Jump Crypto: A comprehensive analysis of the value, use cases and future of on-chain credit

Original compilation: Amber, Foresight News

Original compilation: Amber, Foresight News

Since the massive explosion of DeFi activity and innovation in mid-2020, decentralized lending has become a core pillar of the emerging on-chain financial system. Driven by protocols like Aave and Compound, where borrowers can deposit one token as collateral and extract some of its value by lending another token, DeFi offers a near-frictionless token exchange market and highly flexible trading exposure. However, since most current lending models require overcollateralized debt positions,On-chain borrowers often don’t have access to real credit — i.e. general-purpose loans that are not fully collateralized.

While the status quo works very well for simple tokenized asset transaction logic, we believeThe long-term potential of DeFi lies in the establishment of a truly independent financial system on the chain.The infrastructure of this "parallel" system must be able to meet all traditional financial needs, and for this reason, we see the under-collateralized lending model as an indispensable growth driver.In this post, we will first evaluate the constraints of overcollateralization, and then we will examine two main alternative models for undercollateralization: decentralized prime brokerage and on-chain identity.

Since on-chain entities are not trusted by default, each lending model takes a different approach to rebuilding trust while mitigating credit risk.in the prime brokerage model, the protocol provides credit through contracts or proxy wallets, retaining ultimate control over the use of funds.In an identity-based model, the protocol establishes some mapping from on-chain borrowers to different real-world entities before issuing loans. Both systems exist today, but adoption has thus far been limited compared to the skyrocketing growth of overcollateralized lending. We believe that as the market matures, less-collateralized lending will be increasingly adopted, and that these two approaches represent complementary visions that together can accelerate the growth of on-chain credit.

Credit is the Engine of Growth

Before we delve into alternative methods of credit extension, we need to determine what "credit" means, what it takes, and why it matters. In practice, "credit" in DeFi often means something completely different than in traditional finance.

What is credit?

