这届炒美股的股神们已经不看财报了

- 核心观点:2026年美股AI浪潮中,最赚钱的策略并非持有英伟达等巨头,而是投资于由新一代“股神”发掘的“供应链狙击”型微盘股。这些股神不看传统财报,聚焦于AI产业链上游的“卡脖子”环节,通过注意力经济与叙事传播驱动股价。

- 关键要素:

- 新一代“股神”以Leopold Aschenbrenner(22岁,用2亿美元起始资金赚到140亿美元)和Reddit的Serenity为代表,专攻市值几亿到几十亿美元的微盘股。

- Serenity凭借对AXTI公司(市值70亿美元,垄断磷化铟衬底)的分析,喊出从12美元到150美元的目标价,该股已涨至140.83美元,单笔交易浮盈曾达1000%。

- 这些新“股神”的核心方法是跳过财报,直接分析供应链上游材料、订单线索和技术路线(如光子学、光通信),寻找垄断性节点。

- 微盘股的低流动性与低机构覆盖,使其成为散户驱动的注意力经济战场,叙事一旦形成,价格优先于基本面兑现。

- 机构资金因规模限制无法参与微盘股,为散户提供了信息优势;但该类资产的可持续性依赖于信息差、基本面跟进及退出流动性。

In the 2026 US stock AI wave, the biggest moneymakers weren't those holding household-name stocks like Nvidia, Microsoft, Amazon, and Google. These trillion-dollar market cap giants were certainly rising, but it's hard for elephants to dance.

A new batch of "stock gurus" specializing in "supply chain sniping" are emerging en masse from Reddit, X, and Substack, leaving the old-school Buffett-style value investors far behind in returns. They hold a bunch of micro-cap stocks with market caps ranging from a few hundred million to a few billion dollars, stocks that Wall Street analysts disdain and ordinary investors can't even pronounce the names of.

The man turning these micro-cap stocks into a trading consensus and trend is Leopold Aschenbrenner, a 22-year-old German who turned a $200 million starting fund into $14 billion through stock trading, becoming synonymous with the "new stock guru."

After Leopold, the disenchantment with the Buffett school accelerated. A new batch of "stock gurus" specializing in "supply chain sniping" are emerging en masse from Reddit, X, and Substack. They basically ignore financial reports; instead, they look at those "bottleneck" micro-cap stocks in the upstream supply chain. Following this logic, the BlockBeats editor has found some new stock gurus for everyone to analyze.

Do All "New Stock Gurus" Come from Reddit?

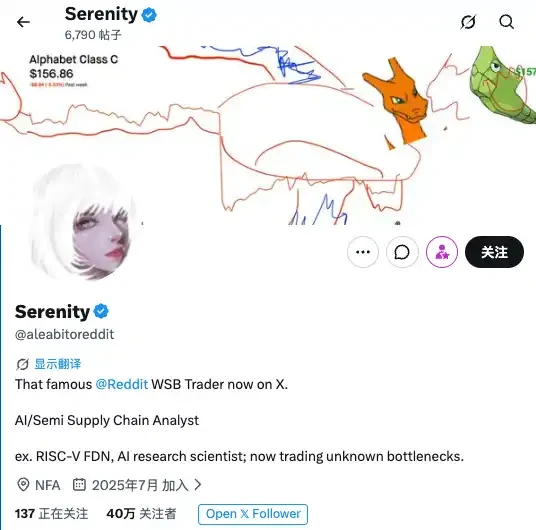

Among this new batch of stock gurus, the one that's hottest and most viral recently is Serenity, originating from the WallStreetBets subreddit.

Many readers trading US stocks are probably familiar with Serenity's story. In short, he was once an AI research scientist, participated in the RISC-V Foundation, published a paper in Nature, and even joked about turning down an offer from Nvidia's AI team when its stock was at $6.

