Money is flowing into bonds and IPOs, leaving only HYPE rising in the crypto space

- Core Viewpoint: Global capital is currently systematically withdrawing from the crypto market, rotating into the bond market (5% yield) and traditional IPOs (a $4 trillion queue), leading to pullbacks in mainstream assets like BTC, ETH, and Solana. Meanwhile, Hyperliquid is bucking the trend by connecting to traditional asset Pre-IPO trading.

- Key Factors:

- The 30-year US Treasury yield has risen to 5.12% (the highest since 2007), and long-term government bond yields in G7 countries are approaching 5%, causing global capital to shift towards assets with deterministic returns.

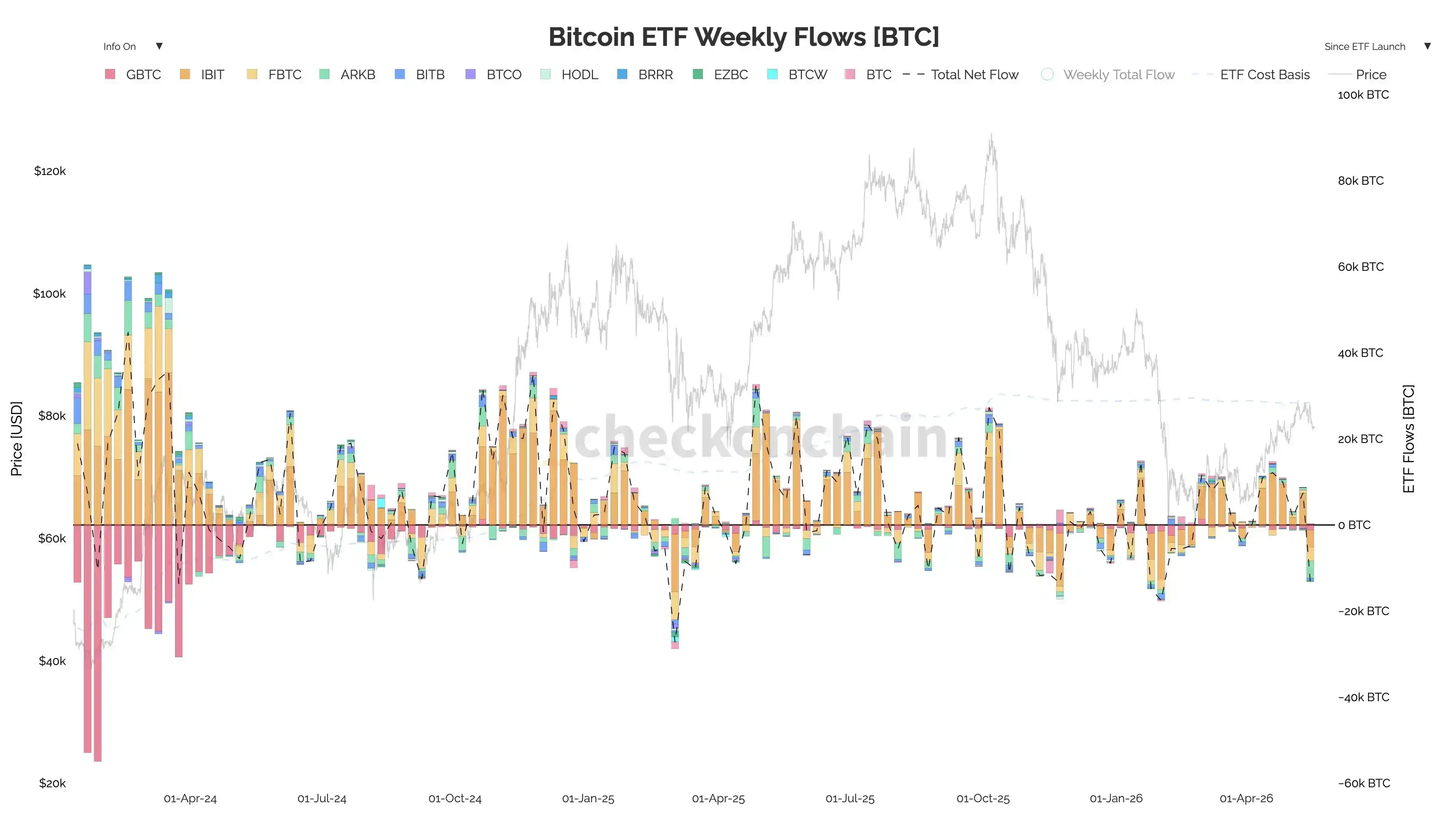

- Bitcoin spot ETFs saw a net outflow of $1.039 billion in the week of May 11-15, ending six consecutive weeks of net inflows. ARKB and IBIT alone recorded outflows of $324 million and $317 million, respectively, for the week.

