GLP War Guide: Is the GMX ecology a clever combination of matryoshka dolls or DeFi Lego?

Original title: "The complete guide to GLP wars"

Authors: Henry Ang, Mustafa Yilham, Allen Zhao & Jermaine Wong, Bixin Ventures

Real Yield (Real Yield) is considered to be the purest form of income that people can find on the chain. It does not rely on excessive token release, but relies on the fees and income generated by the actual transaction of the agreement. This sustainable benefit is extremely attractive to DeFi farmers if the protocol chooses to share the profits with users.

GMX is a representative project that generates real income. As a popular perpetual trading platform, GMX uses GLP as the liquidity of the transaction, and 70% of the losses incurred by user transactions and platform fees will be allocated to LPs and GMX Token holders in the form of ETH or AVAX. In other words, as one of the largest fee generators in the DeFi protocol, GMX distributes most of the fee income to stakeholders.

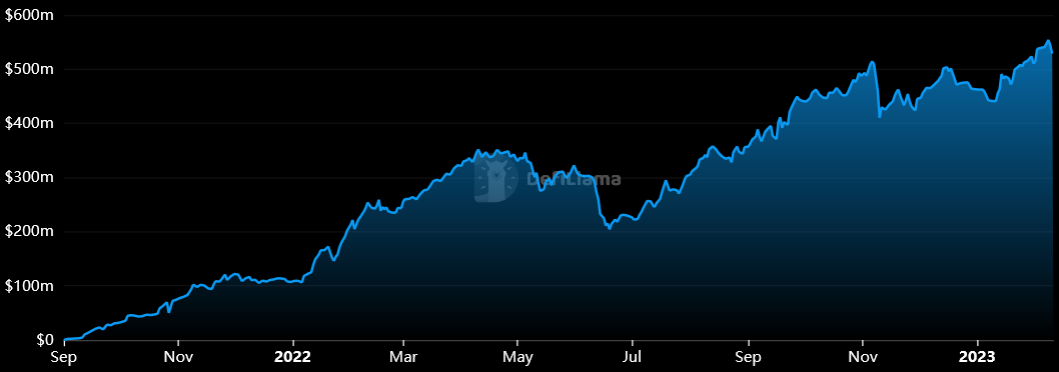

Figure 1: Fees generated by DeFi protocols on February 11

Since the launch of GMX, the market demand for GLP has skyrocketed. At present, the total value of locked assets locked by GMX exceeds 500 million US dollars, and it has been growing. The real income narrative triggered by GMX has also been sought after by more and more people. Developers began to build projects on top of GMX, and attracted GLP share, GLP War follows.

first level title

The Cause of the GLP War

Before understanding GLP War, let's briefly sort out GMX and GLP.

GLP is a LPs liquidity pool similar to Uniswap. It is composed of a basket of tokens as shown in the figure below, of which 48% are stable coins and 52% are composed of other currencies. Due to price fluctuations of BTC, ETH and other currencies , the overall value fluctuates accordingly. Users are incentivized to stake GLP to profit from traders' losses while earning esGMX and sharing 70% of the platform's transaction fees.

Due to market risks, GLP stakers may also suffer losses while gaining profits. The chart below compares GLP's returns to earnings. Since inception, GLP has returned -13%.

Figure 4: GLP returns

first level title

beginning

The various agreements have noticed the problems of GLP and proposed solutions, such as what happens if the risk exposure of GLP is hedged? What happens if the yield is leveraged? What if earnings could be reinvested automatically? What if GLP could be used as collateral? Developers began to look for breakthroughs, and GLP War followed.