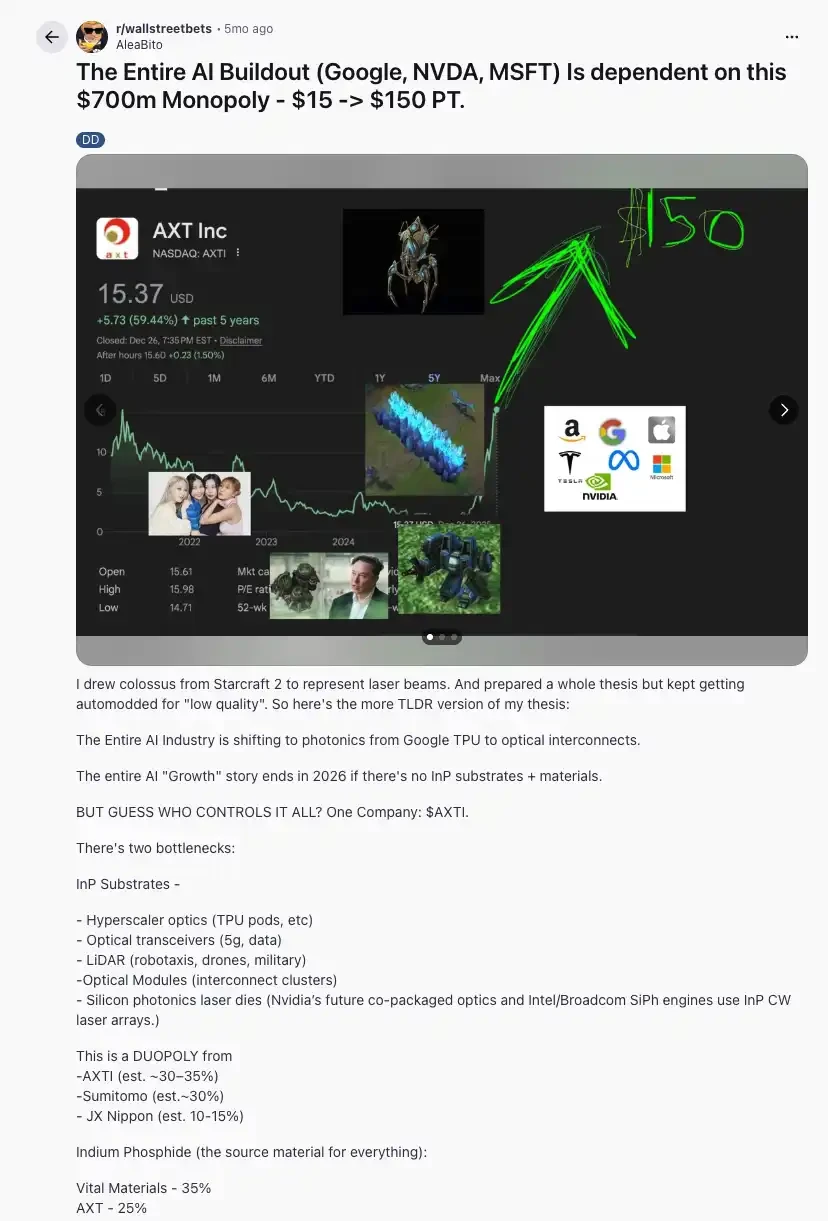

What truly solidified Serenity's "new stock guru" narrative wasn't these self-proclaimed credentials, but because he shouted out a stock called AXTI on WSB. His core argument was direct: The entire AI industry's construction depends on this $700 million market cap monopoly, including all players like Google, Nvidia, and Microsoft, all reliant on its indium phosphide substrates and materials. He believes the entire AI industry is shifting from Google TPUs to photonics, adopting optical interconnect technology. Without indium phosphide substrates, the entire AI "growth" story would end in 2026.

In that viral AXTI post, he directly called for a price target from $15 to $150, with the title being very direct.

Related reading: "Rejected Nvidia’s Offer at a $6 Stock Price, Said He Can Make More Trading Stocks."

The stock price gave Serenity the best endorsement. When Serenity discussed AXTI, the stock was around $12. After that, AXTI rallied all the way, first to $70, which Serenity himself called a trade with unrealized gains once reaching 1000%. As of writing, public market data shows AXTI closed at $140.83, just shy of the $150 price target he set back then.

This makes Serenity's image more complex and multifaceted; he's not just a lucky gambler on WSB, but a deep researcher of the new tech AI industry chain.

Why did this kind of person emerge first from the WallStreetBets subreddit?

We need to spend some time talking about the history of WallStreetBets.