- An estimated $4 trillion IPO pipeline is expected in 2026 (including SpaceX), and surging AI capital expenditure is diverting risk capital away from crypto asset allocation.

- SpaceX's Pre-IPO contract on Hyperliquid recorded $40 million in trading volume on its first day. The HIP-3 platform directs on-chain liquidity towards traditional stock pricing rather than crypto-native assets.

- New Federal Reserve Chairman Warsh faces the contradiction between political pressure to cut interest rates and the bond market's high inflation expectations (five-year inflation expectation at 2.7%). Market bets on rate cuts may be overturned.

Where did all the money go?

The S&P 500 hit a new all-time high last week, and the Nasdaq ended its seven-week winning streak. The 30-year US Treasury yield surged to 5.12%, the highest since 2007. SpaceX's Pre-IPO contract on Hyperliquid recorded $40 million in trading volume on its first day.

Money is flowing everywhere except crypto. BTC only just stood above $82,000 on May 14th, but has since plummeted below $77,000 in the last two days. ETH hasn't fared well either, dropping nearly 10% in a week, falling from the $2,300 range to $2,110. Solana has completely given back its recent gains, falling from a high near $100 back to $84. Apart from HYPE, it seems no major crypto asset is holding up well.

Both are considered risk assets, so why is crypto the only one falling behind?

30-Year Bond Yield Hits Nearly 20-Year High

The bond market is once again becoming the gravitational center for global capital.

The 30-year US Treasury yield has reached its highest level since June 2007, rising from 4.63% at the end of February to 5.12%. Meanwhile, the 10-year yield touched 4.6%, and the 2-year yield rose to 4.08%.

This isn't just a US phenomenon. Torsten Slok, Chief Economist at Apollo Global Management, stated in his report on Sunday, May 17th, that yields on 10-year or longer-term government bonds in G7 countries have all reached their highest levels since 2004, collectively approaching 5%.

Governments worldwide are expanding their fiscal deficits, needing to borrow more and issue more bonds. The US fiscal deficit remains around 6% of GDP. Rising borrowing costs make it harder for governments to spend their way out of crises, precisely when many countries face crises due to wars.

Deutsche Bank's Jim Reid noted in a May 18th report that the bond issue is likely to be on the agenda of the two-day G7 Finance Ministers meeting that opened in Paris that day. However, the structural problems in the bond market are not something any single ministerial meeting can solve.

At a time of heightened geopolitical tension, global capital favors assets offering certain returns.

The data outflows from Bitcoin ETFs support this point.

According to SoSoValue data, Bitcoin spot ETFs saw a net outflow of $1.039 billion in the week of May 11th to May 15th, ending a six-week streak of net inflows. This was also the largest single-week outflow since the end of January.

Looking at specific products, ARKB saw a net outflow of $324 million in a single week, and IBIT saw a net outflow of $317 million, with both leading products bleeding simultaneously. The daily data paints an even sharper picture. There was a net outflow of $233 million on May 12th, a massive $635 million drained on a single day, May 13th, and the 11 Bitcoin ETFs saw a combined further outflow of $290 million on Friday, May 15th, indicating an orderly retreat of institutional capital.

Comparing data from previous weeks reveals the magnitude of this reversal. The week of April 17th saw net inflows of nearly $1 billion, the week of April 24th saw inflows of $824 million, and even the week of May 8th had net inflows of $623 million. The capital flows reversed from "sustained inflows" to a "single-week outflow of $1 billion" within just one week.

During the same period, Ethereum ETFs also saw a net outflow of $255 million, marking five consecutive days of negative flows. The entire crypto ETF asset class experienced a collective turnaround in mid-May.

As the bond market becomes more attractive, the relative appeal of crypto naturally diminishes.

$4 Trillion in IPOs: How Can Crypto Compete?

Bonds are siphoning off risk-free capital. IPOs, on the other hand, are competing for risk capital, which arguably represents the most direct liquidity drain for crypto.

In 2026, a staggering $4 trillion worth of IPOs are queued up, vying for capital. This is a figure capable of reshaping the global capital allocation landscape.

SpaceX has become the next major market focus. In this environment, Pre-IPO and IPO subscription strategies offer an allure that bonds cannot: the potential for non-linear wealth effects.

