Micron’s Long-Term Agreements: Clients Pledge $22 Billion Upfront; Non-Cancellable Contracts Lock in "Most Profitable" Gross Margins in History

- Key Thesis: Through long-term strategic agreements (SCAs) with clients, which involve a combined $22 billion in upfront deposits and locked-in minimum prices and volumes, Micron has transformed from a cyclical storage supplier into a long-term vendor with a high profit floor. This shift is deemed a “game-changer” by three major investment banks, which have unanimously raised their target prices.

- Key Factors:

- SCAs cover approximately 20% of DRAM and one-third of NAND shipments. The minimum committed revenue from 14 signed agreements totals about $100 billion, with final revenue expected to be “significantly higher” than this floor.

- Clients are required to pay a combined $22 billion in deposits ($18 billion in cash + $4 billion in letters of credit). These contracts are non-cancellable, and the deposits raise the cost of default for clients, providing a demand guarantee for Micron.

- The pricing floor embedded in the contract framework corresponds to a gross margin “far above historical peaks” (62%). Currently, Micron’s gross margin stands at 84.9%. Even if the floor price is triggered, profitability levels would still far exceed the best historical periods.

- To fulfill these contracts, Micron has raised its FY26 net capital expenditure guidance to approximately $27 billion. The long-term agreements provide certainty for capacity expansion, though capacity deployment remains a cyclical variable.

- The SCA structure is expected to result in over 50% of the company’s revenue coming from these contracts, with fixed-price or price-range agreements accounting for approximately 40% of revenue, significantly enhancing earnings stability.

Original author: Long Yue

Original source: Wall Street CN

Customers first deposit $22 billion as collateral, sign irrevocable long-term contracts, and accept a pricing framework that is far more favorable to Micron than at any point in its history. These are the core terms of Micron's latest batch of Strategic Customer Agreements (SCAs).

According to information from the Zhui Feng Trading Desk, on June 25, Barclays, Morgan Stanley, and JPMorgan collectively labeled these agreements as "game-changers." JPMorgan semiconductor analyst Harlan Sur characterized these SCAs in a research report as a "fundamental shift" in Micron's business model — transforming it from a cyclical commodity supplier into a long-term provider shielded by multi-year contracts with significant downside protection for both revenue and profits.

The value of these contracts lies in several key aspects: First, the substantial coverage scope — signed agreements correspond to approximately 20% of DRAM volume and about one-third of NAND volume. Second, the binding of price and volume — based on minimum commitment volumes and minimum prices, these 14 agreements represent approximately $100 billion in cumulative minimum revenue. Third, customers must provide a total of $22 billion in deposits and financial commitments. Fourth, the gross margin corresponding to the contract's price floor is "well above historical peaks" (historical peak ~62%), effectively locking in a higher profitability baseline for Micron.

16 Contracts, Covering 20% of DRAM and One-Third of NAND

Micron disclosed that it has signed 16 SCAs, with customers spanning three major markets: data centers, consumer electronics, and automotive.

In terms of customer distribution, there are 4 large customers (the market generally speculates these include hyperscalers and major consumer electronics OEMs), 3 mid-sized customers, and the remaining 9 are smaller customers in the automotive industry.

Contract Duration: Data center and consumer electronics contracts are 5-year terms, covering 2026 to 2030; automotive contracts are 3-year terms.

Coverage Scale: These 16 agreements collectively cover approximately 20% of Micron's DRAM shipments and about one-third of its NAND shipments.

According to a Barclays research report, management indicated that once all planned SCAs are fully executed, it's expected that over 50% of the company's revenue will come from these agreements. Among them, agreements with fixed prices or price ranges are expected to account for approximately 40% of the company's revenue.

$22 Billion Deposits Raise Breach Costs: Customers Pay First, Micron Holds Temporarily, Returns at Maturity

Under the 16 signed agreements, Micron will receive a total of approximately $22 billion in cash deposits and other financial commitments — $18 billion in unrestricted cash and $4 billion in letters of credit.

These funds are held by Micron, remain on the balance sheet during the contract period, and are returned to customers upon contract expiration, with a "back-end weighted" return schedule, meaning the bulk is returned in the latter half of the agreement.