WallStreetBets, or WSB, is the most famous retail investor community for US stocks on Reddit. Its prowess isn't because the people here are rational, nor because you can always find the right answers.

On the contrary, WSB first gained fame because it displayed the two most extreme sides of US retail investors: on one hand, short-term options expiring worthless, going all-in and going bankrupt, mutual mockery; on the other, an occasional post capable of changing market narratives.

The 2021 "retail investors vs. Wall Street" battle started from WSB. A large number of retail investors directly confronted short-selling institutions around GameStop, turning a gaming retail stock, seen as a relic of a bygone era, into a global financial news headline. After that, WSB was no longer just a forum. It became a trading culture: rough, exaggerated, risky, out of control, but occasionally capable of digging out real gems from a pile of noise.

WSB was inherently an extremely suitable breeding ground for "non-consensus trades." And Serenity is a new variant of WSB in the AI bull market.

It used to be GameStop, AMC, short-term options, and memes; now, more and more posts discuss cloud infrastructure, enterprise automation, AI agents, HBM, optical modules, data center power, photonics, and supply chain bottlenecks.

The WSB culture of pumping stocks still exists, but the target of the pump has changed.

This Generation of Stock Gurus Never Reads Financial Reports

And this culture has also spread from Reddit to X.

KawzInvests is another representative of the new generation of stock gurus, with an account focused on US stock trading views and thematic research. Similar to Serenity, his content leans more towards "thematic driving" rather than traditional earnings interpretations.

KawzInvests typically looks at high-elasticity areas like AI infrastructure, optical communications, defense robotics, biotech, in-vehicle software, and small-cap growth stocks, then finds logic from supply chain positioning, order clues, partners, management changes, M&A possibilities, and valuation re-rating potential.

KawzInvests' stock call

PhotonCap is another typical example.

There are rumors in the market wondering if PhotonCap is Serenity's institutional account or another shell. This claim has a folklore feel and fits people's imagination of anonymous masters. However, current public information doesn't show such a relationship. PhotonCap wrote on its Substack that it's a research account run by an optics and photonics engineer, daily dealing with lasers, optical fibers, and transceivers, hence wanting to study how these things are priced in the stock market. It also thanked Serenity for inspiration in a portfolio disclosure article.

Going back to where Serenity first started, Reddit has many similar "stock gurus."

