Crypto CEXs Rush to Sell US Stocks, Traditional Brokers Face Unexpected Guests

- Core Viewpoint: Crypto exchanges are actively entering the US stock market business to address their own traffic challenges and capture the overflow demand for US equities. Binance's "direct broker connection" and Bitget's "tokenization" are two primary paths. The latter, by improving capital efficiency and enabling 7x24 trading, aims to compete with traditional brokers for the pricing power of major global assets.

- Key Elements:

- Demand for traditional US stocks is strong, but non-US investors are constrained by regulations and costs. Crypto CEXs are entering the space through tokenization or direct broker connections, attempting to solve early pain points such as real liquidity, slippage, and asset rights.

- Binance's model provides real US stock trading through introducing brokers and the Alpaca broker infrastructure. It offers broad asset coverage but lacks deep integration into its ecosystem, resulting in lower capital efficiency for users.

- Bitget's model issues 1:1 on-chain certificates (rToken), also accessing real US stock liquidity, while supporting 7x24 trading, use as contract margin, and staking/lending, thereby enhancing capital efficiency.

- Tokenized US stocks rely on market makers for liquidity during non-trading hours or extreme market conditions, which may lead to price volatility; products need to prove custody transparency and properly handle corporate actions such as dividends and stock splits.

- The core advantages of crypto CEXs lie in capital efficiency and ecosystem extensibility, enabling shared margin between stocks, stablecoins, and crypto assets; challenges lie in product experience and regulatory boundaries.

- The long-term trend is the convergence of traditional finance and crypto finance, potentially forming multi-asset financial platforms. Tokenized US stocks represent a significant step for crypto exchanges in beginning to compete with traditional institutions for global pricing power.

Author: momo, ChainCatcher

Selling US stocks has become a top priority for crypto CEXs.

On one hand, the spillover demand from US stocks is simply too tempting. With the US stock market remaining hot in recent years, investors outside the US have a high demand for star assets like Nvidia and upcoming IPOs such as SpaceX and OpenAI. Traditional brokers, constrained by regulatory uncertainty and compliance costs, struggle to efficiently capture this global investor traffic. However, as the SEC approved Nasdaq's pilot for tokenized stock trading, allowing Wall Street to experiment with tokenization, it has become possible for crypto CEXs to enter the US stock market.

But on the other hand, this surge also exposes the crypto CEXs' own traffic struggles. The hotter US stocks get, the colder the crypto market becomes, with no strong catalyst in sight to turn the tide in the short term.

Yet, the crypto industry has never been decided during boom times; it always reshuffles during crises and turning points. The worst of times often become the best of times for crypto CEXs. The major regulatory crackdown of 94 solidified Binance's dominance, and today, the US stock business might just become the new watershed for crypto CEXs.

Looking at the recent acceleration of US stock expansion, there are mainly two paths: "directly connecting to traditional brokers" and persisting with "stock tokenization." This article uses Binance and Bitget as representatives of these two paths, comparing their similarities and differences across a dozen detailed dimensions, and explores whether this move by crypto CEXs can eat into the traditional brokers' pie.

I. Why Were Crypto CEXs' Previous US Stock Products Lukewarm?

Before the formal comparison, let's briefly explain why, after most major exchanges launched US stock products last year, CEXs are now collectively introducing new US stock offerings.

The previous wave of US stock products mostly came in two forms: one was Contracts for Difference (CFDs), where users traded stock price movements without actually holding the underlying stocks; the other was integrating with RWA/tokenization issuance platforms like Ondo, packaging US stock exposure into on-chain assets and then placing them within the exchange's interface.

These two methods solved the problem of "having it," but didn't fully resolve the issue of "it being good to use."

CFDs are more like trading tools, suitable for short-term directional bets, but far removed from real stock assets; early tokenized stocks, based on actual user experience, also had many pain points.

First, concerns about whether the underlying assets were actually real US stocks and their liquidity were the biggest worries for users. Additionally, there were many experiential issues. Bitget CEO Gracy Chen, when discussing the new generation of tokenized US stock products, mentioned several pain points most frequently reported by users with the previous generation. For example, excessive slippage on large orders, making the trading experience feel more like trading an illiquid on-chain asset rather than buying blue-chip stocks; dividend distribution was not smooth, with weak synchronization on the token side after the underlying stock paid dividends; and corporate actions like stock splits and reverse splits often confused users regarding price and position mapping.

