Arthur Hayes New Article: AI Bubble Nears Bursting, Crypto Market Faces Short-Term Headwinds

- Core Thesis: This article posits that the current market is in a "dream state." Rising energy prices will trigger a bursting of the artificial intelligence (AI) stock market bubble, dragging the crypto market down with it. Only after the market clears will Bitcoin be able to bottom out and rebound. The core logic chain is: US-Iran standoff drives up oil prices → inflation intensifies → Trump targets the AI industry for re-election purposes → AI stock market plunges → liquidity contraction causes short-term pressure on Bitcoin.

- Key Elements:

- Oil Price as Core Variable: Global hydrocarbon energy prices are the key to a market reversal. Continued disruption in the Strait of Hormuz will lead to a surge in hydrocarbon energy and basic commodity prices in Q3 2025, impacting the profitability of the AI industry, which relies on cheap energy.

- Triple Headwinds for the AI Industry: Rising energy costs erode profits, blockbuster IPOs from three major companies like SpaceX (with a combined valuation exceeding $1 trillion) absorb market capital, and Trump, to win over swing voters, may introduce anti-AI regulatory and tax hike rhetoric.

- Dollar Liquidity Cornered by the AI Sector: Since the end of 2022, the total debt financing in the AI field has been approximately $1.5 trillion, nearly equaling the increase in US M2 over the same period. This has prevented assets like Bitcoin from receiving liquidity support, causing their price performance to lag behind AI stocks.

- Market Signals vs. Policy Contradictions: The 2-year US Treasury yield is 0.5 percentage points above the federal funds rate, indicating market expectations that the Fed should raise rates to combat inflation. However, the new Fed Chair Kevin Warsh leans towards cutting rates, with policy conflicts increasing market uncertainty.

- Author's Portfolio Adjustment: Based on a mid-to-long-term outlook for rising oil prices, the author has liquidated all AI-related stocks and non-core crypto assets (HYPE, NEAR, WLD, ZEC), retaining only core positions in Bitcoin and Ethereum. The plan also involves using derivatives for short selling to navigate market turbulence.

Original Author: Arthur Hayes

Translation compiled by: Luffy, Foresight News

Is it just my illusion, or has investing in AI really been reduced to subscribing to Citrini Research and blindly buying all its stock recommendations?

Am I dreaming? Or has oil long lost its economic and political influence? That must be why Trump and Iran's Islamic Revolutionary Guard Corps can exchange barbs on social media, while a massive backlog of ships remains stranded in the Strait of Hormuz.

With the two-year US Treasury yield 50 basis points above the effective federal funds rate, releasing such a clear signal, will the Fed really hold steady at its next meeting and refuse to raise rates?

Will all the dividends generated by AI in America truly fall only into the hands of a few tech workers?

This chaotic world forces me to perform a reality check, to confirm whether I'm awake or trapped in a dream. If the test proves it's all an illusion, I will immediately adjust my investment portfolio. This article is my verification process. By the time I finish writing and sorting through my thoughts, my holdings will either undergo a major shift or stay exactly as they are.

Let me state my core judgment first: the current market state feels more like a dream. Within the entire investment system, the price of oil and other hydrocarbon energy sources is the core variable with a reverse-transmission effect. The essence of human perception is converting energy into biological intelligence, and the logic behind AI is no different. This rule will never be broken. The market may deviate from this common sense in the short term, but reality will eventually exact its revenge.

This article will start with oil prices and ultimately end with the US election. The current situation is highly likely to trigger a burst of the AI stock market bubble, dragging the entire crypto market down with it. Only after the dust settles will Bitcoin have a chance to bottom out and rally. I previously asserted that Bitcoin would never touch $60,000 again; clearly, that was a mistake, which is par for the course in market predictions. I always adhere to one principle: have strong opinions, but hold them loosely.

Let's dive into the analysis.

