Q1淨虧損3.941億美元,Coinbase只能緊抱Circle大腿

- 核心觀點:Coinbase 2026年Q1財報顯示營收年減31%且連續兩季淨虧損,核心原因並非僅有市場疲軟,更反映其依賴高溢價的現貨交易業務正面臨用戶流失與競爭加劇,公司正透過裁員降本並押注衍生品、預測市場及穩定幣收入轉型,其中與Circle的穩定幣分潤協議是關鍵的長期收入支柱。

- 關鍵要素:

- 2026年Q1總營收14.1億美元,年減31%,淨虧損3.941億美元,交易收入中散戶部分年減48.2%,已回落至2024年水準。

- 即使剔除加密資產帳面減值(4.82億美元),Coinbase該季度營業利潤仍為負(虧損2140萬美元),顯示核心業務盈利惡化。

- 美國監管成熟導致競爭加劇,超過10家交易所獲牌提供更低手續費服務,散戶用戶開始轉向Robinhood等低成本平台,市場份額上升主要靠衍生品等新產品拉動。

- 公司宣布裁員14%(約700人),表面歸因於AI革命與市場下行,實際為降本增效以應對營收下滑。

- 「萬物交易所」策略下新業務(衍生品、預測市場)Q1最高貢獻7360萬美元收入,遠不及現貨交易主力地位,Base鏈上收入未獨立揭露,長期貢獻存疑。

- 穩定幣收入達3.05億美元,年增10%,占第二大收入來源;與Circle的分銷協議「永不終止」,Coinbase綁定USDC成長紅利,25%流通USDC存儲於其平台。

- Coinbase透過x402協議推廣USDC在AI Agent支付場景應用,預測2030年AI Agent交易量巨大,為未來穩定幣收入增長埋下伏筆。

Original by Odaily Planet Daily (@OdailyChina)

Author: Golem (@web3_golem)

On May 8, Coinbase released its Q1 2026 earnings report. Coinbase CEO Brian Armstrong summarized the quarter during the earnings call, stating, "Despite the weakness in the crypto trading market, Coinbase has performed admirably within controllable limits."

In the earnings presentation, Coinbase highlighted its Q1 achievements, such as its crypto trading market share increasing to a record high of 8.6%; derivatives trading volume TTM (trailing twelve months) growing 169% year-over-year; the prediction market generating an annualized revenue of $100 million in March (only two months after launch); and 12 products generating over $100 million in annual revenue.

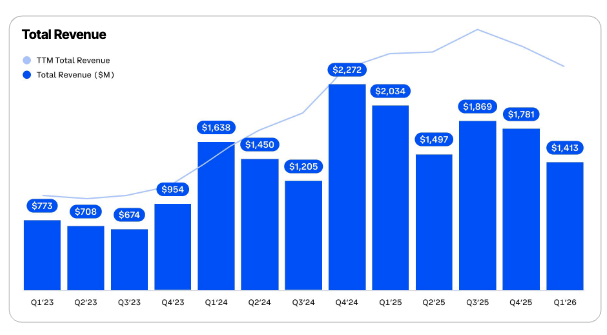

However, no matter how impressive the presentation, it cannot mask the bleak core financial figures for Coinbase in Q1. The report shows that Coinbase's total revenue for Q1 2026 was $1.41 billion, down 31% year-over-year and 21% quarter-over-quarter, missing market expectations. Net loss reached $394.1 million, marking Coinbase's second consecutive quarter of net losses (Odaily note: Q4 2025 net loss was $666.7 million).

Affected by this, Coinbase (NASDAQ: COIN) fell over 5% intraday on May 8, but by the close of trading today, COIN had recovered all its losses, closing at $201.16.

Is the Weak Crypto Market the Sole Reason for Coinbase's Losses?