first level title

secondary title

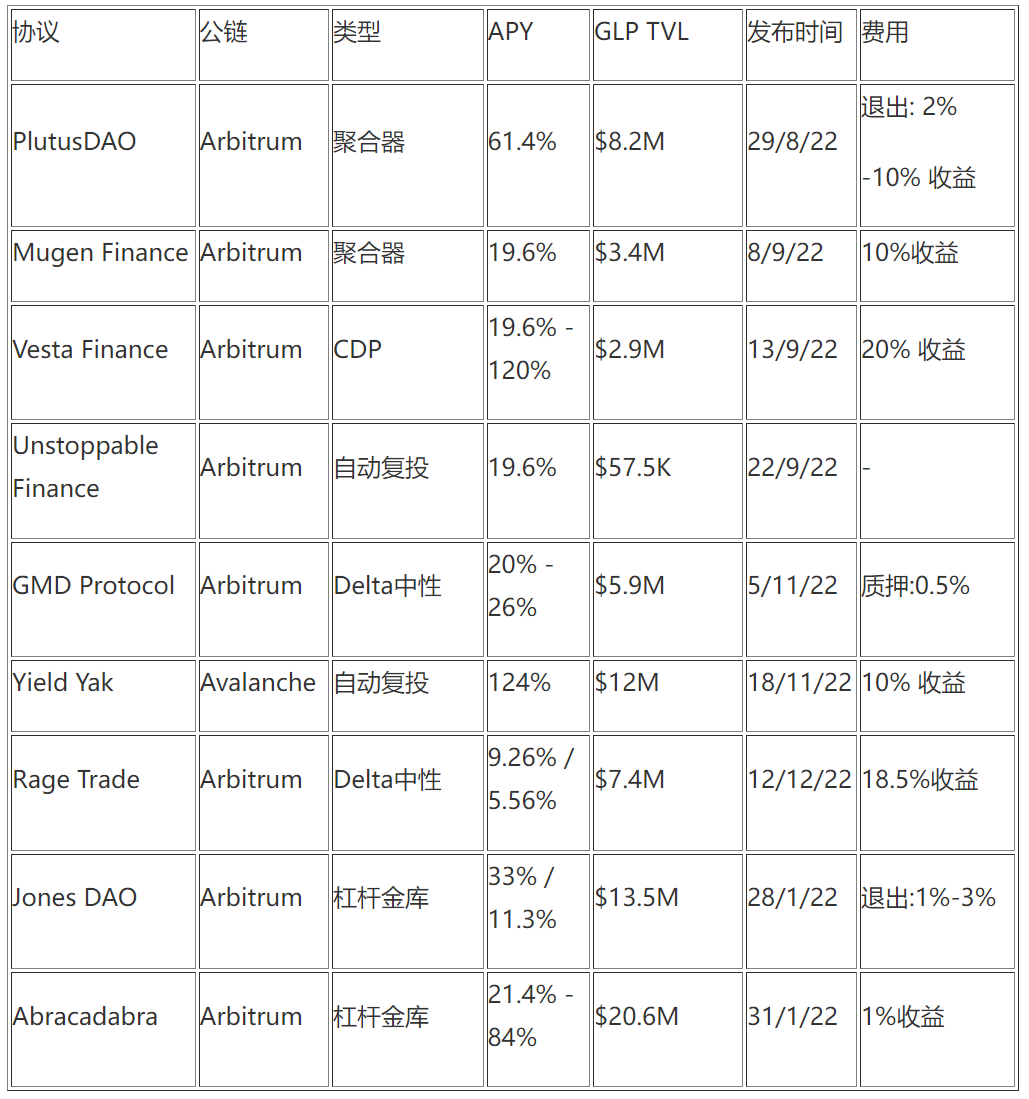

PlutusDAO

PlutusDAO is a revenue aggregator with protocol governance through the native token PLS. It provides liquid staking for veAssets such as veJones, veDPX or veSPA. After integrating GLP, users can deposit GLP to unlock plvGLP with greater functionality.

With plvGLP, ETH rewards will be calculated automatically every 8 hours. Due to automatic reinvestment, the value of plvGLP increases and holders receive higher APY. PLS tokens are also distributed to plvGLP stakers as liquidity mining rewards. Plutus charges 10% of GLP revenue as a fee.

herehereThe relevant strategies are introduced in detail.

secondary title

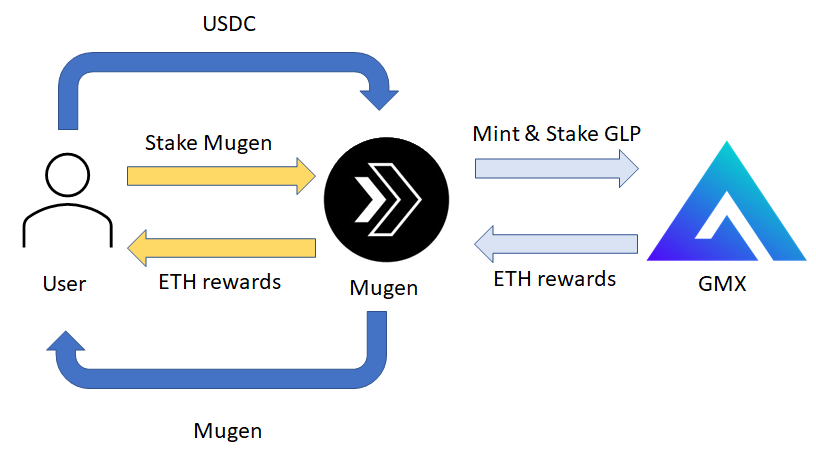

Mugen Finance

Mugen Finance is one of the earliest projects on GMX. Mugen is a cross-chain revenue aggregator built on LayerZero. Users can benefit from multiple agreements on multiple chains, which can be regarded as Yearn Finance on LayerZero. Currently, there is only one strategy on their platform, the GLP strategy.

The GLP strategy is executed by Mugen's treasury according to the amount of whitelisted funds for the strategy, and the treasury earns income by minting and staking GLP. Users who deposit funds into Mugen will mint the native token MGN, and Mugen pledged in the form of xMugen will receive ETH benefits from the treasury. Users can choose to automatically reinvest the income, and use the ETH income to purchase MGN and mortgage it. This helps improve APY because automatic rerolls occur more often than manual rerolls.

Mugen's strategy, while relatively basic, offers farmers a variety of options and automatic reinvestment of returns. In the future, Mugen will integrate more protocols, and users only need to pledge MGN to obtain income from multiple sources and chains.

secondary title

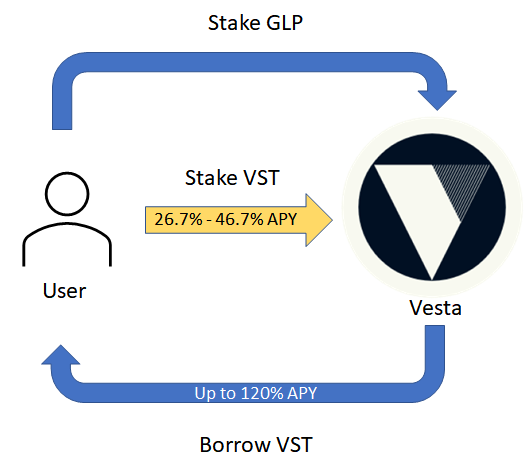

Vesta Finance

Vesta Finance is a collateralized debt platform where users can lock up collateral and mint Vesta’s stablecoin, VST. GLP is one of the collaterals accepted by Vesta, which adds new usage scenarios for GLP for users. Users can deposit GLP and borrow VST to maximize capital efficiency.

