深度拆解 OpenAI Pre-IPO

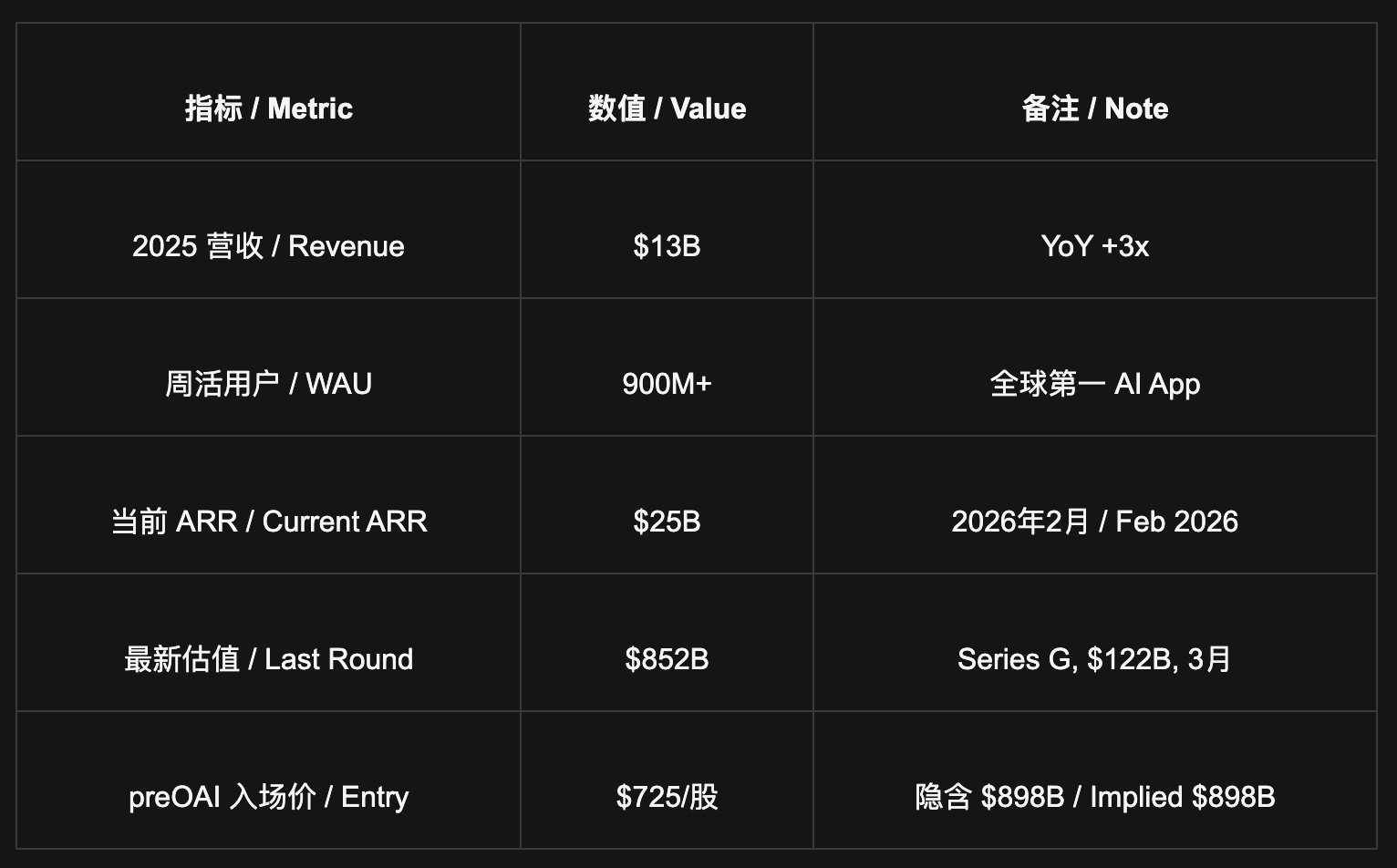

- Quan điểm cốt lõi: Với 1,3 tỷ người dùng hoạt động hàng tháng, OpenAI đang xây dựng một “cổng vào người tiêu dùng chủ động”. Mức định giá hiện tại 898 tỷ USD chỉ phản ánh doanh thu hữu hình từ đăng ký và API, chưa tính đến mảng quảng cáo (dự kiến đạt 25 tỷ USD vào năm 2029), việc định giá lại nền tảng tiêu dùng (C-end) và hiệu ứng tái định giá từ GPT-6, tạo ra dư địa bị định giá thấp đáng kể.

