Saylor bought 1,550 BTC, but it's one of Strategy's worst deals in recent times

- Core Insight: Strategy recently conducted a stock issuance at a premium below its breakeven point, and instead of using all the proceeds to buy Bitcoin, the company allocated some funds elsewhere, resulting in a 0.19% decline in Bitcoin holdings per share, thereby compromising the interests of MSTR shareholders.

- Key Elements:

- The modified Net Asset Value (mNAV) needs to be above 1.30 for an issuance to increase Bitcoin holdings per share, but the mNAV was below this threshold at the time of this issuance.

- This issuance raised $181 million, but only $101.3 million was used to purchase 1,550 Bitcoins. The remaining funds were allocated to bolster USD reserves, violating the premise of using 100% of proceeds for Bitcoin purchases.

- Following the transaction, Bitcoin holdings per share dropped by approximately 0.19%, while USD reserves were only extended from supporting 6.3 months of operations to 7 months—an inefficient outcome.

- Strategy's move essentially sacrifices MSTR's core metrics to sustain STRC's business operations, constituting a high-risk bet.

- If market sentiment does not improve, the company may be forced to continue sacrificing MSTR's interests, potentially facing risks such as delaying STRC dividends or even heading toward decline.

Original author: 100y

Original English translation: Chopper, Foresight News

Bitcoin treasury company Strategy first sold 32 BTC, then made a massive purchase of 1,550 BTC.

I don't want to see Strategy (MSTR) fail, but the truth must be spoken. In my view, this is an extremely poor trade.

On the surface, the move looks quite impressive. Strategy accumulated a large amount of Bitcoin at a relatively low price while also increasing its USD reserve for paying preferred stock dividends from $900 million to $1 billion.

Does this mean a turnaround is imminent for Strategy?

If all you see are positives, it means you haven't truly understood how this company operates.

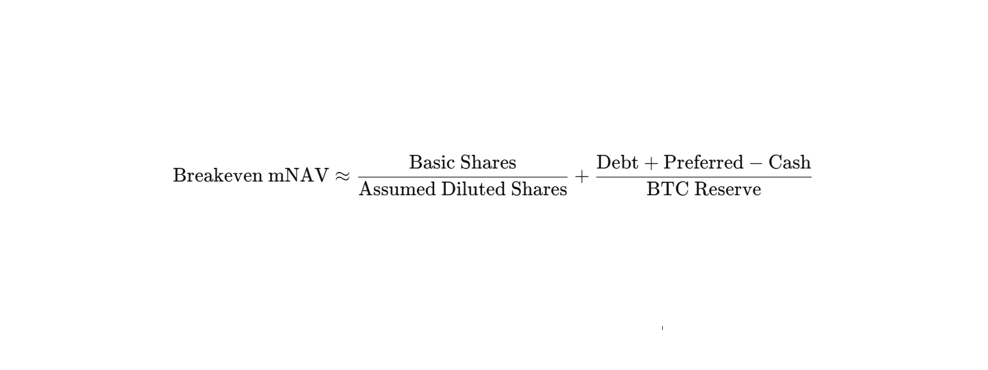

First, Understand the Modified Net Asset Value (mNAV) Breakeven Point

Increasing Bitcoin Per Share (BPS) is one of Strategy’s core objectives for creating value for MSTR shareholders.

The logic for increasing BPS is clear: issue common stock at a premium to the market price, then use all the proceeds to buy Bitcoin.

So, how high a premium does MSTR need to command for this timely equity issuance strategy to effectively boost BPS?

According to the Q1 2026 earnings call, the modified net asset value (mNAV) must be above 1.22. This figure is known in the industry as the breakeven modified net asset value.

The underlying logic is simple: the funds raised by selling one share of MSTR must be able to buy more Bitcoin than the amount of Bitcoin currently attributable to that single share. For the complete derivation, you can refer to my previous post (https://research.4pillars.io/en/research/strategys-magic-number-122).

Ultimately, the breakeven mNAV is calculated as follows:

One important note: the breakeven modified net asset value is no longer 1.22. Estimates show that before this 1,550 BTC purchase was executed, this figure had already risen to 1.30.

Why This is a Bad Trade

Let's revisit this 1,550 BTC acquisition.

