Tether持有美國國債超德國,300人年賺百億背後的隱秘帝國

- 核心觀點:Tether 已從一家備受爭議的穩定幣發行商,轉型為年利潤超百億美元、深度融入全球金融體系並積極構建多元化科技集團的龐然大物,其業務核心是利用美元儲備的利息收入,為新興市場提供美元穩定價值。

- 關鍵要素:

- 驚人的盈利能力:2025年利潤超過100億美元,主要由其持有的巨額美國國債(總敞口1410億美元)等儲備資產產生的利息構成。

- 新興市場主導地位:USDT的核心價值在於為高通膨/低金融效率國家提供穩定的美元價值,其全球用戶估計超5.5億,形成了強大的有機分發網絡。

- 業務多元化與集團化:利用利潤投資超過200億美元,涉足AI、能源、通信、農業、媒體等領域,並通過投資獲取運營控制權,構建以穩定幣為核心的生態系統。

- 監管與合規進展:推出受美國聯邦監管的USA₮穩定幣,並聘請專攻「爭議性審計」的CFO,顯示出向主流合規靠攏的意圖,但離岸USDT的審計透明度問題依然存在。

- 核心風險與競爭:利潤對利率週期敏感;面臨Circle(USDC)在機構市場的激烈競爭;其龐大的多元化投資組合帶來了運營複雜性和風險。

- 基礎設施佈局:開發錢包開發工具包(WDK)、去中心化AI平台(QVAC)等底層技術,旨在將穩定幣更深地嵌入全球商業,但尚未產生大規模獨立影響。

Original Author: James | Snapcrackle

Original Compilation: Deep Tide TechFlow

Introduction: Most people's understanding of Tether is stuck three to five years ago—either as a stablecoin issuer or a potential scam.

Neither framework explains what it has truly become today: 300 employees, annual profits exceeding $10 billion, holding more U.S. Treasury bonds than Germany, and acquiring publicly listed agricultural companies.

This article is currently the most comprehensive breakdown. After reading it, you'll find it's no longer just a crypto company.

The full text is as follows:

The $100 Billion Machine Nobody Has Updated Their Understanding Of

A woman walks into a mobile phone top-up kiosk to buy credit. That kiosk belongs to Tether.

In North Carolina, a former White House official is running a federally regulated stablecoin backed by U.S. Treasuries and custodied by Cantor Fitzgerald. That is also Tether.

A listed agricultural group just replaced its board, taken over by a company that didn't exist twelve years ago. Still Tether.

Most people's understanding of Tether is three to five years out of date.

Crypto media still treats it as a stablecoin issuer with trust issues. Mainstream media still treats it as a potential scam. Neither framework explains what Tether has become while everyone argues about the old version.

What I found is a company with over $10 billion in profits last year, only 300 employees (planning to add 150 more), holding more U.S. Treasuries than Germany—quietly building a tech conglomerate entirely funded by other people's dollar interest.

This article is long. It has to be. The scale at which Tether operates requires you to hold several ideas in your head simultaneously, some of which are contradictory.

Background

Tether reported over $13 billion in profit in 2024 and over $10 billion in 2025. About 300 employees, no external investors, no fees for secondary market USDT transfers (more on that later).

For perspective: roughly $33 million in profit per employee per year.

Tether doesn't make money from regular USDT transfers like card networks do. Direct minting and redemption have issuance fees (0.1% in some cases, with minimums), but the billions of peer-to-peer and exchange transfers that make up daily USDT volume generate zero revenue for Tether. When the company was designed in 2014, they debated whether to charge a 1 to 10 basis point fee per transaction like Visa and Mastercard.

They chose zero. Tether CEO Paolo Ardoino said in an interview it was a deliberate decision to prioritize adoption over revenue.

The result is a business model that looks nothing like a payments company, even though it functions like one. Tether makes money the same way a money market fund does: take in dollars, invest in short-term U.S. Treasury bills, keep the yield. The difference is, money market funds return most of the yield to investors; Tether keeps it all.

As of December 31, 2025, Tether held a $122 billion direct U.S. Treasury position and $141 billion total Treasury exposure (including indirect holdings via money market funds and repo agreements). At roughly a 5% Fed rate, that alone generates about $6-7 billion in baseline yield, not counting other income.