This money cannot be simply viewed as deferred revenue. Its true function is to raise the cost for customers to back out.

Regarding the binding nature of the contracts, a Morgan Stanley research report directly quoted management's statement from the conference call: "These contracts are non-cancellable." If customers fail to take delivery as per the agreed volume and price, Micron can take action against the deposits. For Micron, this effectively adds a safety deposit to a portion of future demand. For customers, it's the cost of commitment paid for supply certainty.

This also explains why customers are willing to accept price ranges and deposit arrangements. Driven by demand from AI servers, data center SSDs, HBM, and high-end end-devices, and when memory supply is tight, locking in volume itself is valuable.

Pricing Structure: Has an Upper Limit, but the Gross Margin Locked by the Price Floor "Far Exceeds Historical Peaks"

The SCA pricing framework falls into three categories: fixed price, price ranges with upper and lower limits, or floating within a close range referenced to the market price.

Regarding the price ceiling: For existing products, the price ceiling is referenced to the market price of the second quarter of 2026. This clause was interpreted by some market participants as Micron "actively capping upside pricing potential," sparking some debate.

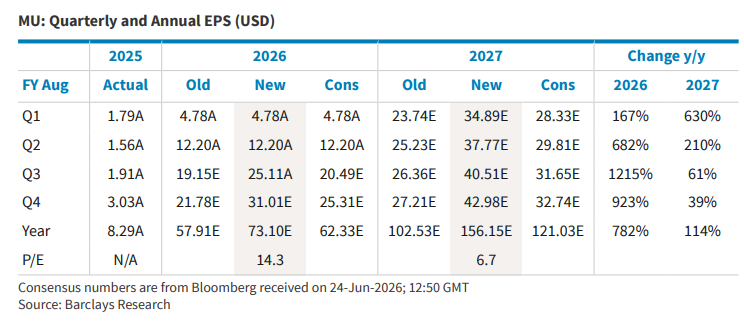

But the price floor is the real highlight: The gross margin corresponding to the floor price is "well above the peak profitability of any historical cycle." Micron's historical gross margin peak was around 62%, while the current gross margin has reached 84.9% — meaning even if the floor price clause is triggered, Micron's profitability level remains far above its best historical period.

However, SCA is not a contract guaranteeing "ever-increasing prices." Some existing products have set price ceilings, with the cap anchored to the market price of Q2 2026. In other words, Micron has traded some future pricing upside for higher revenue certainty and a secure gross margin floor.

Analyst Joseph Moore commented on this, saying that "contract price caps aligning with Q2 prices" indeed raised concerns about the "company capping its upside." But he also pointed out that gross margins are already approaching 90% and are expected to remain in that range for a considerable period — it is reasonable for counterparties to seek some protection in negotiations, and the contract's duration is the core dimension for evaluating its value.

$100 Billion Revenue Floor, and That's Just the "Minimum"

Of the 16 agreements, 14 have clearly defined pricing terms.

According to research reports from Barclays and JPMorgan, the minimum committed revenue (RPO, i.e., remaining performance obligations based on minimum volumes and prices) for these 14 agreements totals approximately $100 billion.

Management explicitly stated that actual revenue is expected to be "significantly higher" than this floor — because this $100 billion is merely the guaranteed baseline calculated at floor prices. If market prices exceed the floor, revenue will naturally increase.

For new products, the agreements also retain additional pricing upside potential.

Scaling Production Required Behind Long-Term Contracts; Capital Expenditure Has Not Disappeared

Locking in demand does not equate to automatic delivery.

Micron has raised its FY26 net capital expenditure guidance to approximately $27 billion, up from around $25 billion. FY27 quarterly capex is expected to be higher than FQ4 levels, with over half of the year-over-year increase coming from construction capital expenditures for pre-investing in cleanroom capacity.

This indicates that SCAs do not lead to an asset-light model, but rather provide a more certain rationale for capacity expansion.

Customers are willing to put down deposits, and Micron needs to invest in capacity. Long-term contracts make expansion more justifiable, but if future demand or prices deviate, capacity deployment could still become a cyclical variable.