VST can be mortgaged in Vesta's mining pool, and a stable currency rate of return of 10-40% can be obtained depending on the lock-up period. When the mortgage rate is 150%, the yield of VST will be 6.7%-26.7%. Overall, without any direct exposure, the GLP yield could improve to around 46.7%.

Vesta also allows leverage on GLP yields. Similar to Degenbox, users can deposit GLP to get a VST loan, which can then be used to buy more GLP. This process is repeated multiple times to obtain a larger leveraged position. With a 120% collateralization ratio, a 6x leveraged position is possible and the APY would be nearly 120%.

Figure 7: GLP Yield Leverage Operation Diagram

However, this strategy can be affected by fluctuations in the price of assets such as BTC and ETH, creating liquidation risk. Risk DAO hasa great articlesecondary title

Unstoppable Finance

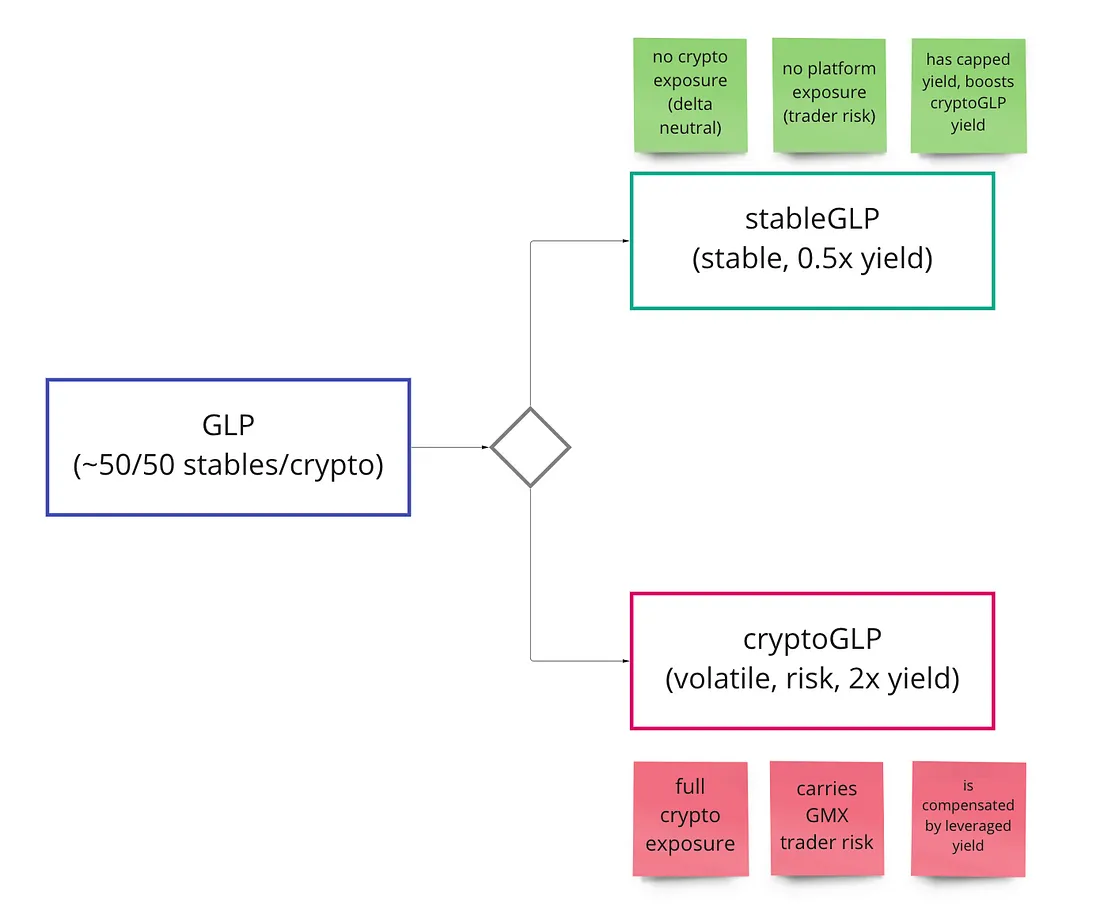

Unstoppable Finance provides GLP holders with a completely free automatic reinvestment tool. Compared with other protocols that charge a certain percentage of fees based on earnings or deposits, using the automatic reinvestor does not charge any fees, so users can save gas costs. The protocol's vaults are built using the ERC-4626 tokenized vault standard, and anyone can build on top of their vaults.