The rest comes from gold (127.5 metric tons in reserves at year-end, with Ardoino stating the position grew to about 140 tons by early 2026), Bitcoin (96,184 coins), and a growing venture capital and commodities portfolio.

Tether estimates over 550 million global users by early 2026, using a combination of on-chain wallet data and centralized platform estimates. This is not a verified count of unique individuals, but even heavily discounted, the scale is massive. In 2025, $13.3 trillion worth of USDT moved on-chain. Out of $33 trillion in total stablecoin flow, $156 billion were payments under $1,000, indicating real economic activity beyond just trading.

McKinsey provided a reality check on these numbers—a 2025 estimate put identifiable real stablecoin payment activity (B2B, remittances, settlements, card-linked spending) at an annualized ~$390 billion, far smaller than raw on-chain volume. There's a huge gap between "on-chain transfer value" and "actual payment for goods and services."

Most balance sheet data comes from BDO assurance reports (including reasonable assurance engagements at year-end), but Tether still does not publish fully audited financial statements in the way typical public companies do. (More on that later.) But the scale is corroborated by enough third-party data (on-chain analysis, Treasury market data, Cantor Fitzgerald counterparty confirmation) that outright denial would be absurd.

The Money Printing Machine

The cleanest way to understand Tether's economic model: imagine you run a savings account for hundreds of millions of people, most living in countries with constantly depreciating local currencies. They deposit dollars, you put those dollars into the safest, most liquid instrument on Earth (short-term U.S. Treasury bills), and give them a token that trades for $1 on every crypto exchange globally.

You keep all the interest.

Your customers don't mind because they weren't earning interest on their dollars anyway.

In Nigeria, where the local financial system might be 20% efficient, simply holding stable dollars is far more valuable than a 4% annual yield. In Argentina, with inflation exceeding 100% in recent years, holding something that doesn't depreciate is the product itself. The yield is Tether's fee, but no one experiences it as a fee.

Ardoino has spoken directly about this dynamic. On a podcast, he stated plainly: the U.S. financial system is already 90% efficient, stablecoins just push it to 95%. In emerging markets that are 10-30% efficient, USDT pushes it to 50%. The 5% margin game in the U.S. doesn't interest him; the 30-40% margin game everywhere else does.

Usage patterns also tell an interesting story, one I suspect will continue to evolve. Tether's Q4 2025 market report shows 63.6% of USDT value transferred that quarter was single-asset transfers (pure dollar movement, not part of multi-token DeFi trades), and about 67% of the market cap sits in low-velocity "savings"-type wallets. These two metrics don't measure the same thing, but together, they paint a picture of a product used as money, not a trading tool.

BIS researchers have independent corroboration, finding stablecoin use correlates more strongly with remittance costs and transaction demand than Bitcoin or Ethereum, especially in emerging and developing economies. (Surprising to no one.)

Standard Chartered predicts stablecoin savings in emerging markets could rise significantly by 2028, arguing stablecoins effectively give people a synthetic dollar bank account, helpful for hundreds of millions of unbanked. The value proposition isn't yield, it's escape from local currency depreciation and friction.

Tether spent less than $10 million globally on marketing between 2020 and 2024, less than a Super Bowl ad.

Growth was organic, crisis-driven. Ardoino says they didn't even understand why market cap went parabolic in 2020 until internal analysis years later: when COVID lockdowns shut down the physical black markets where residents of emerging economies bought physical dollars, tech-savvy teens introduced USDT to their parents on smartphones. The global dollar black market moved onto Tether's rails and never went back.

The interest rate sensitivity question is the most important analytical issue about Tether's business, and the 2025 numbers provide real data. Profits fell from over $13 billion in 2024 to about $10 billion in 2025, a ~23% drop. Tether's own disclosures show Treasuries and repos contributed ~$7 billion to 2024 profits. A rough model: a 200 basis point drop in yield on $122 billion direct Treasuries would reduce annual interest income by ~$2.4 billion. This is significant but not existential, especially given hard asset hedges (gold and Bitcoin positions tend to appreciate in easing rate environments). But it does mean the profit narrative is partly a function of the rate cycle, and Ardoino knows this. He explicitly frames R&D investments in AI, energy, and telecom as a hedge against eventual rate cuts.

