Editor's Note: This article comes fromMeng Yan's blockchain thinking (ID: mytokenomics)Editor's Note: This article comes from

Meng Yan's blockchain thinking (ID: mytokenomics)

, Author: Meng Yan, Wang Wei, Zhou Zhiqiang, reproduced by Odaily with authorization.

Digital assets are becoming a central topic in the digital economy and digital finance. The emergence of blockchain has redefined digital assets and created great opportunities for digital assets, but at the same time it has brought difficult challenges to its research. What exactly are digital assets? How are digital assets on the blockchain different from those in the previous centralized system? How did these differences occur, and what impact will they have? This document is dedicated to systematically exploring and discussing the above-mentioned issues related to digital assets.

asset definition

To discuss what a "digital asset" is, we must first discuss what an "asset" is. Unfortunately, there is no strict, authoritative definition of an asset in law, but there are some clearly thought-out and highly illuminating points. Here are two of our picks:

Mr. Wang Zejian, an authority on civil law, defines assets as:

Reference Definition 1: A collection of rights with monetary value [1]

The Ministry of Finance of the People's Republic of China defines assets as:

Reference Definition 2: "Resources formed by the past transactions or events of the enterprise, controlled or owned by the enterprise, and expected to bring economic benefits to the enterprise." [2]

The essence of Mr. Wang Zejian’s definition (refer to Definition 1) is to point out that assets are a “collection of rights”, that is to say, assets are a group of rights that exist entirely at the level of human consciousness and law, not any physical objects. We must distinguish the collection of rights as assets from the ontology objects that derive this group of rights. This is an extremely profound insight. However, this definition also has obvious shortcomings. What exactly counts as "having monetary value"? It's ambiguous.

The definition of the Ministry of Finance (refer to Definition 2) has three outstanding highlights: 1) It states that assets are "resources that are expected to bring economic benefits." The key point here is the word "anticipation", which shows that the economics of assets are not real, but as long as they are based on subjective judgments or even guesses in the minds of some people, they can be called assets. 2) It points out that the assets must be controlled or owned by the enterprise, and cannot be left alone. 3) Point out that the source of assets comes from past "transactions or events". The meaning of the word "events" is unclear, but it can be clear that assets need to be created through contractual actions such as transactions and legal resolutions. However, this definition also has two outstanding shortcomings: 1) It only discusses the assets of enterprises, that is, the assets of legal persons, but not the assets of natural persons. Of course, this problem is not big, just a little expansion. 2) Defining assets as "resources" is a really serious problem. Not only is the meaning general and vague, but it also confuses assets as a collection of rights and the basic ontology that derives these rights.

We combine the strengths of the two reference definitions and propose the following asset definition:

Assets are a collection of rights that are formed and adjusted by transactions or other agreed actions, have clear owners or controllers, and are expected to bring economic benefits.

Regarding the above definitions, the following clarifications need to be made:

First, assets must have expected economic returns. Among them, "anticipation" is a key point. As an asset, it does not necessarily have to generate positive cash flow, or even have definite economic returns, as long as there is an expected value greater than zero for its future economic returns at this moment. This shows that assets are a purely subjective judgment and, by their very nature, a guesswork. From this we also have an important inference, that is, assets must have arrangements for distributing income. Since assets have expected returns, no matter whether the returns are actually generated or not, the rules for the distribution of returns must be arranged in advance. You can have rules without benefits, and you can't have benefits without rules.

Secondly, in this definition, we adopt Mr. Wang Zejian's view that assets are characterized as a collection of rights. This is of course more accurate, but it will also bring some inconvenience in use. For example, we usually say "this house is Zhang San's property". According to the above definition, this statement is wrong. The correct statement should be "the aggregate of the ownership and control of this house is Zhang San's asset." But it is obviously unrealistic to force people to change their language habits in order to pursue semantic precision. Therefore, we can accept such a statement, but it should also be clear that this is actually a lazy and simplified statement. The essence of this asset is the collection of ownership and control rights derived from the basic ontology. This is an important question that helps us understand assets.

