SpaceX造富潮下的「盲盒股東」:層層套娃,誰在裸泳?

- 核心觀點:SpaceX等明星公司長達24年的私有期催生了龐大的私募二級市場,其中大量SPV(特殊目的載體)層層嵌套,導致買家可能無法核實最終資產的真實性,構成「開盲盒」式的交易,而公司為控制股東數量和監管風險正逐步收緊二級轉讓。

- 關鍵要素:

- SpaceX 2026年IPO估值達1.75兆美元,其私募二級市場已膨脹至2300億美元規模,催生出至少170個圍繞其股份的SPV,部分嵌套深度達五層。

- 每一層SPV都會產生費用(如6%設立費+管理費),導致實際投資縮水;且底層買家無權核實其份額是否對應真實股份,只能依賴上層仲介。

- 公司私有期延長(從1980年的6年至2024年的13年半)使股份反覆流轉,加上SpaceX自身透過優先購買權和回購嚴管交易,推高了外部市場的溢價。

- 為規避美國「股東超2000人須公開財報」的監管紅線,並保護選擇權定價和經營資訊安全,Anthropic、Figure AI等公司正公開聲明未經授權的二級交易無效。

- SpaceX上市文件將首次提供可核對的股東名冊,屆時多年嵌套交易的合法性將接受檢驗,可能揭露部分SPV底層的「空殼」風險。

A couple of days ago, the Wall Street Journal published a report about a little-known hedge fund named Darsana Capital.

Founded in 2014, the fund was relatively small. In 2019, it made a decision: bet on a rocket company that hadn't gone public yet. At the time, SpaceX was valued at around $30 billion.

Seven years later, SpaceX is about to go public at a valuation of $1.75 trillion. Darsana’s roughly $600 million invested over those years is now worth about $15 billion. This single bet ranks among the most profitable hedge fund trades in Wall Street history. SpaceX alone accounts for nearly 60% of Darsana's total assets.

SpaceX, the largest IPO ever, also kicks off this year's wave of tech company listings. Stories like Darsana's have been frequently appearing in the news lately. Google invested $900 million in 2015, now worth over $100 billion. Founders Fund’s $20 million lifeline investment in 2008 has ballooned to $19.5 billion.

But when you flip to other reports, the scene changes completely.

At the end of March, Bloomberg and Reuters both reported a strange incident: a group of investors bought SpaceX shares but couldn't confirm whether they actually owned any. One entrepreneur, Tejpaul Bhatia, believed he held SpaceX stock but couldn't verify if the shares supposedly belonging to him were real or fake.

On one hand, there are wealth creation myths precise to the billions. On the other, there are people who can't even confirm if they bought anything. The same company, the same IPO – why is there such a split?

The Private Secondary Market Driven by "AI Anxiety"

Over the past two or three years, AI has driven valuations in the primary market to absurd heights.

Companies like OpenAI, Anthropic, xAI, and SpaceX boast valuations in the hundreds of billions or even trillions of dollars, and they are still rising rapidly. For ordinary investors looking at these numbers, only one thought remains: I want a piece of that too.

There have never been more people wanting to get in. The problem is, none of these companies are public. For the average person, finding a way to buy in before the IPO is nearly impossible.