- Các yếu tố then chốt:

- Rào cản cổng vào C-end: ChatGPT có 900 triệu người dùng hoạt động hàng tuần. Hành vi người dùng chủ động mở ứng dụng tạo thành một hào kinh tế với chi phí chuyển đổi cao, tương tự các nền tảng nghìn tỷ USD như Google Search, iPhone và WeChat.

- Khắc phục câu chuyện công nghệ: Việc phát hành GPT-5.5 và Image2 đã vượt quá kỳ vọng thị trường, khắc phục câu chuyện về việc vị thế dẫn đầu công nghệ bị san bằng, đồng thời có thể thúc đẩy tăng trưởng WAU mới và dòng ngân sách doanh nghiệp quay trở lại.

- Nguồn doanh thu quảng cáo mới: OpenAI ước tính ARR quảng cáo đạt 1 tỷ USD vào năm 2026 và 25 tỷ USD vào năm 2029; kết hợp với việc liên minh Shopify hoàn thành vòng khép kín mua sắm trong sáu tuần, giá trị tiềm ẩn của kho hàng quảng cáo của họ vượt quá 300 tỷ USD.

- Dư địa kiếm tiền khổng lồ: ARPU trên mỗi người dùng hoạt động hàng tháng hiện tại là 1,5 USD, chỉ bằng 1/10 so với Netflix; cứ mỗi 1 triệu người dùng Pro (200 USD/tháng) được thêm vào sẽ mang lại ARR hàng năm là 2,4 tỷ USD, với dư địa tăng trưởng rõ ràng.

- Định giá và giá tham gia: Giá cổ phiếu tương đương vòng tổ chức là 687,7 USD (định giá 852 tỷ USD), định giá thị trường mới nhất là 898 tỷ USD (725 USD/cổ phiếu); Bitget preOAI là kênh giao dịch duy nhất không yêu cầu tư cách nhà đầu tư, với dư địa tăng +11% đến +28% trong 12 tháng theo kịch bản cơ sở.

- Cạnh tranh không phải trò chơi tổng bằng không: Nhóm người dùng mà OpenAI (nền tảng người tiêu dùng), Anthropic (hệ điều hành cho nhà phát triển) và Google (hệ sinh thái đa dịch vụ) hướng tới hầu như không chồng chéo; mức định giá cho nền tảng người tiêu dùng của OpenAI vẫn chưa được thị trường định giá đầy đủ.

- OpenAI's 1.3 billion MAU is forming the most valuable consumer gateway in human history—users actively open it daily, it's deeply embedded in their workflows, and the switching cost is extremely high. The current $898B valuation only reflects an extrapolation of "visible revenue" from subscriptions + API. The new advertising revenue line (forecasted $25B by 2029), the re-pricing of the consumer platform, and the GPT-6 re-rating effect have not yet been fully priced in. Bitget preOAI, entering at $725/share, is currently the only channel in the retail market that doesn't require accredited investor status, and is directly linked to the public market price after the IPO.

What is OpenAI: Three Revenue Streams, A Consumer Empire Built on Active Engagement

