孙宇晨看好的核能赛道,悄悄开启上市潮

- Quan điểm cốt lõi: Nỗi lo về nhu cầu điện năng do sự mở rộng sức mạnh tính toán AI đang thúc đẩy vốn đầu tư sớm vào các nguồn năng lượng “tương lai xa” như năng lượng hạt nhân và nhiệt hạch. Giá trị của chúng không còn chỉ đến từ những đột phá công nghệ, mà còn bắt nguồn từ tính độc quyền chiến lược trong việc cung cấp “tấm vé mở rộng sức mạnh tính toán” cho các trung tâm dữ liệu trong tương lai.

- Yếu tố then chốt:

- Điện năng trở thành nút thắt của AI: Trung tâm dữ liệu thiếu điện, năng lượng gió và mặt trời không ổn định, nhiệt điện hạt nhân truyền thống có thời gian xây dựng quá dài. Các công ty công nghệ lớn (như Amazon) bắt đầu khóa trước công suất phát điện của các lò phản ứng mô-đun nhỏ (SMR) thông qua các thỏa thuận mua bán dài hạn.

- Vốn đầu cơ vào tương lai: General Fusion tăng 38% trong ngày đầu niêm yết, lên kế hoạch xây lò phản ứng vào năm 2035; X-energy lỗ khi niêm yết nhưng vẫn được định giá 9,1 tỷ USD nhờ đơn đặt hàng từ Amazon. Thị trường đang giao dịch “phiếu đặt trước” chứ không phải nhà máy điện đã phát điện.

- Truyền dẫn chuỗi công nghiệp: Nỗi lo về điện năng cho AI lan truyền từ các nhà phát triển lò phản ứng đến nhiên liệu TRISO (như Standard Nuclear), urani làm giàu cao độ (như Centrus) và các công ty khai thác urani (như Eagle Energy Metals), chiếu sáng toàn bộ thượng nguồn ngành năng lượng hạt nhân.

- Năng lượng hạt nhân gắn kết với AI: Trước đây, năng lượng hạt nhân bán sự an toàn và ít carbon; bây giờ, nó bán “tấm vé mở rộng sức mạnh tính toán”. Các ông lớn như Sun Dũng Thần, Sun Tôn đều chỉ ra rằng điểm đến cuối cùng của năng lượng AI là phản ứng nhiệt hạch, đánh dấu sự thay đổi trong cách kể chuyện của ngành.

- So sánh với cuộc khủng hoảng dầu mỏ: Nhu cầu điện năng của AI đang biến điện năng từ một loại hàng hóa “cắm là dùng” thành một nguồn tài nguyên chiến lược cần được lên kế hoạch từ nhiều năm trước, tương tự như sự thay đổi vị thế của dầu mỏ sau năm 1973.

Some time last year, the market was buzzing with rumors that Justin Sun had bought a power plant in Norway.

To understand his logic, I looked through some of his YouTube videos and found that he had said something like, "If you missed Nvidia, you can look further down, like electricity, like nuclear fusion." He later put it more bluntly: The endgame of AI is energy, and nuclear fusion is a direction worth watching for the long term in the AI era.

At the time, the term "nuclear fusion" felt too distant, and the AI market craze was far from its current intensity. The market didn't seem to pay much attention.

On July 14th, Asia's richest man, Masayoshi Son, talked about AI. He didn't start with chips. He also talked about nuclear fusion.

The SoftBank founder said that within fifteen years, nuclear fusion could potentially power AI data centers, gradually replacing natural gas. He dismissed concerns about the "AI bubble," as usual, and urged Japan not to stay on the sidelines watching the wave pass by.

Two individuals, coming from completely different businesses and contexts, operating from perspectives far beyond the average person, both set their sights on the same machine that doesn't exist yet.

Data centers are starved for electricity.

Fusion hasn't generated power yet, but General Fusion is already up

On July 13th, Canadian fusion company General Fusion listed on Nasdaq through a merger with a SPAC, under the ticker GFUZ. It became the first publicly traded pure-play fusion energy company globally.

On its debut day, the stock price surged, closing up about 38%.

