood as a sentimental commodity currency, we can reasonably expect a stronger relationship between asset demand measured by address count and price. For ETH, this weaker relationship may indicate that its value is derived from other sources such as network usage rather than simply the demand for holding the asset itself.

Risks of the Demand-side Model

1. Ethereum's core value comes from the usability layer, measured by addresses rather than transactions, volume, or usage. The adoption model fails to effectively capture these relationships.

2. While the data shows a relationship between address growth and ETH price, there is no guarantee that this relationship will persist in the future.

3. This model is only a demand-side model, as discussed earlier, Ethereum's supply schedule may change in the future. Therefore, even with increased demand, if supply also increases, the price of ETH may not change or even decline.

Investment Argument 2: ETH as a Yield Asset

Operating Principles of the ETH Yield Model

Since the implementation of the merge, ETH has undergone fundamental changes. This has not only significantly reduced the network's energy consumption but also provided an opportunity for users willing to lock ETH on the consensus layer to earn yields. This transformation involves proof of stake, a crucial turning point in Ethereum's security model.

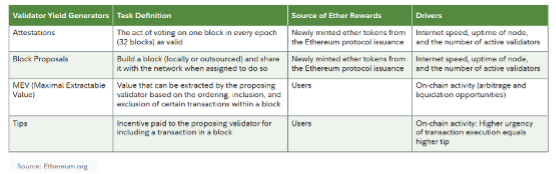

Some may argue that Proof of Stake maintains or even improves network security at a lower cost compared to Proof of Work by punishing inappropriate behavior of validators. Validators contribute resources to the network and fulfill their allocated responsibilities to help Ethereum achieve consensus, and they are rewarded economically for doing so. Below is a brief description of various validator responsibilities and rewards:

Proof of Stake (PoS) is a consensus mechanism used in Ethereum to secure the network and provide economic incentives to validators. In PoS, validators submit attestations or votes once per epoch and propose and validate blocks within 32 slots. These votes contain key data points that indicate the correct content (blocks) for each epoch according to each validator's perspective. These votes are aggregated and subjected to certain rules to determine their validity, allowing the network to achieve consensus on the blockchain and provide economic benefits. The cost of finalizing Ethereum's economic security (i.e., reverting to the finalized chain) is at least one-third of the total value of staked ETH. As of July 2023, this value exceeds $15 billion. This security threshold increases with the value of ETH and the amount of ETH staked.

Block proposal rewards are given to validators who propose blocks. The frequency at which validators propose blocks is relatively low, as there is only one proposer per slot, equivalent to 32 proposers per epoch. The selection of validators is pseudorandom and dependent on their effective balance, which is the amount of ETH that influences reward accumulation. The more ETH one holds, the greater the potential reward. The maximum effective balance for all validators is 32 ETH, and any balance exceeding this amount does not increase the potential reward.

In addition to the value received from the protocol, proposer validators also receive fees paid by users to include their transactions in blocks and MEV (Maximal Extractable Value), which is a mechanism for validators or others to prioritize, include, or exclude certain transactions in blocks based on their value in terms of ordering, inclusion, and information extraction. While the potential rewards from the protocol depend on the number of active validators, the additional income from fees and MEV is directly related to network congestion and activity.

Attestations and block proposal rewards are rewards for minting new ETH from the protocol. These rewards can be seen as incentives for the protocol to maintain its security. The Proof of Stake model minimizes the payment security budget by introducing penalties and significantly reducing deductions. The base reward is equal to the average validator reward per epoch, and the calculation of potential protocol rewards can be done using the following formula:

Base Reward = Effective Validator Balance * (16 * sqrt(Total staked ETH))

The key to this payment structure is that the base reward is proportional to the validator's effective balance, incentivizing validators to stake up to 32 ETH and inversely proportional to the number of validators in the network. As the number of validators increases, the total issuance also increases, but the average reward per validator decreases. The underlying principle of this issuance model is to ensure sufficient participation of validators, as a small set of validators can lead to high issuance events, while also ensuring that unexpected high issuance events do not occur when many validators participate.