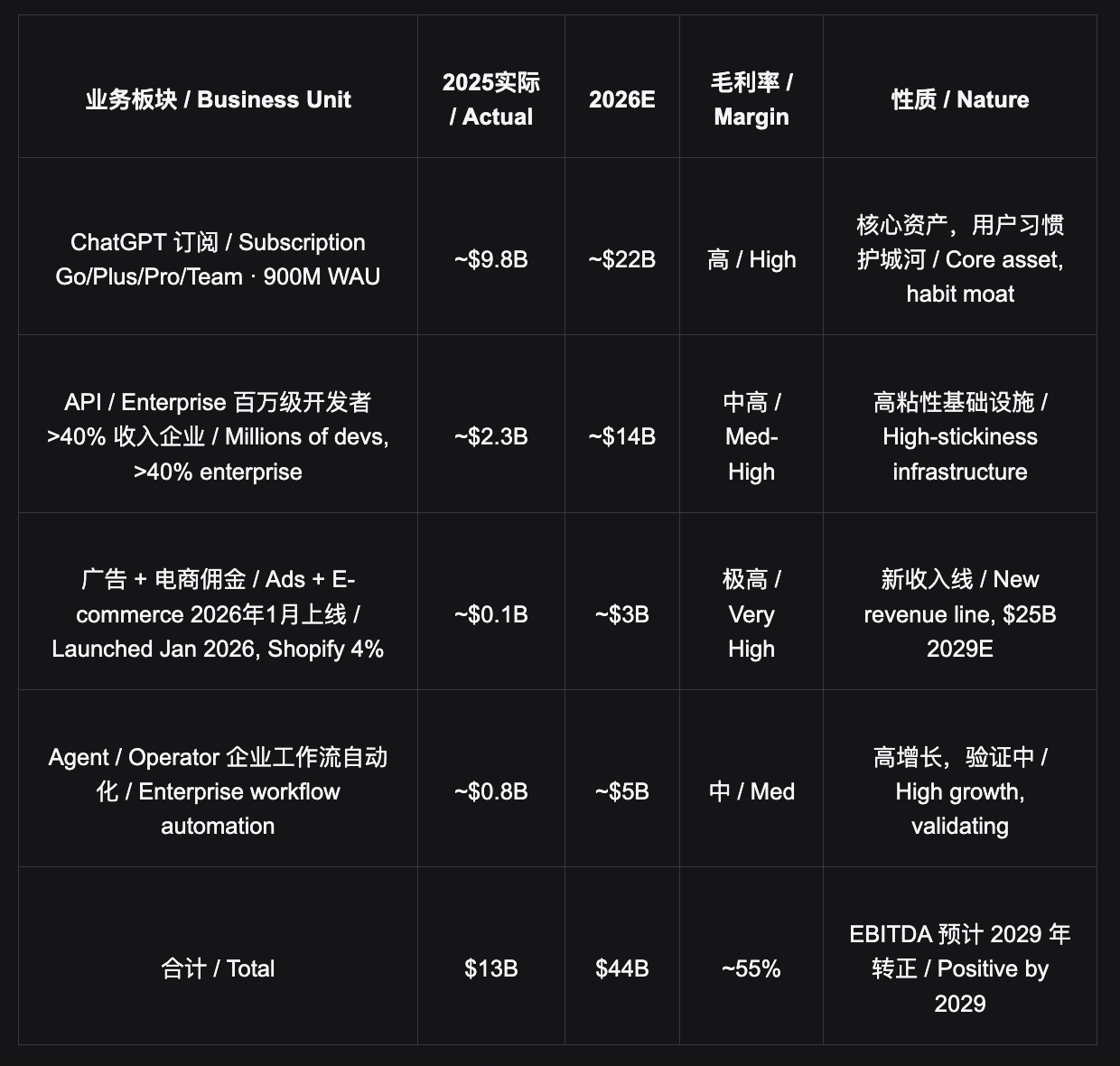

OpenAI's business cannot be understood through the single framework of an "AI company." It is simultaneously a consumer subscription platform (ChatGPT, 900 million WAU), a developer infrastructure (API, relied upon by millions of developers), an enterprise software company (Enterprise, contributing over 40% of revenue), and an emerging advertising and e-commerce platform—these four identities form a vertical closed loop centered on the consumer gateway.

ChatGPT is an app that users actively open, not a feature embedded in someone else's product. This is a fundamental difference from Google Gemini (relying on Search/Suite distribution) and Anthropic (pure API). The daily active engagement of 1.3 billion MAU constitutes the most difficult-to-replicate distribution moat in the AI field to date.

The switching cost is not just changing an app, it's a cognitive restructuring. The cost of reshaping the behavior of a user who "actively seeks answers" from ChatGPT daily is far higher than switching streaming platforms. This habit moat historically belongs only to a few platforms: Google Search, the iPhone, and WeChat—all of which eventually joined the trillion-dollar valuation club.

Why OpenAI is Worth Over $1T in the Short Term, and Approaching $2T in the Long Term

Short-Term Catalysts

The current benchmark landscape for frontier AI remains fragmented: different models have varying strengths across dimensions like knowledge work, scientific reasoning, coding, and multimodal generation. The core market concern over the past period has been: Is OpenAI losing the "absolute technological lead" narrative premium?

However, this narrative is being rewritten. OpenAI has released GPT-5.5, officially positioned as its "smartest model yet," further improving capabilities for complex tasks like coding, research, and data analysis. More critically, Image2 / ChatGPT Images 2.0 has significantly exceeded market expectations, creating a strong user-side perceptual difference in image generation, editing, text rendering, multilingual support, and practical creative scenarios.

GPT-5.5 + Image2 is sufficient to form a new product cycle: On one hand, it repairs the narrative of "OpenAI's technological lead being caught up"; on the other hand, stronger multimodal capabilities drive consumer-side activity, enterprise budget return, and high-priced subscription conversion.

