Who is actually trading on Trade.xyz?

- Core Insight: On-chain analysis of Trade.xyz reveals that while the platform does indeed have a large number of Sybil wallets (accounting for 44% of total wallets), they only contribute 0.77% of the trading volume. The real force behind the platform’s over $50 billion in monthly trading volume is a small group of professional market makers (such as Jump, Selini, Wintermute), arbitrage bots originating from Bybit, and a retail user base that heavily overlaps with Polymarket.

- Key Elements:

- Sybil Layer Disconnected from Volume: 35,453 Sybil wallets can be traced back to the same Polymarket account "Themino," employing a relay-style strategy of small, two-way trades. However, their cumulative trading volume is only about $400 million, representing 0.77% of the total.

- Highly Concentrated Market Maker Power: 363 market maker wallets (0.46% of total) drove 63% of the total trading volume ($327.5 billion). The top 5 accounted for half of this market-making volume, including Powell, Jump Crypto, Selini, and Wintermute.

- Professional Arbitrage Bots (SAT) Dominate Aggressive Trading: 522 HFT bots contributed 6.7% of the trading volume. The top 4 bots captured 89% of this category's share, with the majority of their funding sources traceable back to the Bybit exchange.

- Retail User Base Heavy Overlap with Polymarket: Among the top 400 retail wallets by trading volume, 22% of the volume ($16.3 billion) came from identifiable Polymarket users, indicating that prediction market users are the core driver of trading activity.

- Algorithmic Trading Adds Genuine Liquidity: Algorithmic products like Tread.fi place maker orders to farm points, providing top-of-book depth during periods when traditional market makers are absent (e.g., overnight, weekends). Structurally, this differs from Sybil wash trading.

Original Title: "Who is actually trading on Trade.xyz?"

Original Author: @web3_pastel, Arrakis Finance

Compiled by: Jaleel, BlockBeats

Editor's Note:

On the Hyperliquid landscape, one of the most unavoidable names in 2026 is Trade.xyz. It was the first truly successful product to emerge after the launch of HIP-3, the "permissionless perpetual market deployment framework." It moved assets like US stocks, crude oil, and silver – traditionally confined to conventional financial market hours – onto a 7×24 on-chain order book.

In just a few months, it evolved from a niche experiment with only the XYZ100 index into an on-chain trading venue hosting multiple markets including Oil, Tesla, and Silver, with monthly trading volumes exceeding $50 billion.

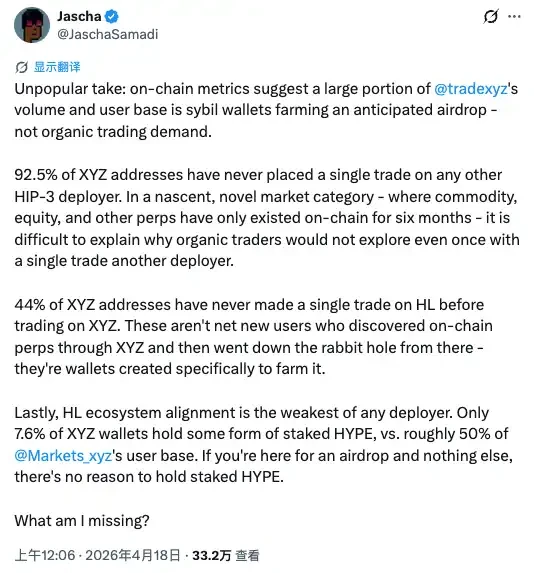

However, at the same time, controversy surrounding it has sparked considerable discussion overseas: of those impressive wallet numbers, how many are real users, and how many are Sybils created in bulk, chasing a yet-to-be-issued token?

Arrakis' research yields a rather interesting result: a Sybil layer does exist, with over 30,000 wallets traceable to a single Polymarket account, "Themino"; but it inflates user count, not dollar volume. The real trading volume is driven by a few professional market-making desks, a group of taker bots originating from Bybit, and a long tail of retail investors heavily overlapping with Polymarket.

The full text is as follows:

Summary

When we wrote our first piece, "Who Trades on HIP-3?", our attribution method was statistical. We classified wallets based on their trading behavior over the previous three months: addresses mainly placing limit orders were categorized as market makers, high-frequency takers as arbitrageurs, and orders with low fill rates and builder tags as retail. While this revealed some interesting market structure characteristics, the classification was probabilistic, and approximately 70% of wallets remained unclassified.

