USDC Strikes Back at USDT, the Real Battlefield is Hyperliquid

- Core Thesis: The stablecoin competition is shifting from compliance to the battle for distribution channels. The core of the Coinbase-Hyperliquid deal isn't short-term profit sharing, but embedding USDC into the high-frequency trading scenario of perpetual futures to gain a global distribution channel to counter USDT's network effects.

- Key Elements:

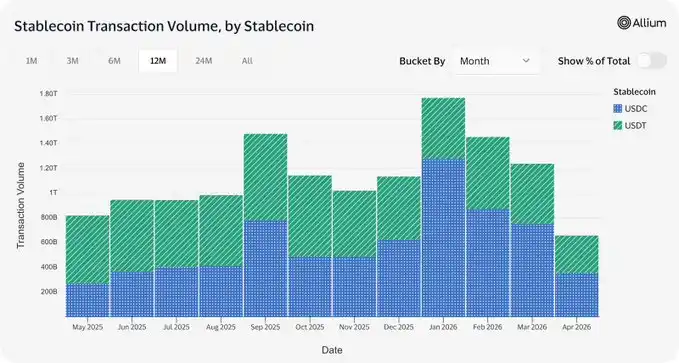

- In May 2026, USDC trading volume surpassed USDT for the first time at $355 billion, but its market share only slightly increased from 27.6% to 28.1%, indicating growth primarily came from the domestic US market.

- Hyperliquid commands 30% of the on-chain perpetual futures market share and 46% of open interest. Its trading volume is already comparable to some centralized exchanges, giving it global reach.

- Post-deal, Hyperliquid receives approximately double the revenue share compared to its previous model and re-integrates USDC, which enjoys high user trust. Coinbase gains a structural distribution channel for USDC within the core perpetual futures scenario.

- Due to regulatory constraints, Coinbase itself covers only about 100 countries, far fewer than Binance, and cannot independently replicate Hyperliquid's global reach advantage.

- Tether is also mimicking this strategy. Following the Drift attack, it invested $147.5 million to make USDT the settlement asset, vying for a slice of the Solana ecosystem's perpetual futures market.

Original Title: How USDC Wins the Hyperliquid Deal

Original Author: David Christopher

Original Translation: Peggy

Editor's Note: The stablecoin competition is shifting from "who is more compliant" to "who can secure more trading entry points."

After the passage of the GENIUS Act, USDC has indeed gained new growth momentum. Circle's U.S. background and compliance advantages have allowed USDC to catch up and even temporarily surpass USDT in trading volume. However, from a market share perspective, the landscape has not significantly changed: USDT still holds the majority of the stablecoin market and maintains a strong position outside the U.S.

This is also the core significance of the deal between Coinbase, Circle, and Hyperliquid. On the surface, it's a stablecoin asset swap: USDC once again becomes Hyperliquid's primary quote asset, and Hyperliquid gains a higher revenue share. But on a deeper level, it's a battle over distribution channels.

Hyperliquid is a core platform in the on-chain perpetual contract market, and perpetual contracts inherently rely on stablecoins as their quote and settlement asset. Whoever becomes the main quote asset in these markets gains long-term usage scenarios from more trading volume, margin, deposits, withdrawals, and on-chain activity. Tether has proven this path through Binance; USDT's strength comes not just from its issuance size, but also from its deep integration into the global trading system.

For Coinbase and Circle, Hyperliquid provides global reach that they themselves find difficult to replicate. Coinbase, constrained by regulations, cannot cover as broad a market as Binance or Hyperliquid. Therefore, embedding USDC into Hyperliquid's trading infrastructure might be a practical path to counter USDT's network effects.

The most noteworthy takeaway from this article isn't whether Coinbase is sacrificing profits, or how much revenue share Hyperliquid receives, but that USDC is attempting to evolve from a "U.S. compliant stablecoin" into a broader "on-chain trading base currency." As perpetual contracts continue to grow, the main battlefield of the stablecoin war may increasingly concentrate on these high-frequency trading scenarios.

The following is the original text:

Tether still dominates Binance, but Coinbase has just reinstalled USDC on Hyperliquid. The battle for stablecoin distribution channels is becoming increasingly fierce.

Hyperliquid is becoming one of the most contested assets in the crypto industry right now. Last week, spot HYPE ETFs launched by 21Shares and Bitwise started trading on U.S. platforms, with Grayscale and VanEck following suit. Behind the rush of institutional capital is a longer-running competition: who can secure a portion of this trading platform's economic returns?

Last autumn, Hyperliquid launched a public RFP for its native stablecoin USDH, aiming to recapture revenue that previously flowed to Coinbase and Circle. At that time, approximately $5.6 billion in USDC was held in Hyperliquid's cross-chain bridge, generating about $200 million in annual interest income, but these earnings went to its centralized competitors. The platform that actually created the demand didn't benefit from it. Ultimately, Native Markets defeated bidders like Paxos and Ethena in a community vote, and USDH was subsequently launched.