Another issue was capital efficiency. Early tokenized US stocks were mostly just "tradable assets." After buying, users could mostly only hold them and wait for price movements, making it difficult to use them as margin for futures or unified accounts, or integrate them into exchange ecosystems like wealth management and lending. For crypto users, this weakened the composability and capital efficiency that tokenization is supposed to offer.

The recent CEX US stock solutions are essentially improvements centered around these pain points. The new moves by Binance and Bitget represent two different paths. The former leans more towards directly connecting with brokers and trading real stocks, while the latter attempts, through Reality/rToken, to integrate real US stock liquidity, tokenized mapping, and the exchange ecosystem.

Next, we'll compare the details of the two solutions across several dimensions where users have experienced pain points.

II. Two New Paths for US Stocks: Direct Broker Connection vs. Persisting with Tokenization

1. Product Underlying: What Exactly Are Users Buying?

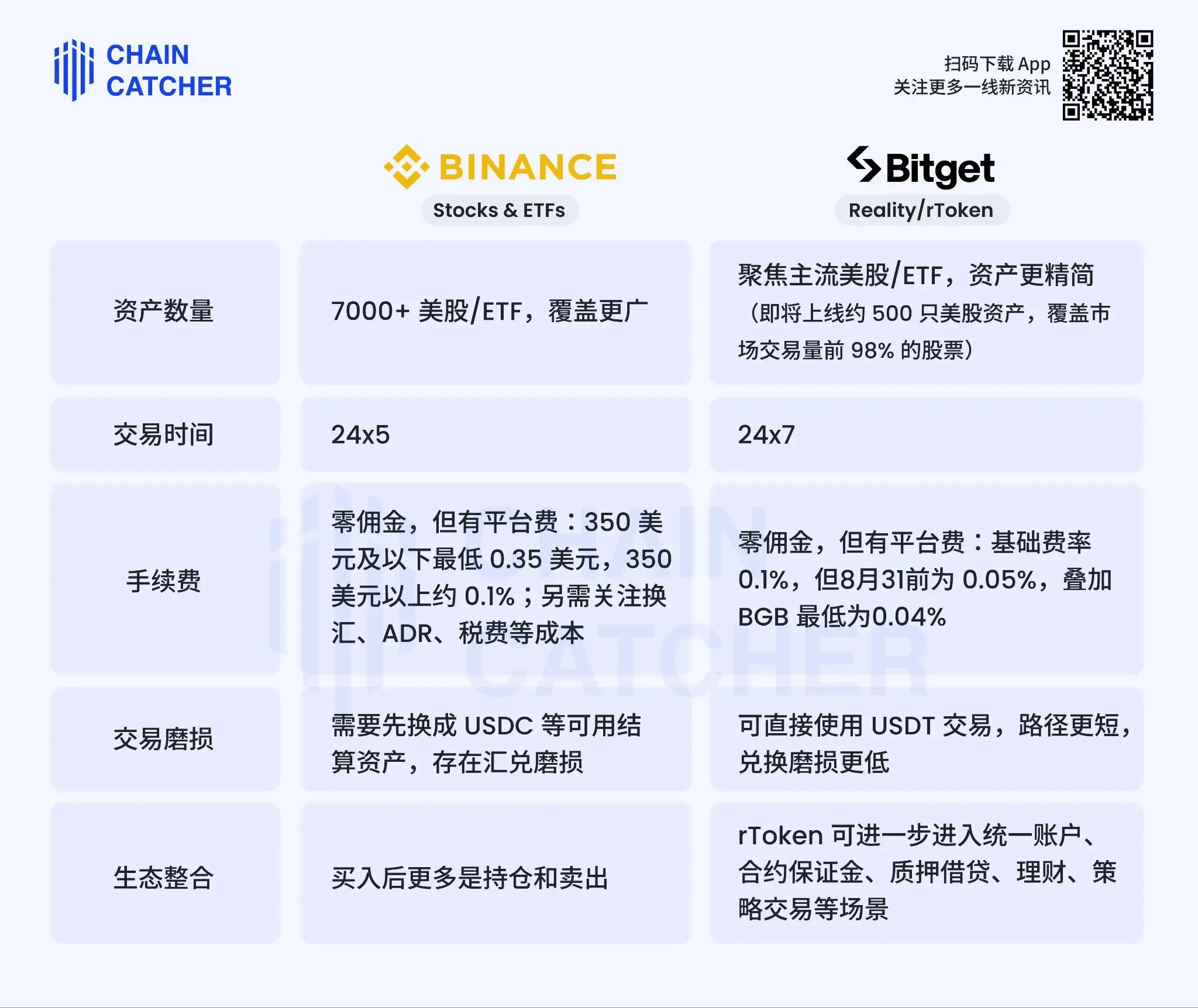

Both Binance's and Bitget's new products have fundamentally solved the issue of directly connecting to US stock liquidity, and both utilize the underlying custodian Alpaca to achieve this. Alpaca is a compliant US stock brokerage infrastructure, and its backend currently supports other key tokenization players like Ondo Finance, Dinari, and xStocks.

Specifically, Binance takes the "broker entry" route. The US stock business order flow is handled by introducing broker Nest Trading, with the backend connected to Alpaca for execution, clearing, and custody.

Bitget, on the other hand, takes the "tokenization" route. Users hold rToken, but orders are executed directly on the US stock market via Reality's on-chain desk. The underlying stocks are custodied by Alpaca, with rToken serving as a 1:1 on-chain certificate. Therefore, the price and depth of rToken are not matched internally on the platform but are connected to real US stock liquidity.

But since rToken is not a stock directly held in a user's traditional brokerage account, where does the security guarantee for this tokenized certificate come from? Currently, Bitget's official response states that three layers of protection are provided through custody by a licensed broker, independent asset segregation, and real-time reserve proof.