Third, this definition requires a clear owner or controller, that is to say, a subject who decides on the arrangement and disposal of assets. Among them, "clarity" is a key requirement. Its meaning is that for any asset, there must be a definite subject that holds its ownership or control. A subject is either the controller of the asset or not, and there is no ambiguity . In addition, there is an important inference, that is, the status of assets is changeable and controllable. Because if the state of the asset is unchangeable and uncontrollable, then the so-called owner and controller are meaningless.

Fourth, the creation and adjustment of assets is achieved through transactions or other agreed actions. This explains where the asset came from and how the owner or controller controls changes to the asset's state. Transactions are easier to understand, so how to understand "agreed behavior"? The agreements here include private agreements, laws and regulations, articles of association, ethnic customs and even general consensus. In short, the status adjustment of assets always needs to be carried out in a certain clear procedure, and be protected or even confirmed by external rules.

Fifth, assets can be symbolized or even materialized. As pointed out earlier, assets are actually a collection of rights, rather than the basic ontology that derives this group of rights (land is not an asset, but the ownership of the land is an asset). But this does not mean that assets are invisible and intangible things. Assets can be symbolized or even materialized. Currency, stocks, options, bonds, bills, land deeds, etc. are the symbols or materialized representations of assets, and they themselves have no other meaning except to represent part or all of the assets. Therefore, with regard to assets, one should clearly distinguish the basic ontology (land), assets as a collection of rights (land ownership), and the materialized representation of assets (land deeds). This conceptual clarity is very important for the following discussion of digital assets.

We can apply the asset definition above to examine some interesting questions.

For example, generally speaking, land is undoubtedly a type of asset, but if A and B land on a new continent and face a piece of unowned land, they decide to fight to determine the ownership of the land. So was the land an asset before the fight happened? According to the definition, there is no clear controller of this piece of land at this moment, and in the future, both Party A and Party B may or may not be the controller of this piece of land, so unowned land is not an asset.

Is health an asset? In various fitness advertisements, the saying "health is the most important asset in life" is already a cliché, so what is the actual situation? We can think that health can produce expected economic benefits, but is health a collection of rights? Can the health status be adjusted by transaction or agreement? It seems that the text is wrong. Therefore, health should not be considered an asset.

For another example, if someone is crazy about certain items and actively collects them, but everyone in the world thinks these collections are worthless, is the ownership of these collections an asset? Many people will answer no. But we can see from the definition that assets are extremely subjective. If a person subjectively expects that this item will have economic benefits in the future, even if other people in the world disagree, this item is also an asset for him. To understand this, imagine that the person anticipates that others may suddenly become interested in the item in the future and demand a high price for it. You can also think about it in reverse. If the item is lost, the person is willing to pay a certain amount of money in order to find it. Thinking about it this way, such a collection does have expected economic benefits, and it is indeed an asset.

Expression of assets

In the above discussion, we pointed out that an asset is a collection of rights, which is abstract but can be expressed symbolically and materially. We also pointed out that standardized tickets such as currency, securities, and land deeds are all expressions of assets. But if we go back to the root, we will realize that the contract is the basic expression form of assets, and the ticket is just a standard contract with a high degree of standardization.

For example, if a loan agreement is signed by both parties, it is an asset for the creditor. And this agreement does not have to be expressed in the form of a standardized ticket. It can be a handwritten white note, or a fingerprint can be used to represent a signature, but as long as the basic requirements of the contract are met, it can be protected by law or custom and become the simplest document. Asset materialized expression.

This is true in logical analysis, and it is also true in history.

At least 5,000 years ago, in the Sumerian civilization, written contracts had already appeared [3]. In modern times, it has been fully applied in all major civilizations of the East and the West. Once the contract technology is produced, it becomes the mainstream form of expressing the ownership of rights, debt relationships and other assets.

In the development of contract technology itself, there is a process from general to special, from heterogeneous to homogeneous, and from non-standardized to standardized.