They also have a new mechanism called TriGLP still in development. The mechanism tokenizes GLP into stableGLP and cryptoGLP, earning different amounts of rewards based on the risks they take. Their goal is to create a delta-neutral stablecoin-like position with ~10% pa and not be subject to volatility; and a cryptocurrency-like position with ~30% pa while maintaining full ETH/ BTC exposure.

secondary title

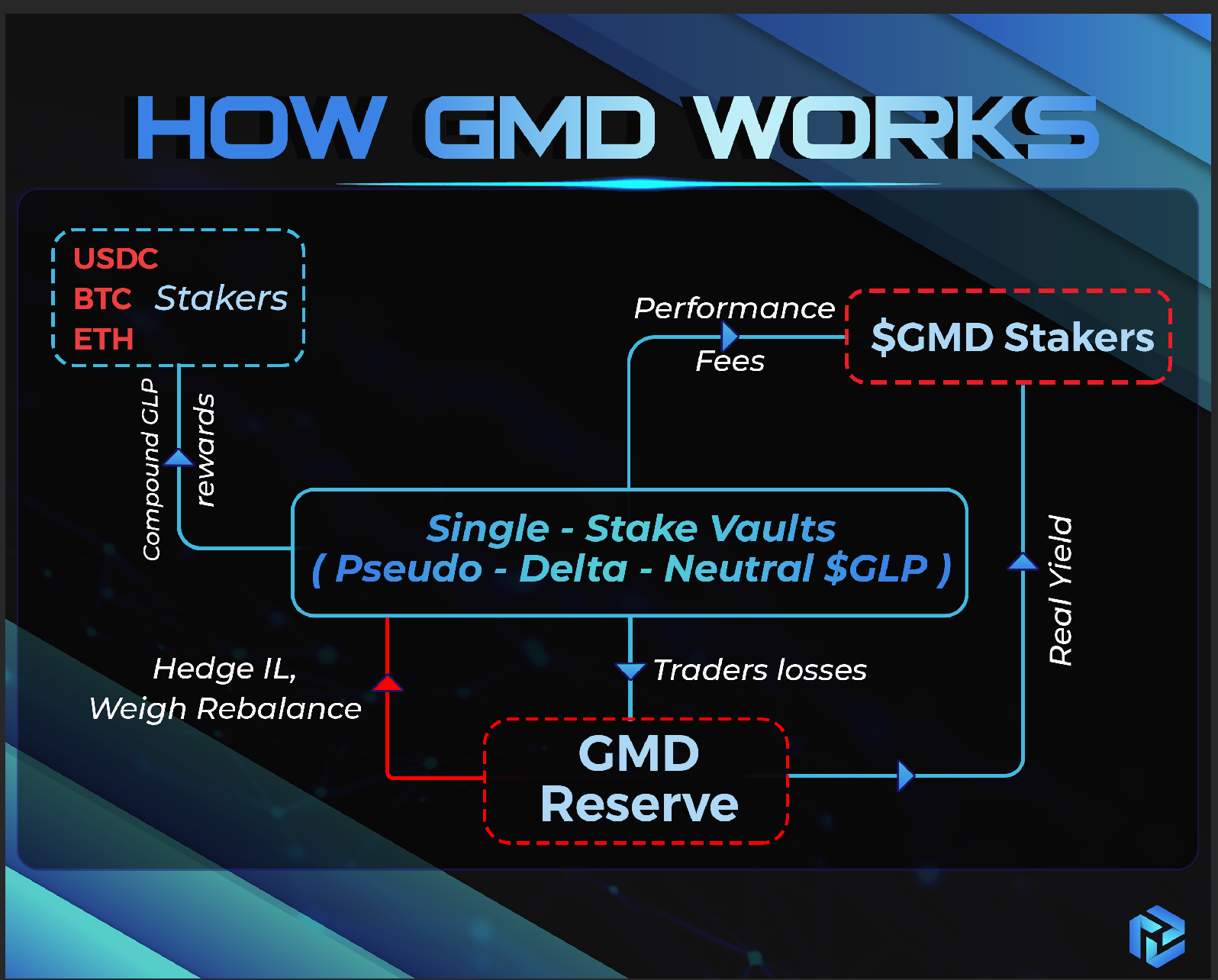

GMD Protocol

GMD Protocol is another yield aggregator that offers additional functionality, mitigating the problem of direct exposure to GLPs by offering the pseudo-delta-neutral strategy.

GMD provides a single collateral vault for BTC, ETH, and USDC, with deposit limits based on the relative ratio of GLP to USDC, ETH, and BTC, and assets in the vault are used to mint GLP and earn yield. This allows users to maintain pseudo delta neutrality to their deposited assets. For example, a user who wants to earn yield on USDC without exposure to BTC, ETH, or other tokens in GLP can deposit funds into GMD’s USDC vault to earn a portion of the GLP yield. This pseudo-delta-neutral strategy uses a GLP-based ratio consisting of USDC, ETH, and BTC.

Over time, the amounts allocated to the 3 vaults on GMD will need to be manually rebalanced weekly to adjust to the new GLP ratio. The GMD protocol does not rebalance user funds, but it does rebalance by depositing 5-15% of the maximum total value in Delta-Neutral Vaults. This helps alleviate the low reserve issue, since the protocol itself has liquidity to draw from.