The stock price decline after the earnings release already reflects the market's concerns about Coinbase's short-term performance, and Coinbase has attributed the main reason for its losses to the weak crypto market. Since Q3 2025, Coinbase's revenue has been declining. Looking at the overall trend of quarterly revenue, the timing aligns perfectly with the crypto market's cycle shifting from bull to bear.

Coinbase Quarterly Revenue

But is a weak market the sole reason for Coinbase's losses? What other potential issues can we uncover from the earnings report?

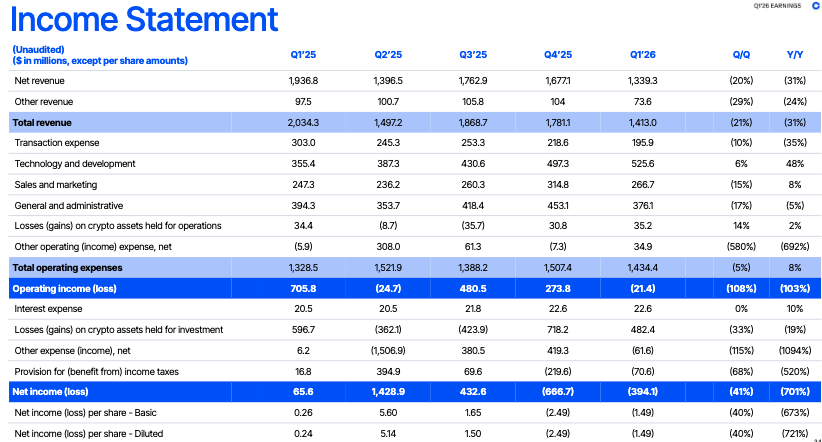

Some analysts believe that Coinbase's Q1 net loss was affected by impairment losses on its crypto asset holdings. The report also shows that digital assets held for investment purposes incurred a loss of $482 million. However, examining Coinbase's Q1 income statement reveals that even excluding these non-operating expenses, Coinbase's operating income for Q1 2026 was negative, with a loss of $21.4 million.

In Q4 2025, also affected by the overall crypto market downturn and weak trading, Coinbase's crypto asset impairment losses amounted to as high as $718.2 million, leading to a final net loss of $666.7 million. However, in that quarter, Coinbase's operating income was still positive, reaching $273.8 million.

Coinbase Q1 Income Statement

This indicates that although the weakness in the crypto market impacted Coinbase's net profit, the company's performance is not as robust and controllable as Brian Armstrong described.

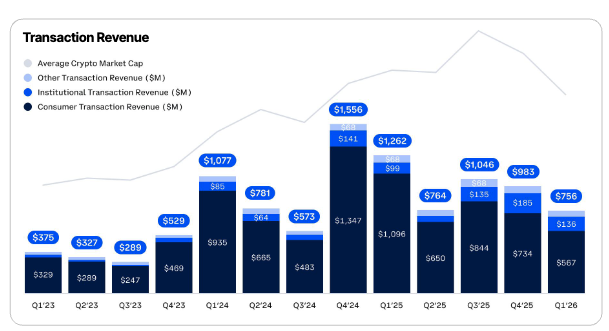

The problem lies in Coinbase's main revenue source: its brokerage business, which provides digital asset trading intermediary services for retail and institutional clients. The Q1 2026 report shows that Coinbase's transaction revenue reached $756 million, of which retail contributed $567 million, down 48.2% year-over-year and 23% quarter-over-quarter. Retail transaction revenue has returned to 2024 levels.

Coinbase Quarterly Transaction Revenue

This actually reflects a potential threat facing Coinbase: in a declining crypto market, users are starting to leave.

Investors should not be misled by Coinbase's record-high crypto trading volume market share shown in the earnings presentation, as it includes products like derivatives and prediction markets, not just the spot market. According to Coinbase CFO Alesia Haas, these new products are not included in transaction revenue (though they are part of total revenue).

