一年暴涨39倍,美股存储板块还能买吗?

- 核心观点:AI 革命的主角正从 GPU 转向存储硬件,内存与存储板块成为新的「卖铲人」,其中 DRAM 结构性稀缺最强,NAND 次之,HDD 稳定增长,SanDisk 因独立时机精准成为最大黑马。

- 关键要素:

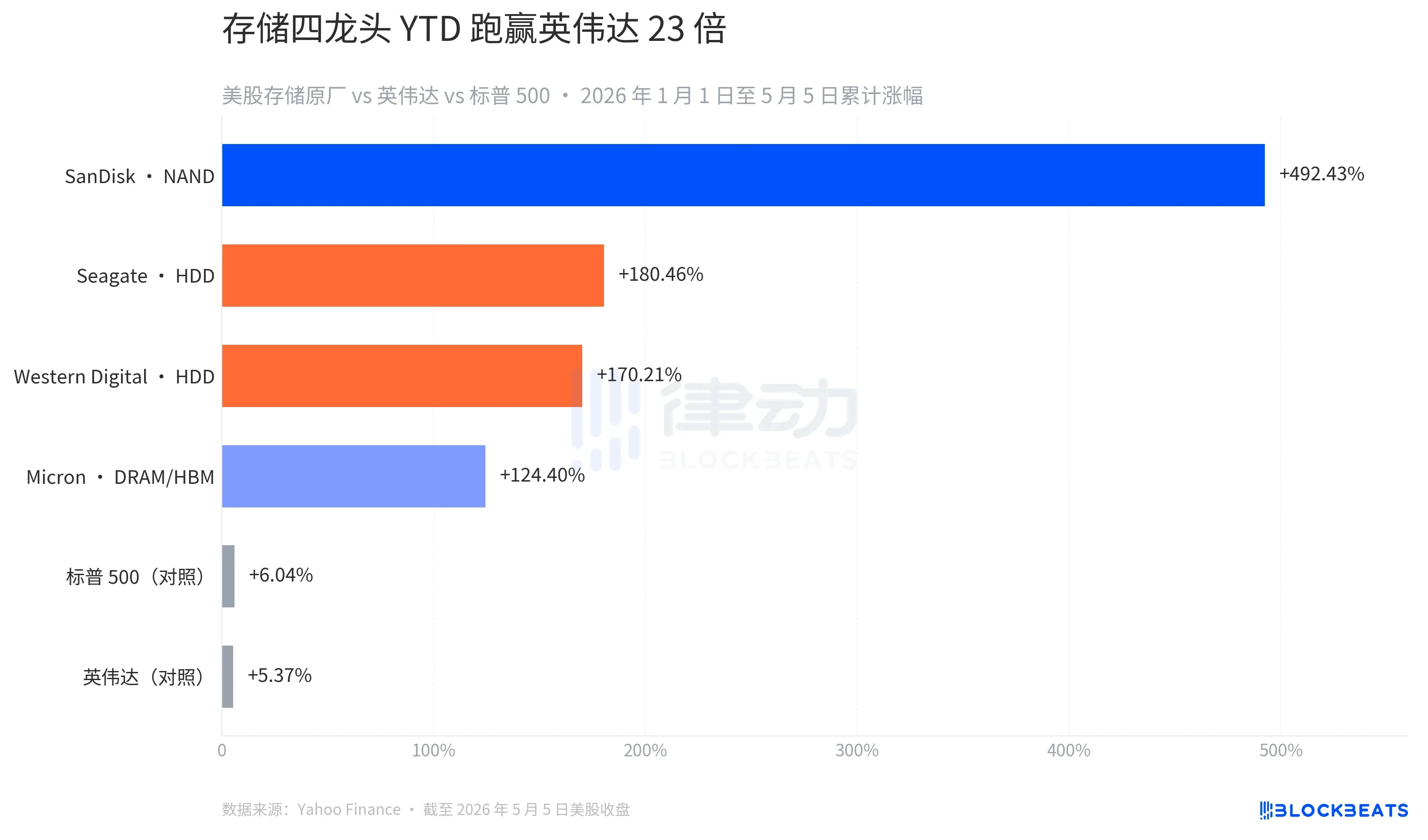