Meanwhile, the AI narrative remains the dominant theme of 2026. An Evercore analyst noted in a May 15th report that US economic data shows demand remains strong, especially with a surge in AI-related capital expenditure. The flip side of this AI spending boom is the life-changing wealth creation by leading AI companies in the secondary market.

The return efficiency of names like Nvidia and Cerebras makes any crypto narrative seem less compelling.

More strikingly, even on-chain platforms are helping traditional markets raise capital.

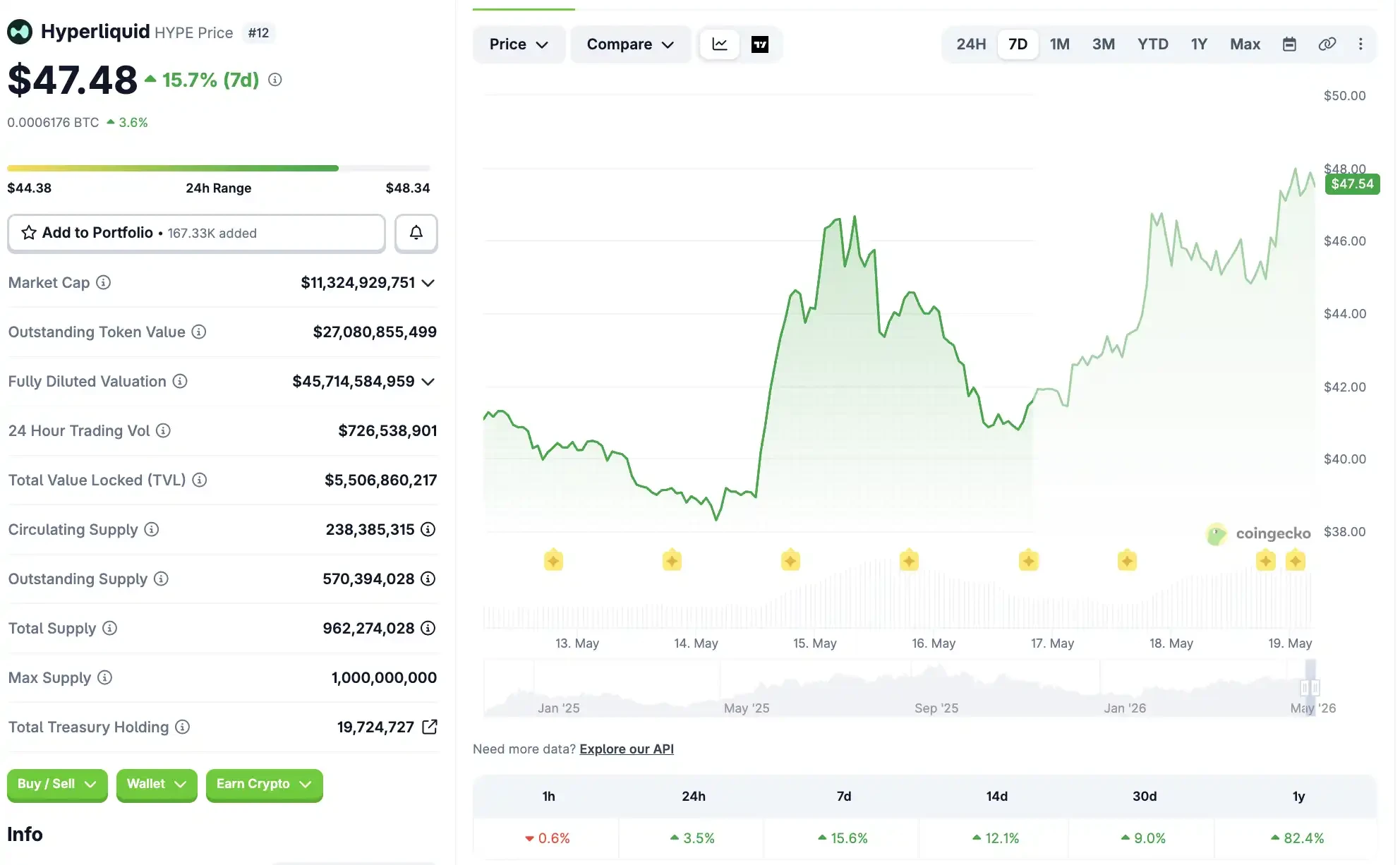

The night SpaceX launched on Trade.xyz, the Pre-IPO contract on Hyperliquid recorded $40 million in trading volume on its first day. The HIP-3 platform is using perpetual contracts for price discovery on traditional stocks. Hyperliquid itself rose 10% to $45 during the week, becoming one of the few mainstream crypto assets to buck the downtrend. Related reading: The Biggest Winner of the SpaceX IPO Might be Trade.xyz.