Regarding CRS, Bitget's rToken currently does not involve CRS at the traditional brokerage account level. Binance's path is closer to a broker and may be subject to regulatory implications in the future.

In summary, both have solved the question of "are they real US stock assets." Binance is more like a broker entry point, while Bitget tokenizes real assets and places them within the on-chain ecosystem, emphasizing on-chain attributes and capital efficiency.

2. Asset Rights: Besides Price Movements, What Else Do You Get?

For users, buying US stocks is not just about price appreciation and depreciation; it also involves a range of rights and corporate actions like dividends, dividend taxes, stock splits, reverse splits, mergers & acquisitions, delistings, and voting rights. The closer a product is to a real stock, the less these details can be ambiguous.

Based on public information, the latest solutions from Binance and Bitget are no longer merely allowing users to trade a US stock price symbol; both are actively supplementing the fundamental economic rights associated with real US stocks.

Corporate actions like dividend distribution, dividend taxes, stock splits, and reverse splits inherently rely on underlying brokerage infrastructure like Alpaca for processing. Therefore, on these basic rights, the direction of both is similar. Whenever the underlying US stock pays a dividend or undergoes a corporate action, the platform needs to synchronize the corresponding result to the user's account.

The difference lies in the method of realization. Binance reflects it more within the US stock account, while Bitget maps it to the token side via Reality/rToken. Stock dividends are distributed 1:1 in real-time to the account in token form, and cash dividends are automatically converted to USDT and directly credited to the account.

Voting rights are not a major differentiator either. Whether it's the broker entry model or the rToken model, under the structure of non-US users, fragmented holdings, and platform nominee holdings, users typically do not directly enjoy shareholder voting rights in listed companies. Voting rights are not a core selling point for these types of products.

The advantage of Bitget's tokenization approach is that while it can achieve everything a direct broker connection can in terms of stock rights, it goes a step further. It enables stock rights to become a highly efficient transferable asset once they enter the CEX ecosystem.

3. Trading Experience and Capital Efficiency

Let's look at the overall trading experience and asset efficiency.