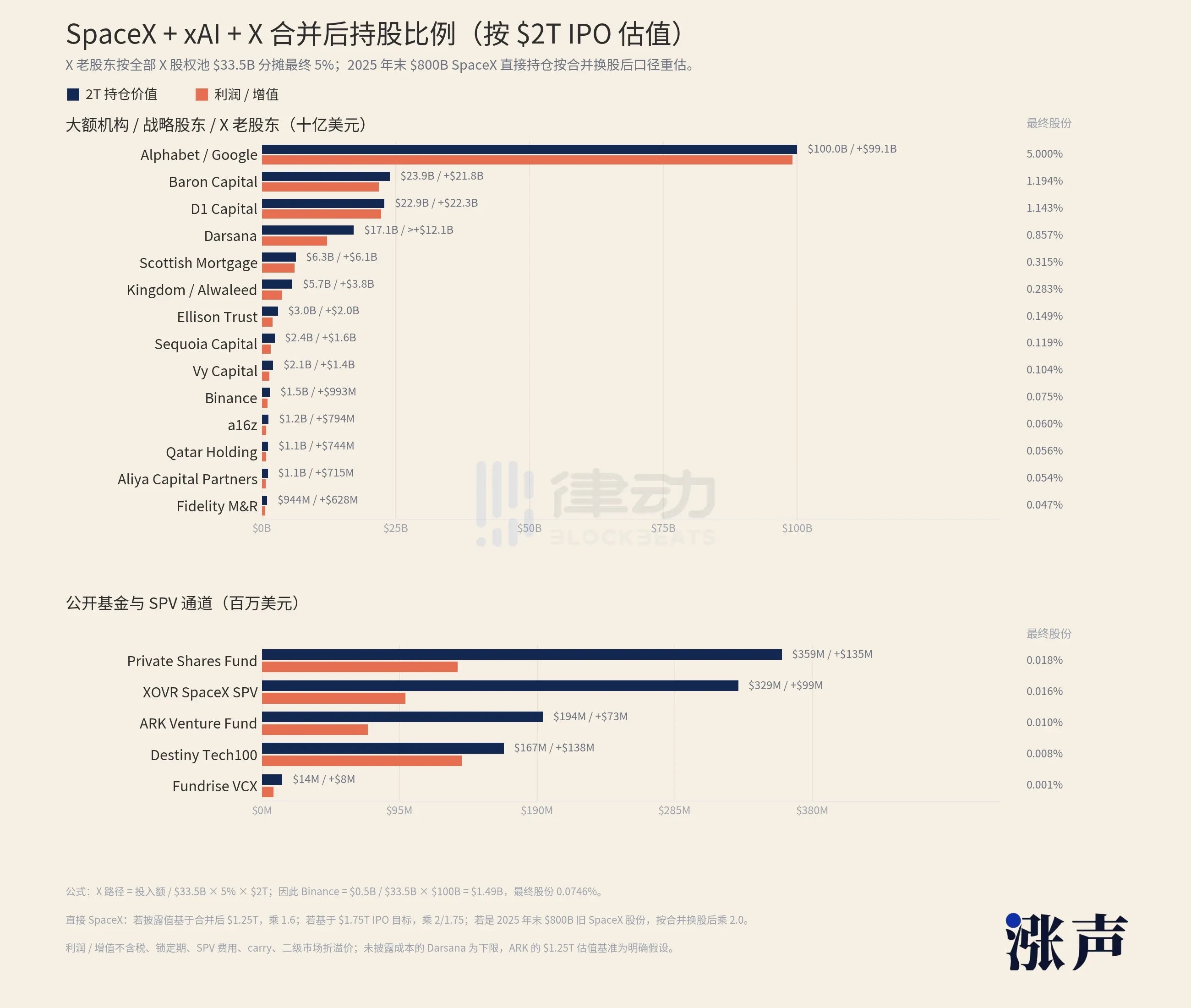

Just look at SpaceX's shareholder list. Large institutions and strategic shareholders hold positions worth tens or hundreds of billions of dollars. Alphabet, Google's parent company, holds over one hundred billion alone. All publicly accessible channels – a few ETFs and funds holding SpaceX – offer a combined exposure of only about $1 billion.

Estimated based on a $2 trillion valuation, how much profit could SpaceX's investment institutions make?

Moreover, most avenues lock ordinary people out. Most channels in the private market are only open to accredited investors. In the US, this means an annual income exceeding $200,000 or net assets (excluding primary residence) over $1 million. Those who don't meet these thresholds can't even squeeze through the $1 billion crack.

For anything else, such a disparity would make people back off. But FOMO works in reverse. The more scarce something is, and the more you see others profiting, the more you want to get in.

