零資金費率?老外都在聊的HyperEVM新合約設計

- 核心觀點:加密交易員Jez在HyperEVM上推出新型永續合約協議PaperTrade,採用無手續費、無滑點、無資金費率模式,但本質上是一種用戶與LP池對賭的機制,並通過代幣PAPER將交易虧損轉化為平台股份。

- 關鍵要素:

- PaperTrade讀取Hyperliquid報價但不撮合訂單,交易在用戶和公共LP池之間直接結算,類似歷史上的「bucket shop」對賭模式。

- LP池不接受外部存款,僅依賴用戶虧損的保證金;用戶盈利部分通過鏈上債權佇列排隊,等待後續虧損單填補。

- 代幣PAPER根據用戶虧損數量按曲線鑄造,LP餘額低於200萬美元時每虧損1美元鑄造100枚PAPER,超過後鑄造速率衰減。

- PAPER質押者可獲得協議抽水收入和LP池超過500萬美元後的所有超額部分,形成「輸家獲得股份、贏家取走輸家錢」的閉環。

- 參與策略建議在LP池TVL低位時虧損鑄造PAPER,TVL高位時質押PAPER坐收分紅。

Crypto trader Jez announced today the development of PaperTrade, a new protocol on HyperEVM, sparking heated discussions in the English crypto community.

Jez is a long-time advocate of perpetual contracts. He took a heavy early position in Hyperliquid, and his account address ranks high on Lighter and Variational's airdrop leaderboards. This time, he's building it himself, launching a Perp DEX with zero fees, zero slippage, and no funding rate.

The Ancient Bucket Shop Goes On-Chain

PaperTrade's mechanism has a disreputable predecessor in financial history. In early 1900s small American towns, bucket shops operated under the guise of securities firms. Clerks would chalk up real-time quotes from the NYSE on a board behind the counter, but customer orders never left the shop owner's drawer. Essentially, customers were betting against the shop owner. This business was outlawed by New York State in 1909 and was largely extinct by the 1920s.

When a user opens or closes a position on PaperTrade, the platform directly reads order book prices from Hyperliquid, and settles the difference between the entry and exit price against a public LP pool. No order ever enters Hyperliquid's matching engine, and no actual perpetual contracts change hands. The transaction is always between the user and the LP pool, with no third-party counterparty.

Perpetual Contracts + P2P + DeFi Ponzi

PaperTrade simultaneously borrows models from DeFi yield farming and P2P lending.

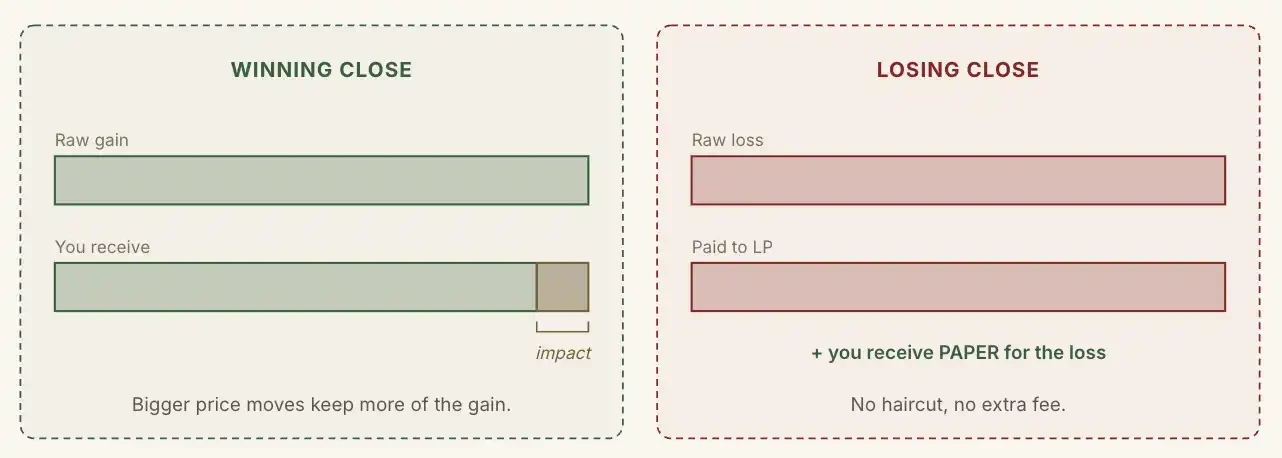

User losses on PaperTrade go directly into the protocol's LP pool, while user profits are skimmed by the platform. The smaller the price fluctuation, the more profit is taken. In other words, the more you earn, the less the protocol skims.

Unlike HLP, PaperTrade's LP pool has no team pre-deposit, no VC funding, and doesn't accept any form of external deposit. Its only source of funds is the margin from user losses.