General Fusion holds roughly $150 million in cash, which the company expects will sustain operations until 2028. They aim to build their first commercial fusion reactor around 2035.

In other words, what the market traded that day was not a power plant already generating electricity.

It was a ticket for nine years from now.

The fusion business has a harsh reality. Progress in scientific experiments can be measured in seconds of plasma stability, a material test, or a device parameter; capital markets lack such patience. They always ask: when will the electricity be sold, who will buy it, and do the numbers work out?

In the past, fusion companies' answers were typically grand.

Clean energy. Artificial sun. Unlimited fuel. Humanity's ultimate energy source.

These words are all correct, but they are far from the balance sheet.

Now, someone has provided a more grounded explanation for it.

AI companies need electricity.

Consequently, a company planning to build a commercial reactor by 2035 suddenly has a visible future customer image. Not some vague utility company, but rows of AI data centers, already built with heavy investment, waiting to be connected to power.

Capital's attitude shifted quickly.

According to the latest statistics from the Fusion Industry Association, global fusion investment added $4.48 billion over the past year, a record high. This number comes with the group's own methodology, so it shouldn't be taken as proof that fusion has already won.

But it at least indicates one thing.

The number of people willing to pay a deposit for "distant electricity" suddenly increased.

When X-energy went public, the market had already changed its algorithm

General Fusion is just the farthest ticket.

A closer ticket is X-energy.

This advanced nuclear energy company attempted a SPAC listing in 2023, but it didn't go through. Back then, people looked at it like someone claiming they would build a rocket. The project was huge, the timeline long, yet the financial statements were on the table, something no one could ignore.

Three years later, X-energy returned with an IPO.

In April this year, the company raised about $1.02 billion, with an offering valuation of roughly $9.1 billion, and its stock closed up about 27% on the first day. Its projected 2025 revenue is around $109 million, with a net loss of about $390 million.

Looking at these numbers alone, they don't look great.

But it also has Amazon.

Amazon and X-energy are partnering with a goal to deploy up to 5GW of Small Modular Reactor capacity by 2039.

It's not just Amazon; Google also secured a deal with Kairos Power to reserve a spot for nuclear power.

These partnerships are far from actual power plants. Approvals can be delayed, projects can change, and options don't equal revenue. Anyone treating them directly as future revenue is easily mistaking a reservation for an invoice.

But in the capital market, a reservation has its own value.

