**Translation Result:** Unraveling the Legal Details of the Manus Case: The Era of Offshore Arbitrage Has Permanently Ended

- Core Thesis: In April 2026, Chinese regulatory authorities, citing national security concerns, intervened for the first time to block a foreign acquisition in the AI sector, prohibiting Meta from acquiring Manus, which had already been legally incorporated overseas. This marks the complete invalidation of the gray path of using "offshore structures" to circumvent regulation. AI entrepreneurs must now choose between "complete divestiture of U.S. capital" and "domestic capital aligning with the national team."

- Key Elements:

- Applying the principle of "substance over form," regulators identified Manus as a "Chinese entity" based on four dimensions: team, computing power, algorithms, and data. Even though the company had completed a redomiciliation to Singapore and had a Cayman Islands structure, its technological origins remained under Chinese jurisdiction.

- Manus's transfer of its core assets overseas was characterized as a systematic "circumvention of export controls." Its core code and training data were deemed a "technology export" subject to the Catalogue of Technologies Prohibited or Restricted from Export and the Data Security Law.

- The transaction parties failed to fulfill the mandatory pre-filing obligation required by the Foreign Investment Security Review Measures. This constituted an independent and unforgivable procedural violation, serving as the key procedural basis for the regulator's final action.

- The fact that the National Development and Reform Commission (NDRC), rather than the Ministry of Commerce, delivered the final ruling signifies that this matter was characterized as a "sovereign security" issue, not a mere "technology import/export" dispute. The intent was to establish a systemic deterrent, clearly defining the red line as the ultimate criterion of "national security."

- The four red lines used to identify "fake foreign capital, truly Chinese" entities are: founders holding Chinese passports; having received funding from state-owned capital (e.g., government guidance funds); the first line of code being written within China; and the use of Chinese data (a "data gene" that cannot be cleansed ex post facto).

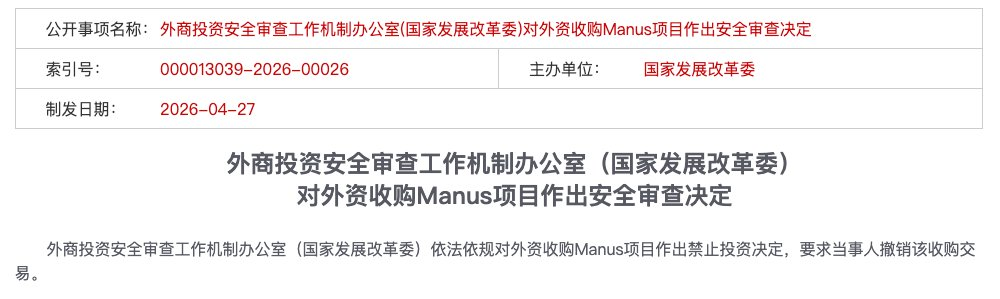

On April 27, 2026, the Office of the Working Mechanism for Foreign Investment Security Review (National Development and Reform Commission) made a decision to prohibit the foreign acquisition of the Manus project in accordance with laws and regulations, requiring the parties to cancel the acquisition transaction.

In just a few dozen words, this directly halted a deal valued at over $2 billion. Years of product development, legal framework structuring, and financing and exit planning by Manus all came crashing down in an instant.

This marks the first publicly halted foreign acquisition case in the AI sector since the "Foreign Investment Security Review Measures" came into effect in January 2021.

This transaction had a unique characteristic: both parties involved had already legally established themselves as foreign entities. Meta is a US company, while Manus had completed its redomiciliation to Singapore and established a holding structure in the Cayman Islands. Yet, Chinese regulators ultimately decided to prohibit the investment.

The ripple effects of this case are now becoming apparent, with AI companies like Moonshot AI, ByteDance, and StepFun facing clearer compliance guidance.

Behind this lies a deeper issue: the traditional offshore structure playbook is becoming completely ineffective. Entrepreneurs need to figure out their compliance path from Day 0.

This article focuses on substance, not stories – what specific laws and regulations govern this decision, where the red line for "showering-style" overseas expansion is drawn, and how companies should choose their path going forward.

1. What Specific Laws and Regulations Are Being Followed?

Looking back at the Manus case, initial industry discussions mostly focused on "what happened" – the move, the separation, the ban. However, as case details gradually emerged, the legal community's focus returned to a more fundamental question: On what basis could regulators call off this transaction? What specific laws and regulations were being invoked?

