英特尔暴涨20%,CPU在Agent时代重回舞台中央

- 核心观点:英特尔2026财年Q1财报超预期(营收136亿美元,EPS超预期29倍),盘后股价涨20%,标志着其战略转型从AI叙事变为财务落地。核心逻辑是AI从训练转向推理和Agent阶段,CPU重新成为不可或缺的地基。

- 关键要素:

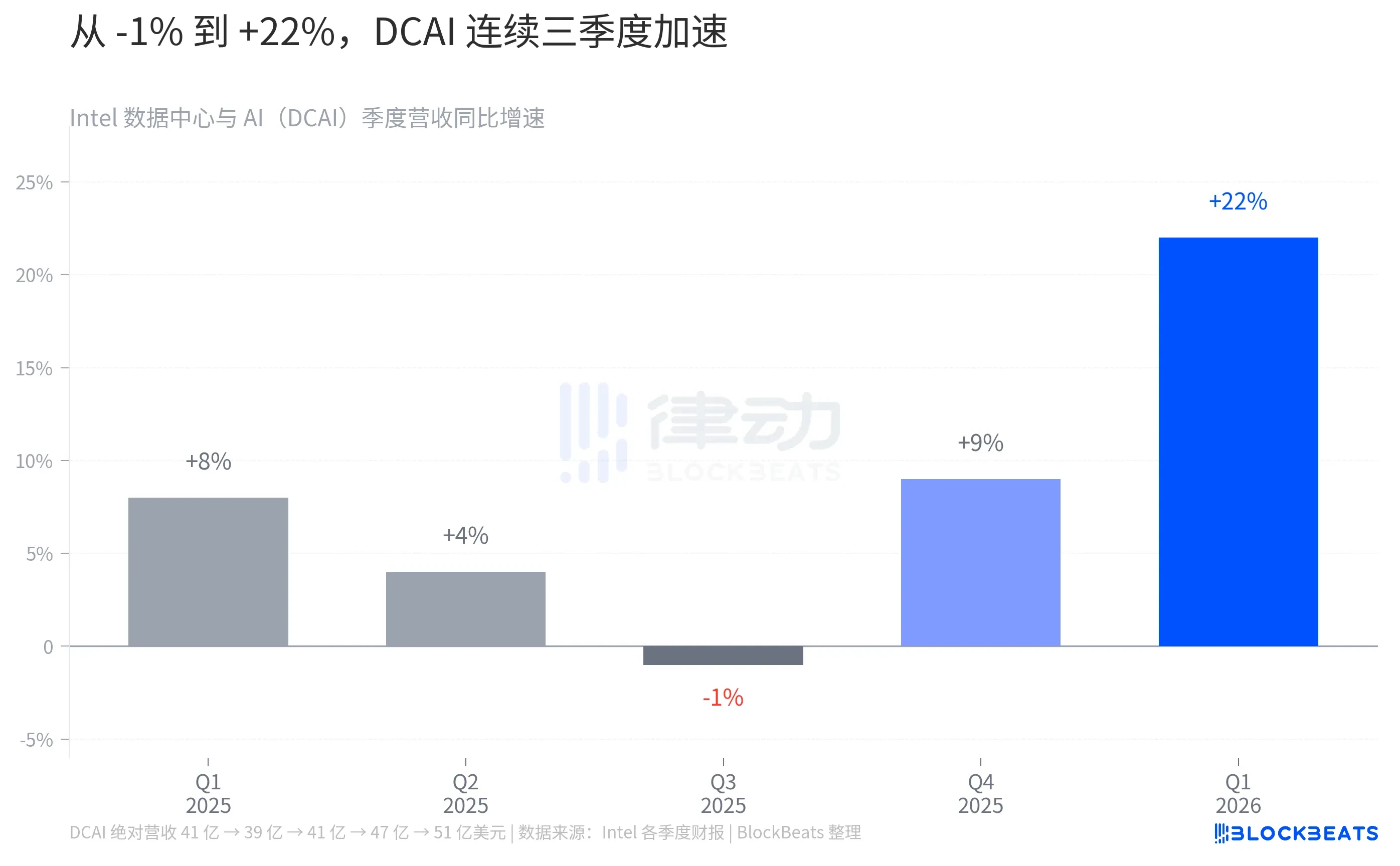

- 数据中心业务(DCAI)Q1收入51亿美元,同比增长22%,创历史新高,表明CPU在AI部署中的复苏已得到财务确认。

- AI从训练(CPU占瓶颈8%)到Agent编排(CPU占延迟50%-90%),市场需求结构变化提升了CPU在算力架构中的权重。

- 公司放弃对标英伟达的GPU项目“Falcon Shores”,转向CPU主场,是新CEO Lip-Bu Tan上任后战略调整的关键点。

- 2025年Q4 DCAI环比增长15%,为十年来最快,而此前2025年中市场曾怀疑CPU复苏仅是叙事,现U形反转已被确认。

- Deloitte预估到2026年推理工作负载将占AI总算力三分之二,Futurum Group预计服务器CPU市场规模到2030年将达600亿美元。

Last night, NVIDIA's stock price briefly touched $70 during regular trading and surged 20% in after-hours trading, as its latest earnings report exceeded all expectations.

Intel disclosed its fiscal first-quarter 2026 results on Thursday, reporting revenue of $13.6 billion, up 7% year-over-year and 11% above the Wall Street consensus estimate. Non-GAAP earnings per share stood at $0.29, compared to the analyst estimate of $0.01, exceeding expectations by 29 times—an extremely rare discrepancy for a large-cap stock. Following the news, Intel's stock price rose as much as 20% in after-hours trading.

The Q2 guidance also pointed in a more aggressive direction, with a revenue range of $13.8 billion to $14.8 billion, above the consensus median. In the earnings call, new CEO Lip-Bu Tan summarized the performance in one sentence, essentially stating that the CPU is re-embedding itself as an indispensable foundation in the AI era.

This is one of the most debated propositions about Intel over the past two years. The company was once considered to have completely missed the first wave of AI.

