Từ Coinbase đến Upbit: Hành Trình 28 Ngày Của Một Token Khi Người Đến Sau "Đón Đỉnh"

- Quan điểm cốt lõi: Trong thị trường gấu năm 2026, việc niêm yết token trên các CEX đã chuyển từ định hướng dòng tiền sang định hướng xác thực, hình thành một lộ trình có cấu trúc: Coinbase/ByBit (Phát hiện) → Binance Perps (Xác thực) → Binance Spot (Xác nhận) → Sàn Hàn Quốc (Đón đỉnh). Sự kiện niêm yết chủ yếu là sự phân phối lại vốn hiện có chứ không phải là chất xúc tác tạo ra dòng tiền mới, nhà đầu tư có thể tận dụng điều này để xác định cơ hội Alpha.

- Các yếu tố chính:

- Coinbase, ByBit và Binance Perps là nhóm đi đầu trong việc niêm yết lần đầu, lần lượt có 67%, 39% và 48% token được niêm yết lần đầu trên các sàn này, đảm nhận vai trò khám phá giá; Binance Spot chỉ niêm yết 19 token, tỷ lệ niêm yết lần đầu là 28%, chú trọng xác thực an toàn.

- Các sàn Hàn Quốc (Bithumb, Upbit) thường xuyên nằm ở cuối lộ trình niêm yết, với độ trễ trung bình khoảng 28 ngày so với đợt niêm yết đầu tiên, tỷ lệ theo sau lên tới 85% và ở vị thế tương đối cao, khiến người dùng thường xuyên "đón đỉnh" (mức premium khi vào lệnh trên Upbit lên tới 27,4%).

- Tín hiệu tiền đề cốt lõi cho việc niêm yết trên Binance Perps là động thái niêm yết trên Coinbase và ByBit (tỷ lệ chuyển đổi lần lượt là 75% và 70%), và phản hồi rất nhanh (trung bình 4,9 ngày), ưu tiên chọn lọc các dự án phổ biến có hiệu suất giá ổn định, tránh các token đang suy yếu liên tục hoặc đầu cơ quá mức.

- Hiệu suất giá sau niêm yết nhìn chung chịu áp lực: lợi nhuận trung bình trong 30 ngày trên tất cả các sàn đều âm, mức giảm dần sâu hơn, phản ánh đặc điểm giải phóng thanh khoản chứ không phải tăng trưởng; sàn niêm yết lần đầu (ví dụ ByBit) đạt đỉnh trung bình +86%, trong khi các sàn theo sau (ví dụ OKX) chỉ đạt +25%.

- Việc lựa chọn sàn giao dịch ảnh hưởng đáng kể đến cấu trúc rủi ro-lợi nhuận: người dùng trên các sàn niêm yết lần đầu (Coinbase/ByBit) có giá vào thấp nhất và tiềm năng đỉnh cao nhất, trong khi người dùng trên các sàn Hàn Quốc phải đối mặt với việc mua ở đỉnh cao và mức giảm sâu (lợi nhuận 30 ngày -25,7%), chênh lệch lãi lỗ có thể lên tới 4,5 điểm phần trăm.

Original Authors: Xinyang & Ethan @ IOSG

Every bear market quietly reshapes the listing logic of centralized exchanges (CEXs). When liquidity tightens and retail enthusiasm fades, each exchange listing decision becomes more deliberate, and therefore carries more signal value. We systematically tracked new listing data from six major exchanges – Coinbase, Binance Spot, ByBit, OKX, Bithumb, Upbit – and Binance Perpetual from 2026 to mid-May, totaling 207 listing records covering 92 unique tokens. The data clearly reveals a core truth: listing is a highly structured pathway of validation and liquidity transmission.

Who first discovers and prices a project? Who bridges and amplifies liquidity in the middle phase? Who completes market coverage at the end? Different exchanges play distinct roles along this chain. By the time a token is finally listed on Binance Spot, it has typically undergone multiple rounds of exchange validation. This report dissects this listing pathway from three core dimensions:

- Landscape & Path: The role differentiation of exchange listings and the flow patterns of tokens between exchanges

- Binance Perps Selection Logic: What kind of tokens are more likely to enter Binance Perp?