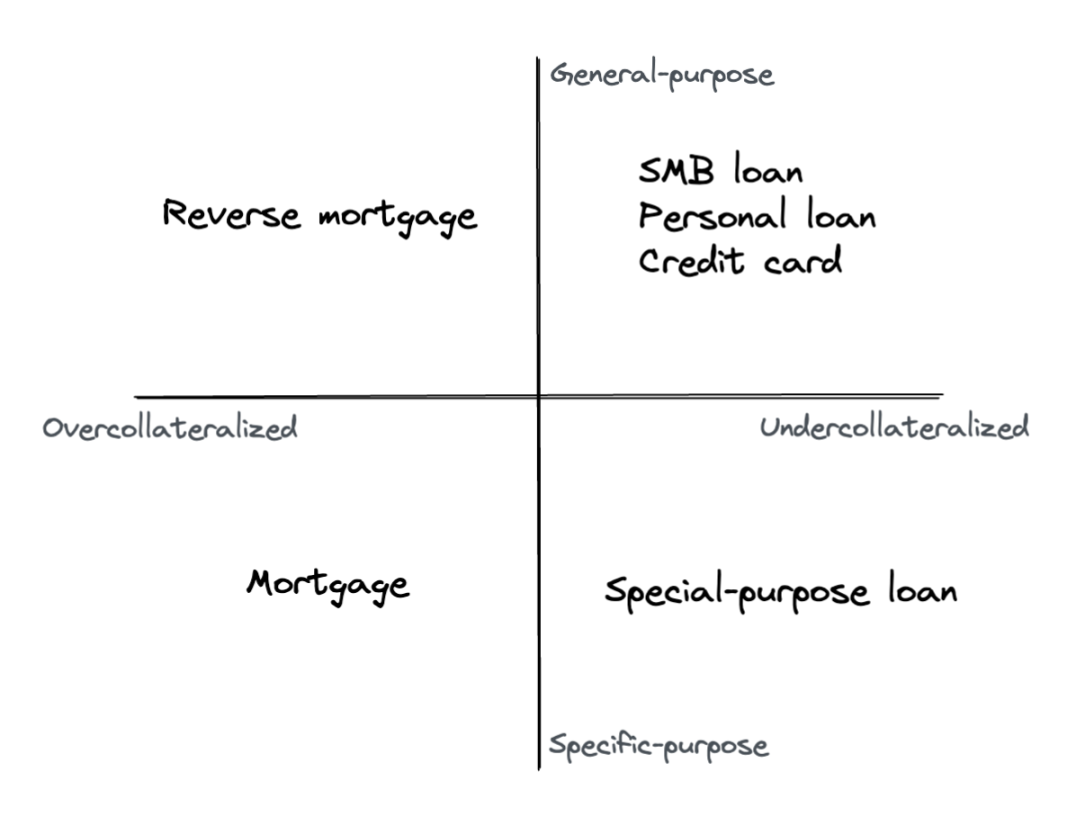

In the real world, when we say "credit," we usually mean the ability to get money that doesn't belong to you.Besides the interest rate, there are two main variables that determine the nature of the loan: what the borrowed funds can be used for, and how the loan is secured.In the case of a mortgage, a homebuyer might put up 20% of the purchase price as a down payment and get the other 80% paid from the bank, with a debt-to-equity ratio of 4:1. The loan is secured or secured by a claim on the house itself. If the buyer stops paying, the bank will repossess the home to recover the value of the loan. Other loans are not secured by direct collateral, but by senior claims on assets or future income. Credit card purchases and corporate bonds are very different in terms of duration and size, but in both cases the lender can use the borrower's other assets to partially cover the lack of collateral. In the case of non-payment, pending claims will eventually be resolved through collection (individual) or bankruptcy (corporate) processes.

Both direct and indirect mortgages are critical to the functioning of the modern economy, because they provide the capital that drives consumption and investment. Considering that every loan occupies some point on the spectrum from overcollateralized to undercollateralized, and another point on the spectrum from specific purpose to general purpose, it is clear that traditional finance supports all quadrants. (In most cases, the main variables are collateral, overcollateralized loans for specific purposes, and undercollateralized loans for general purposes, but we will use both axes for greater precision.)

In the world of DeFi, “credit” provided by decentralized lending protocols often means something completely different: the main use case is not access to more funds, but exposure to a different portfolio of assets. Common applications include arbitrage trading, where borrowing at a higher interest rate versus a lower interest rate, and changing portfolio composition without creating a taxable event. Of course, these are also possible in traditional finance, but this is not the goal of the typical borrower.