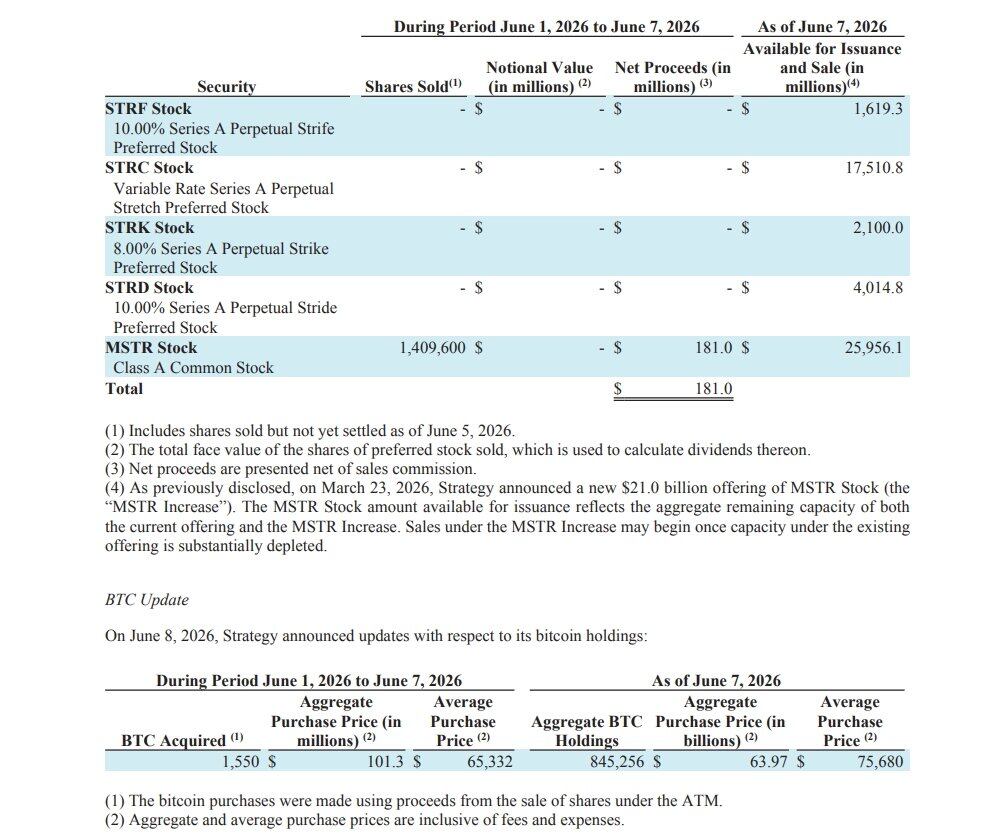

Strategy raised a total of $181 million through its timely equity issuance of MSTR, then used $101.3 million of that to buy 1,550 BTC. This operation has two core problems:

First, at the time of this MSTR equity issuance, the corresponding modified net asset value (mNAV) was below the breakeven point of 1.30. Issuing shares and using the proceeds to buy Bitcoin when mNAV is below the breakeven line will not increase BPS; instead, it will cause the metric to decline.

Second, and more critically, not all the funds raised from this issuance were used to buy Bitcoin. The breakeven mNAV calculation logic is predicated on 100% of the proceeds being used for Bitcoin purchases. Even if mNAV is high, using only a portion of the proceeds for Bitcoin will ultimately dilute BPS.

It is reported that the remaining funds from this issuance that were not used to buy Bitcoin were allocated to the company’s USD reserve.

In other words, Strategy sacrificed the equity value and Bitcoin per share for MSTR shareholders to ensure the normal operations of the STRC-related business.

Estimates show that after this transaction, the company's BPS decreased by approximately 0.19%. And what was the result? The company's USD reserve runway for operations was extended only from roughly 6.3 months to 7 months.

A High-Stakes Gamble for Strategy

Michael Saylor stated on the Q1 2026 earnings call: "Our core goal is to increase Bitcoin per share, and we will do everything in our power to achieve this goal."

However, as this trade demonstrates, Strategy sacrificed the core metric of MSTR's BPS for the development of STRC. This is nothing short of a gamble.

If sacrificing MSTR leads to improved market sentiment, a stabilization and recovery of the STRC token price, and pushes mNAV back into a reasonable range, then the company can continue to raise funds through the timely equity issuance channels of both MSTR and STRC, allowing the entire system to function smoothly.

But if market sentiment fails to improve, the situation could turn sharply. Strategy might then be forced to continuously sacrifice MSTR's interests just to stay afloat.

The worst-case scenario would follow, where the company is either forced to delay STRC dividends or gradually decline amid persistent internal conflicts.

Finally, I hope the prices of Bitcoin, MSTR, and STRC can all recover.