This specific token economy allows ETH to sustain real profits. Since the merge on September 15, 2022, until July 2023, 53% of validator income comes from this mechanism. Here are some other forms of income that are not paid by the protocol but by users, which provides interesting connections between network usage and validators.

MEV (Maximal Extractable Value):

MEV comes directly from user transactions, as increased user activity often creates more opportunities to profit from such activity. As Ethereum has multiple use cases, value can be extracted from user transactions in various ways. Flashbots, an organization dedicated to reducing centralization effects in MEV, states that the most common form of MEV usually comes from arbitrage and liquidations, which thrive in highly volatile environments like in November 2022.

MEV-Boost is a program that aims to outsource the role of building blocks to specialized participants, so that MEV-related rewards can be shared across the entire set of validators. Since the merge, most validators have been using this program. On November 7, 2022, validators using MEV-Boost and Flashbots relays received an average reward of 0.1 ETH per block. Due to the multi-chain liquidations and intense network activity following that day, by November 9, 2022, the average block reward skyrocketed by nearly 700% to 0.68 ETH per block. This rapid growth demonstrates the close relationship between network congestion and validator earnings. During periods of high volatility, on-chain activity surges, incentivizing users to speed up execution with higher fees and increases the amount of capturable MEV.

Although the relationship between MEV opportunities and validator earnings remains strong as of July 2023, many different applications, organizations, and individuals within the Ethereum community are exploring ways to change how MEV is managed. As proposed in Flashbots' recent release of MEV-Share, many of these efforts are focused on returning MEV to the users who generate it.

Other solutions include destroying user-created MEV or encrypted transaction data, so that MEV becomes more valuable and harder to capture. Whichever route the community chooses, it may have a significant impact on MEV-related earnings, as of July 2023, MEV has accounted for around 24% of validator revenues since the Ethereum merger.

Unlike application-specific chains, Ethereum has a wide range of available MEV types, which may continue to grow as functionality improves. This difference suggests that one solution may not be sufficient to reduce all MEV.

Tips:

Since the introduction of EIP-1559 with the Ethereum "London" upgrade in 2021, the fee market in Ethereum has undergone significant changes. Prior to the upgrade, proof-of-work miners received all Gas fees from any transactions included in the blocks they mined. Due to changes in the fee market, there are now two different types of fees in the network: base fee and priority fee (tip). All fees are still paid by the users attempting to execute the transactions; EIP-1559 affects the allocation of these fees after payment.

Validators only collect the priority fee, not all the fees paid by users. Base fees are burned or taken out of circulation. Tips can incentivize validators to prioritize including transactions in their blocks, otherwise validators might package empty blocks (which is more economically viable). For users who need to execute transactions urgently, higher tips compared to other competing transactions in the mempool can incentivize validators to give them priority inclusion.

Note: The mempool (memory pool) is equivalent to a list of pending transactions, including block transaction events that are about to be executed.

While MEV plays an important role in determining which transactions are included in each block, tips still serve as an incentive mechanism as validators decide which transactions to include in their blocks based on tips. Since the transition to proof-of-stake, as of July 2023, tips have accounted for 22% of all validator revenues.