The answer doesn't lie in a single law, but in a three-tiered regulatory logic. These three tiers work together to form an inescapable review framework.

Layer 1: Determining the "Chinese Entity" – The Foundational Basis for Look-Through Review

This is the legal starting point of the entire case: Which country's company is Manus?

From a legal form perspective, the answer seems clear – Manus had completed its redomiciliation to Singapore, with its holding structure in the Cayman Islands. The parent company, Butterfly Effect Pte, is a bona fide Singapore entity. This was also the core legal argument of the Manus team throughout the transaction:

"Our entity structure has been converted to an offshore structure."

But the regulator's response was:

Form doesn't count; substance does.

AllBright Law Offices systematically analyzed from a legal perspective why a "legal shell offshore-ization" failed in the Manus case. The root cause lies in the fact that the core AI assets had an unbreakable substantive connection with China's domestic jurisdiction across four dimensions:

- Talent Dimension: The engineering team mastering the core underlying logic had long accumulated R&D experience domestically; their technical capabilities were trained and developed within China.

- Computing Power Dimension: Domestic R&D created path dependency for technical interfaces and computing power scheduling, embedding a "Made in China" label into the core system's architecture.

- Algorithm Dimension: The R&D and training of core model weights were completed domestically, representing the most legally significant "technological source."

- Data Dimension: The training data accumulated through Reinforcement Learning from Human Feedback (RLHF) based on massive user interactions originated highly concentrated within China.

These four dimensions point to the same conclusion: Manus's legal form may be Singaporean, but the "technological substance" of Manus as a company – its source, core, and foundation – all originate within China. According to the principle of "substance over form," from the regulator's perspective, such substantive connections are sufficient to form the basis for a look-through review – this is the cornerstone for all subsequent legal actions.

Therefore, although Xiao Hong founded Butterfly Effect Technology in Beijing in 2022, set up the "Cayman-Hong Kong-Beijing" red-chip structure in 2023, and redomiciled to Singapore in 2025 while completing team separation and business isolation, the legal determination does not look at "when they moved out," but rather "where they came from." Technological assets originating within China do not change their nationality simply because of a change in registration certificate.

Layer 2: Export Restrictions and Regulatory Evasion – The Legal Characterization of "Showering-Style" Overseas Expansion

Once the first layer is established – that Manus is substantively considered a "domestic enterprise" – the legal logic of the second layer follows directly: transferring your core assets abroad is, in itself, an act of export. Export activities are subject to export control regulations.

From the regulator's perspective, Manus's three-step actions formed a complete puzzle for "evading export controls":

Step one, entity transfer. Moving the company entity from China to Singapore, establishing the offshore entity Butterfly Effect Pte, and setting up the Cayman Islands holding structure. Legally, this was the first step in "de-Sinicization."

Step two, team and asset migration. Quickly laying off nearly two-thirds of its China-based employees (80 out of 120), retaining over 40 core technical personnel to relocate to Singapore.

Step three, data and business separation. Clearing domestic social media accounts, blocking access from China IPs, and terminating partnerships with local entities like Alibaba's Tongyi Qianwen.

Legally, the technical knowledge, R&D capabilities, and algorithmic experience carried abroad by core technical personnel could themselves constitute "technology exports" potentially covered by the "Catalogue of Technologies Prohibited or Restricted from Export." Simultaneously, according to the "Data Security Law" and the "Data Cross-Border Transfer Security Assessment Measures," the training data accumulated from extensive user interactions before the separation originated highly concentrated within China – the data genetics were already written into the model, and the separation action cannot retrospectively delete them.

Therefore, the regulator's look-through logic can be summarized in a cold, hard statement:

Code written on China's soil, data grown from China's users – this is a "Chinese asset." Transferring it is an export, and exports must be controlled.

The essence of "showering-style" overseas expansion is using formal compliance to mask substantive violations – a systemic evasion of the export control regime.

Layer 3: The Voluntary Declaration Mechanism – You Can't Say "I Didn't Know"

If the first two layers represent "substantive violations," the third layer represents "procedural violations" – and it's often the easiest to establish guilt.