To Negotiate or Not: The Core Dilemma

Politicians always act in their own self-interest. The reasons behind Trump's unprovoked military action against Iran are likely known only to him. Facing a barrage of statements from him and his advisors at every moment, it's impossible for outsiders to discern the truth. At this point, dwelling on the cause is pointless. The real questions are whether Trump and Iran's Islamic Revolutionary Guard Corps will choose a ceasefire and how the standoff will end.

This conflict is now entirely orchestrated by Trump. For him and the Republican party, initiating a war in an election year is undoubtedly a difficult position.

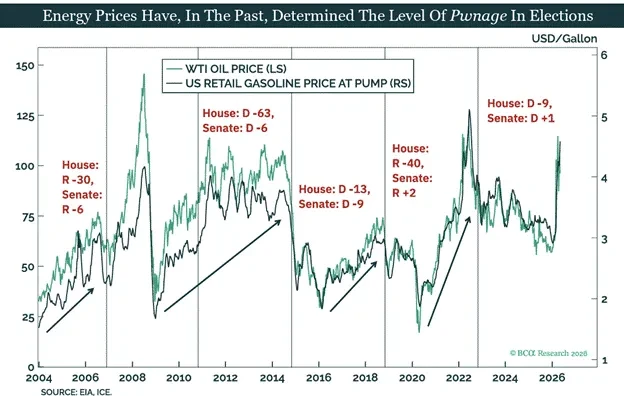

In America, the prices of essential goods like gasoline and food often directly determine election outcomes. With traffic through the Strait of Hormuz blocked, energy and food inflation continues to rise, all stemming from the Trump administration's unilateral action against Iran without public consent. Some might point fingers at Israel, but that argument doesn't hold water. Anyone familiar with US history understands that domestic forces won't follow external orders.

The American public doesn't generally oppose foreign wars, as long as their own lives aren't affected and they don't suffer personal losses. Trump has repeatedly emphasized that only thirteen US soldiers have died in this special military operation. This is also why the US favors using sophisticated long-range precision weapons and engaging in "video game warfare." Even though launching this Middle Eastern conflict lacks a clear winning strategy and defies the expectations of many supporters, the base still stands by the Republican party. This is confirmed by the fact that some Republican lawmakers who wavered in their stance faced pressure from Trump's inner circle and lost their primaries.

Trump's core vulnerability isn't that his base won't vote in November, but that soaring prices will push a large number of swing voters towards the Democrats. The cost of living has become the single biggest issue threatening Trump's electoral chances.

To win over swing voters, Trump must at least stabilize current oil prices. With the supply chain just beginning to absorb the price increases of energy and various production inputs, completely curbing inflation is already unrealistic. What Trump can do now is manage market expectations for inflation, not change inflation itself.

Whether Trump is willing to reach a deal with Iran depends entirely on oil prices. As oil prices climb, his rhetoric will soften; but if the market anticipates upcoming negotiations and oil prices fall, he will harden his stance again. After all, from a geopolitical perspective, any agreement reached through such talks would likely be more disadvantageous than the one the Obama administration signed with Iran. For many voters, this would be seen as a "defeat," costing the Republican party at the polls.

Negotiations always require concessions from both sides, and the Iranian Revolutionary Guard Corps has similar considerations. If oil prices are too high, its major trading partners will pressure Iran to compromise with the US; but once Iran signals a willingness to negotiate and oil prices drop, the pressure from those partners will ease.

At current oil price levels, neither the US nor Iran has a strong incentive to back down. While oil prices are significantly higher than before the conflict, they haven't yet triggered a full-blown crisis. The commodity markets are relatively stable, there's no global famine, and most countries can source critical industrial materials from alternative channels.

However, this delicate balance cannot last forever. A significant reduction in global core energy supply without a corresponding price surge defies market logic. Once global spare production capacity is exhausted, spot prices will inevitably skyrocket – a consensus among many commodity analysts. The crisis hasn't fully materialized yet only because global energy inventories were substantial before the conflict began.

If the US-Iran standoff persists until the end of the second quarter, spot prices for hydrocarbons and various basic commodities will experience a sharp surge in the third quarter.