- Price Impact: How listing timing determines investor entry points, and the actual return differences post-listing across exchanges

For projects, understanding this pathway means a more precise and efficient exchange listing strategy; for investors, identifying positional differences within the pathway could be one of the most important Alpha sources in 2026.

2026 CEX Listing Landscape and Paths

Overview of Exchange Listings

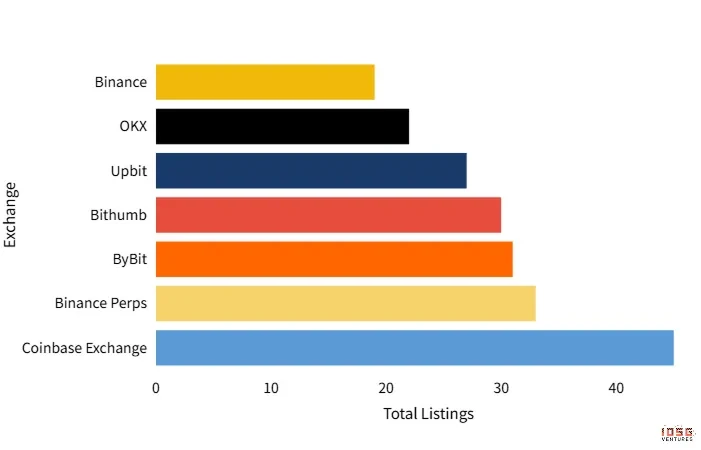

▲ Total Listings by Exchange

Since the beginning of 2026, we tracked new listing data from six major spot exchanges – Coinbase, Binance Spot, ByBit, OKX, Bithumb, Upbit – and Binance Perp, totaling 207 records covering 92 unique tokens.

Listing volumes show a clear stratification across exchanges. Coinbase leads with 45 new listings, followed closely by Binance Perps (33) and ByBit (31). Bithumb (30) and Upbit (27) form the second tier. OKX listed 22 tokens, while Binance Spot listed only 19, the fewest among all observed exchanges.

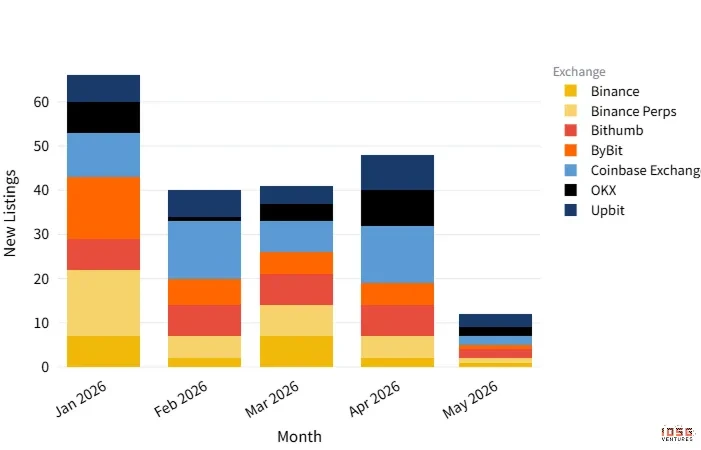

Examining the monthly cadence, January was the peak period for listings across the year. Binance Perps listed 15 tokens in a single month, and ByBit listed 14. From February onward, the overall pace slowed significantly, with average monthly listings per exchange dropping to 5-8, entering a more cautious and stable filtering phase. Coinbase showed a listing rhythm out of sync with other exchanges, with two concentrated listing peaks in February and April (13 tokens in a single month), demonstrating its independent and swift listing decision-making characteristics.

▲ Monthly Listings by Exchange

Mere differences in volume only reflect surface-level activity. More important is the profound differentiation in listing timing and roles among different exchanges, which will be further dissected in the following sections.