1. GPT-5.5 Released: The Technological Leadership Narrative Begins to Repair

The significance of GPT-5.5 is not just a routine model upgrade, but a direct response to the narrative of "leadership advantage being eroded by Gemini / Claude" over the past year. OpenAI emphasizes GPT-5.5's capability improvements in complex tasks, research, coding, and data analysis, indicating that OpenAI still holds a strong position in core knowledge work scenarios.

Image2 Exceeds Expectations: Improvements in image generation and editing are more easily perceived by ordinary users than pure text benchmarks, and are more easily spread across social platforms. Image2 could become the core trigger for the next acceleration in ChatGPT WAU.

2. Media Cycle Explosion → WAU Continues Upward

When GPT-4 was released, ChatGPT's DAU surged 10x within a week. GPT-5.5 improves high-tier user retention, while Image2 drives ordinary user re-engagement. The combination of both is expected to push ChatGPT's active users higher.

3. Enterprise Budgets Re-Centralize Around OpenAI

GPT-5.5 covers professional workflows like research, coding, and data analysis, while Image2 covers marketing, design, e-commerce, and content production scenarios. OpenAI's platform attributes are further strengthened, giving enterprises more reason to re-consolidate their dispersed AI budgets around OpenAI.

4. Accelerated Upgrade from Free/Plus to Pro ($200/month)

Model capability leaps are the strongest driver for users to upgrade their paid tiers. Every 1 million additional Pro users = $2.4 billion in annualized ARR increment. If GPT-6 is released in the coming months and achieves full-dimensional leadership, it will further solidify OpenAI's "number one" narrative before the IPO.

5. IPO Roadshow Valuation Uplift → Q4 2026 $1T Target

OpenAI's capital market story upgrades from "waiting for GPT-6 to regain leadership" to "GPT-5.5 / Image2 has already proven the product cycle restart, GPT-6 is additional upside." This is more robust than simply betting on a future model release and makes it easier to support a higher valuation range.

Long-Term Bullish · Long-Term Bull · Consumer Super-Platform / Consumer Super-Platform

OpenAI is not just an AI company; it is becoming the "default interface for human interaction with information and tasks." Only a handful of products have historically reached this position: Google Search, the iPhone, and WeChat—all of which eventually entered the trillion-dollar valuation club.

- ARPU Comparison: Full Monetization Space. OpenAI's current blended ARPU is approximately $1.5/month ($25B ARR / 1.3B MAU). Netflix: $15/month; Microsoft 365: $10-25/month; Spotify: $10/month; Instagram Advertising Global Average: $3.3/month. ChatGPT's usage depth and frequency rival any subscription product, but its monetization is only 1/10th of Netflix. This gap isn't a ceiling; it's room for growth.

Advertising Business: An Overlooked New Revenue Line. Ad testing began in January 2026, with a full rollout to US users in February. Internal forecasts predict $1B in ad ARR for 2026, reaching $25B by 2029. The Shopify partnership has already proven a closed loop: in-chat shopping exceeded $100M ARR within six weeks, taking a 4% commission. The ad inventory from 900 million WAU, valued at the global average for Facebook, implies a value of over $300B. Almost no one modeled this revenue line into the $898B valuation.

