芯片股「最大利空」終於來了?Meta會是「第一個縮減資本支出的大廠」嗎?

- 核心觀點:Meta計畫出售過剩算力,打破了市場「算力絕對稀缺」的信仰,標誌著AI投資週期從硬體軍備競賽轉向財務紀律與算力利用率,引發晶片股拋售和資金向軟體及削減開支的科技巨頭輪動。

- 關鍵要素:

- Meta組建「Meta Compute」新業務,擬將過剩算力以API服務或直接租賃方式出售給外部客戶,與供應商CoreWeave等直接競爭。

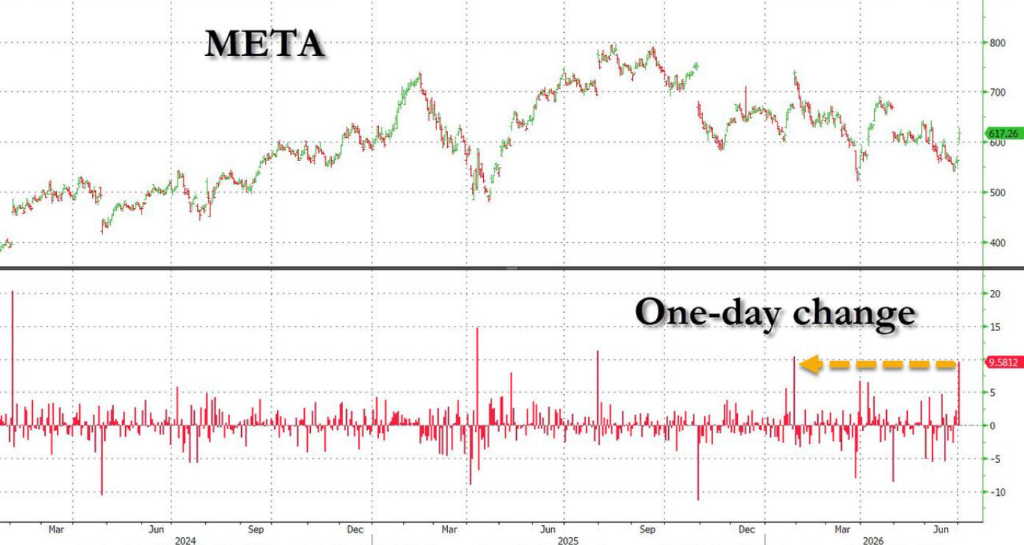

- 受此消息影響,Meta股價單日暴漲10%,而輝達、美光等晶片股及新興雲服務商遭猛烈拋售,納斯達克指數顯著波動。

- 高盛警告稱,「算力稀缺」敘事被顛覆後,硬體領域率先承壓;AI市場如「拉伸的橡皮筋」,負面訊號累積至臨界點將引發估值重構。

- 動量交易策略崩盤,高盛高Beta動量籃子單日重挫9%,多空高Beta動量指數創2020年以來最差單日表現。

- 市場焦點轉向自由現金流穩定性和財務紀律,瑞銀表示此舉緩解了資本支出持續上升的擔憂,資金輪動至軟體板塊。

- 「過剩產能」提法引發對AI真實需求擔憂,即將到來的財報季和資本支出指引是估值重估能否持續的關鍵。

- 儘管成交量創歷史新高,但市場流動性極差,標普E-mini期貨頂層流動性月環比暴跌33%,大額交易易引發劇烈波動。

Original Author: Ye Zhen

Original Source: Wall Street News

Meta's plan to sell excess computing power has shattered the market's core belief in "absolute scarcity of computing power." This strategic pivot has triggered a massive capital outflow from chip stocks, also signaling a turning point in market tolerance for tech giants' unchecked capital expenditures.

The news sparked extreme polarization in the secondary market. Meta's stock, proactively signaling spending cuts, surged 10% in a single day, marking its best performance of the year. Conversely, traditional beneficiaries of AI hardware—semiconductor giants, memory chip manufacturers, and emerging cloud service providers (Neocloud)—suffered heavy losses, dragging the Nasdaq index into significant volatility.

Wall Street institutions generally interpret this as a major narrative shift in the AI investment cycle. Capital focus is rapidly moving from sheer hardware infrastructure buildout towards corporate free cash flow stability and computing power utilization rates. Investors are now rewarding tech giants demonstrating financial discipline with real capital.

This reshaping of the underlying logic not only rewrites the power dynamics between hyperscalers and chip suppliers but also directly leads to the collapse of crowded momentum trading strategies, planting new uncertainties for the upcoming US earnings season and market liquidity.

Meta Restructures to Sell "Excess Computing Power"; Big Tech CapEx Faces Inflection Point

According to Bloomberg, Meta is forming a new business unit to sell its excess computing capacity to external customers for revenue. Insiders reveal potential plans include allowing external access to various AI models hosted on Meta's existing AI infrastructure, a model similar to AWS's Bedrock service. Meta would operate the data centers and chips powering models like Muse Spark and charge developers for access.

Furthermore, Meta is also considering directly selling "raw" computing power. Ironically, Meta had just signed multi-billion dollar contracts with emerging cloud providers like CoreWeave and Nebius, and this move means it will turn around and compete directly with its own suppliers.

This internal initiative, dubbed "Meta Compute," aims to build and manage the company's AI infrastructure. The team is co-led by Meta's infrastructure head Santosh Janardhan, AI department executive Daniel Gross from the Super Intelligence Lab, and Meta President Dina Powell McCormick.