Article 4 of the "Foreign Investment Security Review Measures" clearly stipulates that for foreign investments involving important information technology, key technologies, and other related fields, the parties involved shall "voluntarily declare to the Office of the Working Mechanism before implementing the investment." This is a mandatory pre-investment declaration obligation, not a "recommended declaration," nor a "remedial declaration after problems arise."

Throughout the entire transaction process, including up to the point of closing, neither Manus nor Meta made any form of voluntary declaration to Chinese regulators. During the months-long closing period, Manus and its investors seemed to reach a dangerous tacit understanding: as long as the regulator didn't knock on the door, they wouldn't voluntarily open the window.

In legal practice, "failure to declare when required" is itself an independent and serious violation. It sends the signal: either knowing wrongdoing or deliberate evasion. In either case, the regulator cannot simply let it go.

A compliance lawyer summarized after the case:

"The biggest compliance flaw exposed by the Manus case is not the controversial applicability of a specific regulation, but the company's complete abandonment of its declaration obligation to Chinese regulators. In the legal system, evading the process itself is less tolerable to regulators than substantive violations."

Looking back, Manus's fate was sealed from the first layer: once the look-through review determined it was a "substantive Chinese entity," the export control logic of the second layer and the declaration obligation of the third layer were automatically unlocked. These three layers of legal reasoning are progressive and interlocking, forming a logical closed loop. Within this loop, there is no room for "luck."

2. Why Was It the NDRC?

The Ministry of Commerce (MOFCOM) acted first. On January 8, 2026, a MOFCOM spokesperson publicly stated that it would "conduct an assessment and investigation into the consistency of this acquisition with relevant laws and regulations on export controls, technology import/export, and outbound investment." However, on April 27, it was the National Development and Reform Commission (NDRC) that delivered the final blow.

There's a story behind this departmental shift. Some experts believe that MOFCOM bases its actions on the "Catalogue of Technologies Prohibited or Restricted from Export," which provides very specific descriptions of controlled technologies: artificial intelligence interface technologies specifically designed for Chinese and minority languages. However, after Manus's "shower," all its services were switched entirely to English, and Chinese users were locked out. This means that if the case were pursued purely under export control regulations, some controversy over applicability could arise.

This represents the space for debate regarding regulatory applicability. However, we lean towards a deeper implication, as the applicability of laws often ranks below political considerations.

The NDRC oversees "security reviews," while MOFCOM oversees "technology import and export." The NDRC's involvement suggests this matter has shifted from a "business deal" to a matter of "sovereignty."

In other words, the intervention of the NDRC, a macro-management department with broader economic authority than MOFCOM, itself sends a clear signal – this is not an isolated enforcement action against a single company, but a systemic deterrent aimed at "fighting one to ward off a hundred."

Killing one is meant to warn a hundred.

All practitioners still on the sidelines now see clearly where the red line is drawn – not in the vague area of a specific clause, but on the indisputable ultimate scale of safeguarding national security.

3. Four High-Risk Trigger Points

Based on the Manus case and the "look-through review" principle established by the "Foreign Investment Security Review Measures," the following four red lines are now clear. Hitting any one of them means the "showering-style" overseas expansion path is off the table.

Red Line 1: Founder Holds a Chinese Passport and Has Not Renounced Chinese Nationality

Manus founder Xiao Hong holds Chinese nationality. China's Export Control Law has jurisdiction over natural persons. This means the founder himself may also become a target of regulatory scrutiny, and related arrangements cannot be understood solely at the company level.

An even harsher reality exists across the Pacific: Within North American VC circles, the financing environment for Chinese founders is also tightening due to geopolitical risk assessments. Top Silicon Valley VCs like a16z have significantly decreased their willingness to invest in founders holding Chinese passports under geopolitical pressure.

Manus's Series B round was led by Benchmark, but afterwards, Benchmark faced strong political backlash in the US for this investment, with several Republican senators claiming the deal was "aiding the Chinese government."

An investor from Silicon Valley's Founders Fund was blunt:

The founder is Chinese, the company is in Beijing, and the core technology is a general-purpose AI Agent – that is an "original sin."

Doors are closing on both sides. If you have a Chinese passport, US capital is uneasy. If you have Chinese technology, Chinese regulators won't let go. This gap is narrower than most people imagine.