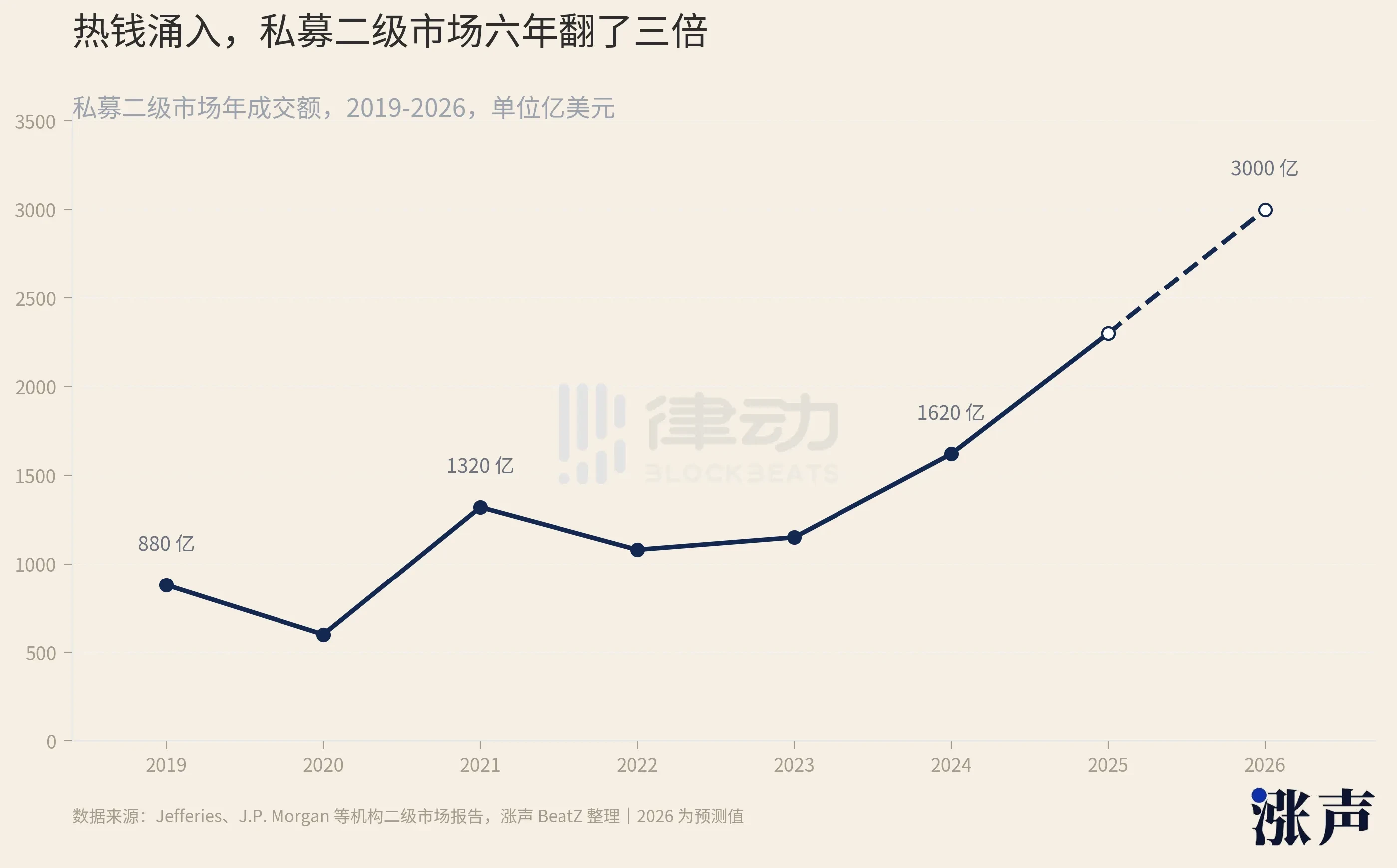

The money didn't retreat. It flowed into a place called the private secondary market.

This market specializes in buying and selling shares of unlisted companies. Early investors and employees wanting to cash out, and those who missed the early boat wanting to get in, along with the platforms, funds, and various vehicles that facilitate these transactions, constitute this market.

In recent years, it has swollen beyond belief. It has tripled in size since 2019. The total transaction volume was approximately $162 billion in 2024, rose to around $230 billion in 2025, and is expected to reach $250 billion in 2026. The number of companies willing to open their shares for secondary transfers jumped from 12 to 31 within a year.

As money poured in, sellers of SpaceX poured out.

How many exactly? According to the New York Times, there are at least 170 Special Purpose Vehicles (SPVs) that have bought SpaceX shares. An SPV is a shell: someone gets some SpaceX shares, puts them into the shell, and sells shares of that shell to subsequent investors. 170 shells, all wrapped around the same company.

These shells come from all sorts of backgrounds.

In October 2025, an institution called Witz Ventures launched an SPV on the fundraising platform Republic, named The Cashmere Fund. This shell bundled three of the hottest targets – xAI, SpaceX, and Perplexity – and sold them to retail investors. About 150 listeners of the financial podcast Rich Habits also jumped the queue into SpaceX through a group purchase. Rapper 2 Chainz and SkyBridge founder Anthony Scaramucci have both publicly stated they own SpaceX.

Retired NBA player Tristan Thompson stated on a show that he invested in SpaceX when its valuation was $300 billion.

The problem is, the quality of these middlemen popping up everywhere is uneven.

One institution, Vika Ventures, collected $5.9 million from investors, promising to buy SpaceX shares. It was later discovered that the founder used the money to buy luxury watches and a private jet. In 2023, another financial broker was sentenced to eight years for defrauding over 50 investors of nearly $6 million, also selling pre-IPO shares including SpaceX.

Another once-popular platform, Linqto, which focused on star targets like SpaceX, went bankrupt in 2025. The SEC is investigating whether it properly verified users' accredited investor status, affecting over 13,000 investors.