In terms of asset variety, Binance offers broader coverage. Bitget focuses on major stocks, soon to cover 500 US stocks accounting for the top 98% of market trading volume, emphasizing selectivity and liquidity coverage.

Regarding trading hours, Binance largely follows traditional US stock market hours. Bitget, through tokenization, enables 7x24 trading, which aligns more closely with crypto user habits.

One might ask, where does liquidity come from when the US market is closed? Bitget's CEO responded on Twitter that it is provided by third-party market makers who hold spot inventory to fulfill buy and sell orders. This means liquidity during non-US market hours is not infinite. Under extreme market conditions or heavy one-sided buying over the weekend, the price could be pushed up, potentially leading to significant fluctuations when the market opens on Monday.

In terms of fees, Bitget currently appears relatively lower. Both offer zero commissions, but Bitget has a platform fee. The base rate is 0.1%, but before August 31 it is 0.05%, and with BGB staking, it can go as low as 0.04%, making it more friendly for high-frequency traders.

Regarding transaction friction, when Binance settles with USDC, users holding USDT need an additional conversion. Bitget directly uses USDT, resulting in a shorter path.

The most significant difference lies in ecosystem integration. Binance's current US stock product is not deeply integrated with its ecosystem. In contrast, Bitget's rToken can enter the unified account system, serving as margin for futures, collateral for lending, etc., thereby improving capital efficiency. It currently supports 15 stock tokens, including Nvidia and Micron, for use as futures margin.

Finally, let's summarize the pros and cons of the two paths.

Binance's direct broker connection model's biggest advantage is that it brings users closer to traditional US stock trading. The underlying assets are real US stocks, liquidity comes from the real US stock market, and asset coverage is broader. It also inspires more trust from users without crypto trading experience. However, the problem lies in its relative simplicity, as user capital efficiency is not fully utilized.

Bitget's tokenization model's advantage is that it captures the core benefits of a direct broker connection—namely liquidity and dividend distribution. Building on this, Bitget further enhances capital efficiency, allowing users 7x24 trading, enabling tokenized stock assets to be used as futures margin and in more trading scenarios, all while offering lower fees. However, for some more cautious users, direct stock ownership may feel safer than tokens. Yet, it is expected that as Bitget continues to refine the user experience for these tokenized US stocks, user concerns will gradually diminish.

III. Can Crypto Exchanges Eat into the Traditional Brokers' Pie?

US stock trading has never been just a competition among crypto CEXs. In the long run, crypto CEXs will still have to face competition from traditional brokers.