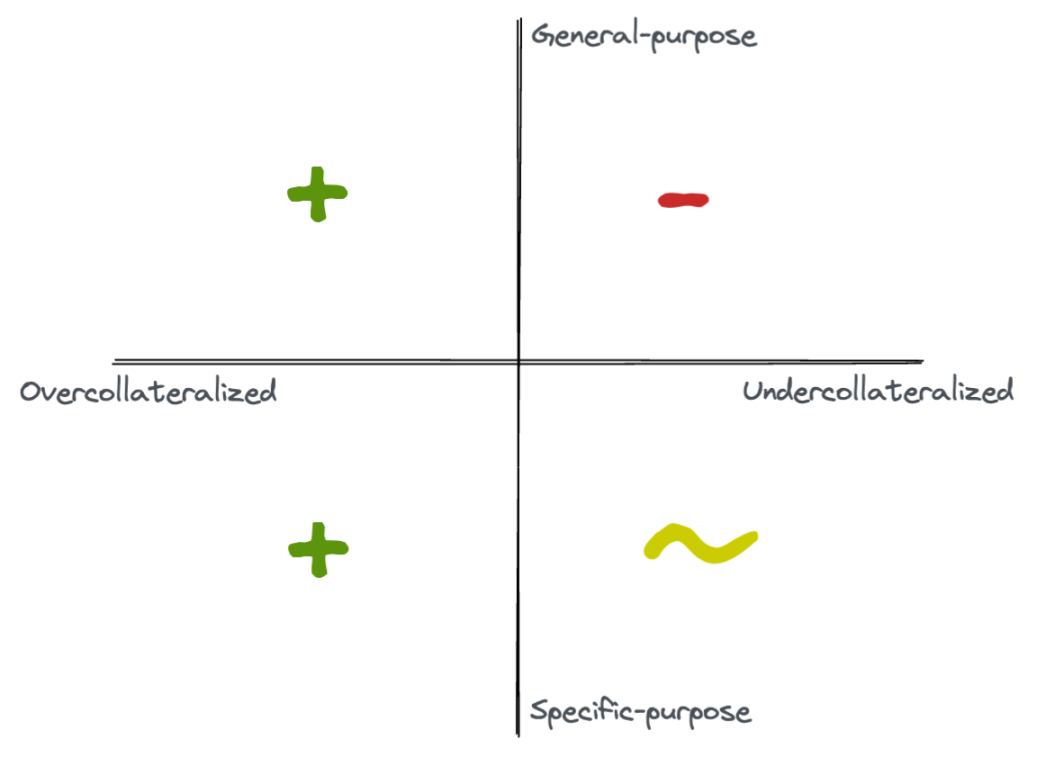

We all know that DeFi can handle over-collateralized loans through protocols such as Aave. What about the other quadrants? As it turns out, we can go a step further in expanding the exposure of our trades. Various agreements including margin trading, perpetual contracts (dYdX), leveraged tokens (Tokensets), and exotic options (Opyn) enable DeFi users to use leverage to trade and obtain richer risk-return options. In the future, we can also use the overcollateralization agreement to simulate leveraged asset purchases such as mortgage loans.However, none of these approaches ultimately provides general, undercollateralized access to credit.To be more specific: If I get a $50,000 personal loan with only $10,000 in the bank, I can use it to buy stocks, buy a car, or bury it under a mattress, and the lender can't interfere with you at all. But if we just use the existing overcollateralized loan agreement, it is difficult for you to "freely control" this part of the borrowed funds.

Re-overcollateralize an undercollateralized loan

Before looking for alternatives, let's try again to see if there is a possibility that we can solve the problem. A fundamental invariant of any over-collateralized protocol is that if you deposit X, you cannot withdraw more than X. However, there are two ways to turn X into a position worth more than X:Recursive deposits and flash loans.

A conceptually simpler approach is recursive deposits, or repurposing debt as additional collateral.It turns out that as long as we can swap from borrowed tokens to staked tokens, we can gain leverage this way. If possible, we could simply deposit collateral into one token, then borrow another token, swap the debt for the collateral token, deposit again, and repeat. (Note that this is similar to "rehypothecation", i.e. pledging the same collateral for two or more unrestricted loans, but this can lead to situations where two or more lenders attempt to forfeit the same collateral. For recursive deposits, This cannot happen even if the entire position is liquidated.)

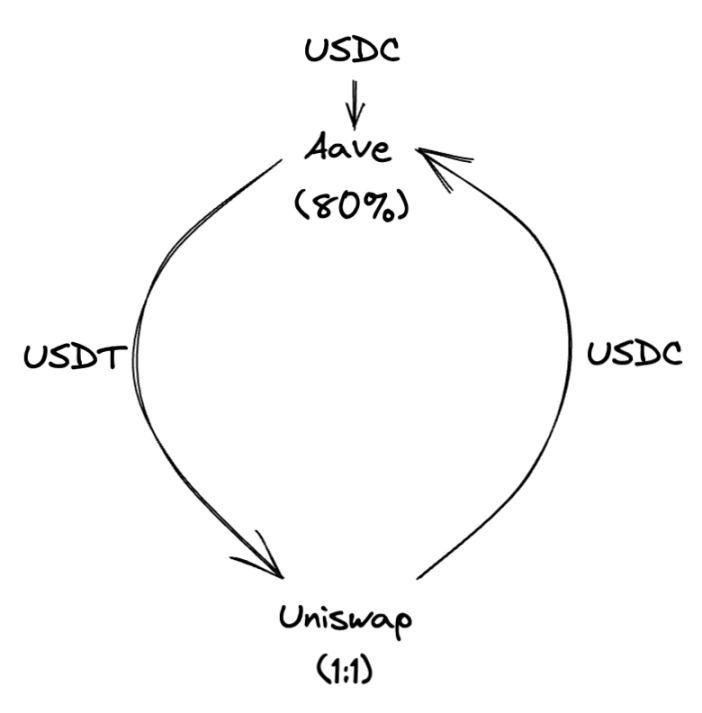

Suppose USDC pays a higher interest rate than USDT, and the yield trader wishes to collect the spread by having a long position in USDC offset by a short position in USDT. If Aave accepts USDC with a maximum mortgage rate of 80%, traders can combine Aave with Uniswap to form a "leverage loop":

The resulting position will be collateral in USDC offset by debt in USDT, allowing our traders to collect the spread on leveraged positions. How much leverage can they get? Neglecting fees and slippage, the collateral ratio r can support leverage up to 1/(1 - r ). For example, with $1 million worth of initial equity and an 80% collateralization ratio, our trader could have $5 million in long exposure - that is, Aave will show lending $5 million versus borrowing $4 million .

