警报拉满:日本央行加息25bp在即,美股、加密重现2024式闪崩?

- 핵심 의견: 일본은행이 6월에 금리를 1.0%로 인상할 것으로 예상되며, 이는 엔화 조달 비용을 상승시키고 캐리 트레이드 청산을 촉발하여 전 세계 유동성을 긴축시킵니다. 이로 인해 고평가된 AI 기술주와 암호화폐는 상당한 조정 압력과 변동성 상승에 직면할 것입니다.

- 핵심 요소:

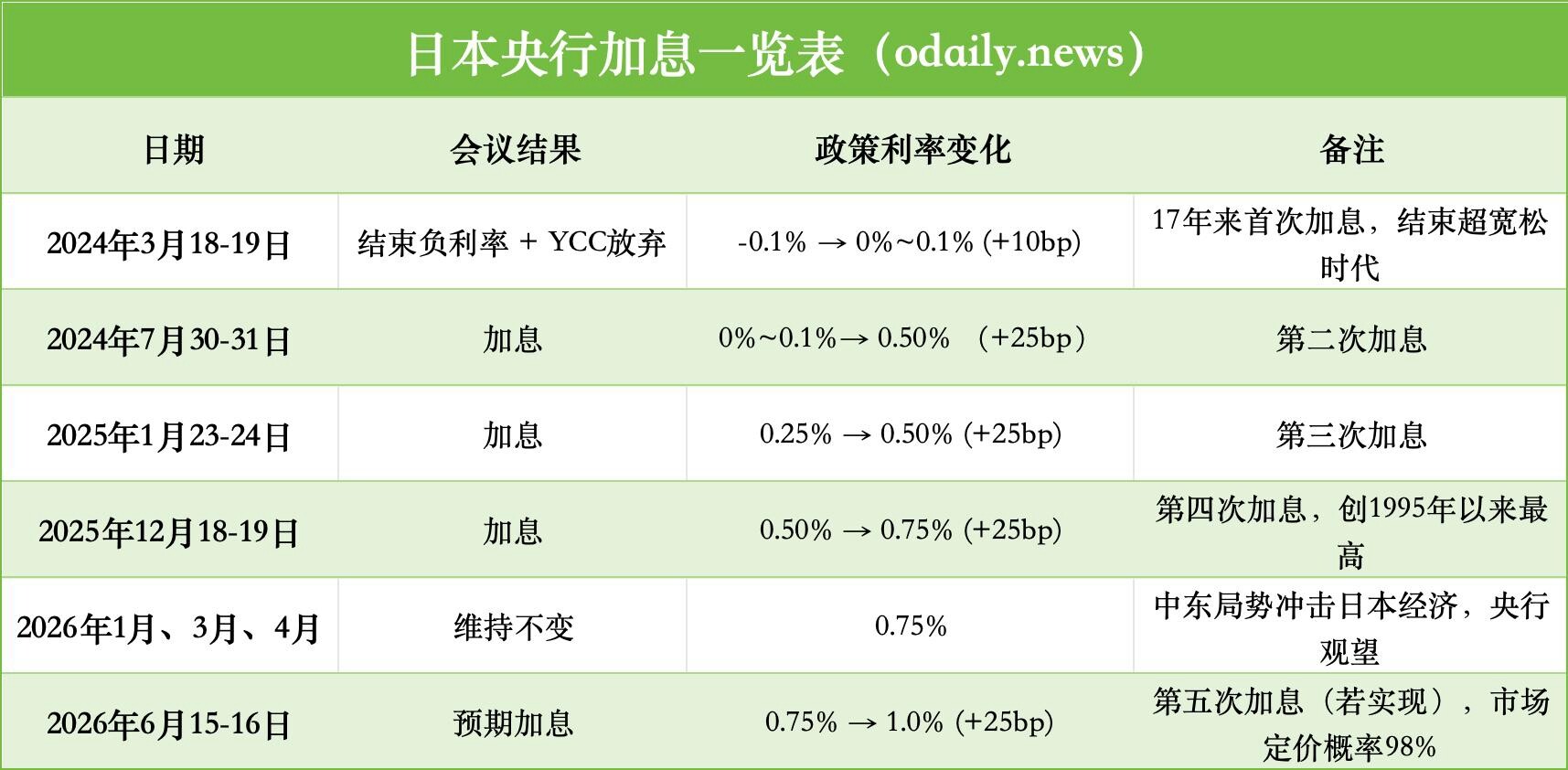

- 일본은행은 6월에 25bp를 인상하여 1.0%에 도달할 것으로 예상되며, 시장은 98%의 확률로 가격에 반영하고 있습니다. 이는 주로 에너지 수입 비용 상승과 엔화 약세로 인한 수입 인플레이션 압력에 기인합니다.

- 엔 캐리 트레이드 미청산 포지션은 여전히 약 5000억 달러에 달하며, 금리 인상은 엔화 강세를 유발하여 투자자들이 위험 자산을 청산하도록 강제하고, 이는 자기 강화적 순환 고리를 형성할 수 있습니다.

- 2024년 8월의 급락은 전형적인 사례입니다: BOJ 금리 인상 후 엔화가 급등하여 닛케이 225가 12.4% 폭락했으며, 비트코인은 하루 최대 15% 하락했습니다.

- 고평가된 AI 기술주는 유동성에 매우 민감하며, BOJ 금리 인상은 자금 조달 비용을 직접적으로 증가시킵니다. Nvidia, Broadcom과 같은 선두 기업 및 Meta, MS와 같은 클라우드 서비스 제공업체는 매도 압력을 받기 쉽습니다.

- 고베타 자산인 암호화폐는 레버리지 포지션 청산 및 AI 기술주와의 유동성 경쟁이라는 이중 압력에 직면해 있습니다. 분석가들은 엔화 강세와 BTC 약세가 고도로 동기화되어 있음을 지적합니다.

Original | Odaily (@OdailyChina)

Author | Qin Xiaofeng (@QinXiaofeng 888 )

According to a Nikkei report, the Bank of Japan (BoJ) is expected to raise its short-term policy rate from 0.75% to 1.0% at its monetary policy meeting on June 15-16, marking the highest policy rate level since 1995. Currently, the market prices a near-certain probability of a rate hike. On PolyMarket, the probability of a "25bp (basis point) rate hike" has surged from 25% in early April to 98%.