In fact, this shift was foreshadowed. Meta CEO Mark Zuckerberg hinted to investors during the May shareholder call that selling excess computing power or API services was "definitely on the table." Another company that previously sold excess computing power, SpaceX, is currently facing intensified competition in this area.

"Compute Scarcity" Logic Shattered; Chip and Momentum Stocks Hit Hard

Meta's move directly challenges the core premise that had fueled the recent surge in chip stocks. Goldman Sachs' 1-Delta desk head Rich Privorotsky warned that the market's core premise has been compute scarcity. Once supply increases and lease prices decline, the scarcity narrative will be directly overturned, and the hardware sector would feel the pain first.

Goldman Sachs warns that the AI market is like a stretched rubber band. The market's persistent disregard for negative signals will eventually reach a tipping point. If any major tech giant takes the lead in cutting AI spending, the valuation logic for the entire AI sector will face a comprehensive restructuring. Simultaneously, the rise of low-cost AI models is challenging the current "spend more for growth" logic.

Following the Meta news, the chip and memory sectors were hit first, with star stocks like Nvidia, Micron, and Sandisk experiencing heavy selling. Emerging cloud service providers were seen as the most obvious losers, with their stocks posting some of the largest single-day declines of the year.

The hardware sector's crash directly triggered a comprehensive collapse of momentum strategies. Goldman Sachs' High Beta Momentum Basket (currently dominated by chip and memory stocks) plunged 9% in a single day after reaching historic gains. BTIG analyst Jonathan Krinsky noted that the long/short High Beta Momentum index fell 10%, marking its worst single-day performance since 2020.

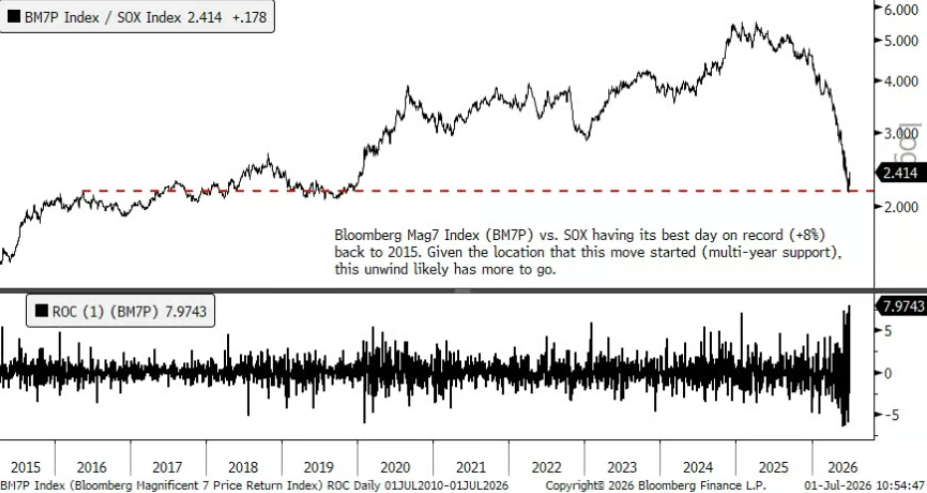

Additionally, the yield spread between the Bloomberg Mag7 Index and the Philadelphia Semiconductor Index (SOX) hit its largest single-day extreme (+8%) since 2015, indicating a frantic capital exodus from the semiconductor sector.

Market Logic Reshaped; Investors Reward "Spending Cuts"

In stark contrast to the hardware stock slump, the market assigned a high premium to signals of capital expenditure cuts. As Goldman Sachs previously predicted, the first hyperscaler to signal the possibility of slowing spending would see a reward in its stock price.

Meta's 10% surge confirms this judgment, indicating that investors find incremental revenue streams and financial discipline more attractive than a bottomless arms race at current valuation multiples.

UBS trader Christina Dwyer stated that the related reports shifted the market narrative towards stricter financial discipline, alleviating concerns about continuously rising capital expenditures. CapEx expectations are no longer unilaterally upward-sloping, and market focus has turned to free cash flow stability.

In the context of capital rotation, the software sector experienced its second-largest single-day excess return relative to the semiconductor sector in a year.

Intensified Competition & Liquidity Concerns; Future Earnings as Key Guide

Meta's entry into the field complicates the supply and demand outlook for hyperscalers. While a new competitor disrupts the existing landscape, easing supply chain bottlenecks could also alleviate cost pressures.

UBS points out that the mention of "excess capacity" has raised market concerns about the true underlying demand for AI. Looking ahead to the upcoming Q2 and Q3 earnings seasons, the guidance provided by companies and their full-year CapEx plans will be crucial in determining whether the current valuation revaluation can be sustained.

Worryingly, while undergoing massive rotation, the market faces severe liquidity risks. Goldman Sachs' trading desk warns that despite US stocks recording the highest average daily volume since 2026, market liquidity remains extremely poor. In June, top-of-book liquidity for S&P E-mini futures plummeted 33% month-over-month, from $12 million to just $8 million.

This means the market is conducting record-breaking trading in a capital pool that has drastically shallowed. Every large order triggers greater market volatility, execution costs are rising, and the risk of abnormal intraday crashes remains high. Compounded by the historically weak seasonality for momentum stocks in July, the tug-of-war between chip stocks and the broader market could face even more violent swings.