Behind the Unanimous Price Target Hikes by Three Major Institutions, the Market Re-evaluates "How Long Peak Profits Can Last"

All three institutions raised their Micron price targets, but the logic extends beyond just the FQ5 quarterly earnings beat.

Barclays (Analyst Tom O'Malley): Raised target from $1,175 to $2,000, based on 12x CY27 EPS of $166.74. The report stated that SCA details were "better than expected," viewing these agreements as "substantively positive for downside protection," while also noting that supply-demand imbalances won't fade in the near term, leaving room for upside.

Morgan Stanley (Analyst Joseph Moore): Raised target from $1,050 to $1,200, based on 30x through-cycle earnings ($40 per share). The report increased the through-cycle earnings estimate from $35 to $40, citing that the run-rate profitability is trending toward $200 per share.

JPMorgan (Analyst Harlan Sur): Significantly raised target from $550 (Dec 2026 target) to $1,540 (Dec 2027 target), based on 10x (median 10-year P/E) FY28 EPS of $154. The report characterized the SCA expansion as a "step-function change," fundamentally altering the nature of Micron's business model.

Underlying these model changes, the key variable is profit sustainability.

Micron's May quarter revenue reached $41.456 billion, up 73.7% quarter-over-quarter; the August quarter revenue guidance midpoint is $50 billion, with non-GAAP EPS guidance midpoint of $31. Quarterly figures are already very high, but the SCAs present the market with another question: If prices stop rising rapidly, can Micron maintain its high gross margins and high free cash flow?

The current framework suggests: A portion of revenue has stronger protection, but not all revenue. Price ceilings, future capacity expansion, and the sustainability of AI demand remain boundary conditions.

Deposits and Cash Flow Open Capital Return Possibilities, But Timing is Constrained

The SCAs also bring about a balance sheet change: deposits come into Micron's hands, and while they must eventually be returned to customers, they will increase the cash balance in the short term.

As of the May quarter, Micron had approximately $26 billion in cash and investments; operating cash flow for the quarter was $25.4 billion, and adjusted free cash flow was $18.3 billion. The August quarter is also expected to receive approximately $10 billion in customer cash deposits.

The path for capital returns is becoming clearer. Restrictions related to the US CHIPS Act limit Micron's short-term share repurchase capacity. After December 9, 2026, as the restriction window passes, the company's tone points towards gradually returning 100% of excess cash to shareholders, with buybacks being the primary method.

This is not a direct revenue contribution from SCAs, but it's another aspect of how SCAs change the market narrative: If high profit levels are sustained and cash accumulates rapidly, Micron may no longer just be a "cyclical profit player" and could transition into a more stable cash return framework.

Earnings Report Itself: Record Gross Margin, Next Quarter Guidance Also Beats Expectations

Beyond the SCAs, Micron's May quarter (FY3Q26) earnings data was also robust:

- Revenue of $41.456 billion, up 73.7% QoQ, significantly beating the market consensus of $35.6 billion

- DRAM revenue of $31.3 billion (+67% QoQ), NAND revenue of $9.9 billion (+99% QoQ)

- DRAM ASP up roughly ~60%+ QoQ, NAND ASP up roughly ~ mid-80% QoQ

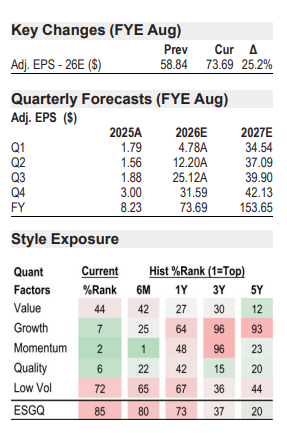

- Gross margin of 84.9%, an all-time high, above market expectations of ~81.8%-81.9%

- EPS of $25.11-$25.12, significantly exceeding market expectations of ~$20.49

August Quarter (FY4Q26) Guidance:

- Revenue guidance of $50 billion (midpoint), above market expectations of ~$43.1-$43.6 billion

- Gross margin guidance ~86%, also above market expectations

- EPS guidance of $31.00 (midpoint), above market expectations of ~$25.31-$25.72