Role Differentiation: Discoverers, Filterers, and Confirmers

Among tokens listed on multiple exchanges, a significant sequential order exists. We define the earliest listed exchange within our tracking scope as the 'Pioneer' and the others as 'Followers'.

Coinbase is the most prominent pioneer listing venue in 2026, with 67% of its tokens being the first to list among the tracked exchanges, bearing the primary responsibility for the market's initial price discovery. ByBit (39% pioneer rate) and Binance Perps (48% pioneer rate) also maintain high activity levels, often listing the same token densely within the same week, collectively forming the first tier for new project launches.

Korean exchanges (Bithumb and Upbit) systematically occupy the end of the listing path. Bithumb's Follower ratio is as high as 85%, Upbit has an average rank of 4.44, and has a high probability of being the last among all exchanges to list a token, lagging the pioneer exchange by an average of approximately 28 days. This is closely related to the longer regulatory review process in Korea and the preference of local exchanges to introduce projects only after they have achieved broad consensus.

Binance internally forms a clear funnel-like division of labor: Binance Perps takes the initiative to pioneer in half the cases, while in the other half, it follows up rapidly after the spot listing (average of only 4.9 days), making it the fastest responder among all exchanges. Its main role is to quickly test liquidity and market demand through the derivatives market. Conversely, Binance Spot lists the fewest tokens (only 19) with a pioneer rate of only 28%, clearly preferring to wait for adequate market validation before selectively listing.

OKX demonstrates a relatively strong ability for independent token selection, with a pioneer rate of 55%. However, its overall listing volume is relatively restrained (22 tokens), with an average rank of 3.58, indicating a high filtering threshold and a more cautious strategy.

Listing Path Paradigm

From the sample of tokens covered by 3 or more exchanges, the listing order exhibits highly stable tier characteristics: early discoverers represented by Coinbase and ByBit pioneer first, Binance Perps follows up rapidly within days for validation, then Binance Spot selectively lists for confirmation, while OKX, Bithumb, and Upbit primarily provide supplementary coverage in the later stages of the path.

Typical Case: ROBO (Fabric Protocol)

On February 27th, the DePIN project Fabric Protocol (ROBO) had its pioneer listing on Binance Perp. Coinbase and ByBit followed suit on the same day. The opening price was $0.022, surging over 80% on the first day. The opening price the next day had risen to $0.0405, nearly doubling from the pioneer price. The project, which raised $20 million led by Pantera Capital, focuses on the intersection of blockchain and the robotics economy. Coupled with the hype from the Kaito public sale and the 'AI + Robotics' narrative, it quickly gained market attention.

On March 5th, Binance Spot officially listed ROBO, with the daily price reaching $0.0493. This became the absolute peak price for ROBO throughout its cycle. When OKX entered, its opening price was already lower than the Binance Spot price. Bithumb listed on March 18th at a price of $0.0303. Although it briefly triggered a price spike, the token price subsequently declined continuously and is now below the pioneer opening price.

From its pioneer listing to the Bithumb listing, ROBO completed a typical 2026 listing path in just about 20 days:

Binance Perps, Coinbase, and ByBit Pioneer → OKX and Binance Spot Confirm at the Peak → Korean Exchanges Catch at the End.

ROBO is not an isolated case. Among the sample of the first five months of 2026, 28 tokens were listed on 3 or more exchanges. The rank distribution of these cross-exchange cases consistently exhibits the same tier pattern as ROBO. Although the exact order may vary slightly depending on project attributes, the overall path structure is stable and predictable.

This path clearly reflects the differing risk appetites of each exchange: Coinbase, ByBit, and Binance Perps tend to proactively seize the early window; Binance Spot focuses on post-validation safety; while Korean exchanges and OKX prefer to enter only after sufficient market consensus has been formed.

Binance Perps Listing Conditions

As a key entry point for the derivatives market, Binance Perps' listing decisions directly influence the flow direction of significant leveraged capital. Through analysis of 33 Perps listing cases, we can clearly distill Binance's core logic for selecting tokens in a bear market environment.