Even if you don't encounter a scammer, things aren't necessarily clear.

DataPower Capital is an institution dealing in SpaceX shares. Its founder, David Yakobovitch, told the New York Times that he only accepts transactions one layer removed from SpaceX. "Go a few more layers down," he said, "and things start to get murky."

Nested Five Layers Deep

Let's go back to those 150 podcast listeners from Rich Habits. They didn't buy SpaceX.

They bought into Witz Ventures, and Witz Ventures bought shares of DataPower Capital. DataPower is the one that directly acquired stock from a registered SpaceX shareholder. In other words, between an ordinary person placing an order after listening to a podcast and the actual SpaceX stock, there are at least two or three layers of shells.

For each additional layer, two things happen simultaneously.

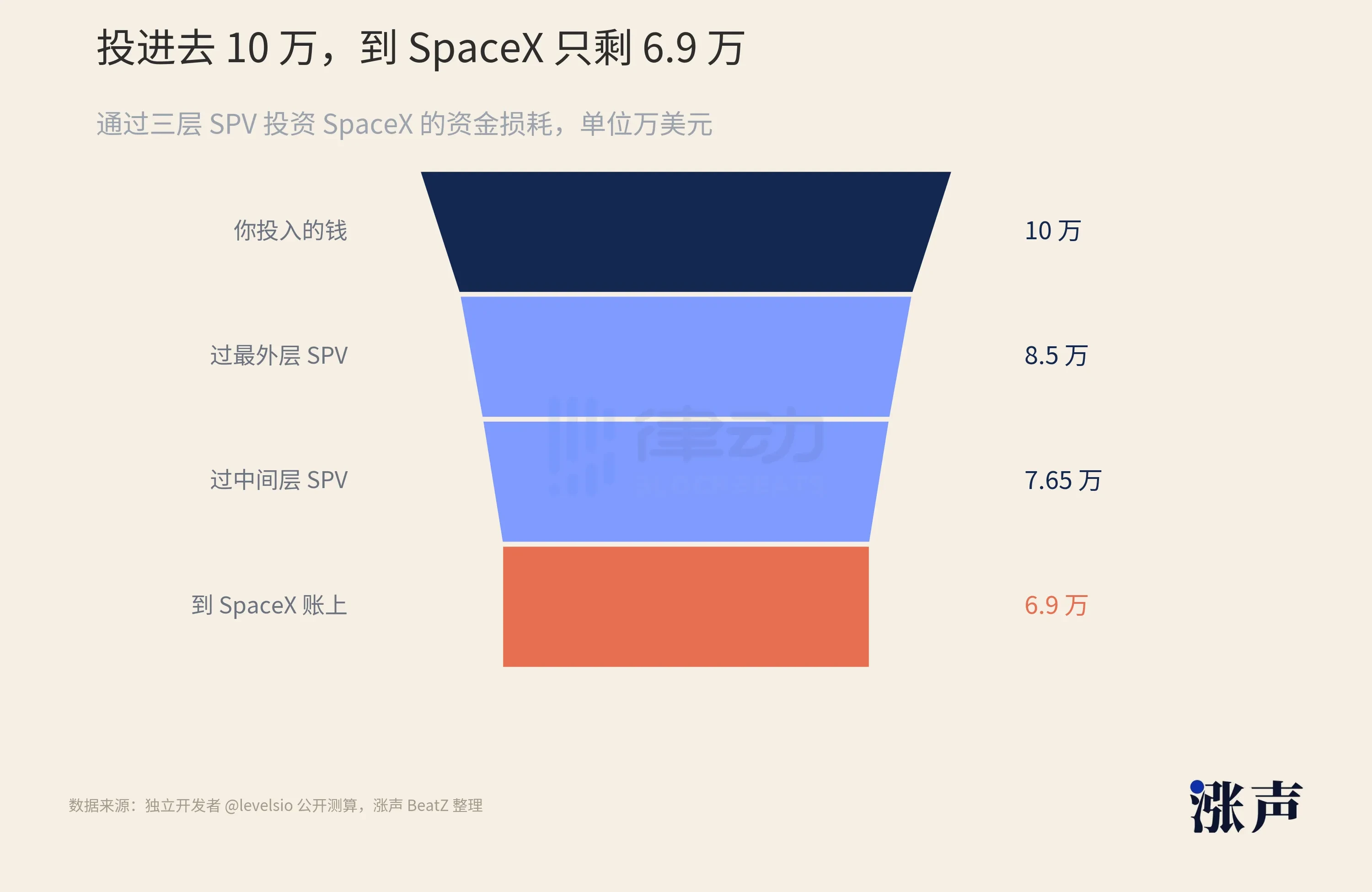

First, the money dwindles. Independent developer levelsio calculated on social media: Suppose you invest $100,000 in SpaceX through three layers of SPVs. The outermost layer charges a 6% setup fee, and the inner two layers each take management fees and profit shares. The money that actually reaches the underlying SpaceX shares is only about $69,000. Before you've even started to profit, 30% is gone.