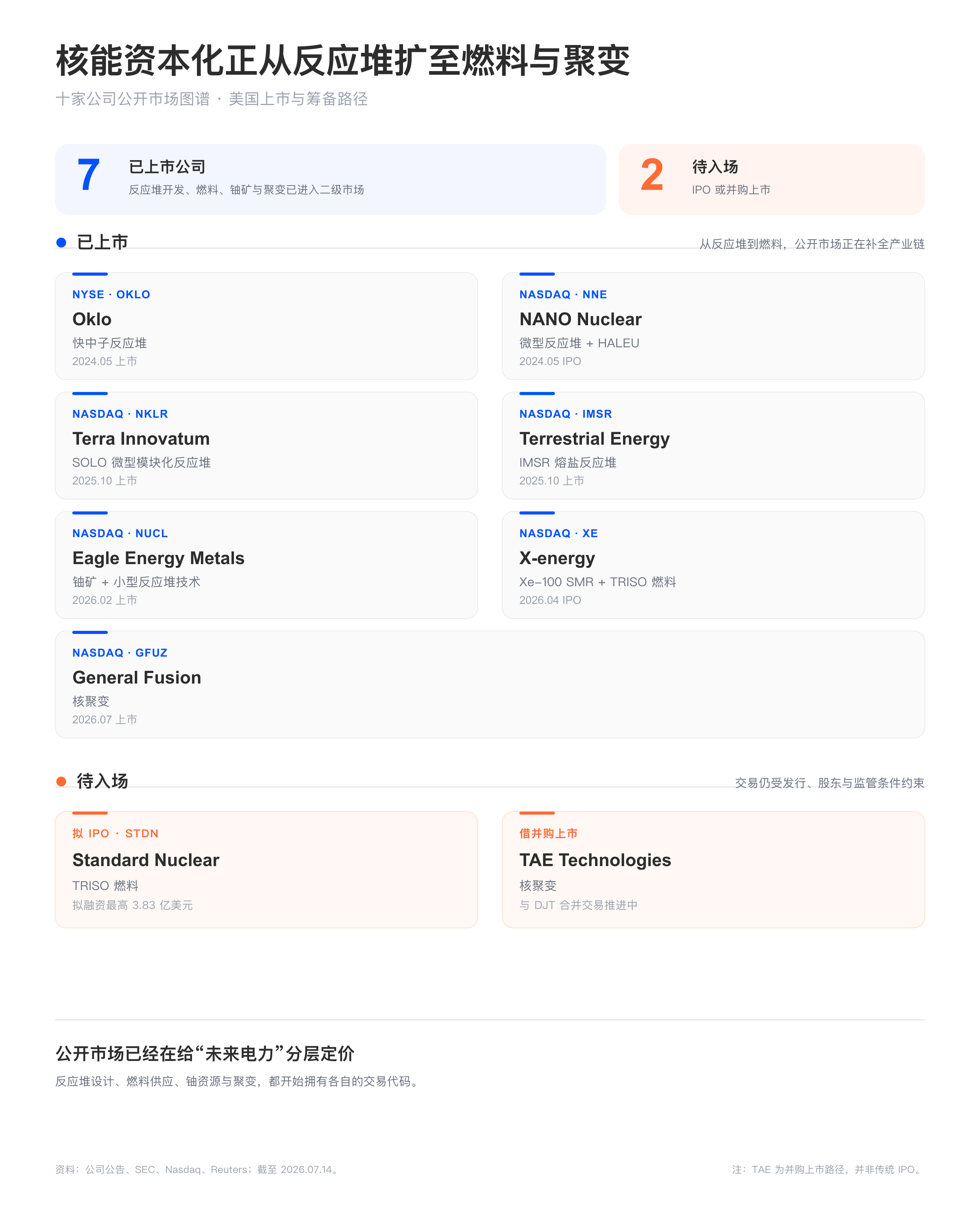

Looking at the bigger picture, you'll see that the nuclear energy track has seen a batch of listings in a short time. Oklo, Terra Innovatum, Terrestrial Energy, and X-energy have brought reactor developers to exchanges; Eagle Energy Metals capitalized on both uranium mining and small reactor technology; Standard Nuclear took the market all the way to TRISO fuel. General Fusion and TAE have brought the most distant fusion stories to the doorstep of public markets.

In the past, nuclear energy companies sold low-carbon, stability, and energy security.

Today, they start selling another thing.

The qualification for computing power expansion.

Secure electricity first, then keep packing chips into the data center

Why would data centers push such a slow technology to the forefront?

Because even if chips are expensive, you can place an order.

Electricity is different.

Servers can be procured in advance, shipped to the site, and stored in warehouses. If GPUs are insufficient, Nvidia can scale up, AMD can follow, and customers can upgrade. Electricity doesn't work that way. You need generation, transmission, substations, and then nods from local governments, regulators, grid companies, and communities.

What AI companies fear most isn't expensive electricity.

They fear building the data center and not being able to connect it to power.

A large data center campus runs non-stop, with both machines and cooling systems generating heat. When training models, thousands of chips work simultaneously. You can't tell a client, "The wind is low today, the model will answer questions tomorrow."

Wind and solar power are essential but depend on the weather. Natural gas units are flexible but come with old issues of fuel, emissions, and supply. Large traditional nuclear plants are stable but have construction timelines long enough to test the patience of internet companies.

SMRs, or Small Modular Reactors, sit right in the middle.

They promise to shrink nuclear plants, make them more standardized, deploy parts first, and then expand gradually. This promise hasn't been tested by large-scale commercial operation, but it fits the data center's temperament well.

They don't want to wait for one giant plant to be built.

They are willing to take a number first.