While the recursive deposit method has some appeal,But transaction costs and slippage limit its usefulness in practice.In fact,

In fact,Flash loans not only improve capital efficiency, but also fundamentally expand the design space for over-collateralized loans.Specifically, they allow us to buy not only tokens, but indivisible assets represented by NFTs. Anything that can be tokenized and used as collateral, whether it’s a boring ape or tokenized real estate, can be “collateralized” in this way. Indeed, if legal and enforceable, anonymous borrowers could use this method to buy properties on-chain, which cannot be done with recursive deposits because there is no way to buy 20% NFTs, but flash loans allow us to do the whole process in one step.

Limits on Overcollateralized Loans

Despite the ingenious design of flash loans, there are stillTwo problems severely limit its usefulness as a form of credit:

The ____ does not work.Generally speaking, the purpose of taking out a home mortgage is to live in the house while you pay off your mortgage. In the above example, the collateral is trapped in the Aave contract, making it unusable anywhere else. For Bored Ape, this problem will be worse, because the "owner" will not be able to sign transactions, making Ape unusable for attending yacht parties that require verification of NFT holdings.

may lose it.If the Bored Ape reserve price falls enough, the Ape used as collateral may be liquidated. NFT floor prices are notoriously volatile, so there would be significant danger in achieving this outcome. This isn't an issue with traditional mortgages -- if the mortgage itself remains in good standing, the bank can't seize your house when its value drops.

Taking it a step further, while recursive deposits and flash loans are great solutions for margin trading, they are much less effective for asset purchases.In the transaction case, the borrower is often indifferent to risk exposure and ownership; ignoring taxes and fees, an index fund or total return swap is as good as the underlying asset itself. For purchases such as houses or NFTs, borrowers are very concerned about full ownership and use of the asset itself, not the flow of funds. Some benefits of re-establishing ownership are possible - imagine Aave having a "restricted transfer wallet" to hold collateral, essentially a MetaMask with minimal value invariants - but even that doesn't fully own ownership.

Exposure versus ownership is also a key issue when assessing volatility. For traders, volatility is an inevitable part of healthy, well-functioning markets, and liquidation risk is acceptable and expected. For buyers, the prospect of "liquidation" in the sense of losing ownership is generally unacceptable, regardless of the expected financial return.

Why are under-collateralized loans important?

Given the above, we might ask why "collateralized loans" (special-purpose loans secured by purchased assets) are on-chain at all, let alone universal credit. Why not continue underwriting in the real world?

We believe that,If the true potential of DeFi lies in building an independent financial infrastructure, it must eventually replicate all the major functions of that infrastructure.Of these functions, universal credit is arguably the closest to modern finance's raison d'être: to adjust capital supply and demand in form and function. in other words,The financial system exists to drive investment and growth by creating liquidity.

From the perspective of borrowers, over-collateralized loans directly lead to the occupation of cash flow, which is obviously not conducive to liquidity. That is to say, for each deposit X locked in the platform, a maximum of Xr can be borrowed, where r is the maximum mortgage ratio. To create growth in a decentralized economy, we must find ways to make r greater than 1: that is, to enable borrowers to receive more money than they currently have.

Crucially, it is liquidity, not just leverage, that drives economic growth.Consider a renewable energy company with a product that could significantly increase the amount of energy available globally (which would also increase global GDP), but only if it required significant upfront investment. Such a company may take 20 years to generate the necessary funds solely from internal profits, while mature corporate debt markets can provide timely cash flow. But there is currently no overcollateralized loan agreement on-chain that could back the project, because the projected revenue stream for securing the loan doesn't exist yet.In order for DeFi to function as a true parallel financial system, we need to establish a mechanism that can provide "starting momentum" for transactions, consumption and investment.

"Witch Borrowing" and "Default Incentives"

Ideally, honest borrowers could establish on-chain credit for addresses as they do in the real world, proving credit through repeated good behavior.However, this naive approach violates a fundamental economic constraint: the incentive to default. The real-world penalties for neglecting debt are often so severe that voluntary default is rarely considered. While we may not be able to send all debt defaulters to jail, the loss of credit score and the consequent increase in lending rates and denial of credit is an effective and fast-acting incentive. If you realize that your social credit score is too low to prevent you from getting on the train, there will naturally be a binding force.