To paraphrase Churchill: Politicians will eventually make the right decision, but only after exhausting all other options. Only when the situation spirals completely out of control will Trump and Iran truly come to the negotiating table. In my view, the disruption to shipping through the Strait of Hormuz will likely last until early Q3.

Let's assume oil prices will trend upwards amidst volatility. In this context, how will rising oil prices interact with Trump's campaign rhetoric?

November Election Showdown: Republicans vs. Democrats

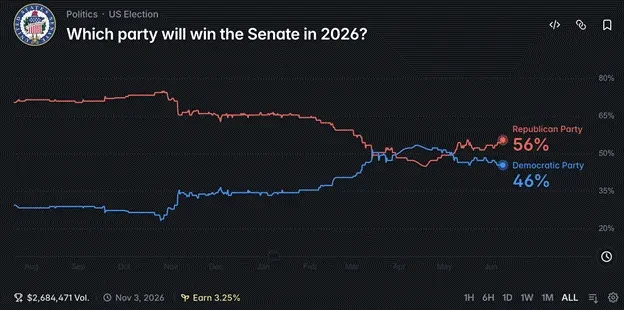

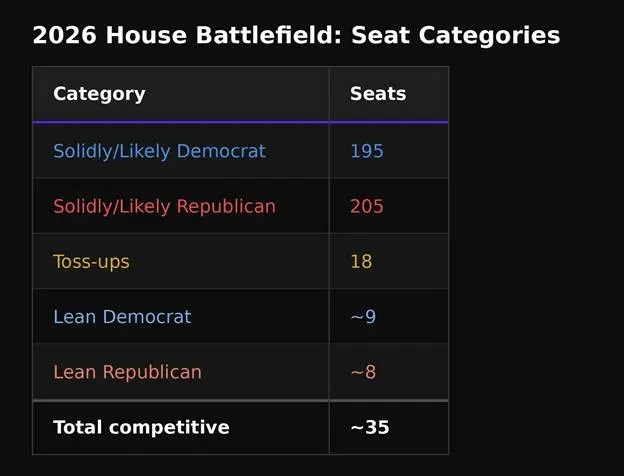

According to the odds on the prediction market Polymarket, the Republican party can currently only hold onto the Senate by a narrow margin, while facing significant losses in the House of Representatives.

There is a general consensus that the Republicans will lose the House, but I hold a different view. Trump still has a chance to turn things around. The key lies in shifting the narrative, specifically by targeting data center construction and the AI industry with regulatory and tax-related statements.

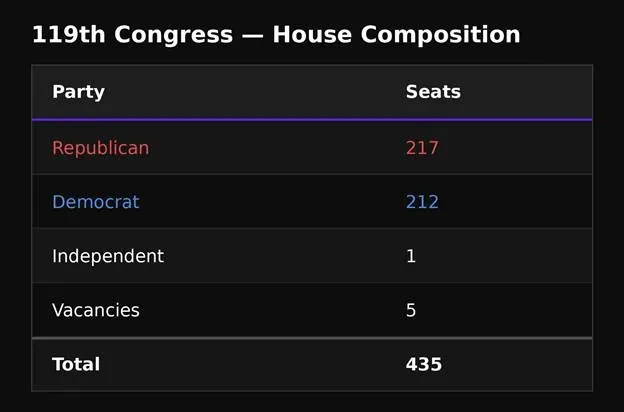

The current seat distribution between the parties is as follows (218 votes are needed to pass a bill):

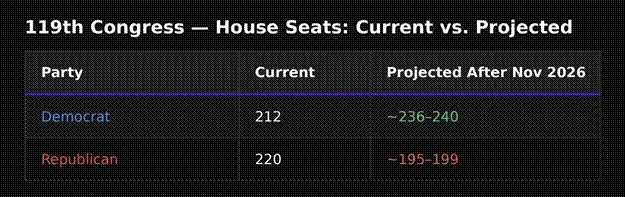

Based on current Polymarket odds, here is the projected party composition after the election:

The post-election outlook for Republican seats in both chambers isn't great. However, the GOP can try to change the situation through redistricting. When the existing rules guarantee defeat, changing the rules becomes inevitable. Assuming Polymarket's predictions are correct, the Republicans need to gain 19 seats. Redistricting could reduce this number.