- 2026 年初至今,美股四家存储原厂股价涨幅在 124% 到 492% 之间,最低者也远超英伟达(5.37%)和标普 500(6.04%)。

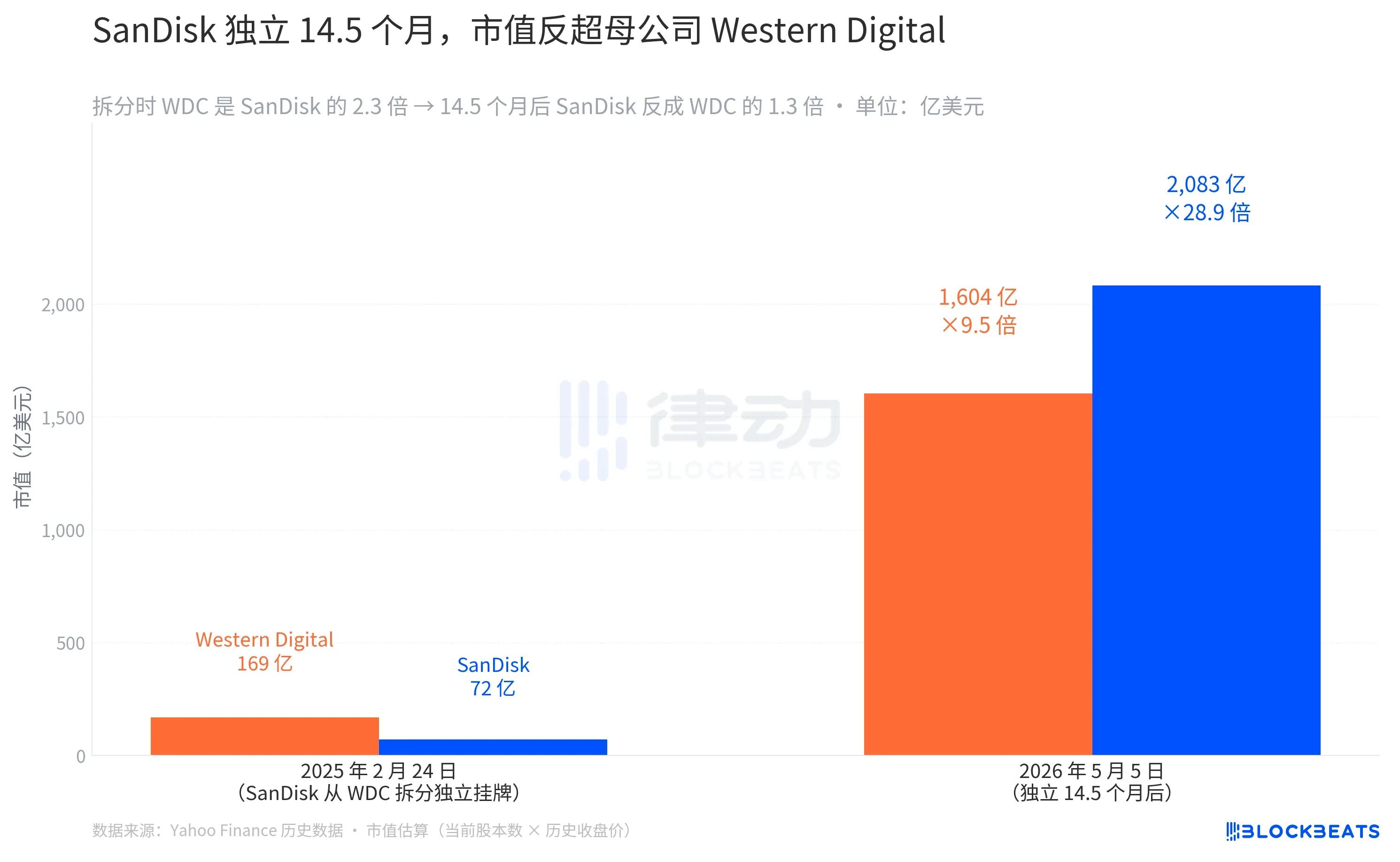

- SanDisk 年内暴涨 492%,独立 14.5 个月后市值(2083 亿美元)反超母公司 Western Digital(1604 亿美元),打破常规拆分案例规律。