In the world of cryptocurrencies, this reasoning does not apply, because we do not have a universal and sufficiently binding social credit score: not for lack of trying, but because the concept of a credit score assumes a well-defined entity to which this score is assigned. Again, this is simple in the real world: the borrowing entity corresponds to a known person or business, and if something goes wrong, it can be traced to a mailing address, tax identification number (SSN or EIN), and phone number. In the blockchain world, the typical "borrower" is a stubbornly non-informative hex address. It may be marked on Nansen (possibly wrongly), but there is no guarantee that there is an identifiable individual behind the address, let alone the possibility of recourse in the event of a breach. That address could be one of many addresses belonging to an individual, or part of a protocol library, or a bot. Of course, this versatility has enough advantages in itself: it enables DeFi protocols to operate permission-free, composable, and decentralized. But what happens when address 0x1337 stops paying interest?

This fragmentation of identities incentivizes what we call witch lending: loans that represent anonymous or one-time entities that then default without wider repercussions on creditworthiness.Witch loan borrowers were also common in the real world before globalization and modern record-keeping, and in 18th-century Europe it was quite possible to accumulate outstanding debts in England, flee to France, and re-establish under a new name. start. Even so, this kind of physical escape requires some sacrifices after all. But on-chain, especially with the help of fake accounts on Tornado or centralized exchanges, creating and funding a new address anonymously can be as simple as a few clicks.

Due to the existence of witch lending, under-collateralized lending protocols must work hard to avoid quickly depleting the protocol capital pool by fraudulent borrowers.Granted, it is possible to somehow reward long-term good behavior, with anonymous participants still incentivized to maintain the reputation of their accounts, just as exchanges reward large numbers of participants with lower fees. However, we do not expect most anonymous borrowers to possess this level of reputational capital.Most borrowers have every reason to view the protocol as an adversary in a repeated prisoner's dilemma, "cooperating" through good behavior until the value of the outstanding loan grows enough to "defect" and abscond with the funds. That’s why protocols designed to provide universal lending must address identity issues in addition to credit risk issues.

Each of the three lending models employs different mechanisms to defend against Sybil attacks.For overcollateralization, the incentive is economic. In decentralized prime brokerage, it's algorithmic and technical. With on-chain identity, it is social and legitimate.All three mechanisms create the conditions for viable decentralized lending markets, but each requires different types of sacrifices and pins success on different types of market participants.

Gain Safety Through Overcollateralization

The first answer to the Sybil attack question, which boils down to "Why don't I take the money and run away?", is to use economic incentives as a form of economic security: you won't default because you'll lose money.This is the promise that every fully collateralized debt position maintains: when given the choice between forgoing collateral or taking out a loan, the borrower prefers to retain access to the collateral because it has greater value.Overcollateralization invariance — ensuring that collateral is always more valuable than the loan — is maintained through liquidation auctions, where participants are rewarded for purchasing debt positions when loan pair values rise to the point of being in danger of being undercollateralized .

Most activity in protocols like Aave and Compound is single layer, depositing and borrowing only once, although as mentioned earlier, there are ways to achieve leveraged exposure. Some protocols, such as DeFi Saver, create an auto-execution (recursive deposit) layer on top of these lending protocols, while others, such as Alpaca, provide platform-native leverage. However, since total debt never exceeds total collateral, all borrowers' positions remain overcollateralized even as notional risk is multiplied, ensuring the solvency of the entire protocol.

Establish a closed system with a prime broker

The second solution to the Sybil problem is to maintain a reliance on "code is law", but look at it another way:Instead of enforcing overcollateralization in an open system, undercollateralization in a closed system can be simulated by restricting the use of funds.Creating a large but well-defined boundary through an interface or set of integrations, protocols can provide the benefits of under-collateralized lending while remaining technically over-collateralized (retaining ultimate control over assets). We can think of this "borrowing in a bubble" as algorithmic security: the code will solve the problem.

Indirect financial action is a feature of traditional prime brokerages, hence the name "decentralized prime brokerage". However, the general concept of "prime brokerage" is much broader than a bank providing execution for hedge funds. The actual operations involved — providing leverage, market access, and other benefits when trading and executing trades on behalf of clients — also happen every time a client interacts with a centralized exchange like Binance, FTX, or Coinbase. For these exchanges, the “boundary” of the system is defined by the exchange’s own partnerships and enforced through a combination of technical controls and human review.