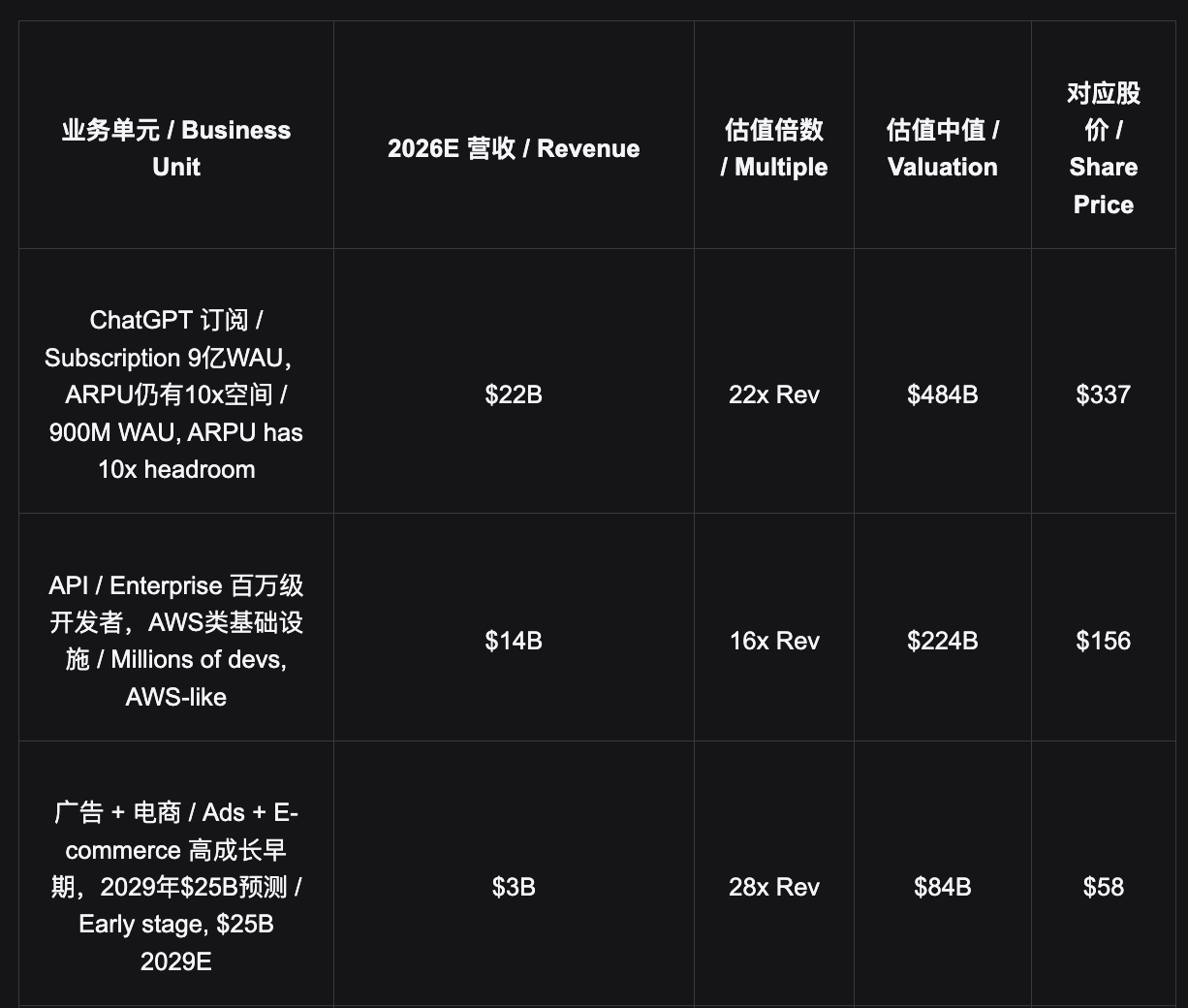

Sum-of-the-Parts Valuation: $898B is Already Below Intrinsic Value

Using expected 2026 financial data for a forward-looking valuation aims to assess whether the Bitget preOAI entry price of $725 is within a reasonable range and to identify sources of upside.