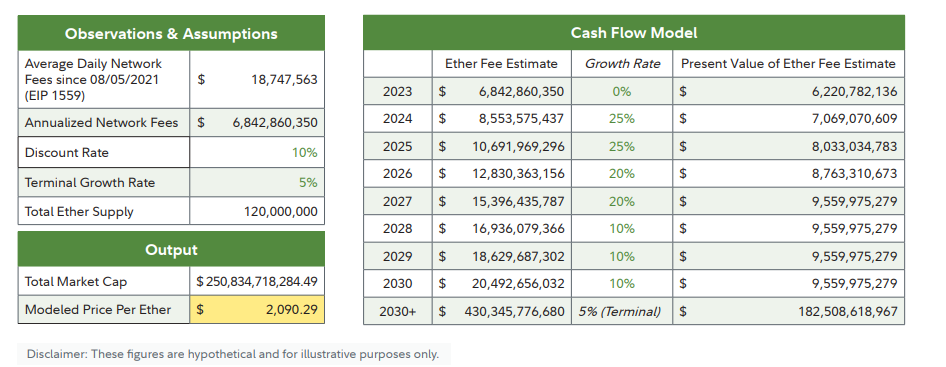

ETH Valuation Based on "Discounted Cash Flow" Model:

With the shift towards proof of stake, it becomes easier to calculate the value of ETH through modeling. The demand for block space can be measured by transaction fees. These fees are either burned or transferred to validators, thereby accumulating value for ETH holders.

Therefore, in the long run, fees and the growth of Ether's value should be inherently correlated. The increase in use cases for Ethereum has created greater demand for block space, which has resulted in higher transaction fees and validator rewards.

We will use a simple discounted cash flow model to demonstrate this relationship. The results of this model can vary greatly depending on growth assumptions and discount rates, similar to cases with high-growth cash flow models. Building such a model is not intended to provide an estimate of the fair value of Ethereum, but rather to describe the relationship between network usage and value accumulation. Additionally, it can also provide further modeling and analysis of ETH value based on estimates of future fees paid to Ethereum equity holders.

The chart below shows the average daily fees paid in USD for Ethereum since the implementation of EIP-1559 in August 2021. The chart is calculated using a two-stage discounted cash flow model, with an initial phase of high fee growth followed by a decrease in the fee growth rate, suggesting that regardless of the utility Ethereum users gain, scaling could potentially lower the upper limit of fee growth.

These are the assumed growth rates for all years after 2030. Such results are common when forecasting the future of high-growth ventures. It is important to note that discounted cash flow models are only theoretically useful.

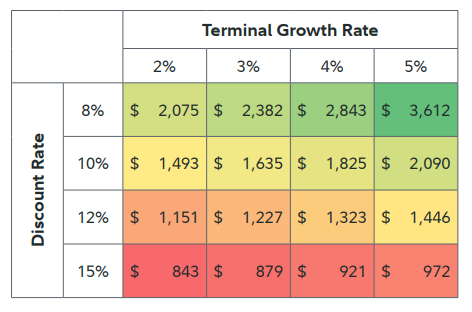

The chart below further illustrates the relationship between modeled prices, assumed growth rates, and discount rates using a sensitivity model. Understanding the relationship between Ethereum's growth and users' willingness to pay fees is crucial. However, models that rely on small changes in future growth assumptions can be highly sensitive and may not be very useful.

Risks of the discounted cash flow model:

If scaling technology reduces fee revenue, the relationship between ETH and the value it provides to network users may weaken unless transaction volume increases and offsets this compressed profit.

Modeling the future of any growth-sensitive asset and applying relevant discount rates is highly subjective, thus valuations may only be theoretically useful.

Ethereum community is making efforts to improve user experience and minimize the negative impact of MEV, which may decrease the output. This aspect has not been adjusted or considered in the model, along with other minor details that may have an impact.

Conclusion

Undoubtedly, Ethereum is a leading blockchain technology platform that enables developers to build decentralized applications. Due to Ethereum's outstanding programmability, many applications are able to achieve things that are not possible on the Bitcoin network. This has allowed the Ethereum ecosystem to host the largest and most active applications in the crypto field, with ETH maintaining its position as the second-largest cryptocurrency by market capitalization.

However, the question posed by investors is, "Will the increase in developer and application activity translate into value for ETH?" We believe that current theory and data indicate that the increase in activity on the Ethereum network drives the demand for block space, which in turn generates cash flow for token holders. However, it is equally evident that these different drivers are complex, nuanced, and subject to change over time as various protocol upgrades and expansions, such as Layer 2, emerge and may change again in the future.