On one hand, it failed to produce a GPU that could rival NVIDIA's; on the other hand, its advanced manufacturing nodes lagged behind TSMC. However, over the past 12 months, as more AI deployments have shifted from model training to inference and autonomous "agent" orchestration, the CPU—once seen as a basic "computer brain"—has regained relevance. Intel's rebound this quarter marks the first financial realization of this technological narrative.

Data Center Business Stages a U-Shaped Reversal

Breaking down the $13.6 billion in Q1, the most critical change comes from the Data Center and AI (DCAI) segment. According to Intel's earnings report, DCAI generated single-quarter revenue of $5.1 billion, up 22% year-over-year and hitting an all-time high.

This is not a one-time surge. Looking back to 2025, DCAI posted $4.1 billion in Q1, dipped to $3.9 billion in Q2, and returned to $4.1 billion in Q3. This mid-2025 stagnation once made the market doubt whether the so-called "CPU recovery" was just a narrative. Then in Q4, according to Intel's disclosures compiled by Tom's Hardware, DCAI jumped from $4.1 billion in Q3 to $4.7 billion, a sequential increase of 15%—the fastest quarterly growth rate for the company in a decade.

Entering Q1 2026, the $5.1 billion figure drew a clear U-shaped curve, with the trough in mid-2025, the inflection point in Q4 2025, and confirmation in Q1 2026. Management attributed this to the ramp-up in volume of the Xeon 6 "Granite Rapids" processor, combined with the AI infrastructure refresh cycle. The company even deliberately sacrificed some client CPU capacity, dedicating wafers to data center chips, thereby boosting the overall profitability of the DCAI segment. According to Intel's Q3 2025 earnings report, the operating profit margin for this segment rose from 9.2% in Q3 2024 to 23.4%, nearly a 2.5x increase.

One AI Narrative, Three Different Trajectories

Comparing Intel's rebound to its peers reveals a picture more interesting than just the percentage gains.