Non-standard and general contracts appeared first, followed by standard contracts. First, they were established by convention, and then the basic format (schema), metadata (metadata) and rule framework of the contract were regulated in the form of laws and regulations or industry standards, allowing both parties to fill in some Customized content, which greatly improves the efficiency of contract formulation, reduces transaction friction, and creates conditions for contract circulation by endorsement.

A security is a special kind of ticket, which is usually a bearer standardized homogeneous ticket, so it has low barriers to understanding and transaction friction, that is to say, it has good liquidity. However, the most important significance of securities lies in their absolute homogeneity (fungible), that is to say, any two units of the same type of securities have exactly the same essence and cannot be distinguished. Because of this characteristic, securities simplifies the abstract asset rights it expresses into a one-dimensional object, degrades complex interest balances into quantitative relational operations, and thus can introduce mathematics, the most powerful tool, into the asset world. Its significance cannot be overemphasized.

image description

Figure 1. Jiaozi in the Northern Song Dynasty

image description

"THIS NOTE IS LEGAL TENDER FOR ALL DEBTS, PUBLIC AND PRIVATE"Figure 2. Ming Bao Banknote

On U.S. dollar bills, the terms are reduced to one sentence:

(The promissory note is the legal repayment of all public and private debts)

Discussions about money are forever filled with heated debates. We do not intend to get involved in the debate on the essence of currency and the origin of currency, nor do we imply that currency has really evolved sequentially from contracts in history. In fact, the historical development of the two is intertwined and intertwined, and it is not necessarily possible to discuss the sequence. Monetary scholar Zhou Ziheng once demonstrated that currency was a differential payment tool in the early days, and it was to be used in conjunction with contracts [4]. The evolution of money into a form of payment in full is a result of the late development of civilization. But now that both have developed to a highly mature stage, when we conceptually construct the entire system, we should realize that, in terms of trading tools, the contract is the basic and general, while the currency is the advanced Yes, special. However, this special abstraction of currency very powerfully embodies the concept of value in transactions, so it has been widely used, so that our contemporary people are submerged in it every day, and are more familiar with it than contracts.

The point is that we have constructed a progressive conceptual structure, that is, contracts are the most basic and general expression of assets, standardized contracts are special contracts, tickets are special standardized contracts, securities are special tickets, and currencies are special securities. The relationship between the five is expressed as the following figure:

image description

Figure 4. Five asset representations

So far we have basically completed the discussion of traditional assets and their performance techniques. Next, we will focus back on digital assets.

Analysis of digital assets

The current popular definition of digital assets on the Internet is that all content stored in digital form can be called digital assets, so all kinds of digital documents, pictures, audio and video objects can be considered digital assets.

However, according to the definition of assets in the first section of this article, assets are essentially a set of rights. Therefore, if the above definition of digital assets is accepted, then digital assets are a collection of economic rights derived from digital objects, or assets based on digital content.

However, blockchain technology redefines digital assets. One of its important applications is that it can digitize asset representation from contracts to tickets and from securities to assets into smart contracts or tokens. Therefore, blockchain The chain can realize the digital expression of assets.

Most discussions of digital assets to date have failed to distinguish between assets based on digital content and digital representations of assets. The sloppyness on this issue is the key reason for people's misunderstanding of digital assets and insufficient understanding of the significance of blockchain and tokens.

We start by discussing assets based on digital content. Since an asset can only be a set of rights in essence, the digital content itself must not be an asset, but only a set of rights attached to the digital content can be called an asset. This is the same as "land is not an asset, but land ownership is an asset". The difference between it and land assets is mainly that the basic ontology is different, one is land and the other is digital objects. It can also be said that such digital assets are actually traditional assets derived from digital objects.

Note that the expression of assets based on digital content is not necessarily digital, it can also be expressed with traditional paper contracts and paper notes. For example, we use a paper contract to establish and distribute the copyright of a certain digital movie. The basic entity is digital content, but the asset itself is expressed in a paper contract. This asset is actually a traditional asset, and its expression and management methods are traditional.

