日本債市,將全面「上鏈」

- 核心觀點:2026年,日本央行清算機構與多家金融機構合作,將日本政府債券(JGB)轉移至Canton Network鏈上,這是傳統金融基礎設施向區塊鏈遷移的重大進展,標誌著全球主權債券擔保品結算正邁向24/7、原子化、跨鏈的即時結算時代。

- 關鍵要素:

- JGB是亞洲最重要的金融擔保品之一,流通價值超9兆美元,但傳統結算需多層託管、僅在東京營業時間工作,導致擔保品被「凍結」,效率低下。

- 美國DTCC等機構已在Canton Network上推進美債代幣化,若JGB不跟進,將面臨被其他高流動性代幣化擔保品(如美債)擠出「頂級擔保品」地位的風險。

- Canton Network因滿足主權債券對法律合規、數據隱私和原子結算的極端要求而被選中,支援跨境、24/7的原子級擔保品與資金同步轉移。

- 鏈上擔保品可實現直接抵押以滿足追加保證金,減少強制拋售循環;原子結算消除了回購交易中的「先給後得」風險,降低了日內曝險和融資成本。

- 一旦JGB加入,Canton Network將整合美、日、歐三大主權債券資產池,形成類似SWIFT的網路效應,可能成為全球擔保品移動的預設基礎設施。

Original Author: Vaidik Mandloi

Compiled and Organized by: BitpushNews

On a Saturday in August 2025, something happened that should have sent every cryptocurrency group on the internet into a frenzy. Bank of America, Citadel Securities, the Depository Trust & Clearing Corporation (DTCC), and Société Générale settled a US Treasury repo transaction in real-time on a blockchain over the weekend.

For context, a repo is one of the most fundamental transactions in institutional finance: one party sells a government bond to another with an agreement to buy it back the next day, typically to raise short-term overnight cash.

This is the "plumbing" of the financial system. Banks, hedge funds, and central banks use repos daily to manage liquidity, with trillions of dollars flowing through this market. This was the first time such a transaction achieved near-instantaneous atomic settlement on a blockchain, outside of market hours, involving some of the world's largest financial institutions.

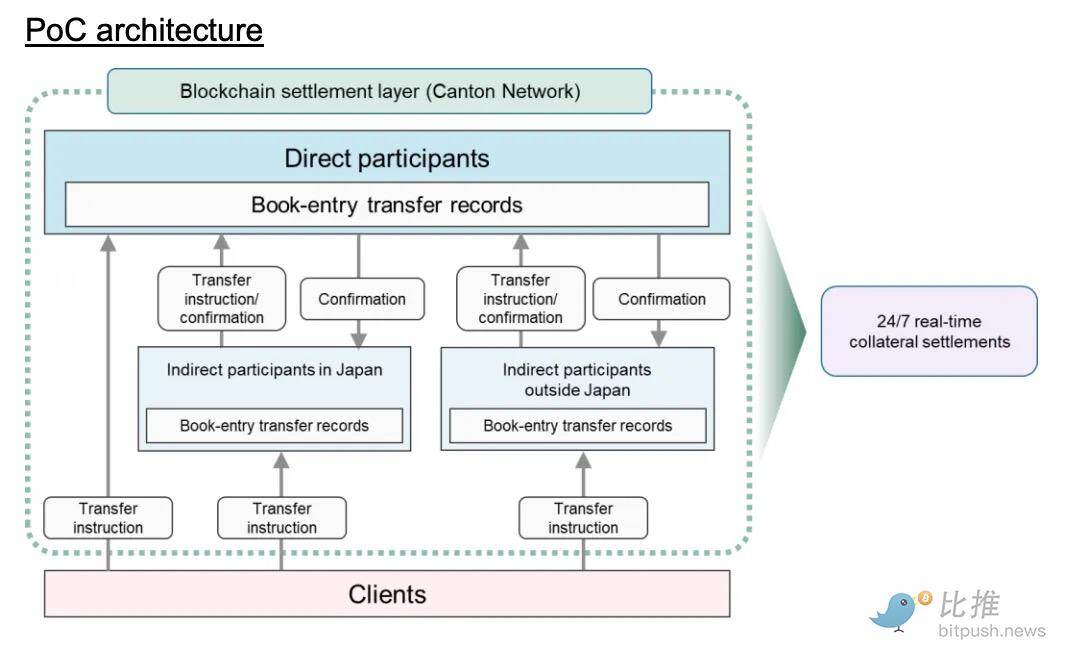

Eight months later, on April 20, 2026, the Japan Securities Clearing Corporation (JSCC), Mizuho Financial Group, Nomura Holdings, and Digital Asset launched a proof of concept (PoC) to move Japanese Government Bonds (JGBs) as collateral onto the Canton Network.

JGBs are among the most important financial instruments in Asia. With over $9 trillion in outstanding value, they are the most widely used single collateral asset in the region's institutional markets. When banks and hedge funds across Asia need to secure their leveraged positions, JGBs are often the first choice. Now, the entire collateral system is migrating on-chain.