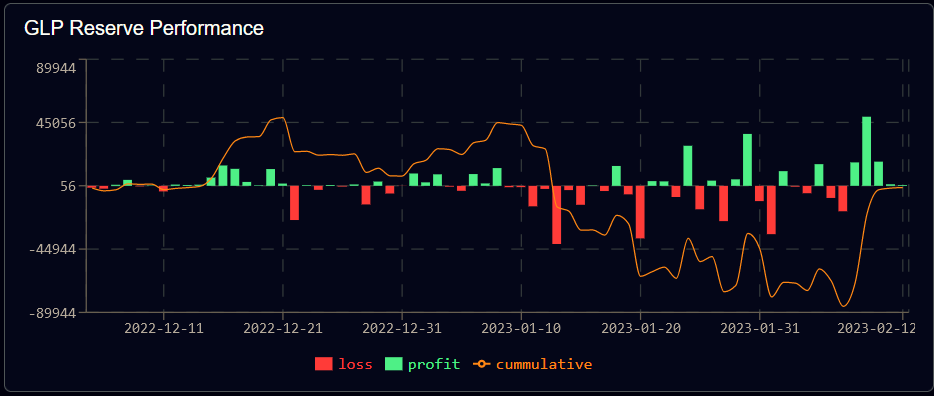

In order to further reduce the volatility risk of smaller assets such as Uniswap in GLP, GMD provides a protocol reserve, which contains GLP with a value of 5%-15% of the total TVL. The protocol reserve is funded by the treasury and will be compensated to users when the value of their assets falls below the value of GLP. GMD believes that the protocol reserve will only grow in the long run as it gains value from the losses of GMX traders.

Figure 9: GMD working mechanism

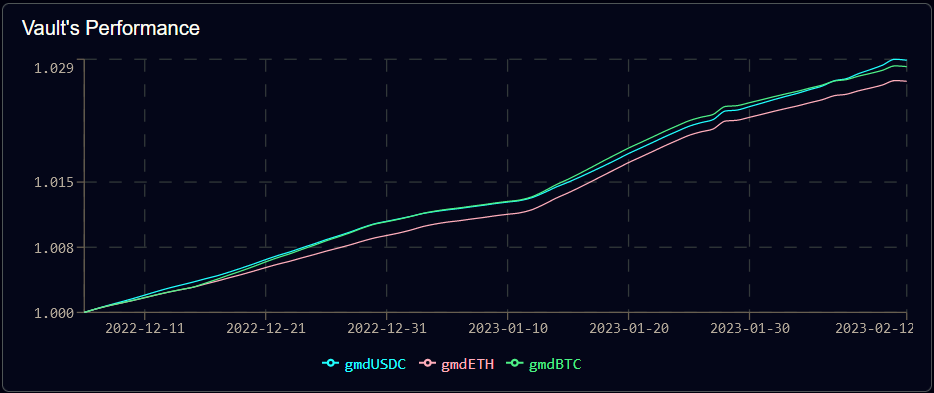

In terms of actual performance, the 3 vaults have yields of 2.6%-2.9% for the period from December 11, 2022 to February 12, 2023. Extrapolating from these results, the APY is approximately 16.6% - 18.7%, which is slightly lower than the advertised 20% - 26% APY.

Figure 10: GMD Vault Performance

While GMD attempts to remain delta neutral, it does not have any short exposure to remain truly delta neutral. The protocol itself requires reserves as backing for impermanent losses. This limits the scalability of GMD as the treasury cannot grow too large without sufficient reserves (i.e. 5%-15% of TVL). They can only scale to a larger TVL based on the performance of the protocol reserves. With GLP reserves at breakeven so far, GMD will be limited in expanding its coffers.

secondary title

Yield Yak

Yield Yak is an Avalanche-based automatic reinvestor. Every user can get compound rewards from AVAX as long as they click to reinvest. This mechanism is an incentive for users.

secondary title

Rage Trade

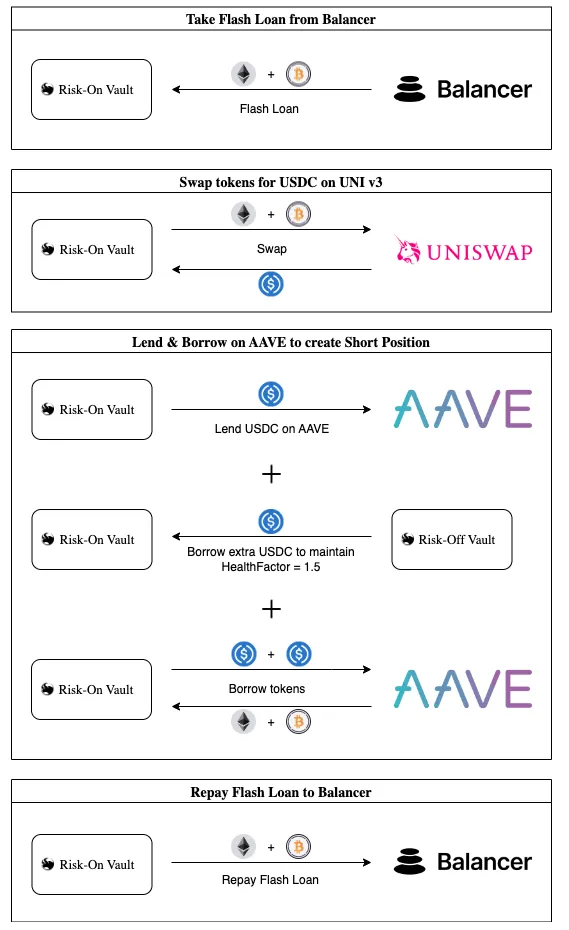

Rage Trade is a perpetual trading platform on Arbitrum that utilizes LayerZero underlying. They are the first project to launch a dual-vault system to minimize direct market risk, with two vaults, Risk-Off Vault and Risk-On Vault, to minimize BTC and ETH by operating on Aave and Uniswap risk exposure.