Second, the truth becomes more distant. A critical feature of this SPV structure is that investors in each layer can only see the layer directly above them. You buy the outermost shell, and its manager tells you it holds the next shell. Is the next shell real? Is there really SpaceX stock underlying it all the way down? You can't see it and have no right to check.

With 170 shells, the deepest nested structures even go five layers deep. This is why Bhatia and others can't confirm their holdings. It's not because they aren't careful enough; the system is designed so that those outside the shell can't see inside.

Why could SpaceX's matryoshka doll structure nest so deeply?

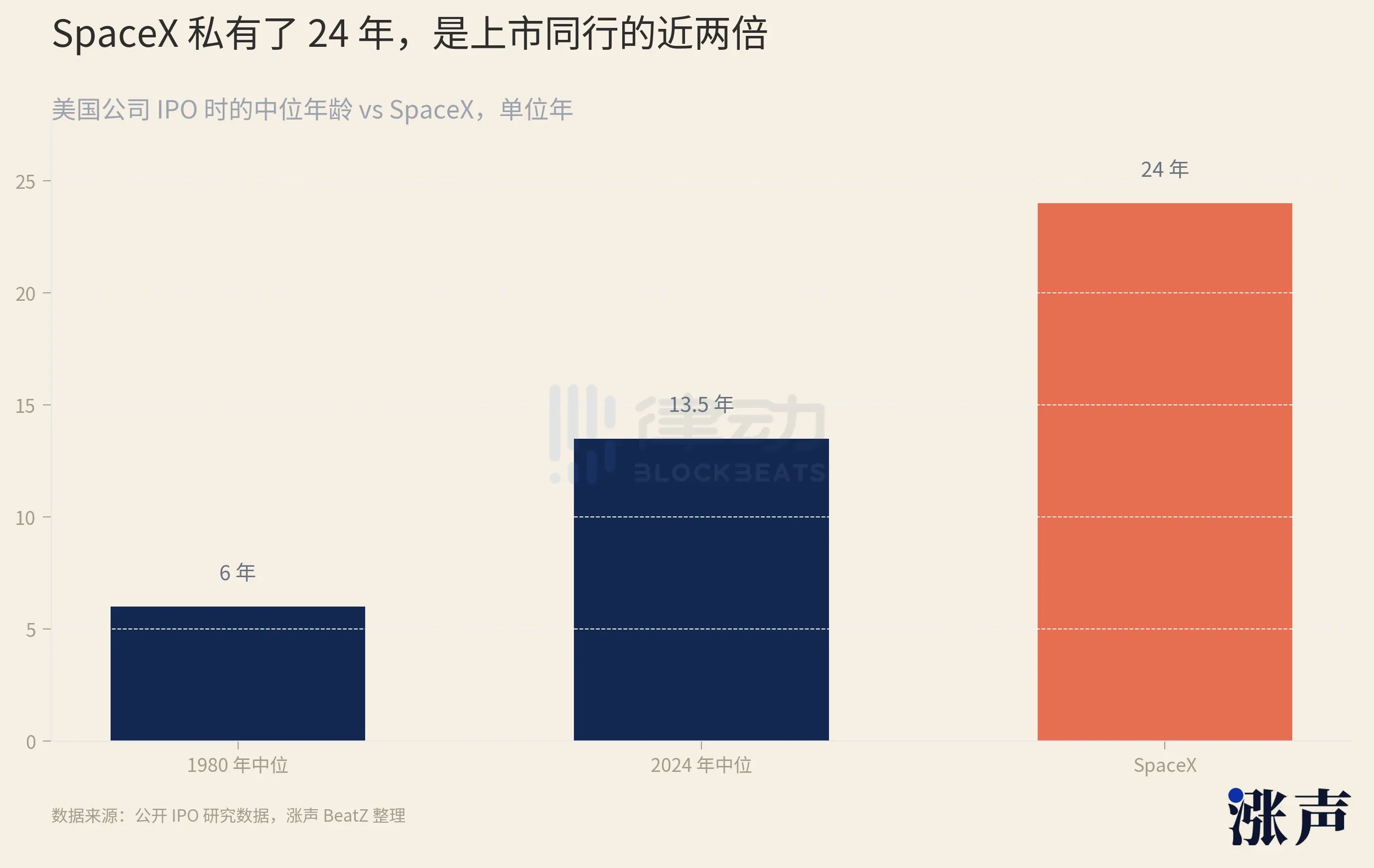

That depends on how long it has remained in the private market. Founded in 2002 and going public only in 2026, it has been private for a full 24 years.