The digital representation of assets is discussed below.

The so-called digital expression of assets is to digitize the way of asset expression in the previous section. For example, a contract that was originally expressed in paper and words can be expressed in a digital PDF file; an original paper boarding pass can be expressed as an electronic boarding pass in a mobile wallet; an original paper stock can be expressed as a CSI The electronic record in the registration system; the original paper banknote, expressed as the balance in Alipay; the original paper real estate certificate, expressed as a record in the national real estate registration database. These are all digital expressions of assets. However, the basic ontology of these digitally expressed assets may be non-digital things, such as houses, equity, money, etc. Of course, the basic ontology can also be digital content, such as a digital movie, a digital photo, an online novel, etc.

The difference between the two is very clear. One basic ontology is a digital object, but the asset expression method is not necessarily digital, and the other asset is expressed as a digital object, but its basic ontology is not necessarily digital. But of course, there is intersection between the two. If an asset whose basic ontology is digital and whose expression is also digital, then it belongs to both categories.

So, when people talk about "digital assets", do they mean the assets attached to the digital content, or the digital expression of the assets?

We hold a clear attitude on this issue, that is, we believe that digital assets should refer to the digital expression of assets. This choice is mainly out of utilitarian considerations, because if digital assets are positioned as assets based on digital content, then it is just adding a new category to traditional assets. After the emergence of blockchain technology, positioning digital assets as the digital expression of assets will open up a whole new world for digital assets, open finance and even the entire digital economy. In order to give "digital assets" a bigger stage, we suggest that digital assets be strictly limited to the digital expression of assets, and assets based on digital content be renamed "digital content assets".

The door to this new world is opened with the emergence of blockchain technology. Therefore, we need to re-discuss the significance of blockchain for asset expression technology.

Blockchain is a technology platform for contract digitization

There have been many different views on the essence of the blockchain. Some people think of it as distributed ledger technology, some define it as a unique data management technology, and some define it as a smart contract platform. Two of the authors of this article (Meng Yan, Wang Wei) and Yuan Dao and Zhu Peijiang of the Zhongguancun Blockchain Industry Alliance jointly proposed at the end of 2017 that the blockchain should be mainly regarded as the supporting infrastructure of the token (token) [5], also in It has caused extensive discussions in the industry and gained a certain degree of recognition.

Text-paper, as a technology, is likely to promote human civilization more than the sum of all other technologies. There are two scenarios for the application of text-paper technology, one is to disseminate information, and the other is to support contracts. Some people may think that a contract is also a kind of information, so there is no difference between the two. But careful consideration leads to different conclusions. Putting words on paper, making multiple copies, advertising them widely, and disseminating ideas and ideas is a use. It is actually another purpose to record the agreement matters, form a consensus and even legal provisions, and preserve evidence for future supervision and arbitration. In the former use, people pursue low-cost reproduction, editing, and dissemination, so printing is widely used. In the latter use, people's appeals are just the opposite. They pursue the authenticity, non-reproducibility, non-tamperability, and non-repudiation of the contract, and are afraid of forgery, let alone copying and editing. Therefore, handwritten signatures and complex signatures are still widely used. Anti-counterfeiting printing technology to be certified.

By understanding the difference between the two application scenarios of text-paper, you can immediately gain a new understanding of the similarities and differences between the Internet and the blockchain: the Internet is the digital upgrade of text-paper technology in the information dissemination scenario, and the blockchain is the The digital upgrade of text-paper technology in the contract support scenario is shown in the following figure:

image description

Figure 6. Two scenarios of text-to-paper technology and its digital evolution

Therefore, we describe the blockchain (one-sidedly) as a distributed system maintained by multiple parties that supports the creation, verification, storage, transfer, execution, and other related operations of digital contracts. The precursor technology of blockchain is text contract, signature, standard contract, ticket, securities, currency, law and other contract technologies. A technical upgrade. Since contracts and laws are the basis of human institutions, the blockchain will have the ability to influence all institutional arrangements.