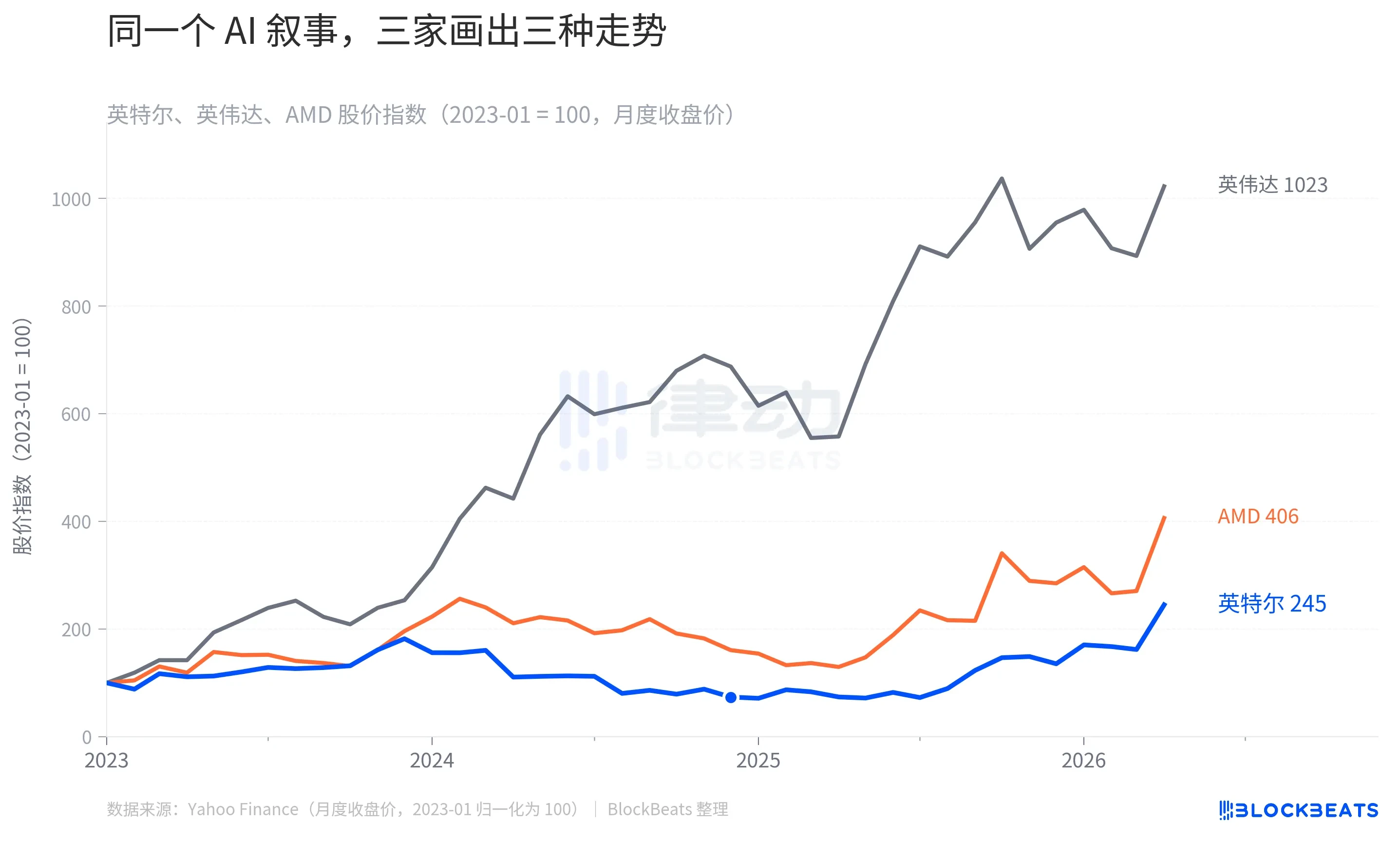

Using January 2023 as a baseline, by April 2026, NVIDIA's stock price index had surged to 1023, AMD's to 406, and Intel's to 245. All three started from the same point but ended with a nearly five-fold difference. However, what's more noteworthy is the shape of Intel's blue line. It didn't climb slowly; it first plunged to 64 in September 2024 (a 36% drop from the starting point), then executed a V-shaped rebound, only catching up to 245 in early 2026.