Precursor Signals: Coinbase and ByBit Listings

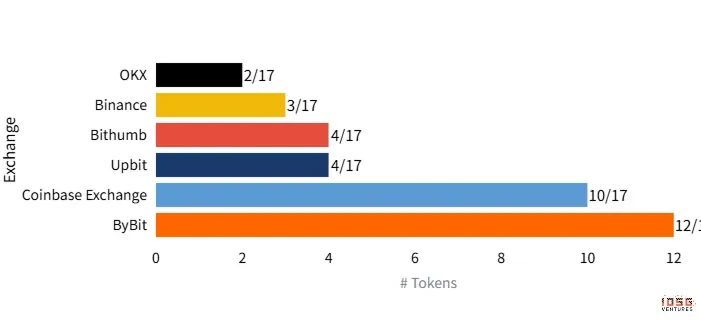

▲ Exchanges Listed Before Perps

Of the 33 tokens that entered Binance Perps, 17 were already listed on other spot exchanges before being added to Perps. Tracking these tokens reveals that Coinbase and ByBit are the most important precursor signals for Perps.

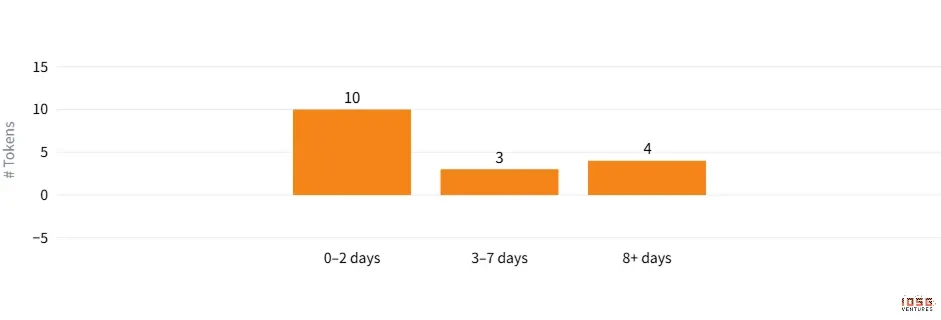

▲ Days from First Spot to Perps

Among these, ByBit listed before Perps in 71% of cases, and Coinbase in 59%. More importantly, regarding response speed: in the 17 follower listing cases, 10 had Perps listed within 0-2 days of the spot listing, with an average delay of only 4.9 days. This extremely fast follow-up indicates that Binance Perps closely monitors the listing activities of Coinbase and ByBit and uses them as a significant decision-making reference.

Looking at the broader sample, 75% of tokens listed on Coinbase eventually entered Binance Perps, while the figure for ByBit was 70%. When a token receives support from both Coinbase and ByBit and shows relatively stable price performance, it has a high probability of landing on Binance Perps within a week. This is one of the strongest and most directly observable precursor signals currently available in the market.

Price Performance is the Crucial Filtering Criterion

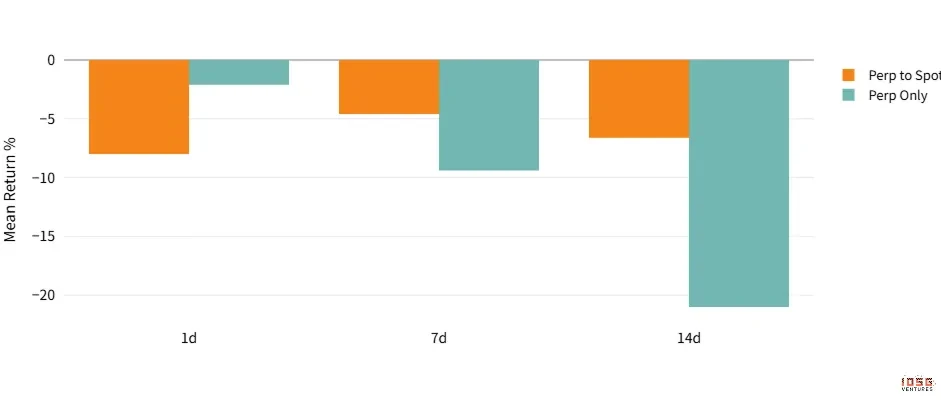

▲ Post-Listing Mean Return(Converted vs Perp Only)

Projects listed on Coinbase and ByBit generally have an opening FDV above $100M, so FDV itself is not a differentiating factor. What truly determines entry into Perps is the price performance after listing.