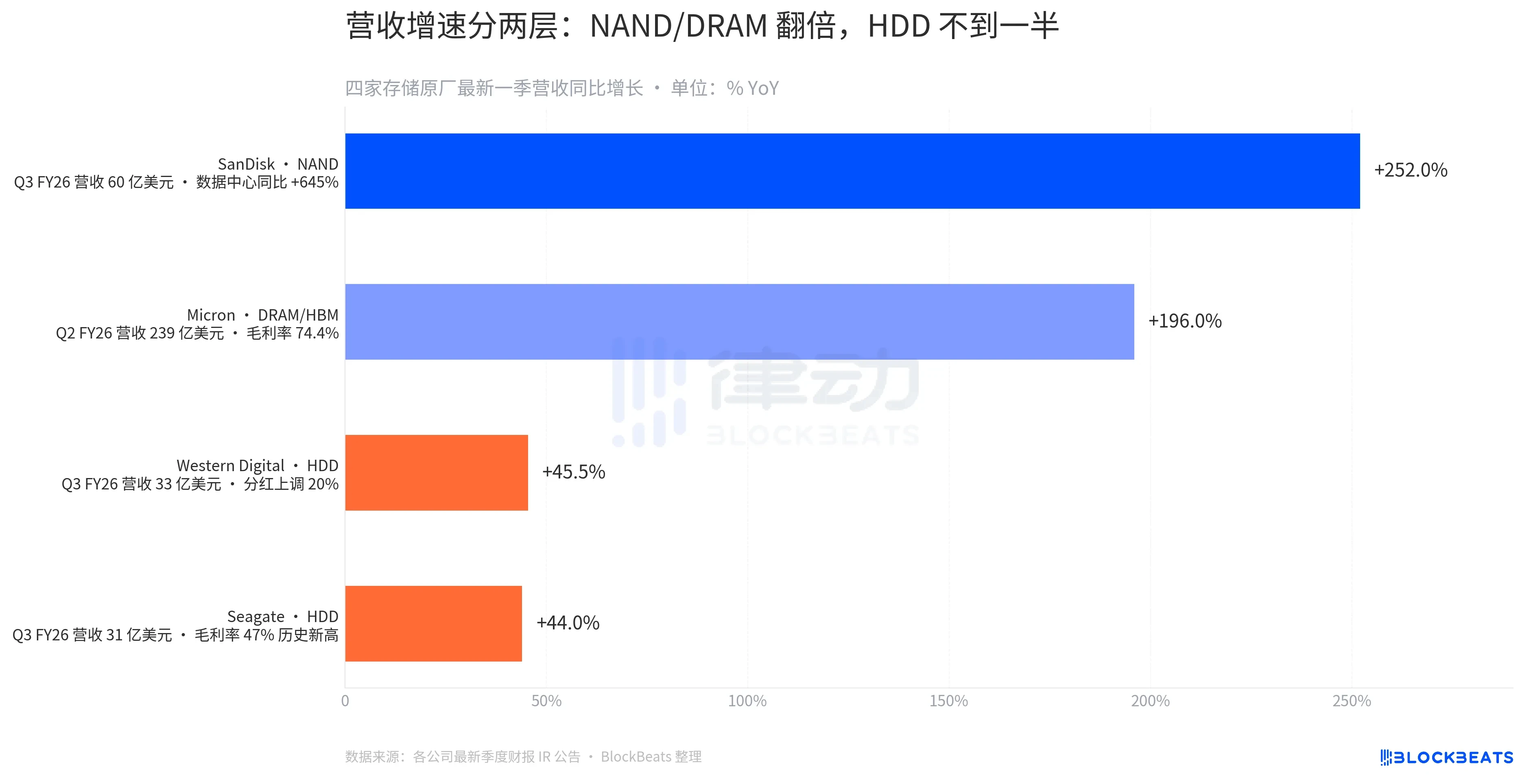

- 存储板块涨幅分化:NAND 厂商(SanDisk)营收同比 +252%,DRAM/HBM 厂商(Micron)营收同比 +196%,而 HDD 厂商(Seagate 和 Western Digital)营收同比约 44-45%,相差 4-5 倍。