Users deposit sGLP or USDC into Risk-On Vault, which lends BTC and ETH through flash loans on Balancer, and sells them into USDC on Uniswap, and the USDC obtained from the sale together with USDC from Risk-Off Vault will be deposited into AAVE Then lend BTC and ETH, and these BTC and ETH will be used to repay Balancer's flash loan. These actions would have created a short position on AAVE, as the Risk-On Vault is now borrowing BTC and ETH.

Another important feature of Risk-Off Vault is to provide collateral for Risk-On Vault, which will be used to maintain AAVE's borrowing health factor of 1.5. Every 12 hours, the position is reopened for fees and PnL is rebalanced between shorts on AAVE and GLP collateral, and hedges are rebalanced based on the composition of GLP deposits.

Figure 12: Risk-On Vault mechanism

Figure 13: Risk-Off Vault mechanism

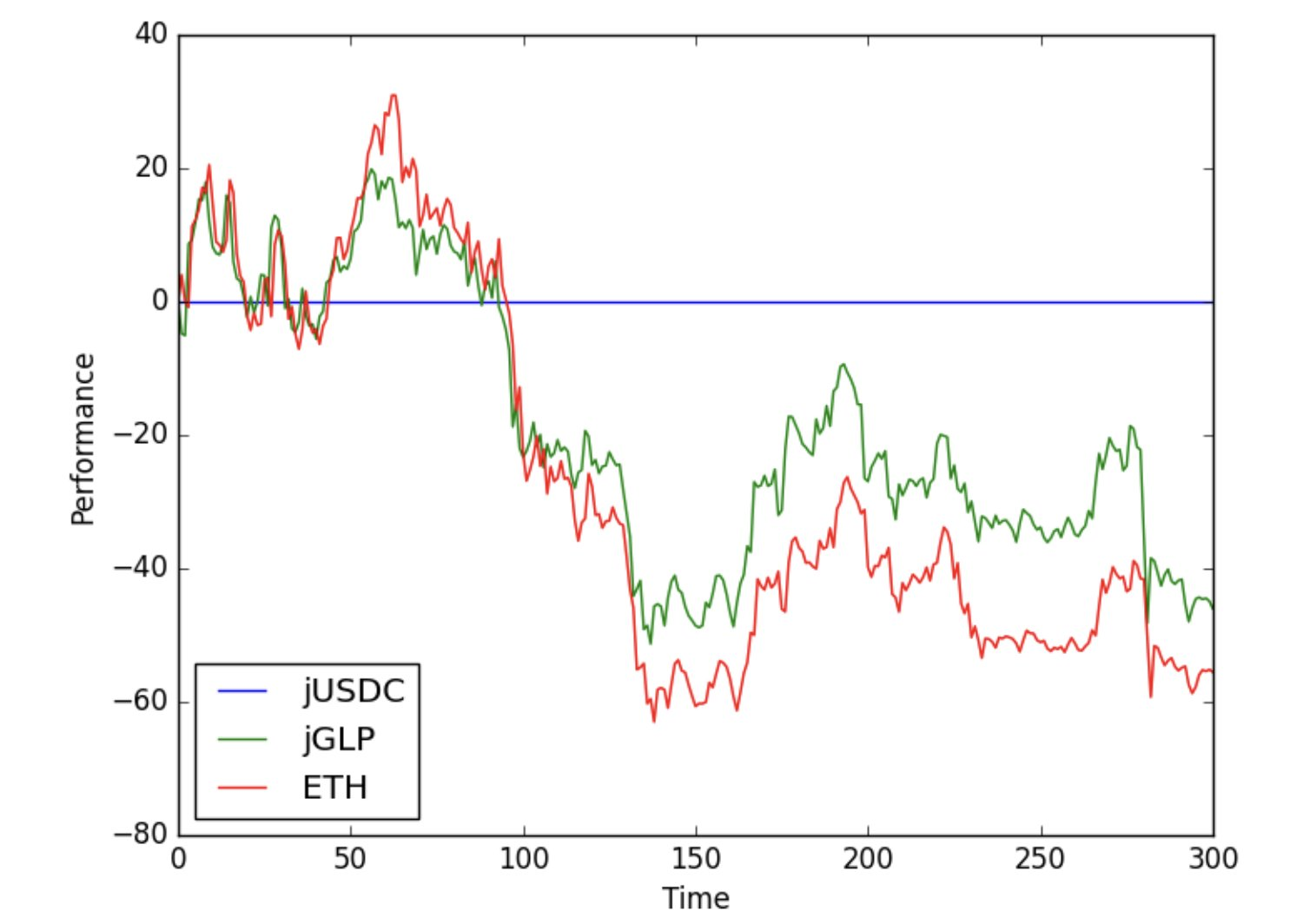

Comparing Risk-On Vault's return performance with GLP's, it theoretically has a profit return of about 25% versus -13% for GLP.

Figure 13: Comparison of Treasury Yield Performance

secondary title

Jones DAO

Jones DAO is a yield, strategy and liquidity protocol designed to improve capital efficiency. Relying on the dual vault mechanism to provide users with leveraged income, Jones DAO's jGLP vault allows the storage of GLP and any assets within GLP, and the jUSDC vault accepts USDC deposits.