This article replaces statistical inference with mechanical classification. Every order on @HyperliquidX carries a set of deterministic tags signed and published by the exchange itself: time-in-force (ALO, GTC, IOC, FrontendMarket), builder code, fill flag, and position duration. We use this order metadata to classify each wallet into one of four categories: Retail, Market Maker, Arbitrage Bot, and Airdrop Hunter.

The second step is identifying the entities behind these wallets, extracting identity and trading behavior data from @arkham and HyperTracker's APIs. The top 450 wallets accounted for 78% of total trading volume. Within this group, we identified several @Polymarket associated accounts, @jump_, @SeliniCapital, @wintermute_t, Abraxas Capital, and others.

Through this two-step classification method, we observed several patterns, which are detailed below.

Trade.xyz Wallet Analysis

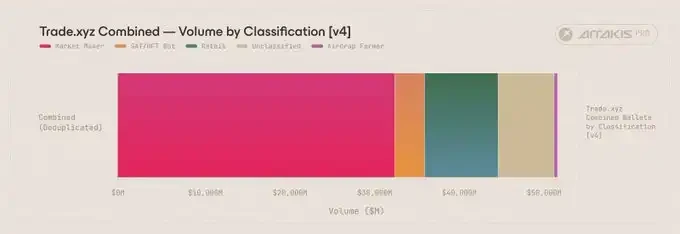

Our observation window was from March 10, 2026, to March 31, 2026, a total of 21 days. During this period, the four markets on @tradexyz (xyz:CL Crude Oil, xyz:SILVER Silver, xyz:TSLA Tesla, xyz:XYZ100) recorded a total of 79,622 unique participating wallets, with a total trading volume of $51.95 billion.

79,622 participating wallets broken down by trading volume. Although market makers account for less than 0.5% of total wallets, they are responsible for 63 cents of every dollar traded.

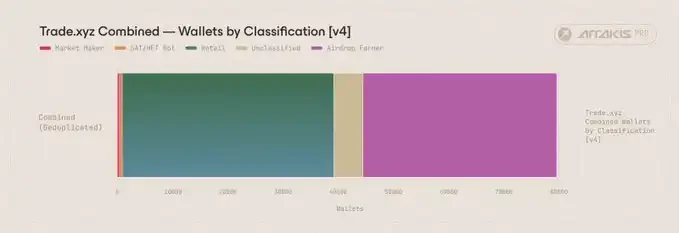

Classified by wallet count (not trading volume). The airdrop hunter category alone comprises 35,091 wallets, almost half of the identified wallets.

The airdrop hunter category is one of the largest by wallet count but the smallest by trading volume share. 35,091 wallets represent 44.07% of the total wallet count, yet they generated only $400 million in trading volume over the entire window, which is a mere 0.77% of the venue's total $51.95 billion. Nearly half of the active wallets on Trade.xyz contributed less than 1% of the total volume.

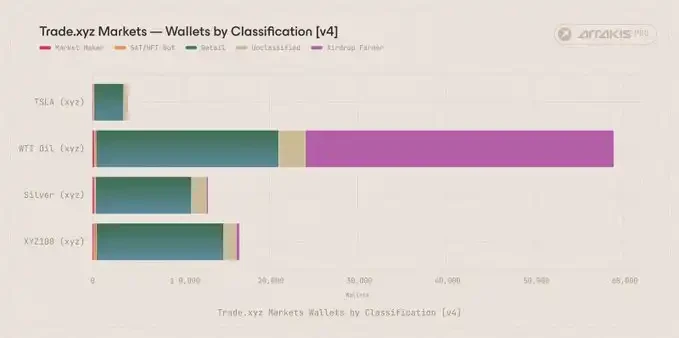

Breaking down by market reveals another distinct pattern.

Wallet distribution across markets. xyz:CL absorbed 99.3% of airdrop hunters, likely due to its optimal execution costs.

Out of the 35,091 airdrop hunter wallets, 34,859 (99.3%) traded xyz:CL during this window, with the remaining 232 spread across xyz:SILVER, xyz:TSLA, and xyz:XYZ100. This pattern is consistent with airdrop hunter behavior: each wallet repeatedly executes small two-way transactions to generate volume without taking price risk. This strategy relies on tight execution costs and is extremely sensitive to slippage. xyz:CL, being the deepest market among Trade.xyz's four, naturally became the preferred venue for this activity.