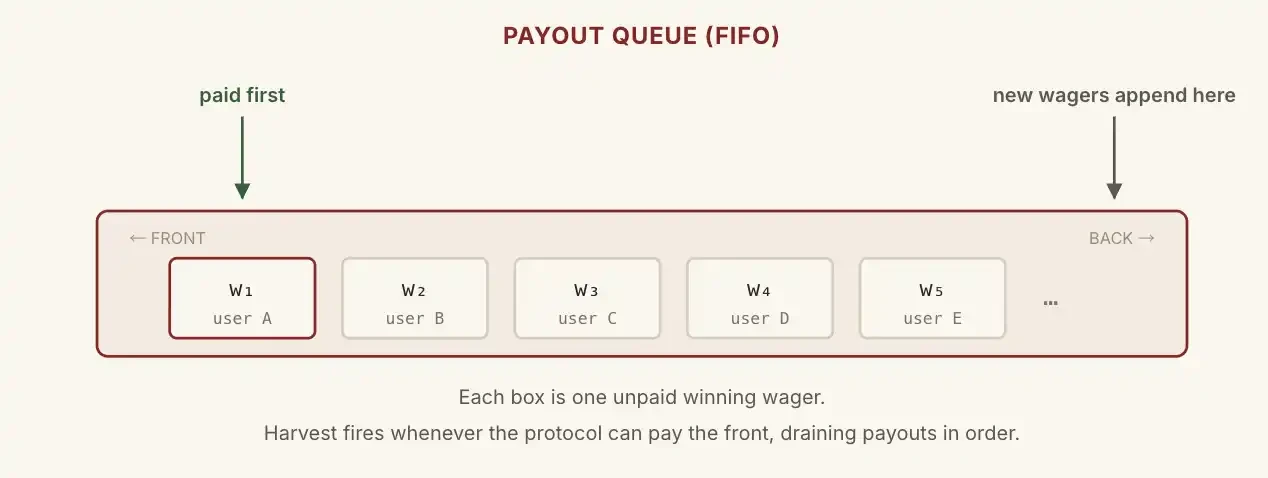

Here's the problem: what happens if the LP pool only has $100, but a user makes $5,000 profit? How does the protocol pay out?

PaperTrade brings the queue system from traditional P2P lending on-chain.

This $5,000 enters an ordered on-chain queue, waiting for the next losing trade to fill the hole. The queue pays out sequentially from the front. A user's principal is always returned immediately; only the profit portion enters the queue.

Theoretically, the LP can become temporarily "insolvent," but every winner will eventually be paid in full, unless the pool of loser funds is insufficient to cover the profits owed to winners.

If it ended here, the project would be doomed to failure. If the LP pool runs dry, winners might have to wait a long time in line to get their profits, naturally having no incentive to trade. As traders leave, even losers disappear, and the platform's debt to winners becomes bad debt.

The essence of PaperTrade lies in its token, $PAPER.

For every dollar a user loses, the protocol mints a certain amount of $PAPER according to a curve.

When LP balance is below $2 million, the minting ratio is fixed at 100 $PAPER per $1 USD lost. Once LP exceeds $2 million, the rate starts to decay. The higher the LP balance, the fewer $PAPER tokens are minted.

X-axis: $PAPER tokens received per unit of loss; Y-axis: LP balance (each grid unit is 1M)

Staking $PAPER entitles holders to two parts of dividends: firstly, the protocol's fee revenue; and secondly, once the LP balance exceeds $5 million, all excess funds are allocated to stakers.

In other words, the LP pool size is designed with a $5 million cap. Beyond this size, all user losses are returned directly to $PAPER holders. This creates a closed loop: "Losers get platform shares, winners take the losers' money, and the platform taxes winners to subsidize losers."

Therefore, a reasonable participation strategy can be summarized as: bet to lose money when the LP pool's TVL is low to mint $PAPER, and stake $PAPER to collect dividends when the LP pool's TVL is high.

A Stress Test for HyperEVM

The author believes PaperTrade's biggest uncertainty lies in its deployment on HyperEVM.

PaperTrade essentially uses Hyperliquid's prices as a free, native oracle, with all remaining logic residing in HyperEVM's smart contracts.

This means any high-performance chain with similar capabilities could replicate PaperTrade's entire mechanism on its own chain simply by integrating an external price oracle. A replicator could even offer what HyperEVM currently cannot: lower gas fees, higher TPS, more generous early subsidies, or more aggressive token incentives.

During the Q1 2025 meme season on HyperEVM, the chain experienced periods of slow transaction speeds and high gas fees. The launch of PaperTrade represents another stress test for HyperEVM.