The long-term procurement agreements signed by tech giants like Amazon and Google are essentially them queuing up for future electricity. They aren't just buying a specific unit of electricity; they are reserving a plug for their future expansion.

This brings something far more valuable to nuclear energy companies than a technical whitepaper.

Data centers trace the problem all the way back to the mine

When the "need electricity" issue was first laid on the table, capital immediately focused on reactors.

Companies like Oklo, X-energy, Terrestrial Energy, and Terra Innovatum were pushed to the front. They all sell next-generation reactors that are still under development. Some are fast neutron reactors, some are molten salt reactors, some are SMRs.

SMRs are Small Modular Reactors. They break down the huge nuclear plants built for city-sized grids into smaller units that can be manufactured in a repeatable way and deployed in batches. Data centers like this concept because they don't want to wait for a giant plant to be built slowly.

But once a reactor is actually scheduled for a project, the problems start cascading down.

What fuel does this machine need?

X-energy's Xe-100 reactor needs TRISO fuel. TRISO sounds like some lab acronym, but you can think of it as a miniature nuclear fuel pellet wrapped in several layers of ceramic materials. It needs to withstand high temperatures and last long enough inside the reactor. No matter how beautiful the reactor design blueprint is, without this fuel, it remains just a computer file. This is what Standard Nuclear does.

So when Standard Nuclear prepares for its IPO, it's no longer just a standalone story of a fuel company.

It sells something very unglamorous. No flashy reactor launch events, no massive data center orders, no fifteen-year grand pronouncements like Masayoshi Son. But when the market starts believing advanced reactors will be built, people will eventually ask who can deliver the fuel to the doorstep on time.

Pushing further back, fuel itself becomes a bottleneck.

Some advanced reactors need HALEU, High-Assay Low-Enriched Uranium. Its enrichment level is higher than the standard fuel used in traditional nuclear plants but much lower than weapons-grade material. The name is long, but the logic isn't complex. New machines need a different grade of fuel, which isn't available in old tanks, and there aren't many factories producing it.

Companies like Centrus are therefore re-evaluated.

The questions don't stop there.

Where does HALEU come from? Where does the uranium itself come from? So companies like Eagle Energy Metals, which hold both uranium mining assets and small reactor technology, can also enter the public market along the same chain. The mines, originally furthest from the AI world, are now illuminated by the electricity anxiety of data centers.

This wave of listings is not the nuclear industry suddenly falling in love with Wall Street.

It looks more like data centers placed an electricity order on the table and then traced backward along the order. First, check who can build reactors. After they are built, check who has fuel. If fuel is insufficient, check who can enrich uranium and who owns the mines.

Every step upstream hits a constraint that cannot be solved with temporary overtime.

Approvals can be expedited. Models can be iterated. Servers can be purchased more. But fuel production lines and uranium mines don't respond to such pressures.

So the market is no longer just asking which company has a good-looking reactor design. They start asking which link in the chain could delay the reactor's operation by a year.

After 1973, oil was no longer just oil

Before the 1973 oil crisis, oil was already important.

Cars ran on it, factories relied on it, planes flew with it. But what truly made governments nervous wasn't discovering that year that oil could burn; it was realizing they had almost no control over a long and fragile supply chain.

Oil wells were far away. Tankers were at sea. Pipelines crossed borders. Prices were set by others.

From then on, oil was no longer just a commodity. It became intertwined with diplomacy, reserves, war, and industrial policy.

AI is making electricity follow a similar path.

Electricity used to be too ordinary. Plug it in, the light turns on, the computer runs. Its ordinariness made people rarely think carefully about where it comes from.

Until a group of companies started planning to increase their computing power tenfold, a hundredfold.

That's when they discovered electricity also has geographical locations, queuing orders, and construction lead times. It's not just a hole in the wall; it's a path that needs to be reserved many years in advance.

Masayoshi Son talks about fifteen years, Justin Sun says nuclear fusion is the next stop, General Fusion surged on its first trading day, X-energy presents both losses and a high valuation to the market.

All these events together don't prove fusion has arrived.

They only prove that more and more people are starting to worry that by the time it actually arrives, they might not have a place in line.