Here are the potential impacts of redistricting:

Now the Republicans need only 11 more seats. Next, let's look at competitive districts. Based on current polling, which districts might lean slightly Republican within the margin of error?

There are 35 seats with significant uncertainty. As mentioned earlier, high inflation and rising living costs are difficult negative issues for Trump to overcome. Another topic capable of galvanizing voters across both parties right now is data center expansion and the impact of AI on the job market.

Almost everyone, except the ultra-wealthy, is worried about data centers driving up costs and afraid of AI taking their jobs. Many regions have already implemented policies to pause new data center projects, and calls for higher taxes on AI companies to subsidize ordinary citizens are growing louder. After all, the vast majority of people are not AI executives or highly paid tech workers.

For voters in competitive districts, these issues are highly influential. Trump could secure the remaining crucial seats by taking a strong stance on the AI industry. At this stage, he only needs to signal his intentions, no need for actual legislation. He simply needs to promise the general public that if the GOP wins, it will crack down on the AI industry after the election.

As an experienced politician, Trump is adept at making campaign promises he seldom fulfills. His handling of the Epstein-related files is a classic example: he loudly vowed to thoroughly investigate those involved during the campaign but only released a small amount of documents after taking office. He could use the same playbook now: campaign on a platform to slow data center expansion and impose a windfall profit tax on AI companies, using the revenue for a new round of stimulus checks; after the election, with the GOP in power, he can gradually walk back these positions.

Some might find it hard to see Trump adopting policies reminiscent of left-wing Democrats. But remember, he launched the largest universal relief program since the New Deal, without restricting how recipients spent the money. To secure his political position, temporarily distancing himself from AI giants like Elon Musk and portraying himself as a champion of the common person wouldn't be a difficult feat for Trump.

If Trump were to actually issue tough rhetoric against the AI industry, the market wouldn't just see it as a campaign tactic. It would interpret it as a signal that the US is serious about limiting capital expansion in AI and increasing the tax burden on the sector. Panic would spread instantly, and the AI stock bubble would burst.

We saw a preview of market sensitivity recently when Elon Musk and Trump publicly bickered on social media. After departments linked to Musk publicly questioned Trump, threatening to cancel related government contracts, Tesla's stock fell 18% in a single day. Politics can nurture an industry, but it can also deliver a swift blow.

That quarrel was later revealed to be a staged PR stunt; the two quickly reconciled, and Musk was even invited to attend a recent summit between Trump and the Chinese leader in Beijing. Yet, at the time, the market took it seriously, triggering widespread selling.

And that was just a tremor from a personal dispute. If Trump, representing the Republican party, clearly states a plan to heavily tax businesses related to AI models and agents, the impact would be far greater. When similar rhetoric emerged from South Korean political circles, the local benchmark index nearly hit the daily limit the next day, only recovering after an official denial. Markets are that sensitive.

The current optimistic outlook for the AI sector is built on the belief that industry revenue will continue to grow exponentially, without public backlash against new technology and wealth concentration. This notion is disconnected from reality, more like a dream. Trump's statement could be the reality check that pops the bubble. Whether he actually pulls the trigger still depends fundamentally on oil prices.

The longer the Iran situation pushes oil prices higher, exacerbating inflation, the fewer options Trump will have for campaign messaging, eventually forcing him to target data centers and the AI industry.

Trump's strong desire to prevent Democrats from controlling the House is clear. If Democrats take the House, they can use their subpoena power to repeatedly call Trump, his family, and his top advisors to testify, posing difficult questions. If the Democrats also win the White House in 2028, a Justice Department armed with ample evidence could pursue a reckoning, investigating Trump's business entities.

Let's trace the logical chain: The prolonged US-Iran impasse pushes oil higher; rising prices anger voters; Trump must court voters by regulating and taxing the AI industry.