What does 24 years mean? The average tech company going public in 1999 was founded only 4 years prior. For the 2014 cohort, the average was 11 years. In recent years, the median age of US companies going public has stretched to 14 years. SpaceX's 24 years is an extreme even on this already lengthening curve.

The longer a company stays in the private market, the longer its shares are traded, transferred, and re-shelled. SpaceX shares have circulated over-the-counter for over two decades, accumulating more and more layers of shells outside.

The lengthening private period isn't unique to SpaceX.

The median age of US companies going public has risen from 6 years in 1980 to 13.5 years in 2024. The reason isn't complicated: there's simply too much money in the private market.

As of 2023, global venture capital firms still held over $650 billion in uninvested capital. Companies don't lack funding, so they are in no rush to go public and face public market earnings pressures and regulations. Consequently, the number of unicorns (companies valued over $1 billion) has piled up. There are now over 1,500 globally, worth a combined $6 trillion, most of which haven't raised a round at a public valuation in over three years.

The longer a company stays in the private market, the longer the shares of its employees and early investors are locked up. For these people looking to cash out, the secondary market is the only outlet. The demand is there, and SPVs specifically designed to meet this demand pop up in droves.

During the peak of venture capital in 2021, the number of newly established SPVs in the US rose by 235% year-over-year. By the third quarter of 2024, there were over 2,400 SPVs still countable and operational. When a tool is used so massively and repeatedly for over twenty years, nesting five layers deep is almost an inevitable outcome.

And SpaceX happens to be one of the strictest companies in the private market regarding its stock. Externally, SpaceX exercises its right of first refusal on almost every share transfer, intercepting trades in advance. It conducts share buybacks every six months, purchasing shares employees want to sell and bringing them under its own controlled umbrella.

The tighter the door is welded shut, the higher the price of the tickets outside.