We mentioned in the previous section that before the blockchain, we could already express assets digitally. For example, digitize contracts with PDF documents, digitize tickets with digital pictures, digitize currency with electronic credits, and so on. We might as well refer to these technologies collectively as traditional contract digitization technologies. So what are the advantages of blockchain and tokens compared to traditional contract digitization technology?

It can be said that compared with the blockchain, the traditional contract digitization technology is actually just "printing" the contracts and tickets originally written on paper to the screen, and it does not really play the main role of the digital computable platform. strengths and potential. On the contrary, traditional contract digitization technology introduces some new weaknesses and even loopholes, not only cannot completely replace traditional paper contracts, but also has some unexpected consequences.

First, it introduces new security risks. Since digital objects are easy to copy and tamper with, and have no natural authentication mechanism, they are easily copied, tampered with and destroyed by unauthorized persons or hackers. To this end, the security and reliability of computer systems must be constantly checked and enhanced. Nevertheless, security vulnerabilities in this area can be described as endless, which makes the cost and risk of traditional contract digitization technology quite high.

Second, it brings new trust and regulatory issues. In order to reduce the cost and risk of traditional contract digitization technology, people concentrate a large amount of data and processes in a few computing centers, and entrust the important responsibility of maintaining the system to a small group of professionals, which indeed reduces marginal costs. But this small group of professionals wields enormous public power, often organized in private companies and working in black boxes. How to ensure their integrity and reliability, curb their impulse to use monopoly position to distort the market, how to effectively supervise and minimize the cost of supervision have all become crucial and very thorny issues.

Third, it brings data privacy issues. Based on paper contracts, both parties can well protect the data privacy of transactions and agreed items. However, the digitization of contracts and centralized hosting in a third-party centralized system is tantamount to exposing business secrets to the hosting platform.

Fourth, it brings about the problem of unfair data pricing. When a large amount of data, especially digital contracts, is centrally hosted on a third-party centralized platform, the centralized platform can obtain huge economic benefits through algorithms such as big data analysis and artificial intelligence. Whether the centralized platform will pay the data custodian for this, and how to price the hosted data, has become a problem. In fact, the current common phenomenon is that centralized platforms use their powerful positions to implement unfair strategies in their favor.

So how does the blockchain improve support for the digitization of contracts?

First of all, the blockchain, with its unique storage structure of time-series single-linked list composed of hash pointers, greatly improves the consistency, tamper-proof, non-repudiation and reliability of the contract expressed in the blockchain, which is very close to physical objects. This greatly reduces safety risks and maintenance costs.

Secondly, the distributed and multi-party maintenance nature of the blockchain greatly improves transparency and reduces trust risks and regulatory costs.

Third, the ubiquitous and ubiquitous cryptography applications of the blockchain provide a wealth of means to protect data privacy.

Fourth, the blockchain can effectively package and express data assets, facilitate their transactions, and discover their fair prices through the market.

Fifth, the smart contract in the blockchain can express the terms of the contract in code, and automatically execute when the condition is triggered, so that the contract execution, which originally needs to be done by a human, can be completed by a computer, which greatly reduces the the execution cost of the contract.

Based on the above characteristics, we can say that the blockchain is the first technology that can effectively support the digitalization of contracts after the emergence of computers and networks. The digitalization of contracts can only be realized after the emergence of the blockchain. In contrast, the previous traditional contract digitization technology is simply unqualified and defective.

Just because the blockchain itself is a platform for digital contracts, and contracts are the basic expression of assets, the blockchain has become an ideal infrastructure for the digital expression of assets, that is, digital assets.

Digital representation of assets in the blockchain

So far, digital assets mainly exist in the form of fungible tokens. Starting from Bitcoin, the vast majority of digital assets in the blockchain and open finance fields are designed as homogeneous tokens. In the Ethereum ecosystem, this homogeneous token is often created following the ERC-20 standard. According to our statistics, as of the end of September 2020, there were a total of 297,000 ERC-20 smart contracts deployed on the Ethereum main chain, while only less than 6,500 smart contracts created heterogeneous tokens. The difference between the two is 45 times, which can be described as a huge disparity .