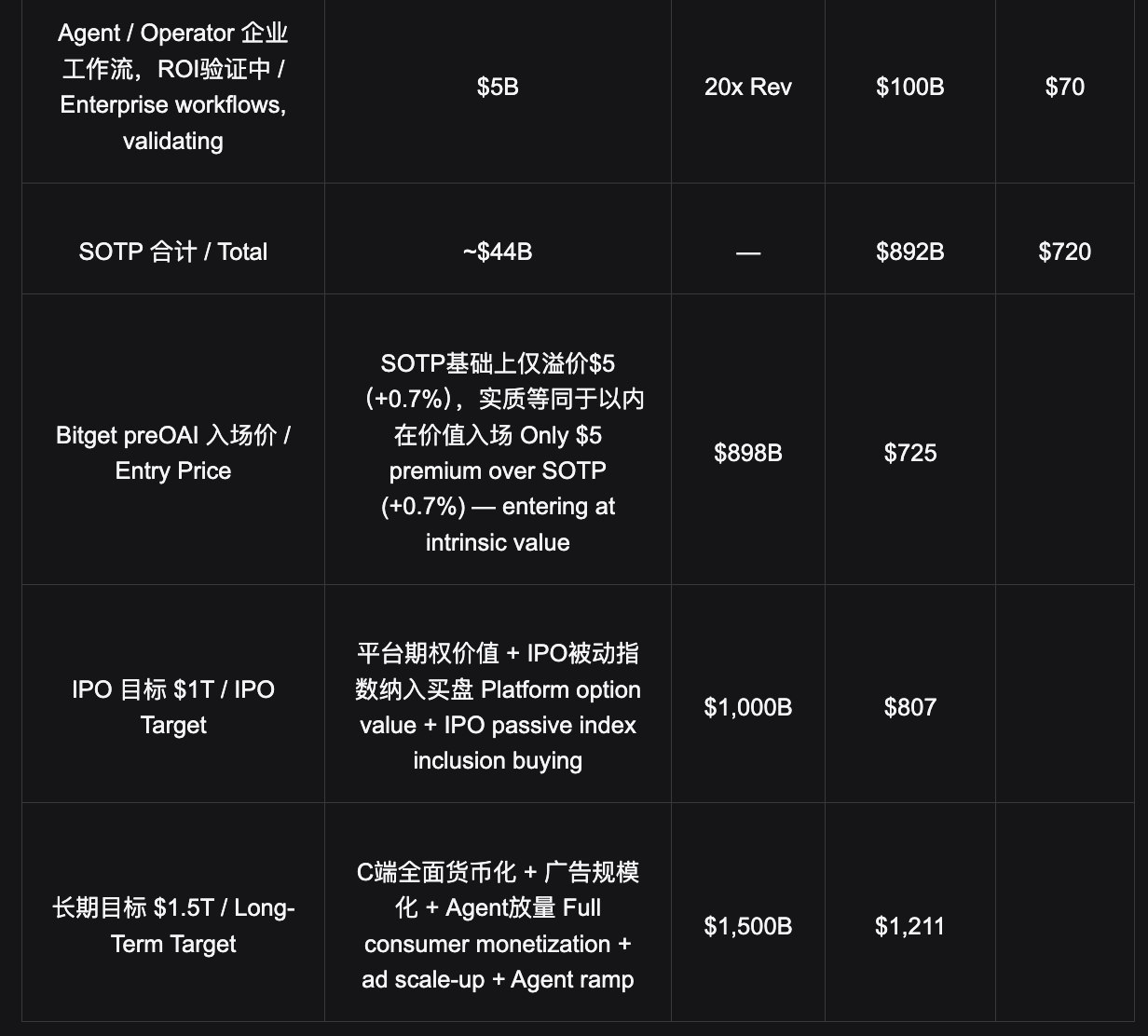

- Core Valuation Conclusion: The $725 entry price is nearly flat with the SOTP median of $720—meaning you enter at a price reflecting "only the visible business." The $300B+ implied option value from the advertising business, the AGI option value, and the upside from re-pricing the consumer platform premium have not yet been factored in. $898B is not an overvaluation; it underestimates the new revenue curve.

Pre-IPO Entry: Channel Comparison and Pricing Analysis

OpenAI is a private company; ordinary investors cannot directly purchase its equity through any public market. Key fact: The Series G institutional round equivalent share price was $687.7 ($852B valuation), with a minimum subscription threshold of $100 million—a magnitude impossible for individual investors regardless of asset size. Bitget preOAI at $725/share corresponds to the current latest market valuation of $898B, making it the only retail market channel with secondary market liquidity.

Access Channel Comparison / Access Channel Comparison

Series G · $687.7

Institutional Round · Institutional Round · Closed / Closed

Implied $852B · Closed / Implied $852B · Closed · Min $100M

To IPO Low End +17.3%

To LT Target $1.5T +76.1%

SoftBank led the $122B round, minimum $100M, accessible only to large institutions. Institutional cost: $687.7 ($852B); current preOAI at $725 corresponds to the latest $898B valuation—the market has repriced OpenAI, and institutions are already up 5.4% on paper.

Hiive · $608

Real Equity · Real Equity · Accredited Only / Accredited Only

Implied $873B · Secondary Transfer / Secondary Transfer

To IPO Low End +32.7%

To LT Target $1.5T +99.2%

Requires accredited investor status (net worth ≥ $1M) and a minimum subscription of $25,000. Private equity transfer, no secondary market, transfer cycles measured in weeks—catalyst events cannot be reacted to in real-time.

preOAI · $725

Bitget IPO Prime · Tokenized / Tokenized · Only Tradeable / Only Tradeable

$898B · Latest Market Price / Latest Market Price · No Accreditation / No Accreditation

To IPO Low End +11.3%

To LT Target $1.5T +67.0%

Only channel with a secondary market. Tokenized structure, no accredited investor requirement, no minimum amount limit. Can be bought and sold anytime—catalyst events like GPT-6 launch, IPO announcements can be traded in real-time. Post-IPO settlement directly links to OpenAI's public market price.