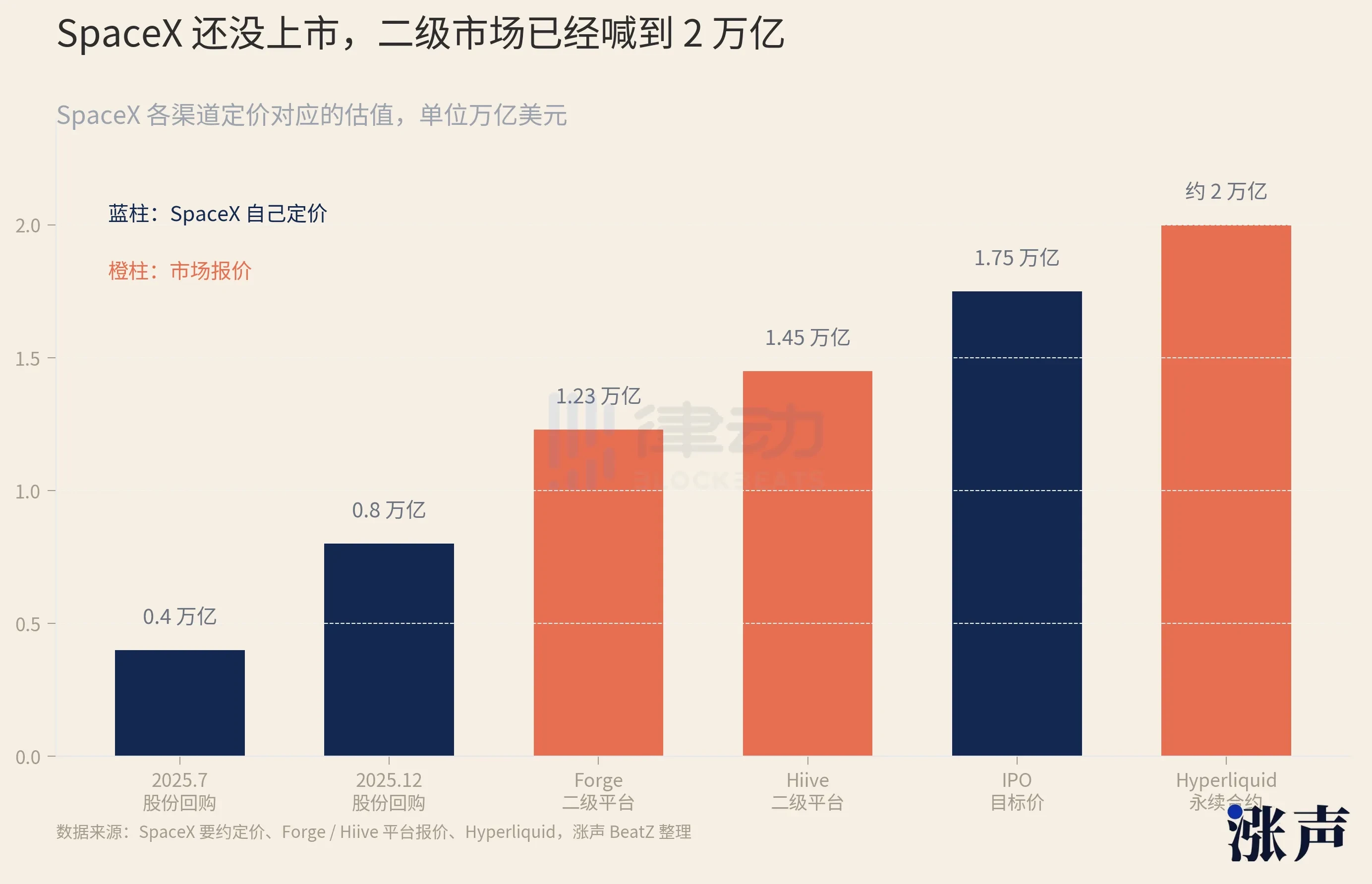

SpaceX's own pricing is calculated: a share buyback in July 2025 corresponded to a $400 billion valuation; six months later in December, that doubled to $800 billion. But secondary market quotes had already run ahead. The Forge platform quoted around $1.23 trillion, Hiive had $1.45 trillion, and contracts listed on crypto exchange Hyperliquid even corresponded to over $2 trillion – higher than SpaceX's own target IPO valuation.

Adding to the tangled mess are mergers. In March 2025, Musk merged X (formerly Twitter) into his AI company, xAI. In February 2026, SpaceX then acquired xAI entirely. Those who bought Twitter and xAI back then, along with their entire set of shells, were all connected to SpaceX's shareholder registry through two stock swaps.

Opening a Mystery Box

At this point, even the companies themselves got nervous.