Observing tokens listed on Coinbase and ByBit but that did not enter Perps, three main categories of characteristics emerge:

- First, projects whose prices continue to weaken and lack market heat post-listing;

- Second, meme coins with excessive speculative characteristics (e.g., WHITEWHALE, ELON), where Binance's screening is significantly stricter than ByBit's;

- Third, tokens that have not passed through Binance Alpha. Alpha acts as a pre-screening channel within the Binance ecosystem and is a crucial preliminary step for entering Perps.

The impact of price performance extends beyond 'whether it gets into Perps' to the subsequent 'Perps to Spot' conversion. Data shows that tokens eventually converted to Binance Spot (Converted group) had a return of -4.6% 7 days after the Perps listing and -6.6% after 14 days. In contrast, tokens that did not convert to Spot (Perp Only group) had a 7-day return of -9.4% and a 14-day return that dropped significantly to -21.0%. Although both groups showed negative returns under bear market influence, the Converted group demonstrated significantly stronger price maintenance ability, indicating that Binance considers 'sustainability' as an important factor during the Perps phase.

Price Impact of Listings

The actual impact of listing events on token prices is the central concern for projects, institutions, and traders. We analyze this from two core dimensions: Price Position (the relative price level at the time of listing) and Post-Listing Return (7-day, 14-day, and 30-day returns after listing).

Price Discovery Concentrated in the Pioneer Window, but Entry Prices Vary Significantly Across Exchanges

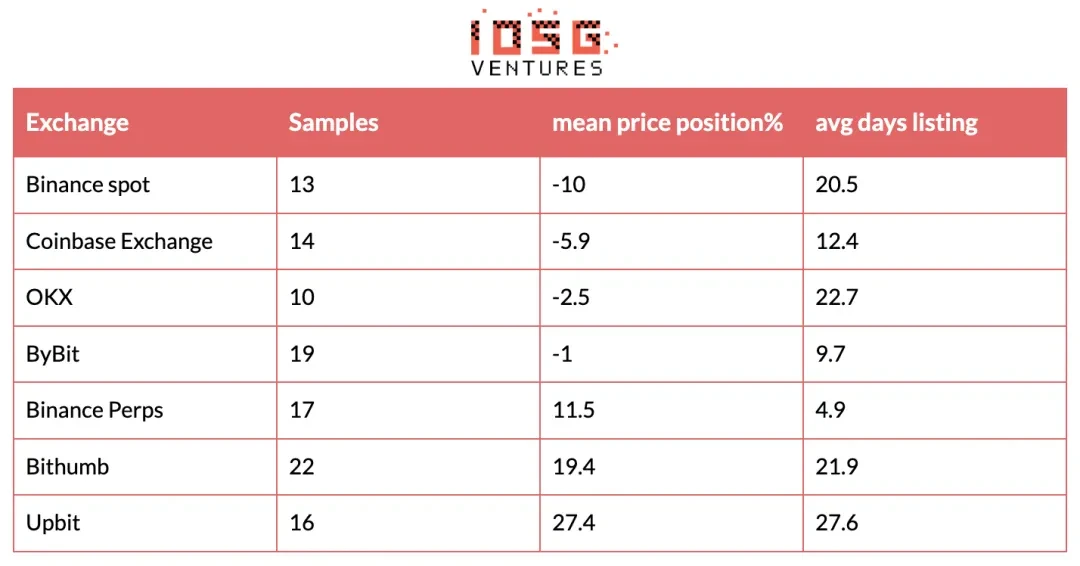

▲ Price Position at Listing

Price discovery primarily occurs within the pioneer window. When ByBit and Coinbase act as followers, their entry prices are roughly flat or slightly lower than the pioneer price, indicating a rapid price convergence among first-tier exchanges.