- 利润率分层更极端:Micron 毛利率高达 74.4%,Seagate 毛利率 47% 为其历史新高,背后反映 HBM 供给集中在三家寡头,价格谈判力远超分散的 HDD 市场。

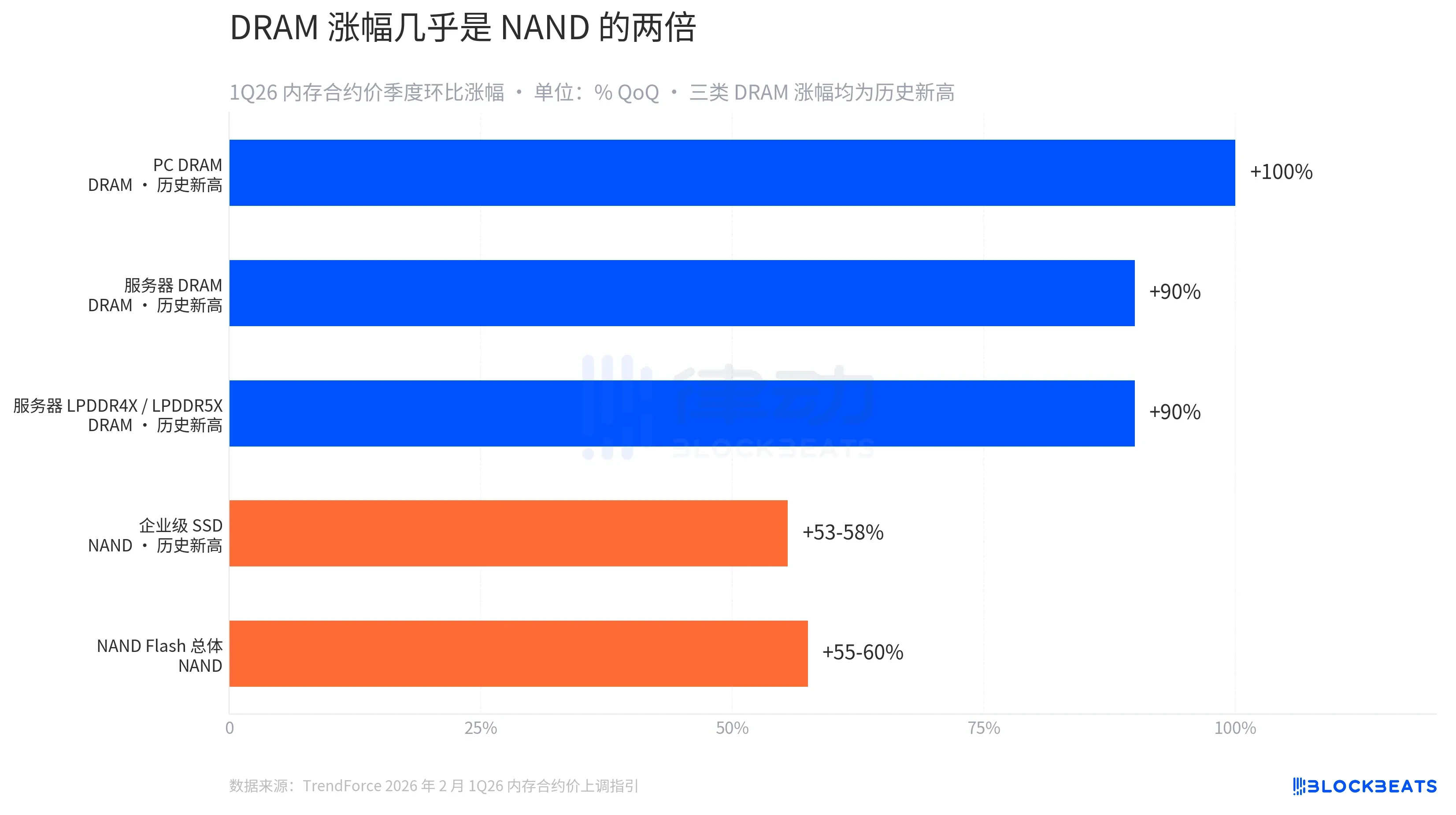

- TrendForce 数据显示 1Q26 内存合约价创历史新高:PC DRAM 季度环比 +100%,服务器 DRAM 约 +90%,而企业级 SSD 涨幅约 53-58%,DRAM 供需缺口大于 NAND。

- SanDisk 已签订 5 份长期合约并收到 110 亿美元财务担保,2027 财年超三分之一 NAND 比特被客户锁定,标志存储行业首次出现类似晶圆代工的长期预付结构。

The S&P 500 has risen 28% over the past 12 months, and Nvidia has gained 73%. However, compared to the storage sector, these gains are still modest. SanDisk, priced at $34.61 a year ago, is now at $1,406.32, a surge of 39 times.

This NAND flash memory manufacturer, spun off from Western Digital just 14.5 months ago, is the best-performing individual stock on the US stock market so far in 2026, skyrocketing 492% year-to-date. Behind it are Micron, Seagate, and Western Digital. The year-to-date (YTD) gains for these four major US storage manufacturers range from 124% to 492%. Even the lowest performer among them has outperformed Nvidia by 23 times. The "pick-and-shovel seller" label of the AI revolution is shifting from the GPU end to the memory end.

May 5th was a particularly notable day. SanDisk surged 11.98% in a single day, Micron rose 11.06%, Western Digital gained 5.18%, and Seagate increased 4.38%. Among the four major US storage manufacturers, three hit new 52-week highs.

The catalysts were two earnings reports and a supply narrative. On April 28th, Seagate reported Q3 FY26 revenue up 44% year-over-year and a record gross margin of 47%. CEO Dave Mosley stated on the conference call, "AI is ushering Seagate into a new era of structural growth," noting that nearline exabyte capacity is already allocated through 2027.

