首日交易量碾压Polymarket,Hyperliquid带着BTC二元期权杀入预测市场

- 核心观点:Hyperliquid 通过 HIP-4 上线 BTC 日内二元结果合约,将预测市场直接整合进其链上交易系统,首日交易量即超越 Polymarket 和 Kalshi 同类市场,旨在将事件合约转化为交易者的风险管理工具,并强化其代币 HYPE 的价值捕获机制。

- 关键要素:

- HIP-4 首日数据亮眼:BTC 价格事件合约交易量达 615 万美元,交易笔数超 5.4 万,参与交易者超 3000 人,远超同类型市场冷启动表现。

- 结算机制创新:HIP-4 作为独立结果市场原语,专为二元结果(0/1)设计结算、争议和预言机确认流程,避免错价套利风险,不同于永续合约的连续定价模式。

- 差异化定位:与 Polymarket(事件丰富度)和 Kalshi(合规路径)不同,Hyperliquid 利用其 L1、链上订单簿和 200k 笔/秒的处理能力,提升交易体验和资金效率。

- 代币质押门槛:未来无许可部署结果市场需质押 100 万枚 HYPE(高于 HIP-3 的 50 万),用于防止预言机操纵等风险,增加 HYPE 的链上质押需求。

- 价值捕获飞轮:协议费用将用于回购 HYPE,若 HIP-4 带来新增交易量,将直接推动 HYPE 的需求和回购规模,形成增长飞轮。

- 发展阶段:当前仅聚焦 BTC 日内市场,尚处在早期,后续需验证能否扩展至体育、政治等品类,以及预言机结算机制的可靠性。

Original by Odaily (@OdailyChina)

Author: Asher (@Asher_0210)

On May 2, Hyperliquid launched HIP-4 Outcome Markets on its mainnet, officially introducing outcome markets to its on-chain trading system. The first batch listed are BTC intraday binary outcome contracts, allowing users to trade on whether the BTC price will be above a specified price at a certain point in time. Contract prices float between 0.001 and 0.999, representing the market's pricing of the event's probability; they settle at 1 if the event occurs and 0 if it does not. Contracts are fully collateralized in USDH, with no fees for opening positions.

This is not a simple product expansion. In the past, Polymarket has functioned more like an information market centered around events, where users enter a specific market due to elections, sports, geopolitical conflicts, or crypto trends, using prices to express their judgment on outcomes. Kalshi, on the other hand, attempts to fit event contracts into a clearer regulatory framework.

Hyperliquid's approach is different. Instead of first building a standalone prediction market and then attracting users to migrate their funds, it directly enters from its most familiar trading environment—allowing outcome contracts, perpetuals, and spot trading to coexist in the same trading interface. For Hyperliquid, prediction markets are not just about betting on an outcome, but a new tool for traders to express direction, manage risk, and construct strategies.

BTC Intraday Market Off to a Strong Start, First-Day Data Exceeds Expectations

The first market under HIP-4 is a daily settlement BTC price performance market. This choice itself is very "Hyperliquid"—instead of starting with political, sports, or entertainment events, it focuses on the BTC price volatility most familiar to crypto traders.