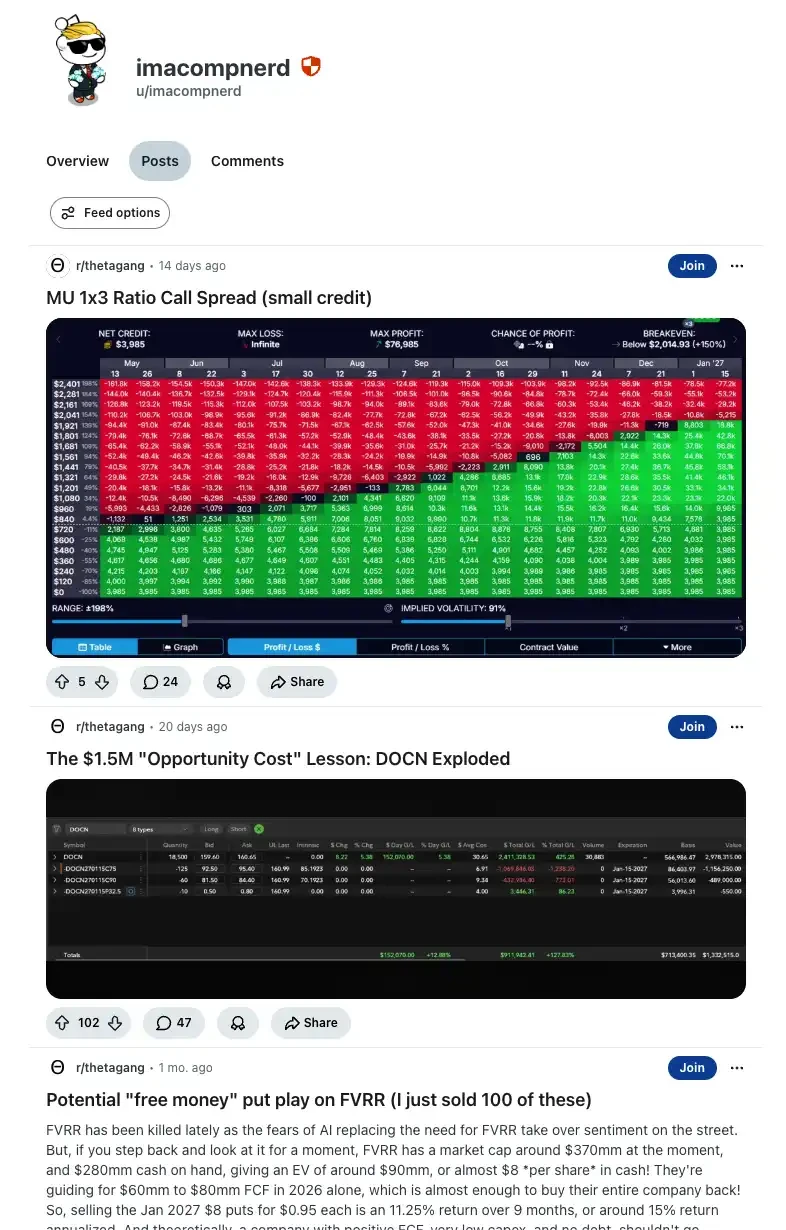

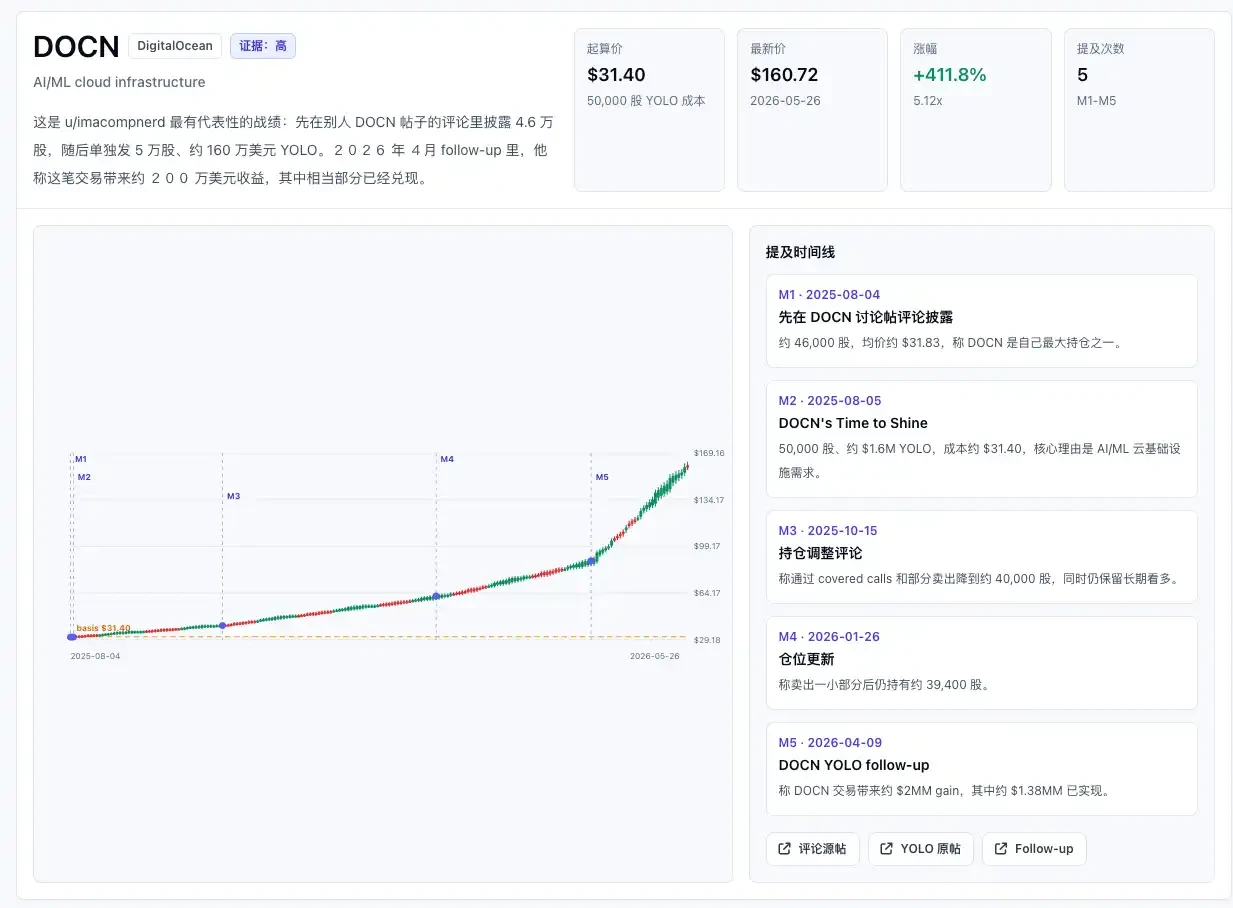

For example, the user with the ID u/imacompnerd.

u/imacompnerd's most famous trade was also DOCN DigitalOcean. This company isn't the most well-known AI leader, but it fits into the middle-layer narrative of AI trades in 2026: Not every developer and SME will directly use AWS, Azure, or GCP, and not all AI/ML deployments need the complex systems of giant cloud providers.

DigitalOcean's story lies in its potential to become a lighter, cheaper, and easier-to-use entry point for AI cloud infrastructure. imacompnerd bet on this position. He once publicly disclosed owning 50,000 shares of DOCN, a position worth about $1.6 million with a cost basis around $31.4; later, he posted a follow-up, stating the trade brought in about $2 million in gains. At current prices, this is no ordinary "bullish" call, but a large concentrated investment with clear wealth effects.

More interestingly, he didn't just become legendary with the DOCN trade alone. Public records also show his heavy positions and reviews of RDDT, GOOG, and MNDY. RDDT corresponds to the traffic, community, and AI data licensing potential of the Reddit platform itself; GOOG is a more traditional large AI platform company; MNDY is another revaluation attempt in enterprise software. The MNDY trade is particularly worth mentioning because it's not a pretty screenshot of victory: he disclosed a position of about $1.9 million, but his cost basis was higher than the stock price at the time of posting, looking temporarily unfavorable. Precisely because of this, this person seems more real than ordinary "returns screenshot" accounts. His portfolio has big wins and unrealized losses; includes AI cloud infrastructure, platform stocks, and enterprise software; involves concentrated bets and position management.

In 2026, the AI sector is fiercely competing in the market.