When Binance Perps acts as a follower, its average price is 11.5% higher than the pioneer price. However, thanks to its extremely fast follow-up speed (only 4.9 days), it still remains in a relatively early position. Binance Spot's Price Position is -10%, indicating its tendency to list only after a price correction, allowing users to potentially secure a comparatively better entry price.

Korean exchanges face the most unfavorable entry positions: Bithumb averages 19.4% higher, and Upbit is as high as 27.4%. With an average delay of over three weeks, users often find themselves catching tokens at significantly higher levels.

Overall Listing Performance Under Pressure in 2026: Liquidity Release, Not Growth Catalyst

▲ Mean Return by Exchange 7d/14d/30d

In the 2026 bear market environment, the price performance of newly listed tokens is generally weak, with no exchange achieving a positive 30-day average return.

From 7d to 30d, the losses deepen progressively, indicating that the price decline post-listing is not short-term volatility but a persistent downtrend. In the current market environment, new listings primarily serve as liquidity release events – providing an exit window for early holders (including projects, investment institutions, and early traders) – rather than attracting sustained new capital inflows.

The performance on the two Korean exchanges is particularly noteworthy: Upbit's 7d return is already -13.5%, reaching -25.7% at 30d. Combined with its +27.4% price position, this means Upbit users not only entered at the highest price but also endured the deepest losses.

Peak Price Performance Under the Listing Path

Although the final returns after 30 days are generally negative, the structure of the peak rebounds shortly after listing (Peak Return) shows a distinctly different distribution. Dissecting the token price data, we find that listing timing directly determines the upper limit of short-term speculative opportunities.