This is arguably the most significant blockchain news of 2026.

This article analyzes why JGBs are the most suitable asset for tokenization, why the Canton Network continues to win institutional mandates while public chains compete for retail traffic, and how "24/7" collateral settlement will fundamentally change global trading desks.

Why JGBs? Why Now?

For decades, Japan has attempted to make the yen a global reserve currency, but this ambition has never fully materialized. Even today, the yen constitutes only about 4-6% of global reserves, trailing behind the US dollar, euro, and even the British pound.

However, something unexpected happened along the way: Japanese Government Bonds have become one of the fastest-growing collateral assets on the Euroclear Collateral Highway, the infrastructure for moving collateral among the world's largest financial institutions. Foreign holdings of JGBs have climbed to approximately 11.9%, meaning about ¥144 trillion is held by entities outside Japan.

In institutional finance, collateral is everything. Every leveraged position, every derivatives trade, every repo requires high-quality assets as security. Backed by the world's third-largest economy, JGBs carry virtually no default risk, making them one of the few globally acceptable assets. When a hedge fund in Singapore builds a leveraged position, or a bank in London covers derivative exposure, JGBs are frequently used as collateral.

The most important infrastructure victory for cryptocurrency is happening within traditional finance. Even though Japan never "won" the currency war, JGBs have become the operational backbone of institutional finance in Asia.

The problem is that the entire collateral system still operates as if it were 1995. Transferring JGB collateral between two institutions requires navigating a multi-layered holding structure: starting with the Bank of Japan (BOJ) at the top, then Hofuri (Japan's securities depository), followed by custodian banks, and then sub-custodians. Each layer requires separate reconciliation and only operates during Tokyo business hours (approximately 9 AM to 3 PM JST).

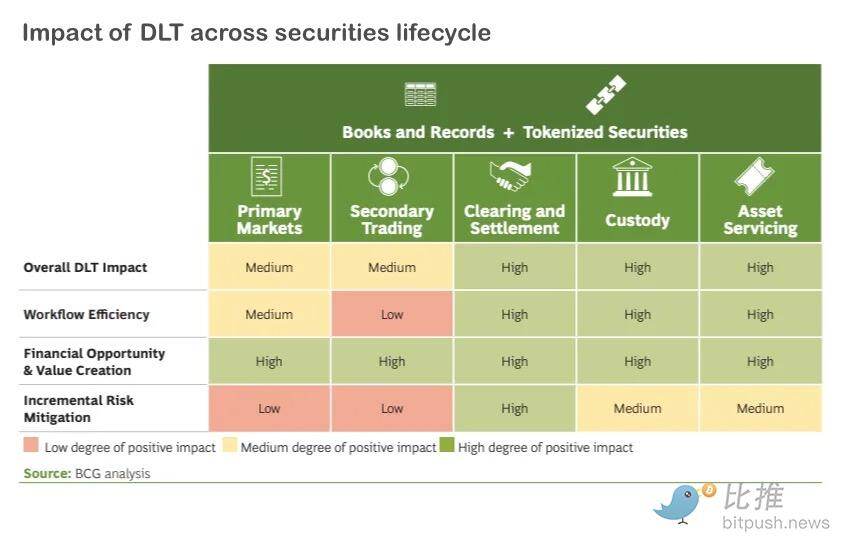

A collateral transfer that should take seconds ultimately takes days. During this time, the collateral is effectively "frozen." A trading desk in New York needing to use it at 10 PM must wait for Tokyo to wake up. A study by the Global Financial Markets Association (GFMA) and Boston Consulting Group (BCG) estimated that blockchain could unlock $100 billion globally in stuck collateral. For a bank handling $100 billion in daily repo transactions, tokenized settlement could save $150 million to $300 million annually in operational costs alone.

There is an unsettling fact for Japan: the United States has already acted.

The DTCC, which holds custody of $99 trillion in US securities and processes $3.7 quadrillion in transactions annually, partnered with Digital Asset in December 2025 to tokenize US Treasuries on the Canton Network. This means the core of US securities infrastructure is moving towards 24/7 tokenized settlement.

Broadridge already processes $354 billion in tokenized Treasury repo transactions daily on the same network; JPMorgan's Kinexys has processed over $1.5 trillion in cumulative transaction volume through its on-chain payment rail. US Treasuries are rapidly becoming "always available, always movable" collateral assets, while JGBs remain locked within Tokyo business hours.

If you are a global fund manager needing to post collateral for a margin call at 2 AM, and you have the choice between tokenized US Treasuries that settle instantly or JGBs that require waiting 6 hours for Tokyo to open, the choice is clear every single time.

Amplified across thousands of trading desks, this choice puts JGBs at risk of losing their "premier collateral" status. For a country whose sovereign bonds are deeply woven into the fabric of Asian financial collateral, this is an existential issue. The four companies involved in the JGB on-chain trial used the word "urgent" in their press release. Considering the pace of US infrastructure evolution, it's hard to disagree.