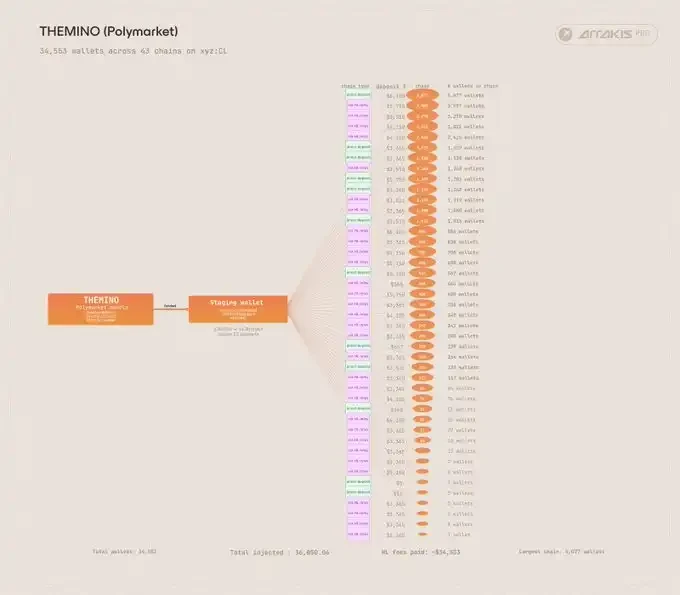

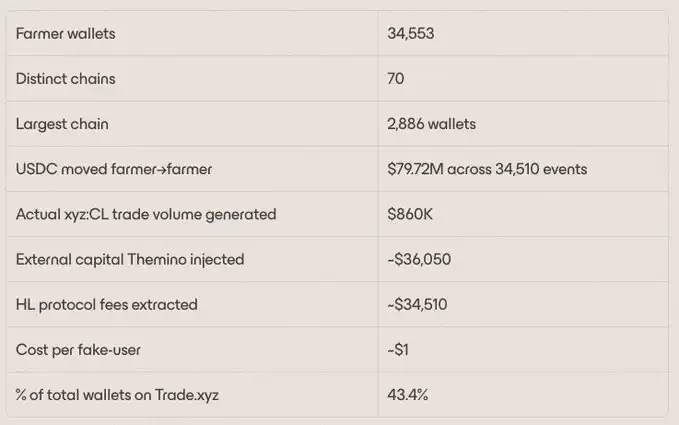

Another noteworthy phenomenon is who operates behind these addresses. The on-chain tracing presented below shows that 34,553 airdrop hunter wallets are linked to the same Polymarket operator. This single entity accounted for 43.4% of all participating wallets on Trade.xyz during this window.

At the other end of the classification is market making. 363 wallets, representing 0.46% of active addresses, drove $32.75 billion in trading volume within the window – 63 cents of every dollar traded on Trade.xyz. The other three categories fall in between. 522 SAT/HFT bots contributed $3.5 billion (6.7%). 38,307 wallets classified as retail contributed $8.7 billion (16.7%). 5,339 unclassified wallets contributed $6.61 billion (12.7%).

The 12.7% volume in the unclassified category cannot be qualitatively assigned to a specific strategy based solely on metadata. A reasonable assumption is that a significant portion comes from retail users placing limit orders via the Hyperliquid frontend, or retail users placing market and limit orders via the Trade.xyz frontend. Neither channel attaches explicit builder codes or specific TIF tags to orders, rendering these fills invisible under metadata-driven classification.

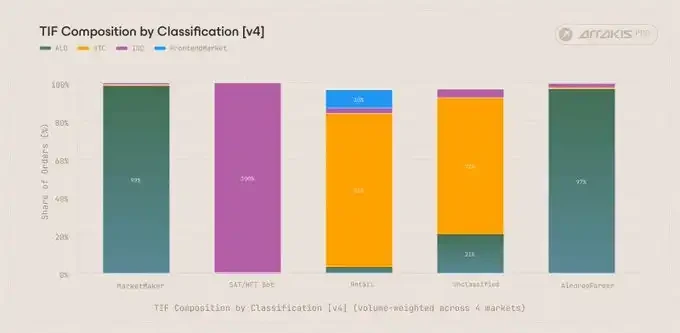

Time-in-force distribution weighted by order count for each category. Unsurprisingly, 98.5% of market maker orders are ALO, arbitrage bots use 100% IOC orders. The unclassified category has 71.5% GTC, a hallmark of manual limit orders placed by frontend users.