From now until the November election, even a 50% crash in AI-related stocks is an acceptable price for Trump to pay to escape endless Democratic investigations. After the election, he can easily reverse his previous stance on data centers and AI, allowing the industry to recover. The S&P 500 could even target the 10,000 mark.

But for investors, market movements are interconnected. A crash in the AI sector would fundamentally alter market expectations for its future returns. After experiencing the shock of regulation and heavy taxes, investors will never blindly favor this sector the way they did before.

California Dreamin': Where Does Liquidity Flow?

Before analyzing the impact of the potential IPOs of three giants – SpaceX, Anthropic, and OpenAI – on global financial markets, let me first address a puzzle: Since late Q3 last year, dollar liquidity has been easing, yet Bitcoin hasn't rallied correspondingly. Why?

On November 30, 2022, ChatGPT was launched for the public, kicking off the AI super-bubble. Almost simultaneously, the scandal of FTX founder SBF misappropriating user funds was fully exposed. Bitcoin bottomed around $15,000 that year and rallied to $125,000 by October 2025, a gain of over six times. But over the same period, Nvidia's stock rose eleven-fold, and numerous small-to-mid-cap tech stocks converting electricity into intelligence via computing power also skyrocketed. The AI sector's returns far outpaced the crypto market, and the gap has only widened since late 2024.

Even at Bitcoin's (white) all-time high, Nvidia (gold) still delivers superior returns

Bitcoin (white) has performed worse after its all-time high, now down 50%. Nvidia (gold), the world's most valuable company since late 2025, is still up 10%

Based on my previous logic linking crypto markets to fiat liquidity, Bitcoin should have seen stronger gains in the current environment. The reality is the opposite. Where did I go wrong?

I used to focus on the total amount of fiat issuance, ignoring the specific direction of fund flows. I assumed liquidity would eventually find its way into Bitcoin, pushing prices up. This time, my judgment was off.

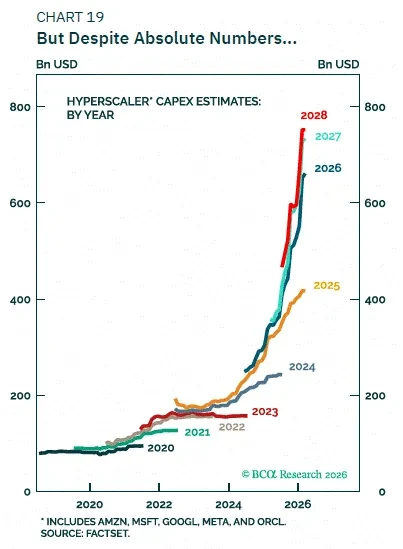

My conclusion is: the newly created dollar liquidity has been almost entirely absorbed by the AI sector. AI is a highly capital-intensive industry. Building the massive data centers needed to run AI requires enormous amounts of energy. Hydrocarbons, nuclear power, and renewables are converted into electricity, which feeds data centers, where specialized chips perform model training and inference computations.

Global capital expenditures for data centers began surging in 2024, accelerating further in 2025. The industry's financing needs exploded correspondingly. Aggregating disclosed data, total debt financing in AI-related fields since November 2022 has reached $1.5 trillion. Over the same period, the increase in the US broad money supply (M2) was also exactly $1.5 trillion. The answer is clear: all the newly created dollars flowed into the AI sector, leaving Bitcoin with no incremental capital.

Bitcoin managed a strong rebound from the FTX bankruptcy low in 2022 only because the massive debt-financed expansion in AI was concentrated after 2025. Of that $1.5 trillion in debt, $1.3 trillion was generated from 2025 onwards. Coincidentally, Bitcoin's price peak occurred in October 2025, precisely when AI capital expenditures reached unprecedented levels.

This linkage is crucial. If the AI stock market crashes, there will be no spare capital left to allocate to Bitcoin. Banks will tighten lending, and many institutions will discover that loans issued based on inflated revenue figures carry significant risks. When the