Why Canton Keeps Winning

When Japan's JSCC needed to choose a network for JGB collateral, they selected Canton – the same chain already used by DTCC, Broadridge, and JPMorgan. The reason lies in the extremely demanding requirements of sovereign bond collateral.

Sovereign bond collateral has specific needs that most blockchains cannot meet. When Mizuho Bank transfers JGB collateral to a counterparty in London, the transaction must comply with Japan's Book-Entry Transfer Act. The blockchain record must remain legally synchronized with Hofuri's official registry.

Each party in the transaction, from the clearing house to the custodian to the counterparty, can only see data they are authorized to view under Japanese and international securities laws. And the entire process requires atomic settlement, meaning the collateral and payment must move in the same instant, or neither moves.

This is an extremely complex set of constraints. Canton was chosen precisely because its architecture was built to solve these problems. Each institution runs its own ledger, and cross-institutional transactions synchronize only the data each party is entitled to see. Smart contracts, written in Digital Asset's Daml language, define exactly who can see what and who must authorize what at every step.

So, when JSCC, Mizuho, and Nomura transfer JGB collateral on Canton, the clearing house sees the full picture, Mizuho sees its side, Nomura sees its side, and no one sees data they shouldn't. Canton is now arguably the only network globally that can allow the three largest sovereign bond collateral pools (US Treasuries, JGBs, European sovereign bonds) to move freely across borders in real-time, 24/7. No other network, public or private, comes close to this capability.

What Does "24/7" Collateral Really Change?

Most reporting on tokenized on-chain settlement stops at "it's faster." But speed is just the beginning. The real transformation lies in how the system behaves under stress.

Consider what happened during the COVID pandemic in March 2020. Markets crashed, volatility soared, and initial margin requirements for stock futures jumped 100% within weeks. Funds unable to meet margin calls were forced to sell assets to raise cash.

But selling assets in a falling market pushes prices lower, triggering more margin calls, which forces more selling. This feedback loop is one of finance's most dangerous dynamics, nearly breaking the system again during the UK LDI pension crisis in September 2022.

How 24/7 tokenized settlement changes this dynamic:

- Direct Collateral Pledging: Currently, when facing a margin call, most funds must first sell assets for cash. With on-chain collateral, funds can directly pledge JGBs or US Treasuries to meet the requirement without converting to cash first. The "forced selling loop" weakens because fewer institutions are dumping assets into a declining market just for liquidity.

- Settling the "Delivery vs. Payment" Problem: In traditional repos, the cash lender sends money first and receives the collateral later. During this window, one party has credit exposure. Banks factor this "intraday exposure" into their haircuts and funding costs.

- Atomic Execution: With on-chain atomic settlement, both legs of the transaction (collateral and cash) move in the same instant. Santander tested this in December 2024, executing $50 million and €50 million intraday repos on JPMorgan's Kinexys, which were automatically unwound three hours later. Intraday repos, once requiring complex third-party setups or committed credit lines, have become routine.

More significantly, during a Canton demonstration in January 2026, the London Stock Exchange Group (LSEG) introduced its Digital Settlement House (DiSH) into the trade. DiSH uses tokenized commercial bank deposits as the cash leg, rather than stablecoins.

This is because banks won't use USDC to settle billion-dollar transactions – USDC is a private IOU, not "money good." DiSH tokens represent actual deposits in regulated banks and can be transferred on-chain 24/7. This solves the cash leg problem, the last piece of the puzzle for institutional adoption. Japan is now planning to plug JGBs into this same infrastructure.

What This Means

If the JGB proof of concept succeeds, with US Treasuries already live and European sovereign bonds in demos, it appears to me that Canton is starting to look like the next SWIFT.

It's a single network becoming the default layer for moving the world's most important collateral across borders. Like SWIFT, once enough institutions join, exiting becomes nearly impossible. Network effects compound. Each new class of sovereign bonds added benefits existing participants and makes it harder for latecomers to compete.

I believe this is worth contemplating. We've spent years in crypto debating decentralization, worrying about single points of failure, and building systems where no single entity can control the trajectory. Yet now, the most significant blockchain deployments in history are converging on a single permissioned network managed by the same institutions that run global finance.

Is this good or bad? It depends on what you think the point of all this is. If the goal is to improve capital market efficiency, reduce settlement risk, and unlock hundreds of billions in stuck collateral, then it's working. If the goal is to diminish the power of existing financial institutions, then it's doing the exact opposite – the old gatekeepers are merely upgrading their infrastructure.

I don't think this makes the achievement less important. Settling government bonds in a blockchain-based, 7x24, cross-border, atomic financial system is a genuine upgrade for how global finance works. But I do think it's worth being honest about what kind of upgrade it is – it's an efficiency revolution: the pipes are rebuilt, but the plumbers are the same people.