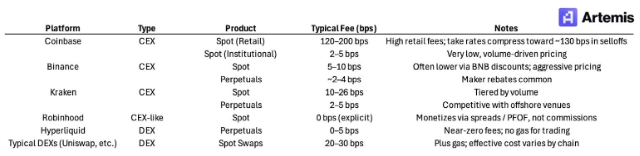

Coinbase's core competitive advantage has been its compliance in the U.S., which historically allowed it to charge fees significantly higher than most global exchange peers. This was both to cover high compliance costs and to collect a premium from users after Coinbase's early "monopoly" of the U.S. crypto market. But the U.S. regulatory landscape has now changed; Coinbase's compliance is no longer a "game-ending" advantage, as over 10 exchanges, including Robinhood, Kraken, and Binance.US, have obtained licenses to offer crypto trading services to U.S. users.

These emerging competitors, without exception, charge lower fees than Coinbase and use this as one of the main competitive strategies to attract retail investors.

Fee Ratios Charged by Different Exchanges

For U.S. retail investors, in the early days of the crypto market, they might have been willing to pay extra to Coinbase for convenience, trust, and regulatory certainty. However, as crypto regulation matures and the market declines, retail users will naturally gravitate towards platforms with lower fees, especially after traditional brokers and financial institutions like Robinhood entered the cryptocurrency space.

Regarding fees, Brian Armstrong responded on the earnings call, stating, "Customers choose us not because we are the cheapest, but because we offer products that meet their needs." Although Coinbase One's paid users have exceeded 1 million, when it comes to the richness of crypto token listings and speed, the rise of DEXs like Hyperliquid has also presented a significant challenge to Coinbase and other CEXs.

Recently, Coinbase announced a 14% reduction in its workforce, leaving approximately 4,300 employees (down from 4,988 at the end of the first quarter). In the layoff announcement, Brian Armstrong cited the market downturn and the AI technology revolution as the reasons. However, the actual revenue situation disclosed in the Q1 report confirms that this layoff is merely a cost-cutting and efficiency-improving measure disguised as an AI revolution. (Related reading: Coinbase Lays Off 14%: Is the Bear Market or AI the Main Cause?)

Painting a Grand Vision While Relying on Circle for Survival

Facing the challenges of a weak crypto market, declining spot trading, and user attrition, Coinbase is also seeking new paths. Brian Armstrong stated on the earnings call that Coinbase is moving away from reliance on spot trading, transforming from a "spot-focused cryptocurrency platform" to one where users can trade a wider range of asset classes, including derivatives, stocks, commodities, and prediction market contracts—an "Everything Exchange."

These products were mostly launched in early 2026. According to Coinbase, retail derivatives annualized revenue exceeds $200 million, and prediction market annualized revenue exceeds $100 million. Coinbase CFO Alesia Haas stated that revenue from these new products is not included in transaction or subscription revenue. Assuming all other revenue is from these new products, the actual situation from the report is that total revenue from these new products in Q1 was up to $73.6 million.

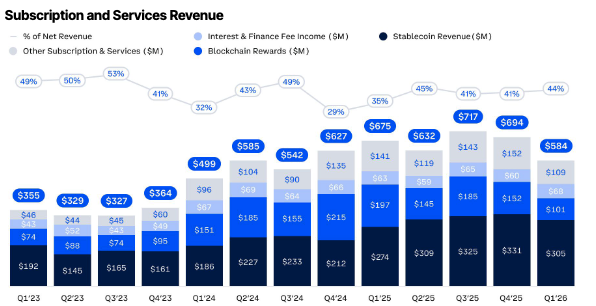

At the same time, Coinbase is deliberately obscuring the profits generated by Base. Brian Armstrong noted that Base processes 62% of the world's on-chain stablecoin transaction volume, and over 90% of on-chain agent stablecoin transaction volume occurs on Base. However, Coinbase did not separately list Base's revenue in the report. After carefully reviewing the report, Coinbase either did not disclose Base's actual revenue or lumped it into the "Other subscription and services revenue" line item. In past quarters, Coinbase has often included on-chain revenue in this item, which only generated $109.4 million in Q1 2026.