The TIF composition supports this speculation: 71.5% of orders in the unclassified category carry a GTC (Good Till Cancel) time-in-force tag, typically used by frontend users placing resting limit orders.

"Themino" Uncovers Over 30,000 Wallets

Over the past few weeks, there has been considerable debate: is Trade.xyz's impressive user count driven by genuine human participation, or inflated by airdrop hunter activity ahead of the anticipated TGE? We do not intend to comment on the broader landscape of airdrop farming on the exchange. However, during our analysis of trade-level data for the four Trade.xyz markets in March, a pattern emerged that is worth presenting.

Analyst Jascha points out that 92.5% of XYZ addresses have never executed a single trade on any other HIP-3 deployer.

Of the 34,602 wallets classified as airdrop hunters, 34,553, or 99.9%, can be traced back to a single Polymarket identity named "Themino".

"Themino," a Polymarket identity based on Arbitrum, spawned 70 independent linear chains covering 34,553 wallets.

How exactly does it work? Hyperliquid's L1 provides a primitive called internalTransfer, allowing USDC transfers between wallets with a flat fee of $1 per transfer regardless of amount. The operator behind Themino used this primitive to pass a seed deposit sequentially through tens of thousands of fresh wallets. Each wallet executes the same five-step sequence in approximately 26 seconds:

1. Receives $X from the previous airdrop hunter wallet via internalTransfer, losing $1 to the HL transfer fee.

2. Transfers $14 to the xyz sub-account.

3. Executes two IOC orders on xyz:CL, one buy and one sell, generating two fills and some trading volume.

4. Transfers approximately $13.99 back to the main account (the $0.01 difference covers execution slippage and trading fees).

5. Transfers $X minus $1 to the next airdrop hunter wallet via internalTransfer.

The next wallet repeats the same sequence.

These 34,510 internal transfers cost Themino a total of $34,510 in protocol fees, a strategy consistent with his trading history on Polymarket.

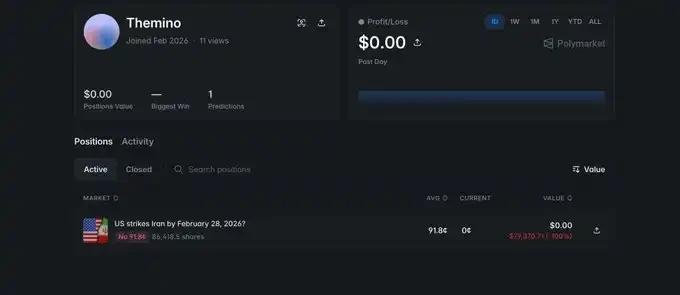

Themino also bet "No" on Polymarket for "Will the US strike Iran before February 28, 2026?", losing approximately $80,000. The strike occurred on February 28.