What's in the Vault (and What Isn't)

Tether publishes quarterly attestations compiled by BDO Italia (one of the Big Five global accounting firms). Quarterly reports provide limited assurance under the ISAE 3000 framework. Year-end reports (including Q4 2024 and Q5 2025) are stricter: reasonable assurance engagements involving more rigorous testing. But both differ from full audited financial statements in the public company sense. BDO reviews Tether's assertions about its reserves and reports whether those assertions are materially misstated. It does not produce the kind of full financial audit institutional allocators typically require.

As of December 31, 2025, BDO's reasonable assurance report confirms: total assets exceed $192.8 billion, total liabilities $186.5 billion (of which $186.4 billion relates to issued tokens), excess reserves ~$6.3 billion.

The Brookings Institution found stablecoin issuers have become meaningful marginal buyers of U.S. Treasuries, actually ranking just behind a few foreign jurisdictions in one recent period. Tether alone holds more U.S. Treasuries than Germany, the UAE, Spain, or Australia. This stopped being a crypto story long ago. Tether has become part of the demand pipeline for short-term U.S. government debt.

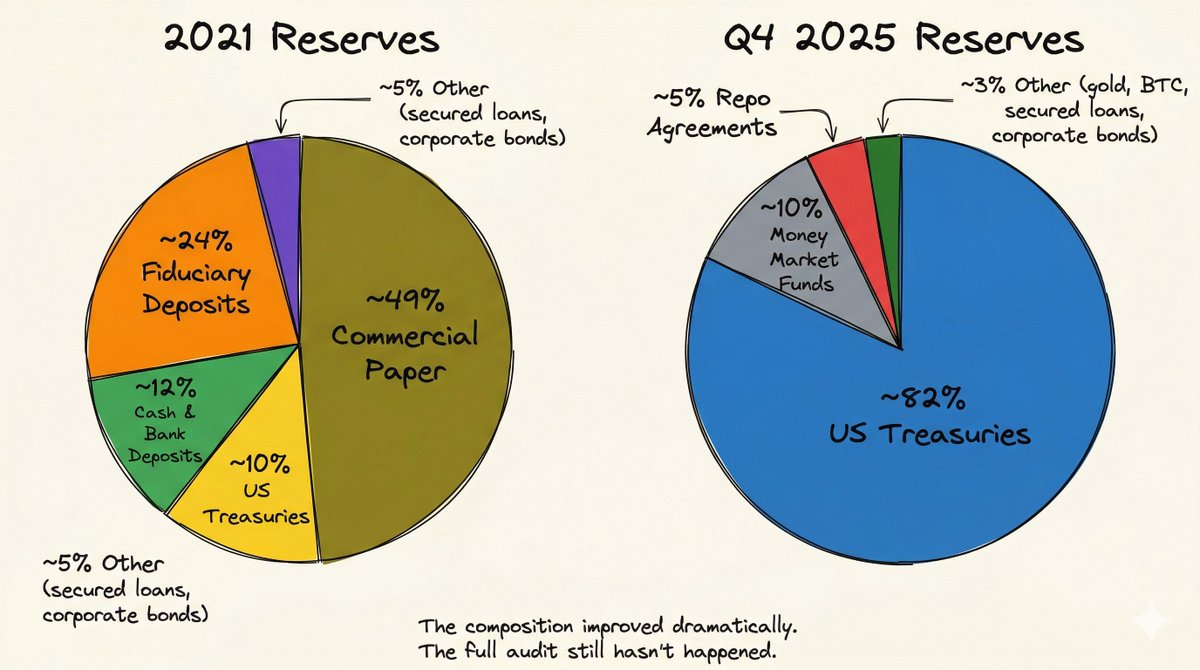

The reserve composition itself is telling. According to attestation documents and supplemental disclosures, ~82% is U.S. Treasuries, 10% money market funds, 5% repo agreements, the rest gold, Bitcoin, secured loans, and corporate bonds.

In 2021, 49% of reserves were commercial paper, actual cash about 3%.

This is a real shift, driven by regulatory pressure, well-documented. But the trust deficit is real and documented. A brief history:

In 2019, the New York Attorney General found Bitfinex (Tether's sister exchange) had misappropriated $850 million from Tether reserves to cover losses after a payment processor's funds were seized by authorities. Tether settled for $18.5 million. The CFTC separately fined Tether $41 million for claiming USDT was "fully backed" by dollars during periods when it "was not fully backed." At some point, Tether's website quietly changed wording from "100% backed by U.S. dollars" to "100% backed by our reserves, which may include assets from affiliated entities."