With the BoJ rate hike imminent, a large number of investors engaging in yen carry trades may be forced to sell overseas assets, convert back to yen, and repay loans, triggering a chain reaction that amplifies volatility in global risk assets. The flash crash in August 2024 serves as a classic example. At that time, the sharp appreciation of the yen led to a short-term plunge in global stock markets, with Bitcoin dropping nearly $20,000 in a single day, a maximum decline of 15%.

Odaily will analyze the macroeconomic backdrop and transmission mechanism of the BoJ's rate hike, and focus on assessing its risk impact on AI tech stocks and cryptocurrencies for readers' reference.

1. Inflation Risks Drive BoJ Rate Hike

Over the past two years, hawkish voices within the BoJ have strengthened, ultimately leading to the end of its 17-year negative interest rate policy in March 2024, raising the policy rate from -0.1% to a range of 0% ~ 0.1%. This was the first rate hike in the current cycle. In July 2024, the BoJ raised the rate by another 15bp to 0.25%, announcing a gradual reduction of its balance sheet. It subsequently raised rates by 25bp in January and December 2025, bringing the rate to 0.75%. The rate was held steady during the first three meetings of 2026. The following chart shows the BoJ's rate hikes across several meetings:

After maintaining the rate unchanged for half a year, why is the BoJ once again rushing to start a new round of rate hikes? This rate hike primarily stems from two factors.