This chart essentially illustrates the market's two pricing rounds for "who truly profits in the AI capital cycle." From 2023 to 2024, money flowed to NVIDIA because training required GPUs. AMD carved out a second slice of the pie with its MI300 series, and its stock followed. Intel, however, was systematically removed from the AI trading list due to disappointing Gaudi accelerator sales and delays in advanced process mass production. According to third-party estimates cited by Fortune in January 2025, NVIDIA's share of the AI chip market rose from 25% in 2021 to 86% in 2024, while Intel's fell from 68% to 6%.

The second pricing round occurred from the second half of 2025 to early 2026, when the market began to re-debate a question: If AI moves from training to inference and agent phases, will the structure of computing power demand change? The answer to this question directly determines how far Intel's blue line can go.

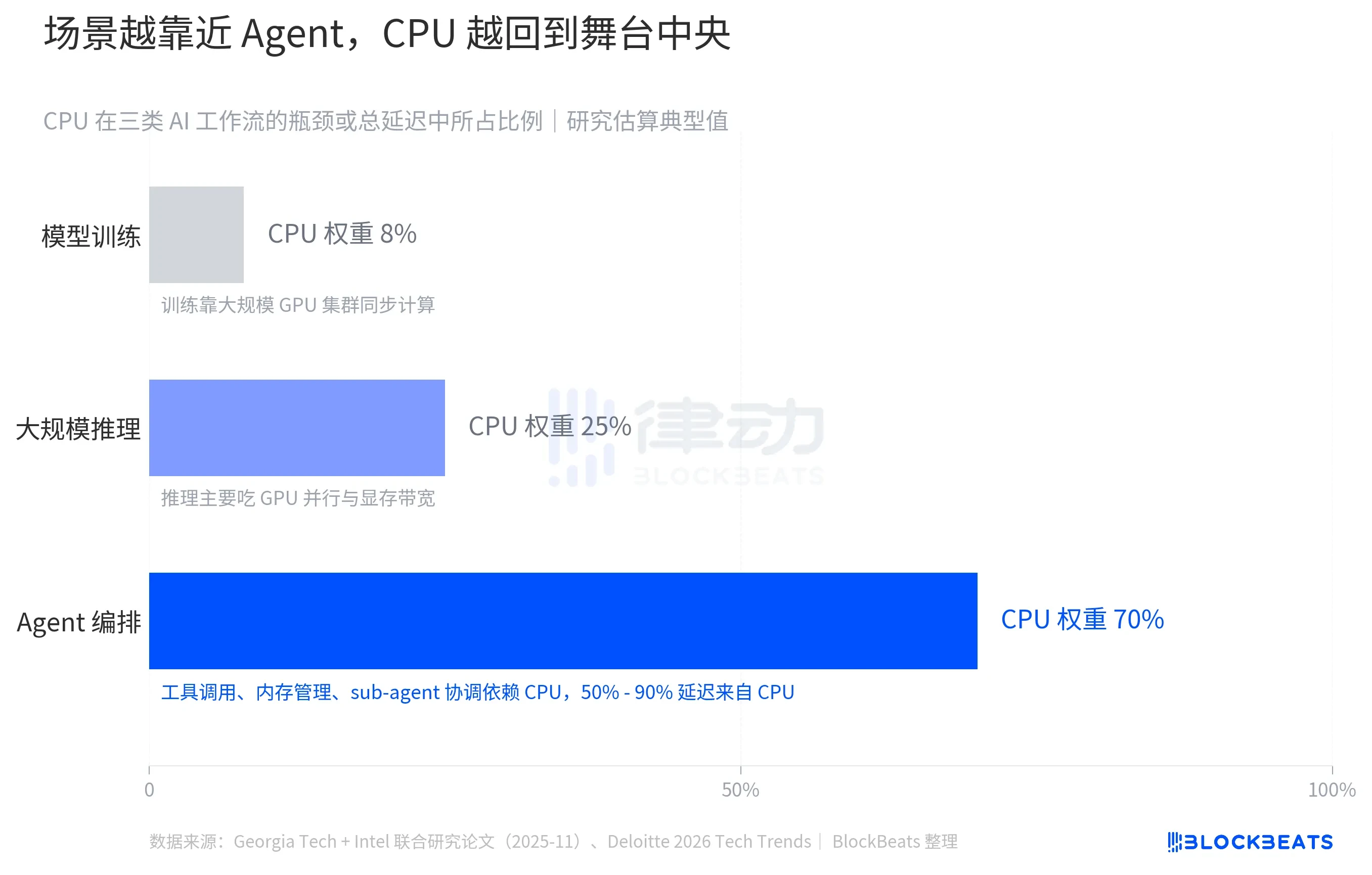

The Closer the Scenario Gets to Agents, the More the CPU Returns to Center Stage

Breaking down AI workflows into three scenarios, the CPU's weight varies significantly. According to Deloitte's 2026 Technology Trends report, during large model training, the CPU accounts for only about 8% of the workflow bottleneck, with the remaining 92% of computing pressure on GPU cluster parallel synchronization—NVIDIA's home turf. As we move into large-scale inference, the CPU's weight rises to 25%, but GPU parallel throughput and memory bandwidth remain bottlenecks.

The real change occurs in agent orchestration scenarios. According to a study jointly published by the Georgia Institute of Technology and Intel in November 2025, CPU processing for tool calls in agent workflows accounts for 50% to 90% of the total workflow latency, depending on the tool type and orchestration complexity. In other words, when an AI agent performs tasks like "calling APIs, pulling data, coordinating subtasks, and managing context memory," the bottleneck is not the GPU, but the CPU.

This trend has quantifiable benchmarks. According to Deloitte, inference workloads are estimated to account for about one-third of total AI computing power in 2023, about half in 2025, and are projected to reach two-thirds by 2026. According to Futurum Group, the server CPU market is expected to grow from $26 billion in 2025 to $60 billion by 2030, a growth rate exceeding the historical long-term average. A more specific signal comes from OpenAI's disclosed computing roadmap, which plans to secure "hundreds of thousands of the most advanced NVIDIA GPUs, along with computing power scalable to tens of millions of CPUs to support agent workloads." The GPU remains the leader, but the scale of the CPU has been publicly placed on the same line for the first time.