If the US AI sector pulls back for half an hour during the trading day, capital quickly rushes in to buy the dip; when memory stocks like Micron and SK Hynix move, the South Korean market follows, and then A-shares in semiconductors, memory, communications, CPO, and optical modules move in turn. The market sentiment spreads like wildfire from one AI market to another.

On the other side, traditional assets are becoming increasingly awkward. Baijiu, real estate, insurance, pharmaceuticals, high dividends—these were once sectors with clear investment logic. Now, they often become another form of psychological torment: they don't rise when AI rises, but fall together when the market drops. In the past, buying the wrong sector meant you could comfort yourself by waiting for a style rotation. Now, the more the AI theme rises, the more it seems to drain capital from other sectors.

At times like this, people fear not losing money, but standing on the wrong side of an era. Watching others continuously make money from memory, optical modules, CPO, AI clouds, and small-cap semiconductor stocks, it's hard for holders of traditional assets not to question their life choices. Once anxiety forms, it pushes more capital into the AI theme.

And when the most prominent AI leaders become too expensive, the most aggressive capital will continue moving towards more niche sectors, further upstream, and more obscure parts of the supply chain.

This is the biggest characteristic of this generation of "stock gurus," and the biggest difference between them and the previous generation.

Buffett's work style is reading 500 pages of material daily, feasting on earnings reports, 10-Ks, and 10-Qs. He once held up a thick stack of papers and told reporters that knowledge compounds like interest. He looks at ROE, free cash flow, debt-to-equity ratios, and whether management honestly admits mistakes in shareholder letters. His targets are companies that have operated for decades, have complete financial statements, and generate stable cash flow. After buying, he is willing to hold for ten or twenty years.

The entire skill set of the value investing school is built on the premise that "financial reports are the soul of the company."