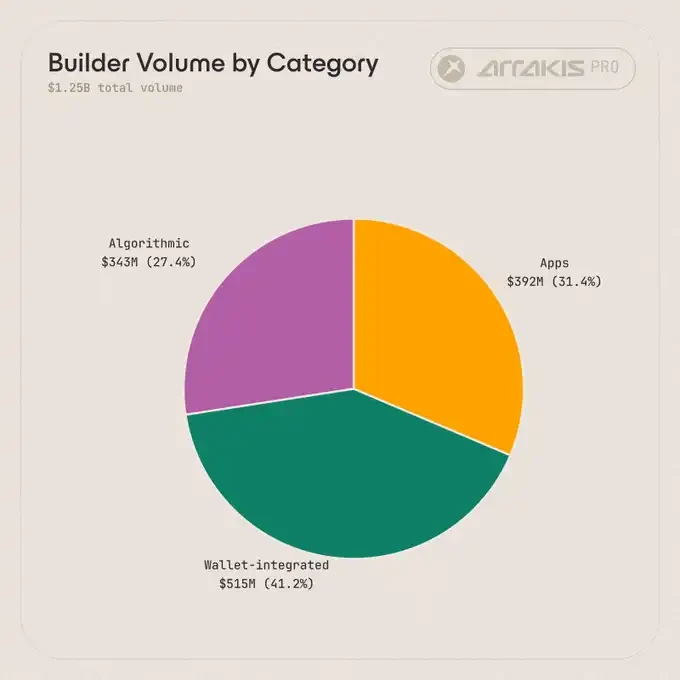

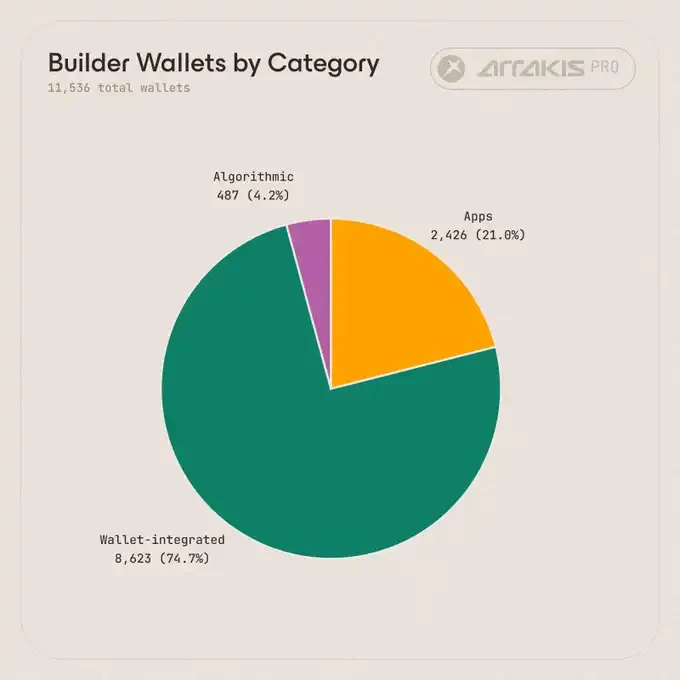

What Types of Builders Are There?

Hyperliquid attaches an identifier to orders routed through third-party frontends, allowing these applications to charge custom frontend fees. This identifier is the builder code, and it's the most direct way to determine which interface a wallet used, if any. Among wallets that traded on the four markets, these builders can be broadly categorized into three types.

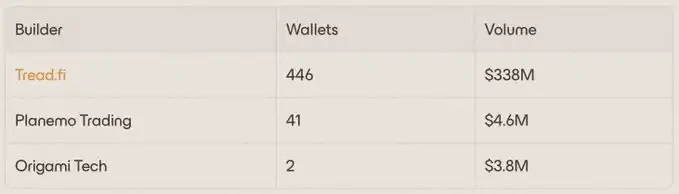

Algorithmic Builders. These are products used by retail users to maximize trading volume on DEXs, aiming to farm potential airdrops. Before late 2025, farming on a perpetual DEX meant either wash trading or algorithmically executing non-directional taker-to-taker strategies, which was costly for participants and net-negative for the exchange. Retail market-making bots like @tread_fi, @PlanemoTrading, and @origamitech_ replaced wash trading with genuine value-adding market making. Every order placed by these products is post-only, meaning wallets are adding liquidity to the order book, not consuming it.

As stated by @davidyjeong, CEO of @tread_fi: "Before retail market-making solutions, farming on perpetual DEXs meant wash trading – inflating volume at the cost of execution fees, slippage, and the risk of account bans. We solved this with a novel farming approach: the bot places maker orders on both sides only. Users farm at a lower cost, often making money from captured spreads, and the byproduct is genuine top-of-book liquidity for the market – exactly what HIP-3 equity perpetuals need during nights and weekends when traditional market makers are absent. It's a better way to farm, and a key reason for the excellent execution experience on HIP-3 markets today."

The contribution of these market-making bots is most evident during periods when traditional market makers are absent. CME WTI futures close on Friday afternoon and don't open until Sunday evening; equity perpetuals face a similar "night and weekend" gap. During these periods, retail market-making bots support the top of the book on markets like xyz:CL and xyz:TSLA.

It's important to note: in this analysis, we classified wallets routed through these algorithmic products as airdrop hunters. However, their trading behavior and market impact are structurally entirely different from Sybil activity.