The Rebound Didn't Start in Q1 2026

Overlaying Intel's stock price over the past five years with six key events shows that the 20% after-hours surge in Q1 was actually the tail end of a series of earlier decisions.

In February 2021, Pat Gelsinger returned as CEO, unveiling the "IDM 2.0" strategy to position Intel as both a chip designer and an open wafer foundry. When Gaudi 3 was launched in April 2024, Intel set its 2024 AI accelerator sales target at $500 million.

On August 2, 2024, Q2 2024 earnings imploded, with revenue of $12.8 billion declining year-over-year, GAAP EPS of -$0.38. The company announced a 15% workforce reduction and suspended dividends, causing its stock to fall 26% in a single day—its worst daily performance since 1974. According to Intel's disclosures at the time, management subsequently acknowledged that Gaudi 3 would not reach the $500 million target for the full year and recorded a $300 million inventory write-down.

According to an official Intel announcement, Gelsinger departed on December 1, 2024, and the company entered an interim co-CEO phase. In February 2025, the new management decided to cancel the independent GPU project "Falcon Shores," which was aimed at competing with NVIDIA, acknowledging that its in-house AI accelerator roadmap could not overcome NVIDIA's ecosystem lock-in. On March 18, 2025, former Cadence CEO and semiconductor veteran Lip-Bu Tan officially became Intel's CEO. At that time, Intel's stock price was around $22, up just over 20% from the September 2024 low of $18.

From Lip-Bu Tan's appointment to this Q1 earnings report, Intel's stock price rose from $22 to $65 before the report, and the 20% after-hours gain puts it near $78. If the period from August 2024 to December 2024 was the company's darkest hour, then the true turning point for the rebound was not Q1 2026, but the moment when it canceled Falcon Shores and selected Tan as CEO. The company abandoned the fantasy of competing head-to-head with NVIDIA and returned to its true strength: the CPU home turf.

The 29x EPS beat is a financial signal, but it actually reflects two things happening simultaneously. The market is beginning to re-price the CPU's position in the AI architecture, and Intel has just completed a management transition and product line rationalization. Neither of these happened in Q1.