First, energy shocks and imported inflation pressure. With oil price volatility caused by conflicts in the Middle East in the first half of the year, Japan, a country heavily dependent on imported energy, saw a significant increase in import costs. The Corporate Goods Price Index (CGPI) rose 6.3% year-on-year in May, the fastest pace since 2023, with petroleum product prices up 9.6% and utilities up 8.5%. The BoJ projects the core CPI for fiscal year 2026 to rise to 2.5-3.0%, well above its 2% target.

Second, yen weakness exacerbates imported inflation. The current USD/JPY exchange rate continues to hover near the high range of 158-160, approaching historically extreme weak levels. The significant depreciation of the yen directly weakens the import purchasing power of Japanese companies, leading to a substantial increase in the import costs of energy, raw materials, and other commodities, further pushing up domestic prices. Although Japan's Ministry of Finance has intervened in the foreign exchange market multiple times, the effects have been limited and difficult to sustain. This situation is forcing the BoJ to tighten monetary policy (i.e., raise rates) at its June meeting to prevent inflation expectations from spiraling out of control.

In a speech on June 3, BoJ Governor Kazuo Ueda clearly shifted towards an anti-inflation narrative, emphasizing that if upside risks to prices outweigh downside risks to the economy, the pros and cons of a rate hike must be discussed.

Reuters, citing three sources, reported that unless the Middle East conflict escalates sharply, the BoJ will raise rates in June and may slow the pace of bond tapering to maintain market stability. Bloomberg and institutions like ING maintain similar views, expecting a total of 50bp in rate hikes from the BoJ in 2026.

This series of shifts marks Japan's transition from the "world's last lender" to a normalizing central bank, directly challenging global assets reliant on cheap yen financing.

2. Unwinding of Yen Carry Trades, Continuous Liquidity Tightening

The BoJ's long-term ultra-loose monetary policy has made the yen carry trade a significant component of global liquidity over the past decade. Investors borrow yen near zero interest rates to invest in high-yield assets such as US stocks, tech stocks, emerging markets, and cryptocurrencies, earning interest rate differentials and capital gains.

The BoJ's current rate hike will directly raise the cost of yen financing and may trigger yen appreciation (USD/JPY decline), forcing leveraged investors to unwind positions and creating a positive feedback loop: Yen appreciation leads to larger exchange losses → Rising financing costs → Forced deleveraging by investors → Large-scale selling of risk assets → Further decline in asset prices → Triggering more stop-loss orders → Intensifying unwinding pressure.

Historically, any signal of BoJ policy tightening has triggered significant market volatility.

On July 31, 2024, the BoJ raised rates by 15bp to 0.25% and announced gradual tapering, which, combined with weak US employment data, triggered violent global market turmoil. At that time, both major South Korean stock indices (KOSPI and KOSDAQ) plummeted, triggering circuit breakers. The Japanese stock market crashed, with the Nikkei 225 plunging 12.4% in a single day and accumulating a drop of over 20% in one week, its worst performance since 1987. Global stock markets fell in tandem, with US stocks and tech stocks also adjusting, and the VIX volatility index spiking. Crypto was also heavily impacted, with Bitcoin and ETH plummeting over 30% in just one week, and leverage liquidations surging.

According to estimates by Morgan Stanley, although a large number of positions have been gradually unwound since 2024, an estimated ~$500 billion in open yen-financed positions still exist in the market. While the market has already priced in some risk, these positions still pose significant latent risks. Morgan Stanley warns that if the yen appreciates rapidly, it could trigger a chain of unwinding during periods of thin liquidity, particularly impacting highly leveraged assets.

Dubravko Lakos-Bujas, Head of Global Markets Strategy at J.P. Morgan, and Meera Chandan, Foreign Exchange Strategist, both point out that the policy divergence between the BoJ and the Fed will exacerbate the instability of carry trade unwinding, potentially leading to a valuation reassessment of global risk assets.

3. Global Risk Assets Hit; US Stocks and Crypto Markets Not Spared

The AI-driven tech boom was the main theme for US stocks in the first half of 2026, with chip stocks like Nvidia and Broadcom, along with hyperscale cloud service providers, leading the Nasdaq to repeated record highs.

