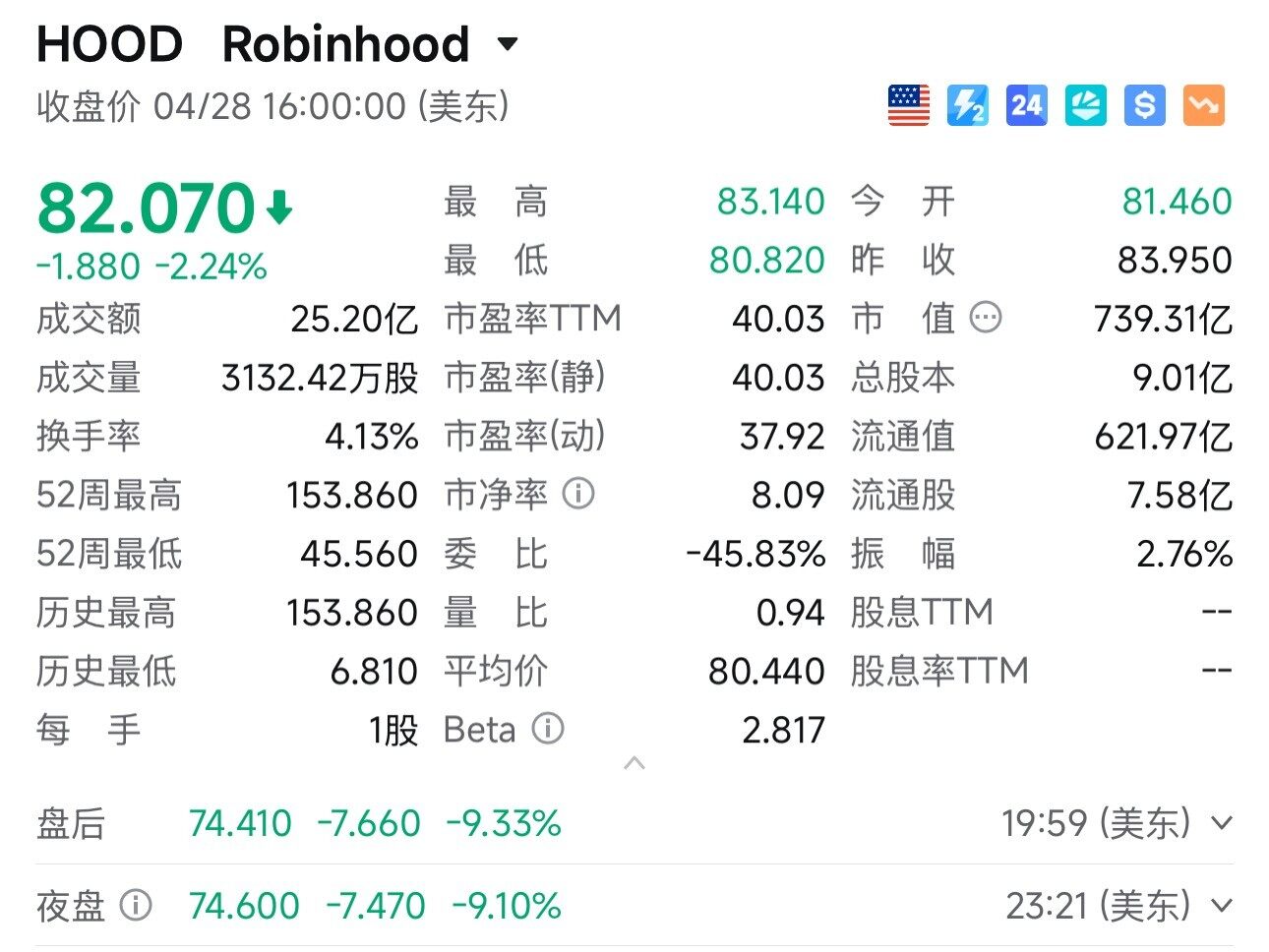

Robinhood, with a market cap of $70 billion, sees its crypto trading revenue outperformed by Hyperliquid

- Core Insight: Robinhood's cryptocurrency business revenue in the first quarter of 2024 fell approximately 47% year-over-year to $134 million, falling short of the $180 million in revenue generated by decentralized exchange Hyperliquid during the same period. High promotional costs associated with the "Trump account" caused Robinhood's stock price to drop nearly 10% after hours, sparking discussions on how to rationally value DeFi projects with strong profitability.