Red Line 2: Has Taken Money from State Capital

It's not just "direct investment from sovereign wealth funds" that counts as state capital. Guiding funds from various levels of government, state-owned components within RMB fund Limited Partners (LPs), and policy bank loans – all these fall within the scope of "state capital infusion." Also, those "trivial amounts" of office space, computing power, and talent subsidies you complained about as being tedious to apply for and too small – those will all be carefully noted when the reckoning comes.

Red Line 3: The First Line of Code Was Written Within China

The initial location where core code was written, the location where algorithm model training was completed, the storage location of technical documentation – these seemingly "purely technical" facts constitute legal proof of the "technological source." Manus's early development was completed within China. When the team relocated to Singapore, the code they carried itself constituted a technology export. Manus never filed any declaration for this transfer as a technology export.

Red Line 4: Has Used Chinese Data

This is the most common illusion among many AI entrepreneurs: thinking that as long as later they purge domestic users and block China IPs, their company becomes "clean."

But in the eyes of regulators, 'technological substance' considers not just code, but also data genetics.

The "Data Security Law" and the "Data Cross-Border Transfer Security Assessment Measures" have clear review requirements for cross-border transfers involving "important data." Although Manus closed its Chinese-language services and blocked China IPs, the user interaction data accumulated in its early stages had already completed core model training – the data genetics are etched into the model's weights, and cannot be retroactively deleted through "later cleansing." Data grows from China's users, so the model carries a "Made in China" label.

4. Entrepreneurs in Specific Industries: Choose Your Side, Starting Now

The "Security Review Measures" establish a security review mechanism for foreign investments that may affect national security, focusing on areas such as military and national defense, as well as important areas where foreign investors gain actual control, including important information technology, key technologies, major infrastructure, and important resources.

In the current regulatory environment following the Manus case, the following points deserve special attention:

First, in practice, the determination of "actual control" does not solely depend on shareholding ratio. If a foreign investor can exert significant influence over a company's business decisions, personnel, finance, or technology (e.g., possessing veto power or right to know key technologies), it falls under this category. This definition is quite broad. For example: even if you only hold a 5% equity stake corresponding to a USD fund, a veto right attached to that 5% stake could be deemed as "exerting significant influence over the company's business decisions," thus constituting "actual control" and triggering a review.

Second, the NDRC, as the lead department of the working mechanism, has the authority to issue compliance guidance based on national security judgments. For example, on April 24, 2026, the NDRC instructed some AI companies to reject US capital. While not explicitly listed in the articles, this falls under the extended scope of "daily security review work and preventive management" authorized by Articles 3 and 7 of the "Security Review Measures."

Third, it is not recommended to use structures like VIE, nominee holdings, or trusts to evade review. In practice, if a company is found to have arrangements aimed at evading review, it may face risks of corrective actions, suspension, withdrawal, or other compliance-related measures.

Conclusion: The old "fence-sitting" gray area has been effectively sealed off from all sides. From now on, companies must establish a clear compliance position from Day 0.

Especially in the AI track, you can only choose one of the following two paths.

Path A: The US Capital Route – Complete Divestiture

If you decide to pursue USD funds, follow the Silicon Valley path, and ultimately aim for an acquisition or a US stock market listing, what you need is not a "shower" but a complete blood transfusion.

A hard criterion: You cannot cross any of the four red lines mentioned above.

This specifically means four things:

First, the founder must resolve their nationality. A Chinese passport itself is a compliance risk label in the eyes of US VCs. If you are determined to take this path, renouncing Chinese nationality is not an option; it is a prerequisite.

Second, do not take state capital. Any funds involving government guiding funds, state-owned LPs, or policy bank loans should undergo thorough compliance penetration at the initial financing stage and be divested or bought back if necessary.

Third, the source of code must be overseas. This is the harshest and most core requirement. The first line of code for your core algorithm must be written overseas. Domestic teams can only work on non-core modules or peripheral business. You need to establish a truly capable overseas technical center from the start – not a shell, but a substantive entity.

Fourth, data and users must be isolated from Day 1. Never touch Chinese user data from the beginning. It's not about "later cleansing," but "never having possessed it."

The prerequisite for taking this path: You can bear the cost of complete separation from the domestic market. Give up all revenue, users, and brand synergy from the Chinese market. You are betting that the global return will be sufficient to cover this cost. Moreover, even if you achieve all the above, you still face an increasingly unfriendly US – your identity as a Chinese founder remains an "original sin" in the eyes of some forces in Silicon Valley.