Bankless previously reported on Hyperliquid's bidding war surrounding USDH.

But just last week, Native Markets sold USDH to Coinbase and agreed to gradually phase out this stablecoin tied to Hyperliquid's interests, allowing USDC to once again become the trading platform's primary quote asset. In exchange, 90% of the related revenue will flow back to Hyperliquid, although the specific revenue capture mechanism remains unclear. The deal is widely interpreted as a victory for Hyperliquid, paid for by Coinbase and Circle. This interpretation is understandable but inaccurate.

What Hyperliquid gains from this deal is clear: a significantly improved revenue share, roughly double that of the USDH model; enhanced regulatory resources through an alliance with one of the most influential voices of the U.S. crypto industry in Washington; and a return to the stablecoin experience around which the platform was originally built and which its users highly trust. Especially in the HIP-3 market, which has brought significant attention to Hyperliquid over the past six months, USDC remains the primary asset used.

From Coinbase and Circle's perspective, many outsiders view this deal as a PR boost: forging a closer relationship with one of the most crypto-native and successful projects of the previous cycle. But combining USDC's current market position with the growth trajectory of the perpetual contract market reveals another beneficiary.

What Coinbase and Circle truly gained is a distribution channel for USDC. And this scalable distribution might be more important than any other aspect of the deal.

How's the Home Performance?

Since the passage of the GENIUS Act, USDC has indeed shown strong growth momentum. Circle was well-prepared for the new environment shaped by this regulatory framework: USDC is headquartered in the U.S. and has always been compliance-centric. This positioning has translated into real trading volume.

Allium data shows that in May 2026, USDC trading volume reached $355 billion, surpassing USDT for the first time in recent months, also reflecting accelerating growth since the GENIUS Act was passed last July.

But the structural landscape of the stablecoin market hasn't changed.

In April 2025, just before the GENIUS Act's passage, USDT held 67% of the stablecoin market, with USDC at 27.6%. A year later, USDT's share is 67.3%, and USDC's is 28.1%. The change is only half a percentage point. In other words, despite USDC's accelerating trading volume, its supply share has barely budged.

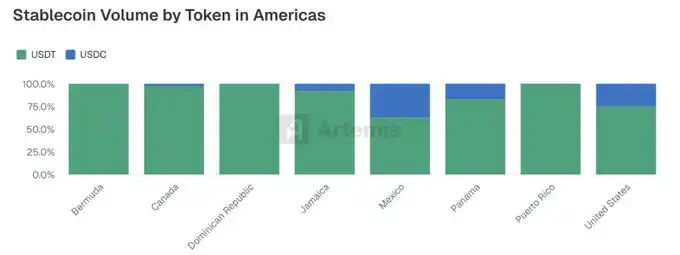

An Artemis report from last October indicated that the U.S. is USDC's strongest market. Given the correlation between USDC's growth after the GENIUS Act and the U.S. regulatory environment, it's reasonably safe to conclude that the U.S. is also the primary source of USDC's growth.

But the problem is precisely that the U.S. is also where new competitors are most concentrated. Stripe has clearly entered the stablecoin business through Tempo and other acquisitions; major financial institutions are also launching their own U.S.-based stablecoins compliant with the GENIUS Act. All are encroaching on USDC's core market.

If pressure in the U.S. home market intensifies further, USDC doesn't have a sufficiently solid overseas base to fall back on. In almost all markets outside the U.S., USDT remains the default dollar stablecoin, widely used for savings, investment, and trading, and is still aggressively expanding. Over the past year, several new chains have been launched specifically to expand USDT distribution; meanwhile, Tether also launched USAT, attempting to enter the boundaries of U.S. regulatory oversight under the GENIUS Act framework, directly challenging USDC's home market.

Coinbase and Circle now have the momentum to continue expanding, but the window to lock down distribution channels before competition fully heats up is narrow. Trading scenarios, especially the perpetual contract market, are the most suitable battleground for seizing this distribution entry point.

Bankless previously reported on Tether's launch of the U.S.-regulated USA₮ stablecoin.

Perpetual Contracts Are the Real Battlefield

Like stablecoins, perpetual contracts are one of the fastest-growing categories in the crypto industry, consistently maintaining double-digit or even triple-digit year-over-year growth rates.

Perpetual contracts and stablecoins are structurally highly interdependent, as stablecoins are typically the primary quote asset in perpetual contract markets. USDT has already established a significant foothold in this area: on Binance, the world's largest perpetual contract trading platform, most trading markets use USDT as the primary quote asset. Any user trading on Binance's core markets mainly transacts in USDT. This further solidifies USDT's supply within the exchange and naturally creates downstream pull effects for deposits, withdrawals, and on-chain activities related to the platform.