- Key Elements:

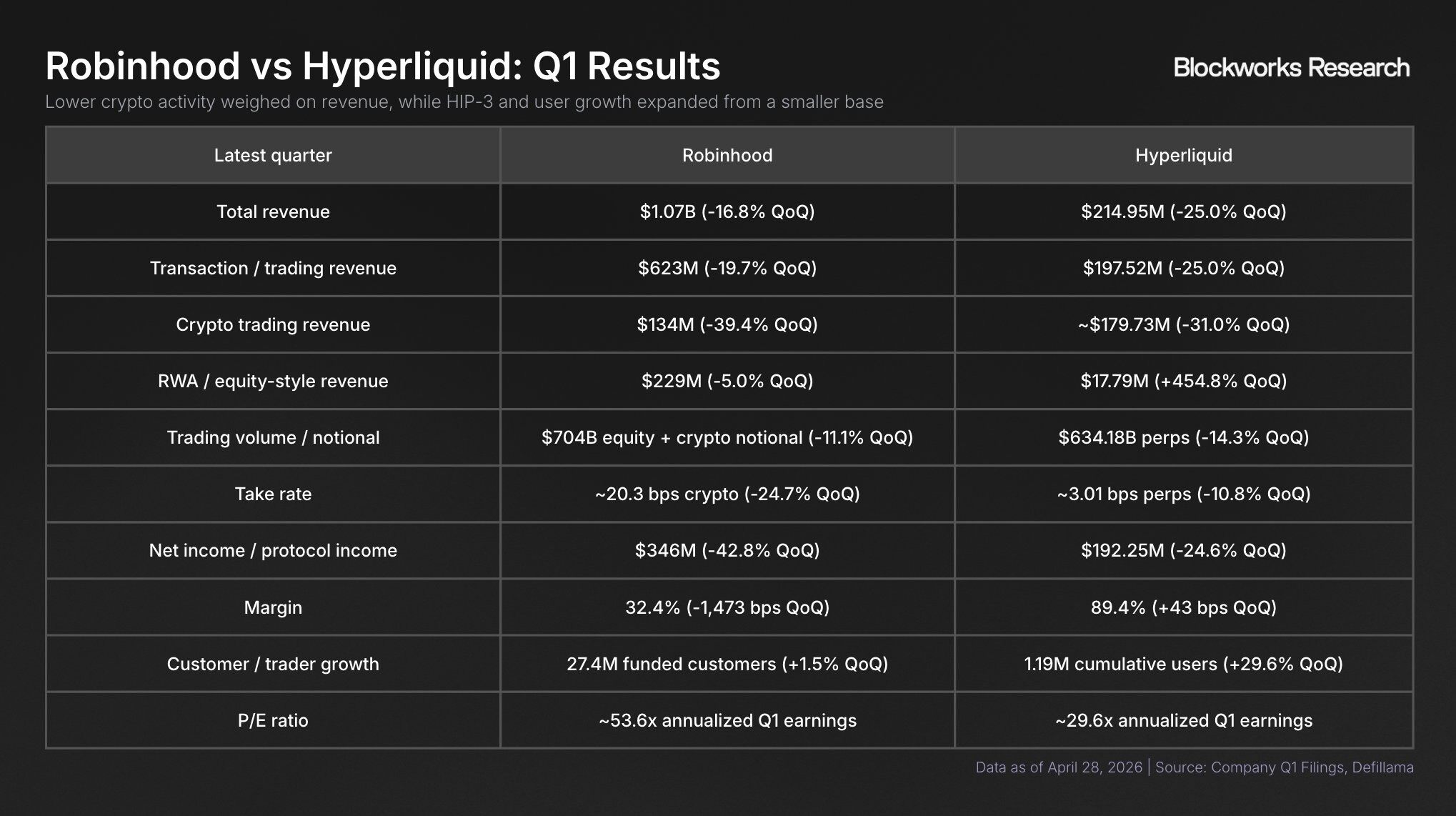

- Robinhood's Q1 crypto trading revenue was $134 million, down 47% year-over-year; notional trading volume was $24 billion, down 48% year-over-year.

- Hyperliquid's crypto trading revenue was close to $180 million during the same period, surpassing Robinhood, although both saw revenues decline by over 30%.

- Robinhood's overall net profit for Q1 was $346 million, while Hyperliquid's total protocol revenue was approximately $192 million, with an estimated profit margin potentially exceeding half of Robinhood's.

- Based on Q1 data, Robinhood's estimated P/E ratio exceeds 50 times, while Hyperliquid's is less than 30 times (if calculated by FDV, its valuation reaches $39 billion).

- Point of Contention: Hyperliquid represents DeFi projects with loose regulation, no tax pressure, and unlimited leverage. However, token holders lack shareholder rights, making valuation difficult.

Original Author: Eric, Foresight News

In the early hours of April 29, Beijing time, Robinhood released its first-quarter financial results after the US stock market close.

Robinhood's cryptocurrency-related revenue for the first quarter was $134 million, and its in-app notional transaction volume was $24 billion, representing year-over-year declines of 47% and 48%, respectively.

Despite the decline in cryptocurrency trading data, Robinhood made up the gap in other areas. The company's overall transaction revenue for the first quarter increased by 7% year-over-year to $623 million, primarily driven by a 320% surge in event contract revenue. Additionally, revenue from options and stocks stood at $260 million and $82 million, up by 8% and 46%, respectively.