- Liquidity is the core differentiator: preOAI is a tokenized product with a secondary market, allowing buying and selling anytime—GPT-6 releases can be traded on price catalysts within weeks, capturing the window. Hiive is a private equity transfer, no secondary market, cannot react to catalysts; institutional rounds also lack exit paths. preOAI at $725 is approximately 5.4% above the institutional round of $687.7, corresponding to the latest $898B market valuation—the entry price reflects the latest market consensus on OpenAI's value.

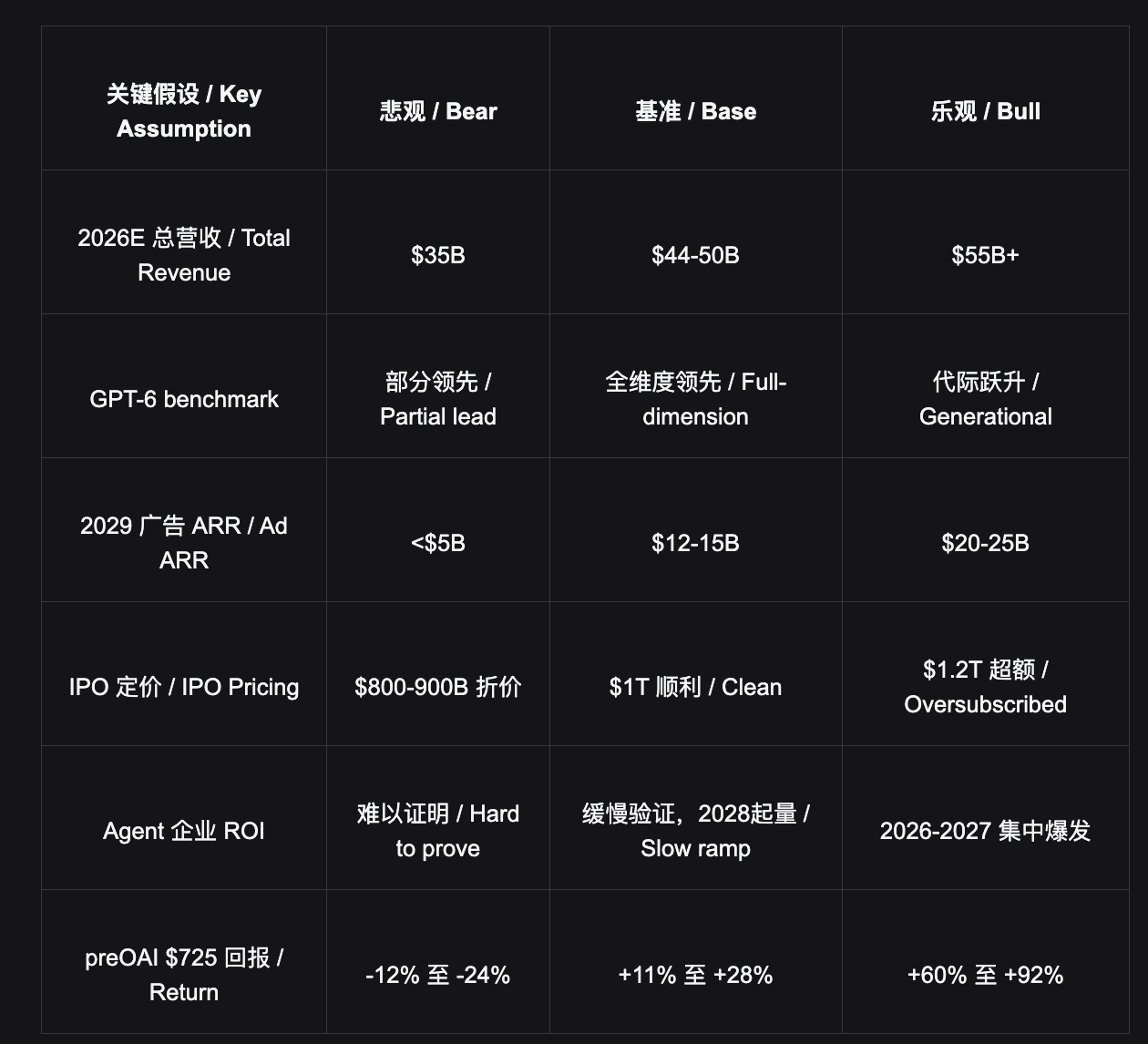

Scenario Analysis and Key Assumptions

Scenario Analysis / Scenario Analysis

Bear Case $475—$550 $682B — $790B

GPT-6 disappoints; Gemini significantly erodes market share; advertising monetization damages user trust; IPO priced at a discount. Calculated from preOAI $725: downside of approximately -12% to -24%. ChatGPT's 1.3 billion MAU provides a floor.