But Leopold Aschenbrenner and Serenity's generation of "new gods" basically don't read them. This generation of "stock gurus" looks at: every detail of earnings calls, customer qualification cycles, the rhythm of the industry chain and production lines, whether upstream materials are monopolized, whether a certain technology route is moving from papers to mass production, and whether a certain company is still perceived by the market as an old-cycle enterprise.

They are also different from traditional sell-side analysts. Sell-side analysts look at DCF, EPS, guidance, and target prices. But this generation of stock gurus bypasses financial reports entirely, jumping directly to the upstream of the industry chain to find that "bottleneck" node. For example, a small company with a market cap of a few hundred million dollars but a client list that includes Nvidia and Google; a substrate material monopolized by a certain company; a qualification cycle not yet covered by sell-side analysts.

Ignore financial reports, look at the logic of the industry chain and supply chain – this is the unique skill of the pumpers from the WallStreetBets generation.

These people come from the same era's climate and together form the new school in the 2026 AI bull market.

An Attention Economy Bull Market

Low liquidity assets, early-stage narratives, strong propagation symbols, community diffusion, and the "haven't been discovered by mainstream capital" entry feeling.

Listing these terms together, you find they can describe both meme coins and the hottest batch of micro-cap stocks in today's US stock market. The difference is that meme coins always admit they are attention games, while micro-cap stocks wear the cloak of "hard-tech supply chain research."

But the essence is the same. Small market cap, thin trading volume, low institutional coverage, yet often placed within an industrial story that sounds grand enough. A $700 million market cap company is framed as the bottleneck of the AI era; a $3 billion market cap cloud provider is described as the AI entry point for SMEs; a little-known substrate manufacturer is portrayed as the shared upstream of Nvidia, Google, and Microsoft. Once the narrative is established, the price runs first; whether the fundamentals will truly materialize won't be known for several quarters.

The most interesting thing about micro-cap stocks is that it's not a battlefield where institutions naturally have an edge. On the contrary, the further you go towards small market caps and low liquidity, the more Wall Street's advantages can become constraints.

An asset management institution with a scale of hundreds of billions or even trillions of dollars, looking at a small company with a market cap of three or four hundred million dollars, first thinks not "is this the best opportunity," but "can I buy in, and can I sell out?" It has position limits, liquidity rules, risk committees, disclosure requirements, and transaction impact costs. For a retail investor, a small-cap stock with a $300 million market cap and tens of millions in daily trading volume might be huge; for an institution like BlackRock, this might be just a tiny, almost negligible position. Buying too little is meaningless, buying too much can directly push up the price, or even trigger position disclosure. When it's time to sell, thin liquidity can cause significant slippage.

So, it's not that they can't see it, but often that they can't play. The larger the institutional money, the more powerful it is in large-cap assets; but in micro-cap stocks, scale becomes a cage. The micro-cap pond is too shallow for big ships to enter.

But the attention economy also has its own physical laws.

So whether this cross-market alpha can persist depends on three things.

First, whether the information asymmetry still exists. If only a few FinTwit accounts can clearly explain the photonics supply chain, then CT (Crypto Twitter) followers might indeed get exposure to a batch of low-coverage assets early. But once mainstream sell-side, ETFs, and quantitative funds start covering them, the narrative premium will be quickly compressed.

Second, whether fundamentals can keep up with the attention. AI optical communication is not an empty narrative, but the biggest problems for small-cap stocks are uncertain orders, concentrated customers, financing dilution, and long capacity verification cycles. A company might be in the right track but fail to capture real economic value.

Third, the speed of propagation itself creates exit congestion. The rise of low-liquidity assets is easily interpreted as "the market is validating the narrative," but it could also just be a short-term influx of attention. The more it resembles a meme coin, the more one must be wary of a meme-coin style liquidity ebb—the story is still there, but the buying pressure is gone.

This also hints at a market migration for us: crypto traders are applying the narrative intuition honed on-chain to US micro-cap stocks, AI hardware, energy, power, and supply chain assets. This might be the most noteworthy trading culture shift within the crypto circle this year.

The attention economy attribute of US micro-cap stocks existed long before the emergence of meme coins.

Times create heroes, and times never lack new gods.