However, entering June, the market experienced significant rotation and pullbacks. Particularly on June 5, US stocks saw their most severe single-day pullback of 2026. The Nasdaq fell 4.18%, its biggest single-day drop since April 2025; the S&P 500 fell 2.64%, ending a nine-week winning streak; the Dow fell 1.35%, and the Philadelphia Semiconductor Index plunged over 10%, with AI core stocks like Nvidia, Broadcom, Micron, and Marvell leading the decline. (Recommended reading: "Nasdaq Drops 4.2% in a Day, Does 'Black Friday' Pop the US Stock Bubble?")

The US stock pullback is due to both macroeconomic factors like geopolitical tensions and Fed policy uncertainty, but a factor that cannot be ignored is the potential impact of the BoJ's rate hike.

First, liquidity tightening will directly hit high-valuation growth stocks. AI companies have massive capital expenditure needs and are highly dependent on cheap financing. The unwinding of yen carry trades will reduce global risk-seeking capital inflows, with high-beta tech stocks being the first to suffer. Semiconductor leaders like Nvidia and Broadcom, as well as hyperscalers like Meta and Microsoft, are highly sensitive to valuations and are extremely vulnerable to selling pressure. Investing.com analysis points out that high-valuation growth sectors are most sensitive to changes in global liquidity, often experiencing rapid deleveraging once carry trade unwinding begins.

Second, rising energy costs will significantly compress AI profit margins. The Middle East conflict pushes up oil prices, leading to a sharp increase in data center electricity and cooling costs. Combined with the BoJ rate hike, this creates a "stagflationary" macroeconomic environment, severely testing the sustainability of the AI business model.

BitMex founder Arthur Hayes clearly warned in his latest article "Reality Test": "Energy reality is testing the market's current 'dream' state." High oil prices not only raise operating costs but may also slow down corporate token usage growth, further impacting AI-related revenue expectations.

Finally, there is the supply shock from mega IPOs and political/regulatory risks. Giants like SpaceX, Anthropic, and OpenAI plan intensive listings in the second half of 2026 with valuations reaching hundreds of times sales. The expiration of lock-up periods will bring massive supply pressure. Concurrently, Trump may pivot towards an anti-AI stance for the midterm elections, increasing regulatory uncertainty.

Cryptocurrency, as a global high-beta risk asset, is also not in a favorable position. On one hand, the yen rate hike raises financing costs, directly increasing the cost of global leveraged trading and forcing large-scale liquidation of crypto leverage positions. On the other hand, in the competition for liquidity with AI, AI capital expenditure has already absorbed significant market funds, leaving crypto lagging behind. The BoJ's action will further tighten marginal liquidity.

Yahoo Finance analyst Lockridge Okoth stated that the 98% probability of a rate hike could trigger the next liquidity shock for Bitcoin. Investing.com analysis indicates that yen appreciation and BTC weakness are often highly synchronized, serving as a typical signal of rising global risk aversion.

Arthur Hayes has also emphasized in multiple analyses that the dynamics of the yen carry trade remain a key variable affecting Bitcoin liquidity, reminding investors to watch for short-term liquidity shocks caused by policy signals. In a recent article, Arthur Hayes stressed the need to be wary of the combined impact of short-term energy costs and monetary policy risks; BTC/ETH may adjust in line with risk assets in the short term, with their long-term trajectory depending on a liquidity restart.

Conclusion:

The resurgence of concerns over the BoJ rate hike is not an isolated event but a signal of tightening global liquidity on the margin. Especially when combined with other factors like the current Middle East geopolitical conflict pushing up oil prices, AI capital expenditure consuming liquidity, and Fed policy uncertainty, the buffer room is further compressed.

For investors, in the short term, global risk assets, particularly high-leverage and high-valuation sectors (AI tech stocks and cryptocurrencies), may face significant correction pressure, and volatility is likely to rise markedly. Maintaining high vigilance and paying attention to leverage risks is necessary.