Base Case (Primary) $807—$928 $1T — $1.15T

GPT-6 rebuilds leadership, IPO Q4 2026 priced at $1T, advertising gradually scales, 2026E revenue of $44-50B realizes as expected. Calculated from preOAI $725: upside of approximately +11% to +28%, visible within 12 months.

Bull Case $1,000—$1,200 $1.44T — $1.72T

GPT-6 establishes generational leadership, Agent enterprise ROI is proven and accelerates volume, IPO is oversubscribed, advertising reaches $25B ahead of the 2029 schedule. Calculated from preOAI $725: upside of approximately +60% to +92%.

※ Key Downside Risks: ① Google Gemini leverages its full product suite for a large-scale comeback (20% probability); ② Advertising monetization damages user trust leading to WAU contraction (10%); ③ Persistent Agent delivery delays affect Enterprise renewals (15%); ④ Governance controversies (10%). The impact of these risks occurring independently is limited; Floor support: The user habit moat of ChatGPT's 1.3 billion MAU will not collapse.

LLM Competitive Landscape: Strategic Divergence and Long-Term Coexistence of the Big Three

Competition in the large model layer is not a zero-sum game, but rather coexistence among a few oligopolists—each company's core user base hardly overlaps. OpenAI's 1.3 billion active users, Anthropic's 1-2 million high-paying developers, and Google's 3 billion ecosystem users represent three different infrastructure models of the AI era.

Competitive Landscape / Competitive Landscape

OpenAI

$852B (Institutional Round / Institutional Round)

▸ Strengths / Strengths

1.3B MAU consumer gateway, active engagement, habit moat; The only entity capable of fundraising at "national scale"; Bottom-up culture allows for generational leaps by talent

▸ Challenges / Challenges

Coding being encroached upon by Anthropic; 300+ internal projects, execution dispersion; High C-end traffic creates pre-training burdens

▸ LT Ceiling / LT Ceiling

$1.5T+ (Consumer Platform Grade / Consumer Platform Grade)

Anthropic

Existing shares imply ~$800B, next round expected $800-850B

▸ Strengths / Strengths

Sacrificed C-end to go All-in on Coding, organizational execution is the moat; 1-2 million core developer revenue already exceeds OpenAI's 50 million consumer subscriptions; API transitioning to Agent OS

▸ Challenges / Challenges

No consumer platform, ceiling is "the best developer tool" rather than "the largest consumer platform"

▸ LT Ceiling / LT Ceiling

$1.5T+ (Developer OS Grade / Developer OS Grade)

Google / Gemini

Alphabet $2T (AI upside not separately priced)

▸ Strengths / Strengths

Abundant compute, most data, unrivaled distribution (3B+ ecosystem users); Complete advertising infrastructure

▸ Challenges / Challenges

Inflated benchmarks, Coding behind by 3-4 months; Complex internal politics, lack of PM culture; Always chasing, always half a step behind

▸ End-Game / End-Game

Each finds its place; Google strong in distribution, OpenAI strong in active gateway

- Core Judgment: OpenAI and Anthropic are both long-term $1.5 trillion-level companies. Different paths, similar destination—OpenAI takes the consumer platform path (like Apple/Google), Anthropic takes the developer OS path (like AWS). The core user bases of the two companies hardly overlap. This is not a zero-sum game, but the parallel evolution of two dominant infrastructure models of the AI era. However, OpenAI's consumer platform premium has not yet been fully priced by the market—this is the core thesis for entering at $725 and the structural mispricing compared to Anthropic.

Disclaimer

This report is for internal research reference only and does not constitute investment advice. The tokenized product (preOAI) does not grant shareholder rights, voting rights, or dividend rights. Economic returns are linked to a reference index, and the settlement mechanism relies on the platform's credit. Private equity (Hiive) is limited to accredited/certified investors, with fees of 3-5% and lock-up periods depending on the shareholding structure. OpenAI's S-1 is in the preparation stage; IPO valuation, timing, and offering structure are subject to change. Financial forecasts are analyst estimates, not official disclosures by OpenAI.

OpenAI — $122B Funding Announcement · CNBC — Series G $852B · Sacra — OpenAI Equity Research 2026 · Business of Apps — ChatGPT Statistics 2026 · Hiive — OpenAI $608.06 (April 2026) · Polymarket — GPT-6 Release Odds · IndexBox — OpenAI IPO $1T Target 2026 · ALM Corp — ChatGPT Ads $25B 2029 Projection