Ethereum supports Turing's complete smart contracts, which upgrades the blockchain to a general digital contract management platform. In other words, the blockchain has the ability to express general, non-standardized contracts, which are smart contracts. Of course, its expressive ability is far behind that of natural language, but it can already solve many practical problems. Moreover, since the blockchain can digitally express general contracts, it can also digitally express standard contracts, tickets, securities, and currencies.

We show the corresponding technology as follows:

image description

Figure 7. The corresponding technologies of the five asset expression forms in the blockchain

At present, a variety of asset expression methods have been effectively supported in the blockchain:

Corresponding to general non-standard contracts and laws, it is digitally realized in the blockchain with smart contracts (Smart Contract);

The standard contract is also implemented as a smart contract, but the standard contract can be realized as a smart contract template or a code library (library);

Ticket is an asset expression technology with rich content and wide applicability. At present, there is no standard implementation technology corresponding to tickets in the blockchain. The closest thing is Non-fungible Token (NFT), but it is still far from covering various scenarios of tickets. This is not difficult to achieve through the deep use of smart contracts.

Securities and currencies can be supported by tokens or native cryptocurrency in the blockchain. This is the most advanced and special form of asset expression, but it is the earliest implementation in the blockchain .

It can be seen that the blockchain already has the ability to support all major digital asset forms, and has brought huge technical advantages to the definition, management, and application of digital assets, and has become the most ideal support platform for digital assets.