Two days later, SanDisk reported Q3 FY26 revenue of $5.95 billion, up 252% year-over-year and $1.15 billion above the high end of its guidance. Data center revenue surged 645% year-over-year, nearly doubling sequentially. Q4 guidance calls for another 308% to 334% increase year-over-year. Coupled with Micron receiving a credit rating upgrade from Fitch, the entire sector saw a collective rally on Monday.

But that's the surface level. Looking across the four stocks, the notion of a "storage sector rally" is actually misleading. They are rising on three completely different supply narratives, with vastly divergent gains.

In terms of year-to-date (YTD) performance: SanDisk +492.43%, Seagate +180.46%, Western Digital +170.21%, and Micron +124.40%, placing them in four entirely different tiers. During the same period, the S&P 500 rose 6.04%, and Nvidia gained 5.37%. Nvidia has even fallen 7.82% in the past five days. The "primary AI beneficiary" label is migrating: the GPU story driven by large model training has completed its valuation expansion cycle over the past year. Capital is now shifting downstream, moving into the memory and storage needed to handle AI workloads.

This migration is not uniform. It is stratified according to media properties.

Recent quarterly earnings figures clearly illustrate this stratification. SanDisk saw NAND revenue up 252% year-over-year, Micron saw DRAM/HBM revenue up 196% year-over-year, while Western Digital and Seagate saw HDD revenue up between 44-45% year-over-year. NAND and DRAM represent the explosive growth tier in this cycle, while HDD represents the steady growth tier, with a 4 to 5 times performance gap between them.

