Binance Research: Layer 1 Track 2022 Development Summary and Future Prospects

Original title: "2023 CMC Crypto Playbook: Layer-1 s — What Has Happened and Where Are We Headed?》

Original source: Binance Research

Compilation of the original text: The Way of DeFi

Considering where 2022 is supposed to be and all that is happening in the crypto space, Layer 1 (“L1”) can still be described as having a very interesting and eventful year. In 2022, many noteworthy events occurred in L1 space. From the transition of Ethereum from PoW to PoS in September, to the thunderstorm of the Terra ecosystem in May. New L1 projects have also made significant progress, such as Aptos launching its mainnet, while Sui is expected to launch early next year. Notably, BNB Chain and Layer 2 (“L2”) solution Polygon gained more market share in the market vacuum left by Terra, while Solana has had a more challenging year, driven by the recent FTX event One of the more influential L1. The year was filled with major events that arguably affected the entire course of cryptocurrency development.

first level title

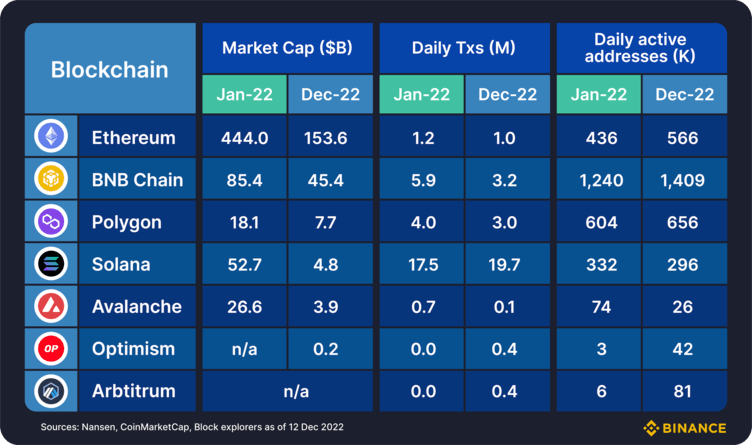

Figure 1: L1/L2 market cap and daily on-chain metrics in 2022

first level title

main observation

• Of course, there are many reasons for the lower market capitalization, and we are not going to discuss them specifically. However, we should note very clearly that market cap does not necessarily correlate with very important on-chain metrics in terms of daily transactions and active addresses. As we can see, BNB Chain and Solana are doing well here, while Ethereum, despite having a higher market cap, is significantly lower in terms of daily activity.

• Ethereum: Merge! We don't want to go on repeating what happened to the merger, but we want to talk about its impact. The data shows that since the transition to PoS was completed in mid-September, $ETH supply growth has dropped significantly (from 3.58%/yr to 0.005%/yr). In fact, combined with its burn mechanism, $ETH was a deflationary asset for most of November and is currently very close to that level.

• BNB Chain: BNB Chain has had a commendable year with only ~45% market capitalization down year-to-date, much better than key competitors Ethereum (-64% YTD) and Solana (-90% YTD). BNB Chain is one of the main L1s helping developers displaced by the Terra and FTX scandals. Daily activity metrics remain very high, with BNB liquidity staking and the launch of zkBNB being notable highlights. Innovation and partnerships in the NFT space are also in full swing, with OpenSea recently announcing support for BNB Chain NFTs on its platform.

• Layer 2 (Layer 2): While L2 is a technical step down from L1, no discussion of L1 would be complete without at least commenting on the growing expansion market. Polygon is the undisputed leader in this area, with a wide range of comprehensive solutions. It's been a strong year for Polygon, and their business development continues to shine (Starbucks NFT, Reddit NFT, Instagram/Meta NFT, etc.). More surviving L2s, Arbitrum and Optimism have also performed strongly over the past year and continue to increase activity/take market share from some of the smaller competing L1s. The launch of the OP token earlier this year was a notable moment for Optimism, while Arbitrum continued to focus on their core product with the launch of Arbitrum Nitro and Arbitrum Nova.

first level title

Expectations for 2023

Now that we've seen how the major L1s have progressed during the year and some of their notable events, what about the year ahead? What are our initial expectations?

L1s (especially some smaller competing L1s) feel pressure from L2s

• One of the main narratives for the year is the so-called "L222", referring to the fact that 2022 is the breakout year for L2. Is it really? L2 Total Value Locked (“TVL”) data shows an increase of 118% (in ETH terms) since the beginning of the year. So, in a way, yes. 2022 is undoubtedly the most glorious year for L2 so far. However, in absolute terms, the total TVL locked in L2 is only around US$4.5bn. When we compare with the total DeFi TVL in Ethereum (approximately US$25 billion) and the total cryptocurrency market cap of nearly US$900 billion, we can see how far L2 still has to climb.

• Also consider the fact that, as shown in Figure 1, both Arbitrum and Optimism outperform Avalanche in terms of daily on-chain activity. Add to this the growing deployment of competing L1s dApps on L2s, such as Avalanche's Trader Joe recently announced their deployment on Arbitrum, and it will be interesting to monitor what happens with some of the smaller competing L1s. Many in the crypto space are discussing the idea that the main L1 will simply be the settlement layer, with execution and activity happening on the L2. While we've seen some of this already, 2023 is likely to be the year we see this happen on a much larger scale.

If the new L1 really brings something new, they can survive