Overall, Robinhood's first-quarter revenue was $1.07 billion, a 15% increase year-over-year; net profit was $346 million, a 3% increase year-over-year. While not spectacular, the overall single-digit growth was reasonable, especially considering that the cryptocurrency trading data, which often drives stock price increases, was nearly halved.

However, the real reason behind Robinhood's nearly 10% stock price drop in after-hours trading was the high expenditure incurred for promoting the "Trump Account".

Robinhood stated that its first-quarter expenses jumped by 18% and warned that its "Trump Account" promotion plan would require an additional $100 million investment. Furthermore, Robinhood mentioned that its contract for these accounts is based on a cost-plus model, resulting in lower profit margins.

This so-called "Trump Account" is an account established for American children under the "Big and Beautiful Bill" (note: likely a reference to a specific legislative act), with Robinhood acting as the broker and initial trustee.

For this company with one foot in the crypto circle, the discussion points on CT (Crypto Twitter) are not about the stock price or performance, but rather that this once-popular online brokerage's revenue from its cryptocurrency business hasn't even surpassed Hyperliquid's.

An analyst from Blockworks, going by the X handle shaunda devens, used a chart to visually demonstrate the comparison between Robinhood and Hyperliquid's data.

Due to business diversification, many data points are not highly comparable. However, in cryptocurrency trading, although both Robinhood and Hyperliquid saw their first-quarter revenue drop by over 30%, Hyperliquid's revenue from cryptocurrency trading approached $180 million, compared to Robinhood's mere $134 million.

In terms of overall profit, Robinhood's first-quarter net profit was $346 million, while Hyperliquid's total protocol revenue was approximately $192 million. Although the cost structure of Hyperliquid is unknown, it's unlikely to be very high, so its net profit could be at least more than half of $346 million.

Many Hyperliquid supporters on X believe that Hyperliquid is severely undervalued based on this comparison. Robinhood has far more users than Hyperliquid and also charges higher fees than Hyperliquid.

Even under such circumstances, Robinhood's price-to-earnings (P/E) ratio, estimated based on first-quarter data, exceeds 50 times, while Hyperliquid's is less than 30 times.

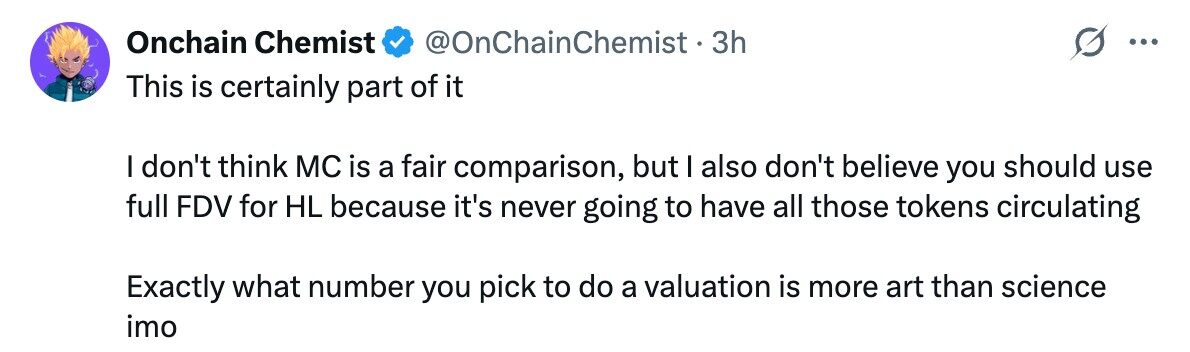

Another researcher from Blockworks raised some questions about this, pointing out that Hyperliquid's token Fully Diluted Valuation (FDV) has reached $39 billion. Using this figure for calculation seems to make everything quite reasonable.

Opponents argue that valuing a project using FDV is like valuing Robinhood based on its potential future stock issuances. Meanwhile, an X user known as "on-chain chemist" also stated that valuation has always been an art, not a science.

How to value an on-chain project has always been a topic worth discussing. DeFi projects like Hyperliquid are relatively easier to value among on-chain projects. Often, by analogizing to brokerages in the stock market, one can arrive at a vague valuation range. The reason it's called vague is that it's difficult to delve deeper for scrutiny.

DeFi projects have loose regulation, no taxable income pressure, and unlimited leverage. To some extent, they satisfy speculative demand. However, what patterns this speculative demand will exhibit is the core reason why the current market finds it difficult to estimate a project's future revenue.

Furthermore, the relationship between a project's token and the project itself is currently not clearly defined. Buying Robinhood's stock makes you, to some extent, a shareholder, but buying Hyperliquid's token seems to grant no actual power over the Hyperliquid project itself.

Using a chain to settle transactions is a major advancement Web 3 has brought to the world. In the future, cases similar to Hyperliquid, where profitability exceeds that of traditional companies, may continue to emerge. But how to value these emerging platforms might be, as previously mentioned, more an art than a science.