On the audit issue, Ardoino is more candid and more defensive than most reporting suggests. In a CNBC interview, pressed on why no Big Four firm audits Tether, he admitted: "They haven't even started looking at our numbers." He attributed the delay to "reputational risk" created by the last U.S. administration, making major accounting firms wary of touching crypto businesses. Then he pivoted to note that Silicon Valley Bank, Silvergate, Credit Suisse, and Wirecard all had clean audits before they collapsed.

In early 2025, Tether hired a new CFO from LetterOne specializing in "controversial audits," a signal they are staffing up for eventual Big Four business. But "eventual" is doing a lot of work in that sentence.

Chart: Tether Reserves

Tether's cash and bank deposits are near zero.

The Q1 2025 attestation shows $64 million in cash (0.04% of total assets). Treasury bills are the most liquid instruments on Earth, and Cantor Fitzgerald can liquidate positions same-day. The risk thesis hinges on: in a severe stress event, Tether needs the Treasury bill market to function and Cantor to execute quickly.

In 2022, coordinated short-sellers triggered $7 billion in USDT redemptions in 48 hours, $25 billion over 20 days. Tether honored every redemption. But the circulation was $80 billion then. At a $186 billion scale, the stress test hasn't been run.

S&P downgraded its stability score to the lowest ("5") at the end of 2025, citing specifically rising exposure to higher-risk assets (Bitcoin, gold, corporate bonds, secured loans) to 24% of reserves, up from 17% a year earlier. Ardoino responded publicly: "We wear your contempt with pride." Interpret that as you will.

USA₮: The American Card

On January 27, 2026, Tether launched USA₮, a federally regulated dollar-backed stablecoin designed for the U.S. market. The product is structured under the GENIUS Act (signed into law July 18, 2025), although the law's implementation timeline is phased and the full regulatory regime is still being established.

USA₮ is issued by Anchorage Digital Bank, the first federally chartered crypto bank in the U.S., operating under OCC oversight. Cantor Fitzgerald serves as reserve custodian and preferred primary dealer. Bo Hines, former Executive Director of the Presidential Digital Assets Advisory Council (White House Crypto Council), serves as CEO of Tether USA₮, headquartered in Charlotte, North Carolina.

This isn't Tether slapping a new label on USDT. This is a structurally separate product, different issuer, different regulatory framework, different reserve requirements. Anchorage and Cantor are shareholders in the U.S. entity and will share revenue, though specific economic terms aren't publicly finalized.

The strategic logic is a fork. USD₮ remains the offshore product, issued from El Salvador, serving hundreds of millions globally, especially emerging markets. USA₮ is the onshore product, built for U.S. institutional settlement, issued by a state-chartered bank under federal regulation.

Bo Hines described the relationship in an interview as "symbiotic," adding "at the end of the day it's Tether." But the competitive dynamics the two products face are completely different.

In the U.S., Ardoino expects stablecoin profitability to be "competed to zero." As bank-issued stablecoins enter the market under the GENIUS Act, they will compete by sharing yield with holders, effectively becoming tokenized money market funds. USA₮ can't win on margin; it must win on programmability, institutional services, and Tether's distribution advantage.

Offshore, USD₮ faces almost no competition (zero yield for holders) because its users have no better alternative. The product is stable dollars. It's a monopoly position that's hard to attack.

Hines is also confident the U.S. Treasury will eventually establish "reciprocity standards" under the GENIUS Act, allowing offshore USD₮ to gain legal recognition in the U.S. market. Tether operates two structurally separate businesses under one brand.

The rarely articulated bear case: by launching a highly regulated, transparent U.S. product, Tether implicitly acknowledges the offshore USD₮ standard is not that. If institutional markets start seeing the two products as proxies for each other's reputation, the opacity around USD₮ could bleed back into USA₮.

The Conglomerate

The way I discovered Tether's investment portfolio made it look like a list of random bets. It's not.

Tether's proprietary investment arm manages over $20 billion (separate from USDT reserves, funded by