The stratification in gross margins is even more dramatic. Micron's Q2 FY26 gross margin was 74.4%. This is an extreme figure achievable by a chip manufacturer, meaning for every $100 worth of DRAM and HBM sold, $74 flows into the profit statement. Seagate's 47% gross margin, while a historical high for the company, is still an order of magnitude lower than that of DRAM makers. This reflects differences in supply structure. HBM production capacity is concentrated among three players (SK Hynix, Samsung, Micron) and is largely sold out under long-term contracts through the end of 2026. HDD capacity, however, is more evenly distributed between Seagate and Western Digital, resulting in relatively fragmented pricing power.

Price signals tell the same story.

According to TrendForce's revised 1Q26 memory contract price forecast on February 2nd, PC DRAM prices are expected to rise 100% quarter-over-quarter, server DRAM about 90%, and server LPDDR4X/5X about 90%. These price hikes for all three types of DRAM are historical records. On the NAND Flash side, enterprise SSDs are expected to rise 53% to 58% during the same period, with overall NAND up 55% to 60% – an increase only slightly more than half that of DRAM.

This reflects a crucial divergence. AI servers require both NAND and DRAM, but they have a greater need for bandwidth (HBM) and capacity density (DDR5, LPDDR5X). The supply-demand gap for DRAM is much larger than for NAND. Micron's CEO succinctly put the supply story during the Q2 FY26 earnings call: "We're sold out for 2026." HBM4 36GB 12H has already begun volume shipments for Nvidia's Vera Rubin platform. The FY26 full-year capital expenditure has been increased from $20 billion to $25 billion to prepare for another ramp-up in 2027.

Among the four manufacturers, SanDisk deserves the closest individual examination.

SanDisk was spun off from Western Digital on February 24, 2025, and began trading on the Nasdaq. It opened at $52 on its first day, closed at $48.60, giving it a market cap of approximately $7.2 billion. On the same day, Western Digital closed at $49.02, with a market cap of about $16.9 billion. On the day of the split, Western Digital was 2.3 times the size of SanDisk.

Today, 14.5 months later, SanDisk's market cap stands at $208.3 billion, while Western Digital's is $160.4 billion. SanDisk has now become 1.3 times the size of its former parent. This kind of reversal is uncommon in the history of major corporate spin-offs. In most cases, the subsidiary spends the first year re-establishing investor relations, and it typically takes 3 to 5 years for its market cap to catch up to the parent company. SanDisk did it in 14.5 months.

The reason is that it was spun off at the perfect time. When Western Digital decided to split in 2024, the stated rationale was that "NAND and HDD are in different capital cycles, and separate operations will provide clearer valuation." This judgment has since been validated by the market: SanDisk, independent and focused on NAND, perfectly captured the explosive demand for enterprise SSDs from AI data centers. Western Digital, dedicated to HDDs, capitalized on the structural growth of cloud storage archiving. Separated, each company corresponds to a distinct narrative. If they had not split, a single company housing two businesses with completely different supply cycles would likely have been valued more conservatively by the capital markets, landing somewhere in between.

On May 4th, Bernstein raised its price target for SanDisk from $1,250 to $1,700, citing the visibility of the data center SSD business. SanDisk's earnings report revealed it has signed five long-term contracts, received $11 billion in financial guarantees, and has locked in over one-third of its NAND bits for fiscal year 2027. This is a sector traditionally treated as a commodity cycle, now showing a "long-term contract + customer prepayment" structure for the first time, similar to advanced process wafer foundries.

Overall, capital is flowing from the GPU side to the memory side. DRAM is the true alpha in this cycle. HDD represents a structural long-distance race at a different pace. SanDisk, a company independent for only 15 months, has surpassed its parent company Western Digital in market capitalization, driven solely by its NAND data center business.

On the same trading day, May 5th, Nvidia fell 1.03%, TSMC fell 1.79%, but SanDisk rose 11.98%. All are considered "AI beneficiaries," but the market is already voting with its feet, distinguishing which segment of supply is the most scarce.