Decentralized prime brokerage is the result of defining boundaries and executing trades on-chain.Decentralized prime brokerage protocols can enforce necessary restrictions through several types of access controls,For example:

Issue assets to specific wallets, allowing well-defined command sets and smart contract interactions

Issue assets to proxy contracts, allowing deposits from any wallet, but only implementing a specific set of functions

Denominated in specific tokens, transferable only between protocols with pre-specified interfaces to lenders (we haven't seen this approach yet, but a modified ERC20 could theoretically work this way)

restrictions may be specific, such as a whitelist of function calls allowed per smart contract, and possibly general, such as a minimum invariant of addresses holding debt. Regardless of the approach, the key is to ensure that the loan (a) can be fully utilized, but (b) cannot be converted into a freely tradable token in an unrestricted self-custodial wallet.

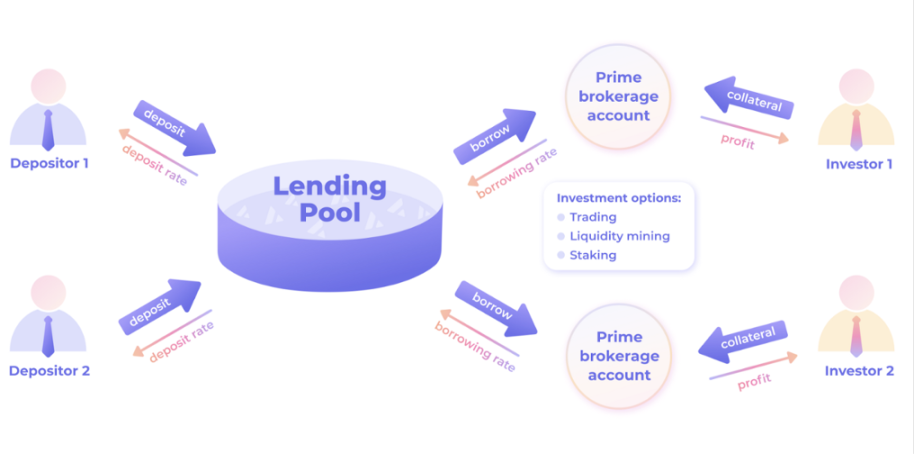

Oxygen is an example of a decentralized prime brokerage, and others like DeltaPrime are rapidly building new solutions. Gearbox's credit account is another variation on this model, although leverage is currently limited to farming mining and liquidity provisioning.However, the cumulative volume across all decentralized prime brokerage protocols is still orders of magnitude lower than overcollateralized loans.

In the long run, we expect decentralized prime brokerage solutions to exhibit strong network effectsimage description