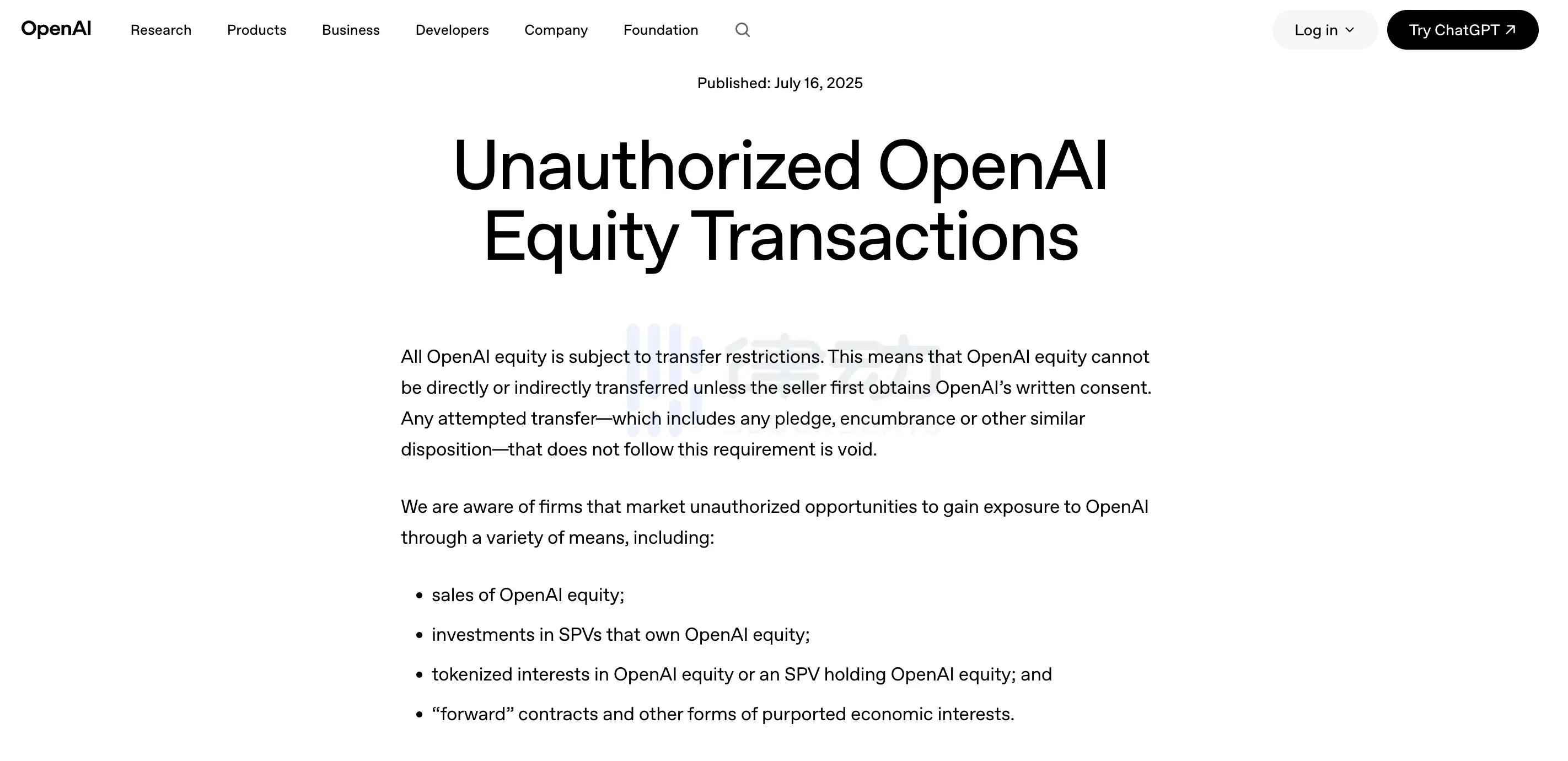

In May 2026, Anthropic and OpenAI both issued public statements, clearly telling the market that any share transfers not approved by the board of directors are void and will not be recorded in the company's books. They named names, listing eight platforms including Forge and Hiive as unauthorized. The news caused the relevant linked tokens on pre-IPO on-chain secondary markets to crash instantly, losing 30-40% in a single day.

This kind of announcement against secondary market trading isn't a whim of just one or two companies.

Recently, robot company Figure AI, amidst reports of a $39.5 billion valuation, also stepped in to block secondary trading of its shares. Almost all the hottest targets in the private market – Anthropic, SpaceX, Anduril, Stripe, Databricks – are doing the same thing: turning their tolerance for secondary trading down to zero.

Why did they collectively turn hostile?

This brings us to a seldom-noticed IPO "red line." Under US rules, if a company's shareholder count exceeds 2,000, even if it's not public, it must regularly disclose its finances like a public company. Nesting SPVs makes it impossible for companies to know exactly how many shareholders they have. One SPV counts as one on the register but might hold hundreds of people behind it. If a company inadvertently crosses the 2,000 line, it is forced to open its books.

Another reason relates to pricing employee stock options. If a company's shares are freely traded and driven to high prices in the secondary market, the company can't ignore that number when setting the exercise price for employee options. The crazier the secondary market, the less valuable the employees' options become.

More critically, it's about information. Shareholders have the legal right to obtain the company's operational information. For AI companies, model architecture, training data, and compute arrangements are the most sensitive internal secrets. When a company can't even count its own shareholders, it also can't control who is receiving this information.

Cleaning up countless shareholders, safeguarding option pricing, and closing information leaks – none of these issues is new individually. But when the secondary market swells to $230 billion and nesting reaches five layers, companies find they can't control it through private means anymore. So they step onto the public stage, writing "Your shares are invalid" in their first public announcements for the first time. SpaceX hasn't followed with a similar statement, but its right of first refusal system already does the same thing.

The company's pronouncement of "invalidity" leaves those several-layered shells hanging in the air. You buy an SPV and pay the money. Whether the underlying SpaceX shares in that tranche were ever approved or count for anything – no one can give you an answer until the company publicly reconciles its books.

Thus, buying a SpaceX SPV feels increasingly like opening a mystery box.

When the box opens is fixed. On June 12, SpaceX rings the bell on Nasdaq. In its IPO filing, for the first time, there will be a public, verifiable shareholder register. Every single layer of shell that has wrapped around its stock over the past 24 years will be reconciled at that moment. If it matches, the box contains real stock; if not, it's a worthless piece of paper. On that day, Bhatia will find out which one he got.

But after SpaceX, there's OpenAI, and Anthropic, and a long list of names waiting. Swipe through your social feed, and you'll see countless posts from agents promising shares of these hottest AI companies.

The hot money generated by AI in recent years has nowhere to go. The truly worthwhile targets are few and are all locked up tightly. Too much money, too narrow a door, and countless shells grow in the middle.

As long as this imbalance persists, the private secondary market will remain what it is now: a mystery box that everyone wants to play, but no one can really tell what they've drawn.