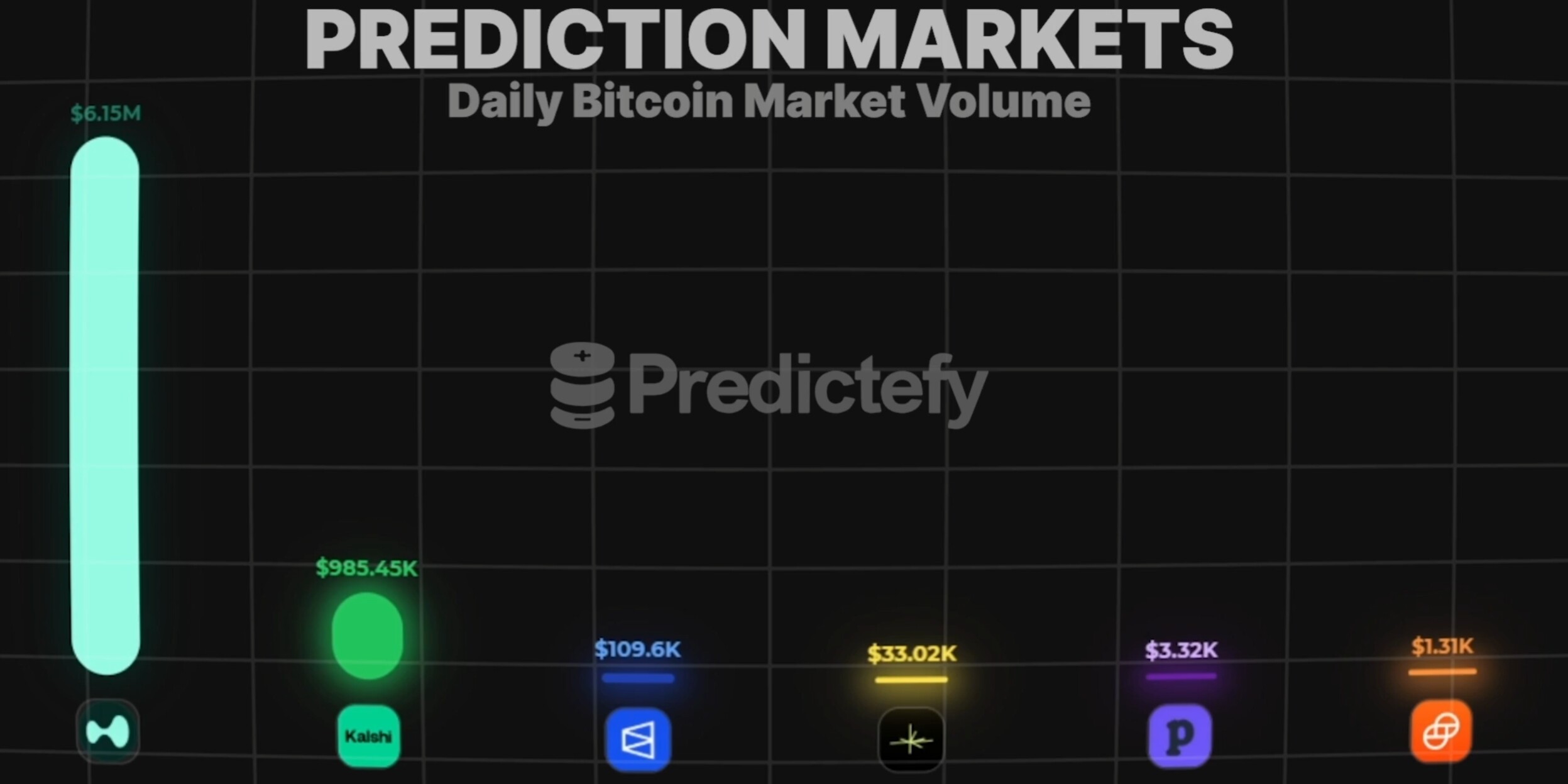

On its first day, HIP-4 posted impressive data. According to Predictefy, on the first day of Hyperliquid's event contracts launch, the trading volume for its BTC price-related event contracts reached $6.15 million, significantly surpassing similar markets on Kalshi, Polymarket, and other prediction platforms. In other words, looking solely at the niche of BTC price-related event contracts, Hyperliquid has already reached the top tier on day one.

Data Source: Predictefy

Furthermore, on the first day of the HIP-4 launch, total fees from trading volume exceeded $12,000, with over 54,000 trades and more than 3,000 participants. For a newly launched prediction market-related HIP-4, this set of data is already quite impressive. It wasn't achieved by rolling out a vast array of event categories, but by completing a cold start within the single BTC intraday market, making HIP-4's first step even more significant.

Why HIP-4 Isn't Simply a Modification of HIP-3

Hyperliquid previously supported Builders in deploying perpetual contract markets through HIP-3. So the question arises: if the perpetual market can already be deployed, why is a separate HIP-4 needed? The answer lies in the fundamentally different settlement logic of outcome contracts.

Perpetual contracts require continuous pricing, where the oracle price can be adjusted gradually; but binary outcome contracts can only settle at 0 or 1. If an oracle mechanism unsuitable for binary contracts were used, it could leave a lengthy window for incorrect pricing even after the event outcome is determined, creating nearly risk-free arbitrage opportunities for traders.

Therefore, HIP-4 is designed as a separate outcome market primitive. It is not a rebranded perpetual, but a contract type specifically designed for expiration, settlement, disputes, and Oracle result confirmation. For the average user, a prediction market might just seem like buying Yes or No; but for a real trading system, the true difficulty lies in how the event is defined, who confirms it, when it settles, how disputes are handled, and how erroneous results are corrected and penalized. The core of a prediction market is not just the front-end page and trading entry, but the settlement mechanism itself.