Technical discussions

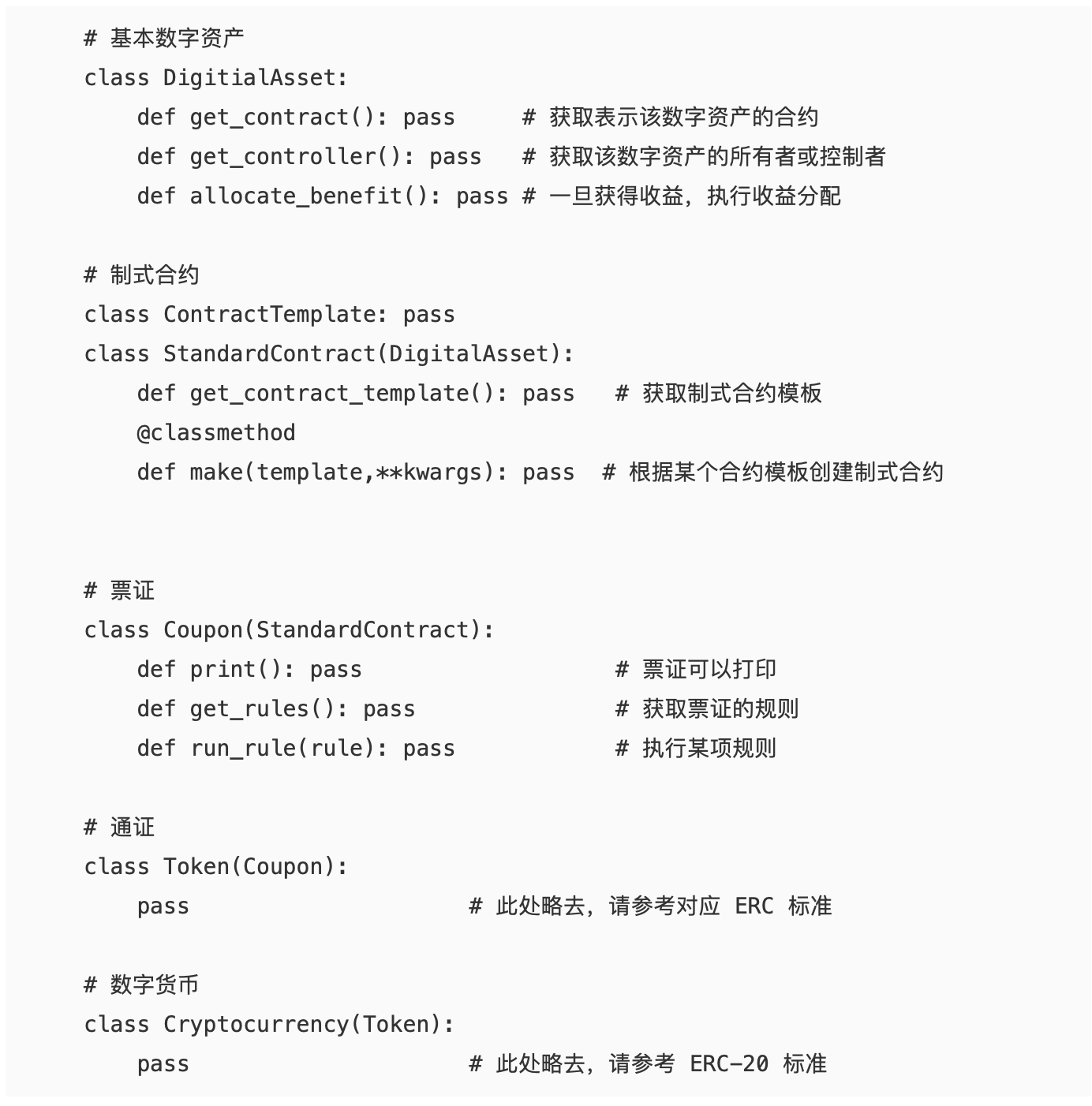

So far, we have expressed our main views on digital asset issues in the form of narrative. Readers with object-oriented programming experience may have noticed that the description of the relationship between the five types of digital assets (contracts, standard contracts, tickets, securities, and currencies) in this article actually constitutes a typical class derivation chain. Therefore, it will be clearer and more concise to discuss this part in code.

Therefore, the last part of this article discusses how to use code to define the above five types of digital assets.

In fact, defining digital assets with code is not only for concise and precise description, but also has huge practical application value. It must be stated that we are still studying this, and there are still many problems to be solved. Even for the problems that have been solved, because they may involve intellectual property rights and commercial secrets, they are not fully announced here, and only general ideas are proposed for reference by colleagues.

For example, when defining assets, we mentioned that assets are expected to bring benefits. This sentence is easy to say, but how to express it in code? In other words, how to use code to express that something has expected benefits? It seems impossible. But as we mentioned in the extended discussion of this issue in the first section, the direct inference of assets having expected returns is that assets must have arrangements for distributing income, that is, the rules for income distribution must be arranged in advance. Therefore, we believe that the way to express "assets have expected benefits" in the code is to arrange a method allocate_benefit() to perform benefit distribution. Questions like these need to be carefully considered one by one.

Summarize

The following will no longer elaborate on theoretical issues, but directly describe several major types of digital assets in a Python-like pseudo-code manner.

Summarize

This paper explores a series of issues from asset definition to digital asset expression, classification, and blockchain digital assets. We first define an asset as a collection of rights that are formed and adjusted by transactions or other agreed actions, have a clear owner or controller, and are expected to bring economic benefits. Then, we point out that contracts are the most general form of expression of assets, while standard contracts, bills, securities and currencies are contract expressions with increasing standardization. For digital assets, this paper defines it as the digital expression of assets. Corresponding to the five expressions of assets, the blockchain provides ideal digital support. Therefore, we believe that blockchain is an ideal support and management technology platform for digital assets.

[3] David Graeber,Debt: The first 5,000 years

[1] Wang Zejian, General Principles of Civil Law

[2] Order No. 76 of the Ministry of Finance of the People's Republic of China, Accounting Standards for Business Enterpriseshttps://blog.csdn.net/myan/article/details/78712506

[4] Zhou Ziheng, Account, Social Science Literature Press, 2017

[5] Yuan Dao, Meng Yan, Token is the key to the next generation Internet digital economy,