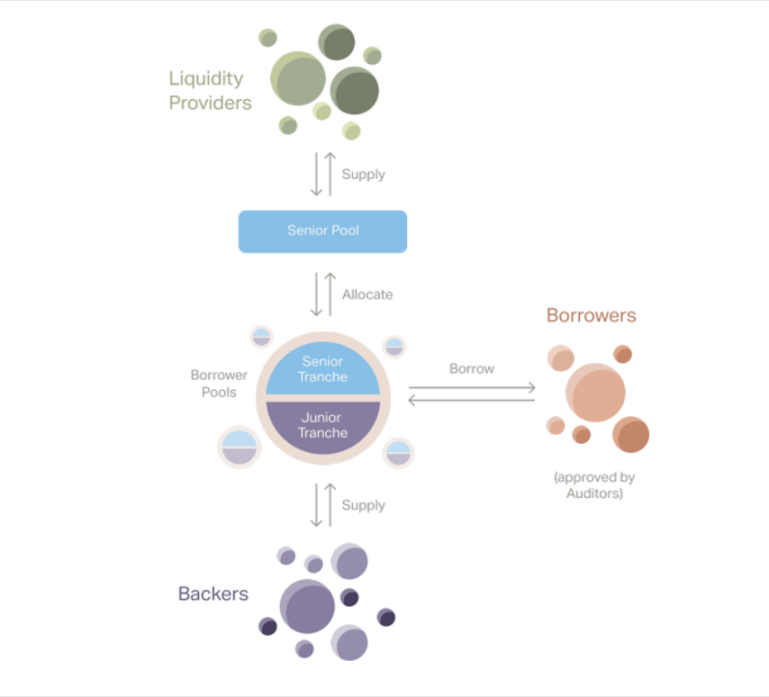

DeltaPrime Prime Brokerage Lending Model

Real-world mapping with on-chain identity

Both the overcollateralization and prime brokerage approaches impose restrictions on credit, limiting the type of leverage that can be obtained (overcollateralization) or the available use of capital (prime brokerage).In order to have a fully universal loan where borrowers can actually run away with their money, we need another incentive to ensure that the net loss of doing so outweighs the immediate gain.Ultimately, this requires imposing broader consequences on the borrowers themselves, which we call socio-legal security: you will not default because you will be penalized off-chain.

Going back to our earlier example of social credit scores, borrowers who default in the real world face two consequences: the prospect of their income or assets being forcibly redeployed, and the impact on creditworthiness, which will make future loans less profitable. more expensive or unavailable. As long as any of these conditions hold, borrowers will generally cooperate, and in either case, each loan must be traceable to realities that could impose reputational and/or legal consequences on it world entities. That is, while there must be a party with sufficient information about the borrower to impose consequences, it does not have to be the lender.This is the idea behind performing a minimalist version of KYC via on-chain identities.As long as there is at least one participant who can prove the identity of the borrower, thereby providing an incentive, and one participant who is willing to underwrite the loan and provide the funds, there is no need to disclose the identity of the borrower to any party other than the source of funds.

image description

Goldfinch's lending model

Horizontal comparison of the three methods

After outlining the three main approaches to on-chain credit, we can compare their pros and cons in several ways.

basic attributes

We'll start by summarizing the basics: what are the fundamental properties of each approach, and what types of lending activities do they support? We define the categories as follows:

Security:How does the lending mechanism prevent witch lending?

Impact on Borrower Liquidity:Are borrowers' access to liquidity increased or decreased?

Borrower Identity:Who or what is ultimately responsible for repaying the loan?

Credit usage:What is the range of uses for acquiring credit assets?

As noted earlier, overcollateralized loans generally reduce borrower liquidity, unless (in a limited sense) magnified by revolving or flash loans. Decentralized prime brokerage occupies a middle ground between over-collateralized and identity-based models, creating liquidity for trading risk and asset ownership, but only for services integrated with protocols. Identity-based lending succeeds in unlocking truly universal credit, but in return requires a stronger notion of identity.

key growth point

At a systemic level, we can also evaluate each lending mechanism by looking at the key growth drivers of the protocols that use it.

System complexity:How many "moving parts" are needed to facilitate a loan?

Network Effects:To what extent does utility depend on the number and quality of participants?

Value driver:What are the key points that determine the value of the service to the borrower?

Key groups:Which type of players is most critical to building a strong ecosystem?

The overcollateralized model wins handily for simplicity and low startup costs, which explains why overcollateralized lenders tend to include DEXs as the first addition to every new blockchain ecosystem. Both the identity-based brokerage model and the prime brokerage model require more effort to overcome the cold start problem because they have relatively strong network effects. However, the two types of networks rely on different core growth drivers: decentralized prime brokerages scale by adding integrations and partnerships, while identity-based systems scale through their underwriters. As these network effects drive higher cost of capital for identity-based systems and wider use of capital for prime brokerage systems, we believe network effects on the prime brokerage side are more fundamental.