USDC from the jUSDC vault can be used to mint more GLP and gain leveraged positions in GLP. The GLP rewards are then split between jGLP and jUSDC depositors, who earn 33% and 11.3% annualized returns, respectively. The jGLP vault will automatically balance its leverage to prevent liquidation, and users can also choose to automatically reinvest.

Figure 14: The protocol mechanism of Jones DAO

The fee structure of Jones DAO is as follows. They have established a unique fee structure for long-term growth. Users who continue to stake will receive fees from users who unstaked, encouraging users to continue staking in Jones DAO.

Figure 15: Fee Structure

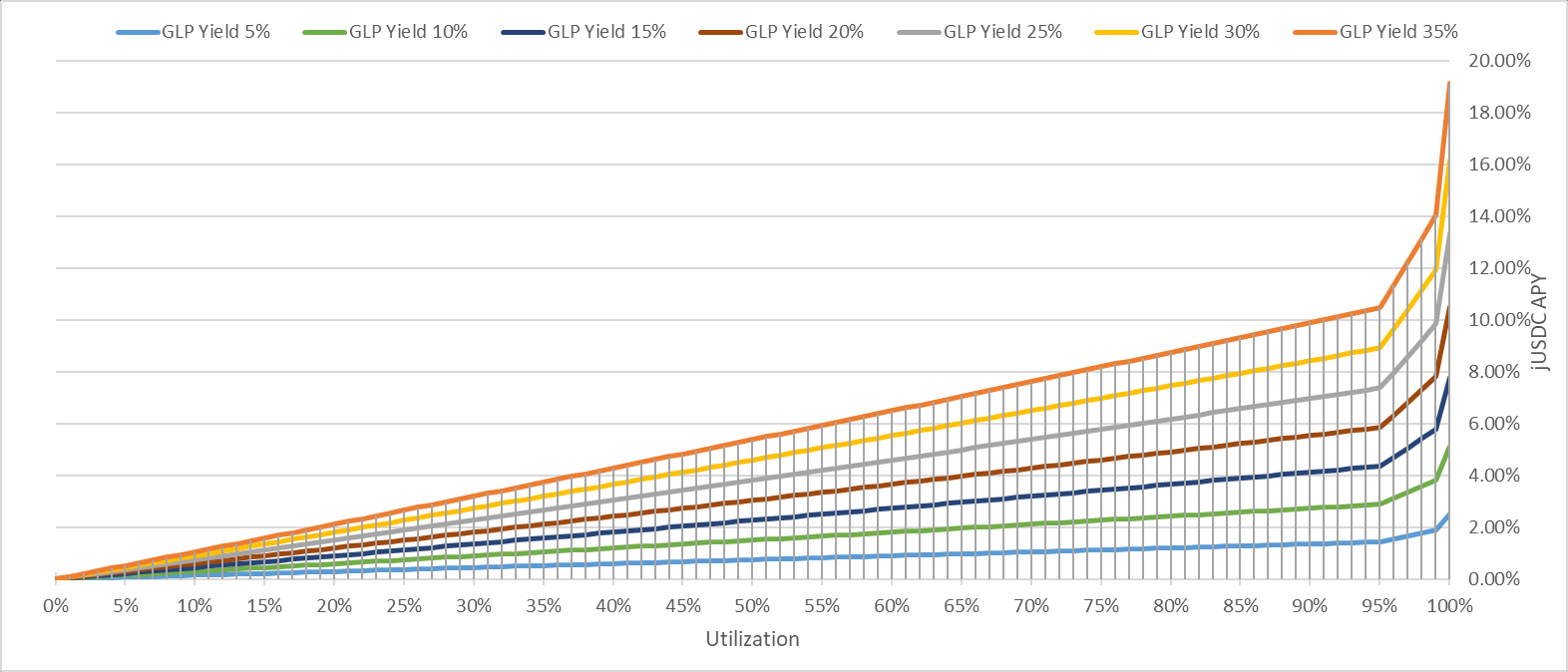

The more USDC deposited into a jUSDC vault, the more GLP can be purchased, resulting in higher leverage. The chart below shows jUSDC APY vs. vault utilization, where GLP yields 35%, and jUSDC yield can rise to nearly 20% due to increased leverage.

Figure 16: jUSDC APY vs. Vault Utilization

In terms of return performance, jGLP does not hedge market risk, it actually magnifies it. This means that the actual performance of jGLP vaults depends on market conditions. Backtesting against 0% GLP yield and 80% utilization shows that jGLP outperforms ETH. Results could have been better if GLP production had been included.