1. Crypto CEXs Selling US Stocks: Specific Advantages and Challenges

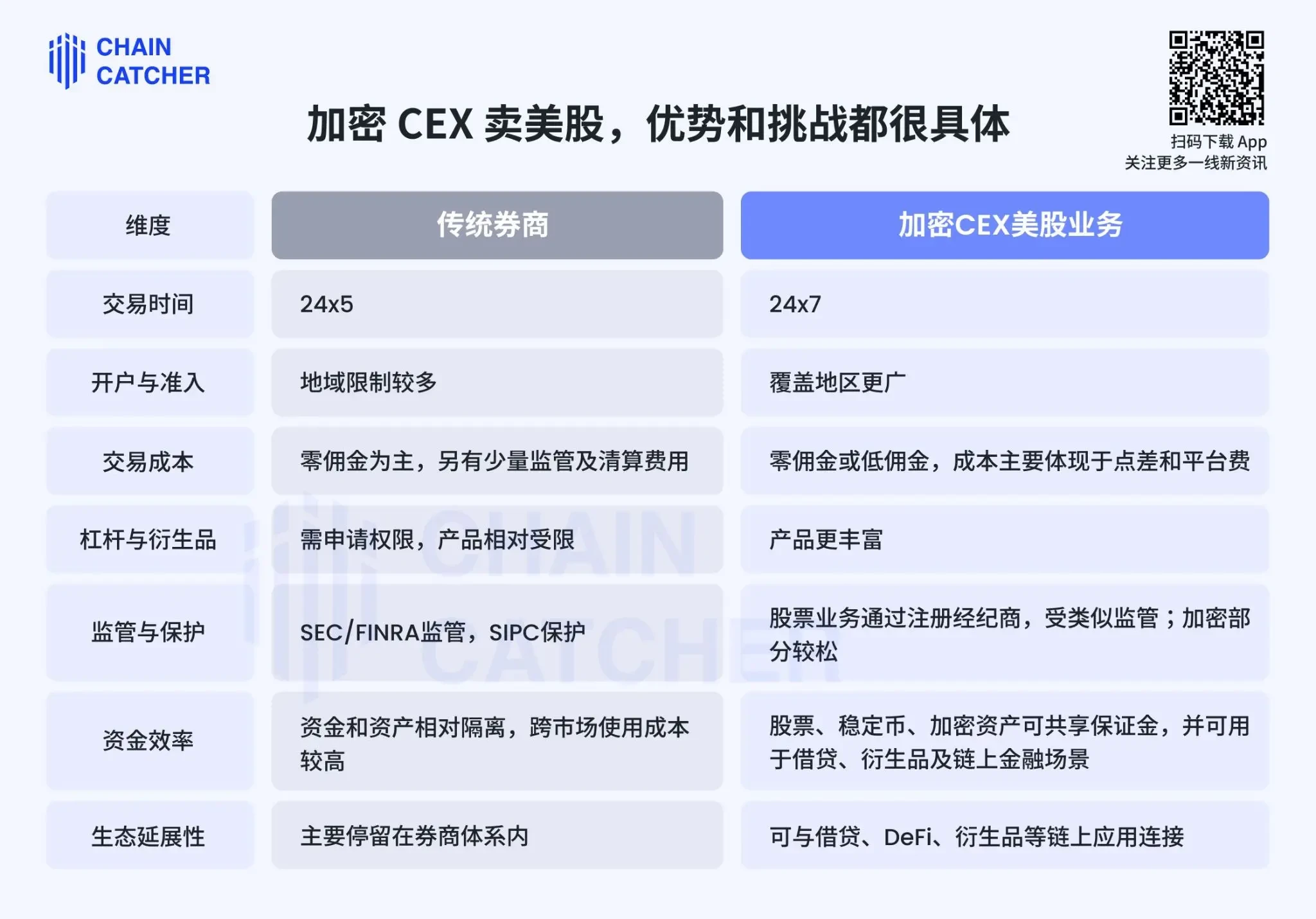

Looking at several key dimensions, the advantages of crypto CEXs over traditional brokers lie in these areas: Trading hours, where crypto CEXs can achieve 24/7 trading through tokenization, better meeting investor demands. In account opening and access, traditional brokers have more geographical restrictions, whereas crypto CEXs offer broader coverage.

However, the most core advantage is capital efficiency and ecosystem extensibility. In traditional brokerage accounts, stock funds are relatively segregated from other assets, making cross-market usage costly. Crypto CEXs allow stocks, stablecoins, and crypto assets to share margin, and can be used in lending, derivatives, and on-chain financial scenarios. This is likely why Bitget persists with the tokenization path—bringing US stocks on-chain, turning them into 7x24 tradable, collateralizable, and reusable assets. This is currently the strongest core competency distinguishing it from traditional brokers.

Of course, the challenges are also specific. The closer a product gets to the real stock market, the more users' demands on the CEX approach those for traditional financial products. Platforms must prove the underlying stocks actually exist, ensure custody and reserves are transparent, and handle details like dividends, stock splits, taxes, and liquidity properly. Especially for tokenized products, price stability and sufficient liquidity during non-trading hours or extreme market conditions will directly determine user trust.

2. The Endgame May Not Be About Replacing, But About Moving Towards Universal Exchanges

Currently, the larger trend is that traditional finance and crypto finance are moving towards each other.

On one side, crypto CEXs are no longer content with just crypto-to-crypto trading. Binance has already directly connected to a broker for US stocks, while Bitget has clearly articulated its strategy as a Universal Exchange (UEX), aiming to place stocks, gold, forex, and crypto assets into a single account. On the other side, traditional platforms are also embracing tokenization. Brokers like Robinhood![]()

![]()

![]()

![]()

![]()

![]()

![]()

![]()