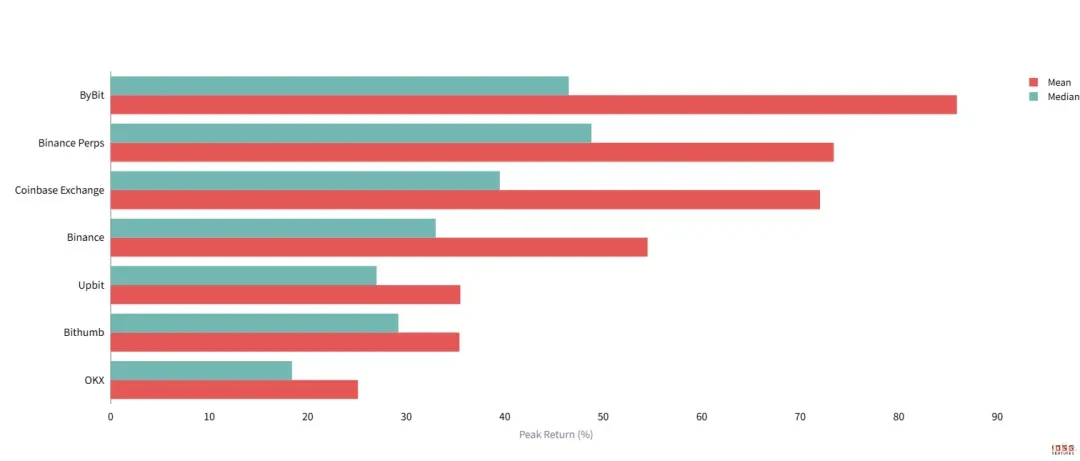

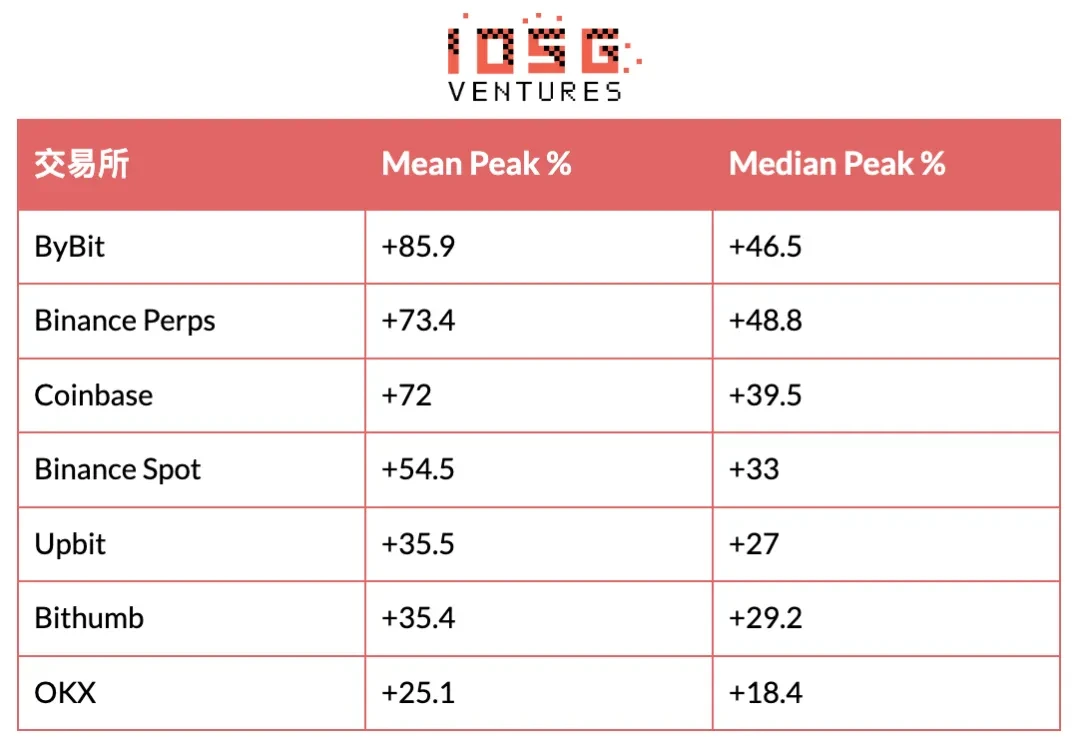

▲ Peak Return by Exchange (14d High)

Pioneer exchanges hold an absolute advantage: ByBit's average peak return is as high as +86%, and Binance Perps' median is the highest at (+49%). The first tier of listing exchanges (ByBit, Coinbase, Binance Perps) captures the highest price elasticity, offering a substantial liquidity premium for early tokens. Even if the price subsequently goes to zero, there is ample time to exit at the peak.

Late-stage followers face limited potential: The peak returns on Bithumb and Upbit are capped around +35%, while OKX's is only +25%. Due to the lagging entry timing, buying pressure on these platforms primarily absorbs profit-taking by early holders rather than initiating a new upward move.

This difference confirms the liquidity transmission path: Pioneer exchanges bear the primary price discovery function, providing the best exit liquidity for early holders. As time passes, buying pressure on subsequent exchanges is more about absorbing realized gains, leading to diminishing marginal utility. For traders, this means that the later one enters the listing cycle, the lower the probability of capturing excess returns.

Exchange Choice Determines the Risk-Reward Structure

Combining the three metrics – Price Position (entry point), Peak Return (peak potential), and Mean Return (final outcome) – users on different exchanges face completely different risk-reward structures.

Users on pioneer exchanges (Coinbase/ByBit), while also facing negative returns, possess the best risk buffer. With the lowest entry prices (-10% ~ -5.9%) and the highest peak potential across the market (average over +70%), even if they fail to precisely time the top, absolute losses relative to the pioneer price are relatively manageable. They even have the opportunity to lock in profits during the upward surge.

In contrast, users on Korean exchanges face a classic 'buy high, crash deep' scenario. They enter at a premium of nearly 20% to 27%, but the peak potential has already been exhausted by pioneer exchanges