Base's On-Chain Fee Revenue Over the Past 30 Days is $2.72 Million (Source: DeFiLlama)

In summary, it appears that Coinbase is trying to paint a grand long-term narrative for investors around derivatives, prediction markets, AI, and on-chain activities, diverting market attention from the poor performance of its main business. Whether these areas will ultimately become new "cash cows" for Coinbase remains to be seen over time. Aggressively expanding product lines to chase market hotspots can provide more stories to tell the market, but a single misstep could lead to a mess.

However, Coinbase has the capital to experiment, thanks to its "good brother" Circle providing a lifeline.

The Q1 report shows that Coinbase's stablecoin revenue in Q1 2026 was $305 million, up 10% year-over-year. Stablecoin revenue is Coinbase's second-largest revenue source (Odaily note: the largest source is retail transaction revenue, and together they account for 62% of total revenue).

Coinbase Q1 Subscription and Services Revenue

This substantial revenue is mainly attributable to the revenue-sharing agreement between Coinbase and Circle. According to the agreement signed in August 2023, Coinbase receives all interest income generated by USDC held on its platform, while interest income from USDC held off-platform is split 50/50 between Coinbase and Circle. During the Q1 2026 earnings call, Alesia Haas reiterated that the distribution contract between Coinbase and Circle automatically renews every three years and never terminates.

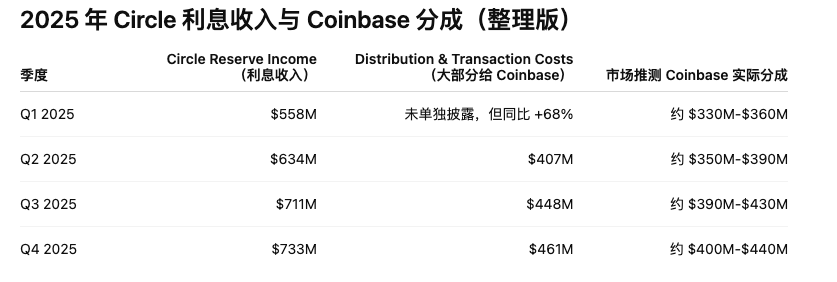

This structure positions Coinbase as a tollbooth for USDC, and stablecoin revenue could very likely become Coinbase's largest revenue source in the future. On one hand, the amount of USDC held on Coinbase's platform and products is continuously growing. According to the report, over 25% of all circulating USDC is stored on Coinbase (averaging approximately $19 billion in USDC held in Coinbase products). On the other hand, as stablecoins go mainstream, Circle's interest income is also growing. As shown in the chart below, Circle's interest income increased from $558 million in Q1 2025 to $733 million by the end of the year.

On May 11, Circle will release its Q1 2026 earnings report, allowing investors to examine Circle's Q1 2026 interest income and the profits distributed to Coinbase.

However, Coinbase has indeed played a significant role in distributing USDC. Besides conventional channels, Coinbase is also actively promoting USDC in the AI and agent-to-agent (A2A) payment space. According to the report, Coinbase's x402 protocol (Odaily note: now operated by the Linux Foundation) has processed over 100 million payments, with more than 99% of x402 transactions completed using USDC. Coinbase estimates that by 2030, AI agents will process between $3 trillion and $5 trillion in transactions, and cryptocurrency will become the preferred native execution channel for agents. If USDC dominates agent transaction settlements, it will also create immense economic value for Coinbase.

Therefore, if the distribution agreement between Coinbase and Circle never terminates, Coinbase will be permanently tied to the USDC "money printing machine." As long as the global stablecoin market continues to grow, and USDC keeps expanding into areas like payments, AI agents, cross-border settlements, and internet finance, Coinbase can steadily extract profits. To some extent, this could be even more profitable and more stable than Coinbase's current exchange business and the revenue from various new products.