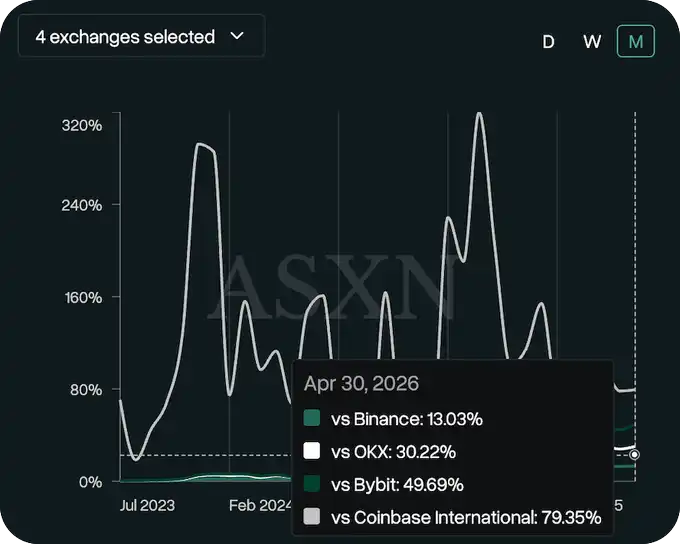

Despite having significantly lower trading volume than Binance, Hyperliquid is already the largest on-chain perpetual contract trading platform, holding a 30% share of the entire on-chain perpetual contract market and commanding 46% of open interest. This position has remained robust against repeated competitive challenges.

At the same time, although Hyperliquid is not a centralized exchange, it has clearly demonstrated the ability to compete at their level. As of April 30, its trading volume was about 50% of Bybit's, 30% of OKX's, and 79% of Coinbase International's. Combined, this is only about 13% of Binance's volume. But the key point is that this number is still growing, and the growth curve points only in one direction.

Although still in its early stages, Hyperliquid's dominance in the on-chain perpetual contract market, coupled with its ability to match or even sometimes surpass centralized exchange volumes, gives it global reach comparable to Binance's coverage outside the U.S. This opens a new channel for Coinbase and Circle: they can leverage Hyperliquid to compete with Tether, transforming it into a structural distribution channel for USDC.

Coinbase Chose Its Battlefield

However, this raises the question: why doesn't Coinbase simply develop its own perpetual contract business further and build this distribution channel itself?

The reason is that Coinbase is constrained by regulatory frameworks, limiting the customer base it can serve and the number of markets it can list. Currently, Coinbase covers about 100 countries, slightly more than half of Binance's coverage of 180 countries. Hyperliquid, benefiting from a more "lenient" operating environment, can reach a broader market, giving it an edge over both Binance and Coinbase—an advantage Coinbase would struggle to replicate.

Therefore, Coinbase and Circle choose to let Hyperliquid play the global reach role, with USDC entering these markets as the underlying asset. This deal allows them to share in the upside through USDC supply growth and the resulting revenue, without having to engage directly in a jurisdiction battle they are unlikely to win outright. They only capture a portion of the economic benefits, but it's a scale Coinbase cannot achieve on its own.

Tether Is Replicating the Same Playbook

Tether is also executing its own version, albeit on a much smaller scale. Following the attack on Drift in April, Tether committed up to $147.5 million to support its recovery. This deal made USDT the settlement asset for Drift, established Tether-backed USDT credit lines for designated market makers, and funded incentives for traders.

In other words, Tether leveraged Drift's crisis to change the base currency of a major Solana perpetual contract DEX. Prior to this deal, USDC's stablecoin presence on Solana was more than double that of USDT, a pattern common across the entire Solana chain.

Both sides of the stablecoin war have realized the same thing: the perpetual contract market is a critical battlefield in the stablecoin competition.

Overall, to capitalize on the growth momentum generated by the GENIUS Act, Coinbase and Circle need more distribution channels. The Hyperliquid deal may be precisely such an entry point: enabling USDC to spread within the core scenarios of on-chain trading, entering one of the fastest-growing categories in the crypto industry, and gaining the potential to compete on equal footing with USDT and Binance.

This might also be a bet on the further opening of U.S. domestic regulatory boundaries. CFTC Chairman Selig has explicitly stated a desire to allow perpetual contract trading in the U.S., and the passage of the CLARITY Act could ensure this. Reports this week indicate that the SEC is preparing to introduce an "innovation exemption" under its Project Crypto initiative, allowing crypto-native platforms to offer on-chain trading of tokenized U.S. stocks under lighter registration requirements.

Combining the stance of the CFTC under Selig's leadership with the SEC's direction under Atkins, Coinbase seems to be positioning itself in advance: enabling Hyperliquid to gain distribution capacity in the U.S. market, with USDC already installed as the core asset.

Bankless previously reported on the arriving window of opportunity for perpetual contract trading.

Of course, the above is still speculative. But it does align with how Wall Street and institutional players might view Hyperliquid: as an entry point into the future regulatory framework for perpetual contracts. For an asset, this is arguably one of the most attractive tailwinds.