Hyperliquid, Polymarket, and Kalshi Each Have Their Own Battlefield

If we look at Hyperliquid's HIP-4, Polymarket, and Kalshi together, they represent three different directions for prediction markets:

- Polymarket's core advantage is event richness and user mindshare: It excels at turning complex events into tradable questions, combining public attention, media dissemination, and market probabilities. Political elections, geopolitical conflicts, celebrity events, sports tournaments, and crypto project milestones can all be quickly transformed into markets.

- Kalshi's strength lies in its compliant pathway: It is closer to an event contract platform within the traditional financial context, with a target user base and regulatory framework not entirely identical to Polymarket or Hyperliquid. The recent escalating debate in the US over prediction market regulation, and the conflict between the CFTC and state-level regulators, also indicates that event contracts are no longer a fringe product but have entered the core discussion area of financial regulation.

- Hyperliquid's advantage is trading experience and capital efficiency: Hyperliquid has its own L1, HyperCore matching engine, on-chain order book, and spot and perpetual infrastructure. Official documentation shows HyperCore includes fully on-chain perpetual and spot order books, with orders, cancellations, trades, and liquidations executed transparently, capable of processing 200k orders per second.

Therefore, Hyperliquid may not necessarily steal all of Polymarket's users in the short term. A lightweight user interested in the US election, sports events, or entertainment gossip might not enter Hyperliquid's trading interface just to buy an event contract. However, a trader already using Hyperliquid for BTC, ETH, gold, oil, or stock perpetuals might naturally incorporate BTC intraday outcome contracts as part of their portfolio.

HYPE Could Become the Primary Value Capture in This Competition

The significance of HIP-4 for Hyperliquid goes beyond adding a new trading scenario; it further binds the prediction market with HYPE staking, fees, and buyback mechanisms. According to HIP-4's design, the first phase involves validators deploying standardized markets, with the second phase opening up to permissionless deployment. Future market creators wishing to create their own prediction markets will need to stake 1 million HYPE. Each staking seat can support rolling and periodic markets, which can be reused after settlement; in cases of oracle manipulation, abnormal market states, or prolonged downtime, the staked assets may be slashed.

This threshold is significantly higher than HIP-3's 500,000 HYPE. The reason isn't hard to understand: outcome markets are more dependent on event definition and Oracle settlement than perpetual markets. Perpetual market prices can adjust continuously, but outcome markets only have 0 and 1 as final outcomes. An erroneous settlement damages not just the trading experience of a specific market, but the credibility of the entire prediction market system.

For HYPE, HIP-4 brings two layers of incremental demand. First is staking demand. More Builders wanting to deploy outcome markets need to lock up more HYPE. This is especially true as categories like sports, macroeconomics, politics, crypto events, and entertainment gradually open up, making the right to create high-quality markets a potentially high-barrier franchise. Second is the fee and buyback logic. Hyperliquid already has strong trading volume and fee capture capabilities, with a significant portion of protocol fees used to buy back HYPE. If HIP-4 can generate new trading volume, outcome markets won't just be an added feature, but will become part of the growth flywheel for fees and HYPE buybacks.

This is also a key difference between Hyperliquid and Polymarket or Kalshi. Growth for Polymarket and Kalshi is more reflected in platform trading volume, market share, and brand influence; whereas Hyperliquid's growth maps more directly onto the demand and value capture for HYPE.

Market is Optimistic, but HIP-4 Still Needs to Prove Itself

The market's feedback on HIP-4 leans optimistic, for a straightforward reason. Hyperliquid already has mature trading infrastructure, active trading users, and a clear HYPE value capture mechanism. Entering the prediction market doesn't require building a matching system from scratch or finding the first batch of traders from zero.

However, HIP-4 is still in a very early stage. Currently, the market is concentrated on BTC price outcomes. Whether it can successfully expand to more categories like sports, politics, macroeconomics, crypto events, and entertainment depends on the smooth rollout of the permissionless deployment in the second phase. Additionally, outcome markets have higher requirements for oracles and settlement mechanisms. Event definition, data source selection, dispute handling, and erroneous settlements will all directly impact market trust.

So, the significance of HIP-4 is not that Hyperliquid has already won the prediction market, but that it offers a new competitive direction for this track. Polymarket proved that events can become information markets, Kalshi represents the path of compliant event contracts, and Hyperliquid aims to prove that event contracts can also be an integral part of an on-chain trading system.

If past competition in prediction markets was about who could capture more trending events and attract more users to bet, then after HIP-4, a new line of competition has emerged: who can truly integrate event outcomes into a trader's capital, positions, and strategies.

This also means Polymarket's competitor is no longer just Kalshi. With Hyperliquid entering the fray, the next phase of prediction markets might not just be competition between event markets, but competition between trading systems, liquidity, and asset pricing capabilities.