secondary title

Abracadabra

secondary title

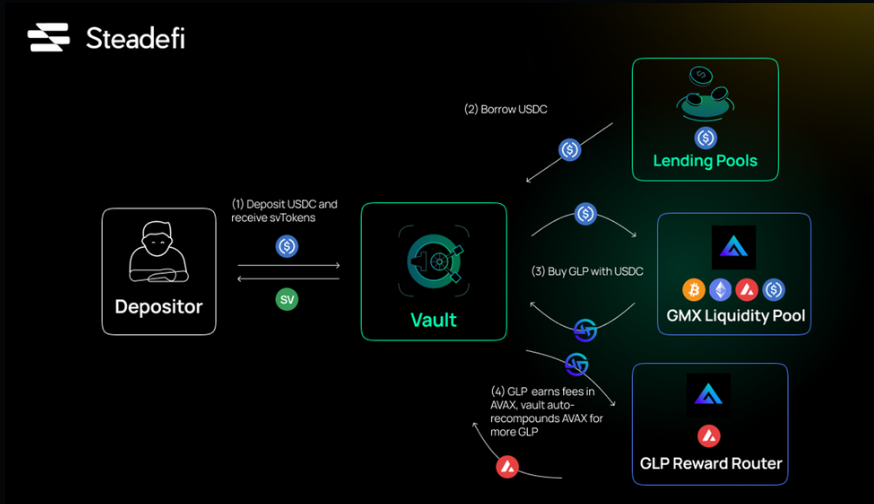

Steadefi

Steadefi is a platform that provides strategies for automatic return leverage, and they currently have a vault that can provide 3x GLP leveraged positions.

For every $1 a user deposits into the vault, $2 is borrowed from the lending pool to mint GLP. This effectively creates a 3x leveraged position that is automatically reinvested over time and rebalanced when necessary.

Figure 18: Steadefi mechanism

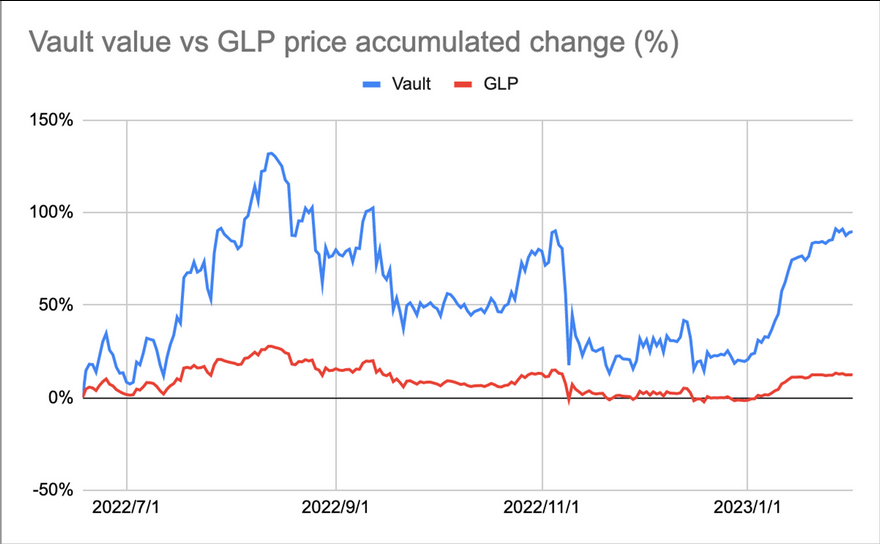

In terms of performance, with a PnL of 12.3% for GLP, Steadefi's vaults outperformed GLP with a PnL of 89.8%, a 7x higher yield.

Figure 19: Performance comparison of Steadfi and GLP

image description

first level title

secondary title

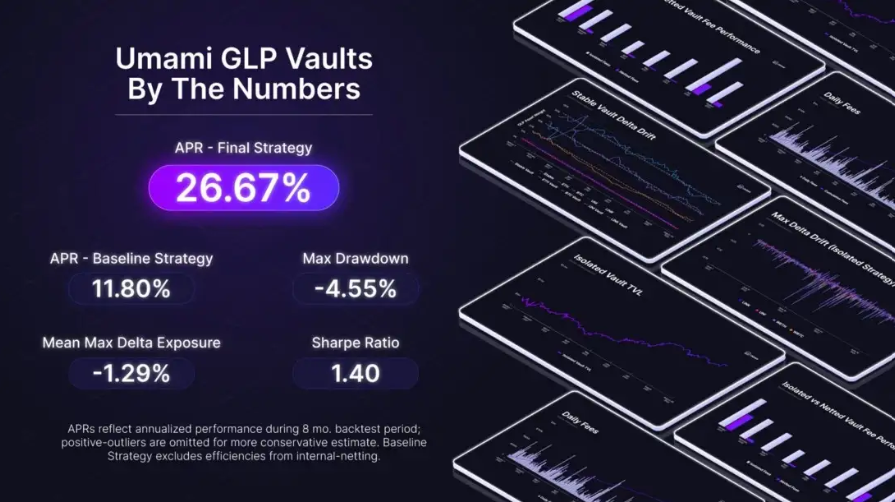

Umami Finance

image description

secondary title

Yama Finance

Yama Finance is building a full-chain stablecoin optimized for maximum capital efficiency, speed and security, and has yet to launch its GLP yield leveraged product on Arbitrum.

first level title

The Future of GLP War

It can be seen that many developers have established many agreements based on GMX, and many agreements have also brought together millions of dollars in TVL. The entire market has a clear demand for GLP-based products.

Due to the composability of DeFi, this Lego-like operation enables GLP to play a role in various agreements, including yield leverage, automatic reinvestment, and lending. As the GMX ecosystem grows, expect more protocols to integrate GLP into their protocols. Of course, GLP also has the risk of being completely exhausted due to traders earning profits from transactions and withdrawing assets from GLP. Therefore, many protocols may try to hedge traders' PnL in the future to reduce risks.

Disclaimer: The above information does not constitute investment advice. Additionally, the above mentioned project Rage Trade is one of our portfolio investments, you can read more about us hereResearch。