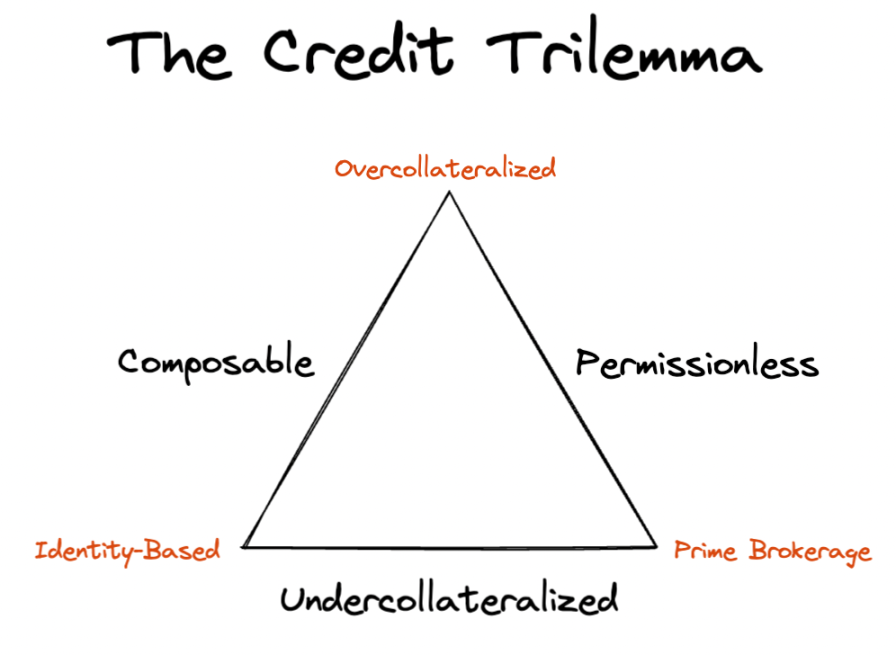

Crypto Spirit and the Impossible Triangle of Credit

Decentralization:

Decentralization:To what extent can the system be controlled by a few dominant parties?

Composability:How easy is it to integrate the service with other protocols?

No permission required:How dependent is the system on gatekeepers or third-party agencies?

Autonomy:How much control do borrowers have over their identity?

Over-collateralized lending embodies the benefits of an on-chain approach: anyone can lend to, lend to, or build on top of a protocol without identifying information or requirements for third-party gatekeepers (except for permissioned pools). Both identity-based lending and prime brokerage lending make sacrifices to enable broader lending, but the tradeoffs come from different areas. Decentralized prime brokerage retains permissionlessness and autonomy at the cost of composability and some decentralization. Driving new use cases and partnerships may require a focused core team effort, and composability is limited because money can only flow within the boundaries defined by the protocol. In contrast, identity-based lending retains composability due to universal lending, but forgoes being permissionless, as each loan requires due diligence and approval by an off-chain gatekeeper. Self-sovereignty also suffers, as borrowers must voluntarily provide real-world information, even if ultimately only a final proof or cryptographic hash is published on-chain.

In fact, we can think of the trade-offs of on-chain borrowing and lending as another trilemma — the credit impossible triangle.On an ideal platform, loans would be composable, permissionless, and under-collateralized, but each solution fundamentally solves only two problems, but is challenged on the third:

The end of the story: what will the world end up like?

After addressing the pros and cons of each lending method, we might also ask: Is one party "should" win in the end?

A prime brokerage-driven credit market ends up looking a bit like an archipelago, with “islands” of services integrated with each protocol linked through mutual agreements between them.Each protocol will benefit from internal network effects as its total capital and reach grow, but also from inter-protocol "trade" via reciprocal agreements to fulfill debt positions. This highly interconnected, execution-agnostic end state is familiar to veterans of traditional finance: When a hedge fund buys a stock, its clients neither know nor care whether Morgan Stanley or Goldman ultimately makes the purchase.

on the contrary,Identity-based credit markets may tend to recreate real-world relationships. Local underwriters will have better risk models to fit the demographics they know best, and borrowers will be able to get better rates from underwriters who better understand their identity and credit history.Even in a "decentralized" network with many independent members, these structural factors are preserved to some degree. However, the importance of geography may diminish as lenders learn to export their risk models to similar borrowers in different markets. In the long run, a competitive on-chain marketplace with borderless lenders and a semi-commoditized risk model could not only drive better access to credit, but even act as an equalizing force in real-world credit markets.

Although the scales of the two models are quite different, we believe thatThey are complementary, with each model tailored to a different core use case and borrower profile.You can use a decentralized brokerage firm to take out a loan, send your own BAYC to the proxy wallet, and let you sign the title. Or you only need to have a good loan history, then you can use your credit score to obtain a loan while protecting your identity.

bright future

In this post, we examine three lending mechanisms that enable secure and decentralized credit markets:Overcollateralized, decentralized prime brokerage, and on-chain identity.While the overcollateralization model has driven over $100 billion in lending activity and enormous innovation in protocol design, we believe that forTo enable the full range of economic use cases, prime brokerage and identity-based models will be critical.DeFi already provides excellent solutions for trading, foreign exchange, remittances, and "borderless" capital, butDriving durable economic value also requires a more general on-chain credit model.Original link