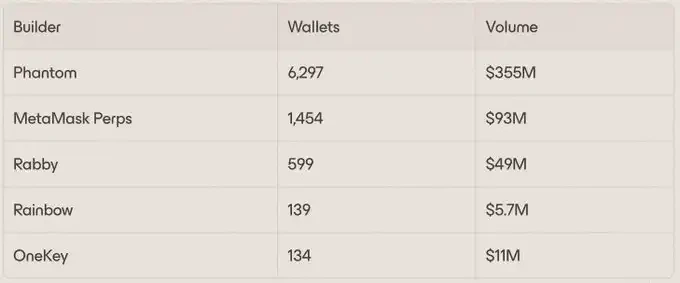

Wallet-Embedded Builders are perpetual interfaces embedded within consumer wallets. Since early 2026, this type of integration has become one of the largest sources of retail order flow on HIP-3. This group includes @phantom, @MetaMask, @Rabby_io, @rainbowdotme, and @OneKeyHQ. Their median trading volume per wallet ranges from $1,000 to $3,000, consistent with the order size of a retail segment prioritizing ease of use over marginal builder fees.

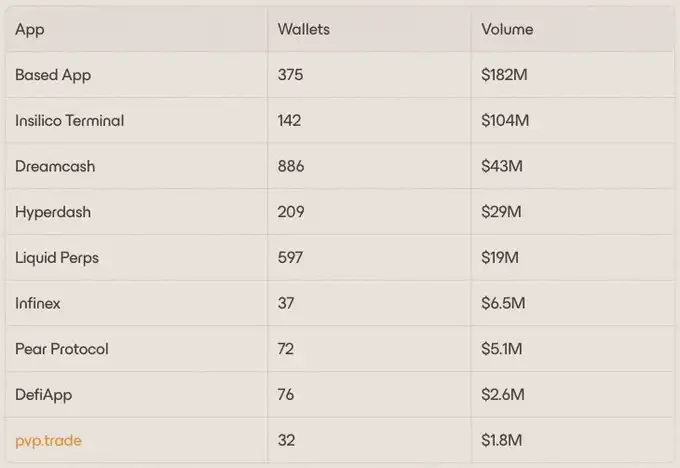

Application Builders are standalone perpetual frontends and integrated products: products designed for traders with specialized workflows, serving users who find wallet plugins insufficient and require better order placement, charting, position management, and execution tools. This group has fewer wallets than the wallet-embedded group but higher volume per wallet, aligning with advanced users who prioritize functional depth over plug-and-play ease. This category includes products like the @InsilicoTrading terminal, @liquidtrading, @hypurrdash, @BasedOneX, @Dreamcash, @infinex, @pear_protocol, @defiapp, and @pvp_dot_trade.

@0xVKTR, Head of Growth at @InsilicoTrading (the team behind the Insilico terminal), describes it this way: "At Insilico, we view HIP-3 markets as the next step in making real-world exposure native to crypto rails. Traders don't just want another frontend. They want fast execution, clean market access, and the ability to move seamlessly between crypto and macro assets without leaving their existing workflow. Trade.xyz is one of the clearest examples of this demand. The order flow routed through Insilico proves that when a venue has depth, the product is useful, and the trading experience is built for serious participants, there is a real base of advanced users for on-chain perpetuals."

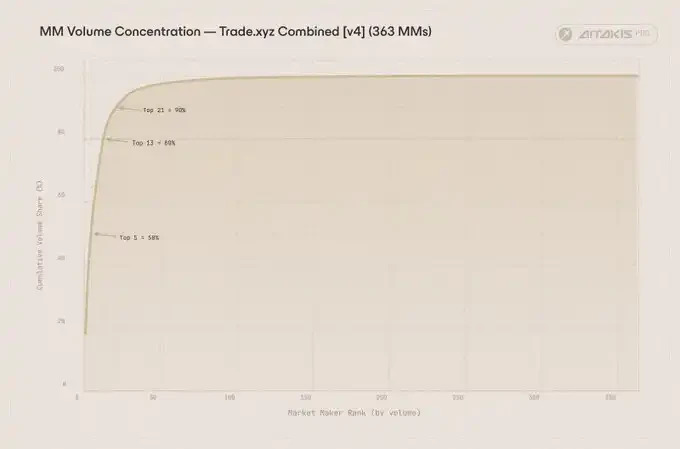

Who Are Trade.xyz's Largest Market Makers?

The market-making landscape across Trade.xyz markets is highly concentrated. The top 5 market makers account for 50% of the market-making volume, the top 13 for 80%, and the top 21 for 90%. A handful of market-making desks support the vast majority of the exchange's market-making book.

Cumulative share of market-making volume ranked by wallet. The top 5 desks command 50% of all market-making flow, the top 13 reach 80%, and the top 21 reach 90%.

The second-largest market maker is the most interesting