In the short term, this isn't good news for native crypto assets.

On-chain liquidity is being redirected to price traditional stocks like SpaceX, rather than flowing back into Bitcoin, ETH, or Solana. Even Hyperliquid's price increase is essentially a spillover benefit from traditional asset narratives, not a crypto-native one.

Warsh Takes Office, But Rate Cuts May Be Off the Table

The bond and IPO markets are draining liquidity from the crypto space. Looking at the Fed, the new liquidity we were hoping for might not materialize either.

Powell's term ended on May 15th. Warsh was confirmed by the Senate as the new Fed Chair last week and is now awaiting final approval from the official Presidential Appointment Commission and completing asset divestitures to comply with ethics rules.

Before Warsh is even formally sworn in, he already faces significant challenges.

Trump nominated Warsh partly hoping he would be more aligned with the White House's cost-reduction agenda than Powell. Treasury Secretary Bessent has spent the past few months placing the reduction of government borrowing costs at the core of the White House's cost-cutting promises. In his speech at the New York Fed last autumn, he clearly stated that lowering government borrowing costs means lowering corporate borrowing costs, mortgage rates, and car loan payments, thereby improving affordability for all Americans.

However, as mentioned earlier, the reality today is that the bond market has pushed the 5-year inflation expectation to 2.7%, the highest since 2023. A May 17th report from Yardeni Research directly points out that the 2-year Treasury yield of 4.08% is the market telling the Fed, through prices, that the current target range of 3.50%-3.75% is set too low.

According to Warsh's own logic, he should continue raising rates, or at least not cut them. But the White House, and Trump personally, have made their political desire for rate cuts almost public.

On the other hand, if you've heard Warsh's testimony before his confirmation, you would know he spent considerable time discussing AI. He believes AI will boost productivity and suppress inflation, thus supporting rate cuts. The problem is that short-term data shows no signs of this happening.

Interactive Brokers' Senior Economist José Torres' view likely represents a large portion of market participants. In his May 15th report, he concluded that due to a lack of progress on geopolitical conflicts, the market has abandoned bets on the tightening of interest rate space.

If Warsh chooses to succumb to Trump's political pressure and cuts rates forcibly, the bond market will respond with higher long-end yields, making things worse for all duration-sensitive assets. If Warsh chooses a hawkish stance, expectations for rate cuts this year will completely evaporate, forcing a repricing of all bets on liquidity easing.

This means the market's bets over the past few months, anticipating rate cuts after Warsh took office, may be completely overturned.

HYPE Leads the Crypto Charge

After October 10th, the recovery phase following the crypto market leverage wipeout should have depended on fresh capital inflows.

With $4 trillion in IPOs queued up for 2026 and AI names continuing to generate wealth effects, the appeal of trading altcoins in this environment is continuously diluted. Even Bitcoin, the most institutionally-oriented crypto asset, is starting to cede ground to traditional markets. The weekly outflow of $1 billion from ETFs is the most direct evidence.

High bond market interest rates lead to Bitcoin ETF outflows. The recovery phase is stretched indefinitely, preventing crypto from ever regaining the broader rally pace of risk assets.

However, it's worth noting a divergence emerging within the crypto market itself.

Hyperliquid rose 15% for the week to $48, with a year-to-date gain of 69%, driven by the Pre-IPO price discovery narrative on HIP-3. Assets that can tell new stories and capture the entrance to traditional markets continue to rise, while assets relying purely on beta are being compressed by pricing, even forcing Bitcoin to take a backseat.

Zooming out to look at the overall financial market reveals that three forces have been simultaneously draining crypto liquidity over the past few weeks. The bond market pulls risk-free capital back with 5% yields. IPOs consume incremental risk budgets with a $4 trillion pipeline. And the new Fed Chair, Warsh, may not deliver the expected rate cuts this year.

However, there might be some positive catalysts for Bitcoin in the next phase.

The upward catalyst is the enactment of the CLARITY Act in August. This is the biggest policy tailwind for crypto this year, with increased regulatory clarity potentially unlocking some pent-up institutional demand.

The downside risk is potentially retesting the $70,000 level before the catalyst materializes. If the current $77,000 level fails to hold, the next significant support is likely around $70,000.